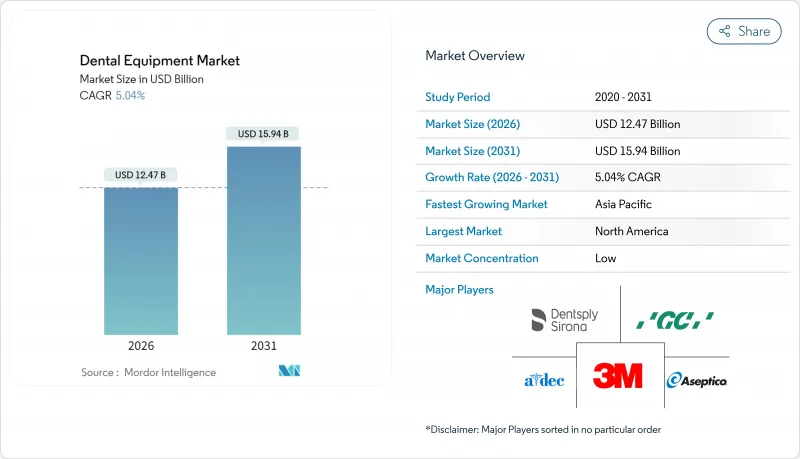

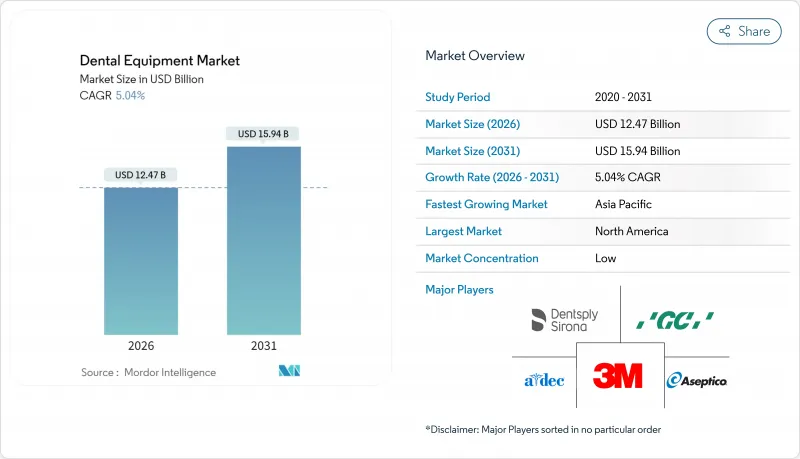

치과 장비 시장은 2025년 118억 7,000만 달러로 평가되었고, 2026년에는 124억 7,000만 달러로 성장할 것으로 예측됩니다. 2026-2031년에 걸쳐 CAGR 5.04%로 성장할 것으로 보이며, 2031년까지 159억 4,000만 달러에 이를 전망입니다.

디지털 이미징, 인공지능(AI), 체어사이드 제조 기술의 도입으로 시술 시간이 단축되고 진단 정확도가 향상되며 환자 수용률이 증가하고 있습니다. 치아 우식증 및 치주 질환 발생률 증가, 선택적 미용 시술의 꾸준한 성장, 높은 강도와 자연스러운 심미성을 겸비한 수복 재료의 강력한 파이프라인이 수요를 더욱 뒷받침하고 있습니다. 대형 제조사 간 통합은 연구, 조달, 세계의 유통에서 규모의 경제를 창출하는 반면, 신규 진입업체들은 AI 기반 영상 분석, 로봇 수술 보조 장치, 바이오세라믹 임플란트 등 좁은 전문 분야에 집중하고 있습니다. 치과 관광과 디지털 방사선 촬영에 대한 정부 인센티브로 부양된 아시아태평양 지역 클리닉들은 첨단 시스템을 대량 구매하고 비용 효율적인 치료를 제공함으로써 경쟁 구도를 재편하고 있습니다. 동시에 강화된 감염 관리 규정은 멸균 장비, 기구 추적 시스템, 오토클레이브 업그레이드에 대한 지속적 투자를 촉진하고 있습니다.

세계의 역학 연구에 따르면, 특히 신흥 경제국의 고령층과 어린이를 중심으로 치료되지 않은 충치와 잇몸 감염이 지속적으로 증가하고 있습니다. 이에 따른 임상 업무량은 기본 수복 재료, 근관 치료 파일, 치주 치료 기구에 대한 수요를 유지시키고 있습니다. 인도 및 인도네시아의 국가 구강 건강 캠페인은 더 많은 초진 환자를 진료소로 유입시켜 정기 예방 치료량을 확대하고 예방 페이스트 및 실런트 판매를 촉진하고 있습니다. 이러한 증가하는 예방 치료 수요는 간접적으로 치과 장비 시장을 강화합니다.

콘빔 CT 및 구강 내 영상 플랫폼에 통합된 AI 알고리즘은 미세한 병변을 표시하고, 골 수준을 정량화하며, 치과 의사가 진료 중 공유할 수 있는 치료 계획을 자동 생성합니다. 초기 도입자들은 AI 시각 자료가 설명과 함께 제공될 때 치료 수락률이 10-20% 증가한다고 보고하며, 이는 중형 치과 진료소 전반에 걸쳐 업그레이드 사이클을 촉발하고 있습니다. 오버젯(Overjet)의 규제 승인을 받은 소프트웨어는 현재 매월 수백만 장의 방사선 사진을 처리하며, AI 진단의 급속한 정착을 시사하고 치과 장비 시장을 강화하고 있습니다.

보험사는 레이저 치은 수술과 충치 제거를 '선택적 치료'로 분류하는 경향이 있으며, 회복 기간 단축 및 임상 결과 개선에도 불구하고 도입 속도를 늦추고 있습니다. 제조업체들은 보험 적용 범위 내에서 치료가 가능하도록 치과 의사가 기존 방식과 레이저 모드 간 전환이 가능한 하이브리드 장치를 출시하며 대응하고 있습니다.

치과 소모품은 진료 시마다 반복적으로 사용됨에 따라 2025년 치과 장비 시장의 43.12%를 차지했습니다. 인상재, 복합레진, 버, 마취제 등에 대한 꾸준한 수요는 이 부문를 거시경제 사이클로부터 보호합니다. 고령 인구가 내구성이 뛰어나고 자연스러운 색상의 옵션을 추구함에 따라 바이오세라믹 임플란트와 생체활성 수복재가 주목받고 있습니다. 반면, 장비 판매는 절대적 규모는 작지만 더 빠르게 증가하고 있습니다. 진단용 스캐너, 디지털 방사선 촬영 패널, 체어사이드 밀링 장비, 다이오드 레이저 시장은 AI 소프트웨어 업데이트와 클리닉의 현금 흐름을 원활하게 하는 구독 모델에 힘입어 2031년까지 연평균 6.05%의 성장률을 보일 것으로 전망됩니다. 번들 서비스 계약과 클라우드 라이선스가 제조업체 수익을 점차 주도하며, 이는 하드웨어 일회성 판매에서 평생 가치(LTV)로의 전환을 시사합니다. 따라서 고가치 장비의 치과 장비 시장 규모는 역사적 평균보다 빠르게 확대되어 공급업체에게 소모품을 넘어선 다각화된 성장 기회를 제공합니다.

북미는 높은 1인당 지출, 보험 보급률, AI 영상 및 CAD/CAM 제작의 광범위한 채택으로 인해 치과 장비 매출에서 가장 큰 비중을 차지합니다. 미국 보험사는 얼라이너 케이스 제출을 위한 구강 내 스캔 비용을 보상하여 디지털 도입을 강화합니다. 그러나 인력 부족과 노동 비용 상승으로 인해 진료소들은 문서화 및 멸균 과정을 자동화하도록 유도되어 통합 소프트웨어 제품군에 대한 수요가 증가하고 있습니다.

유럽은 두 번째로 큰 시장으로, 독일, 프랑스, 영국이 프리미엄 임플란트 시스템과 저선량 CBCT 장비 구매를 주도하고 있습니다. 지속가능성 규제로 수은 기반 아말감 분리기 및 일회용 플라스틱 대체가 가속화되며, 클리닉들은 친환경 설계 도구를 채택하고 있습니다. 의료기기 규정(MDR)에 따른 EU 적합성 업데이트로 인증 소요 기간이 연장되어, 규정 준수 역량을 갖춘 기존 공급업체들이 유리해졌습니다.

아시아태평양 지역은 가장 빠르게 성장하는 시장입니다. 일본의 공적 보험이 특정 CAD/CAM 크라운에 대한 보상을 시작하면서 스캐너 설치가 증가하고 있으며, 한국의 병원들은 지역 관광객을 대상으로 완전 디지털 스마일 디자인을 홍보하고 있습니다. 인도의 도시 중심지에서는 신흥 중산층을 겨냥한 투명 교정기 패키지를 제공하는 중저가 체인점이 급속히 확장 중입니다. 중국은 수입 의존도를 낮추기 위해 국내 3D 프린터 브랜드와 지르코니아 블록 제조에 지속적으로 투자하고 있습니다. 전반적으로 아시아태평양 지역의 치과 장비 시장 규모는 양적 성장과 기술 구성 업그레이드에 힘입어 향후 10년간 두 배로 증가할 것으로 예상됩니다.

The Dental Equipment market is expected to grow from USD 11.87 billion in 2025 to USD 12.47 billion in 2026 and is forecast to reach USD 15.94 billion by 2031 at 5.04% CAGR over 2026-2031.

Adoption of digital imaging, artificial intelligence, and chairside manufacturing is shortening procedure times, improving diagnostic accuracy, and lifting patient acceptance rates. Demand is further supported by rising incidences of dental caries and periodontal disease, steady growth in elective cosmetic procedures, and a strong pipeline of restorative materials that pair high strength with natural aesthetics. Consolidation among large manufacturers is creating scale advantages in research, procurement, and global distribution, while new entrants concentrate on narrow specialties such as AI-based image analytics, robotic surgery aids, and bioceramic implants. Asia-Pacific clinics, buoyed by dental tourism and government incentives for digital radiography, are reshaping the competitive balance by purchasing advanced systems in bulk and offering cost-effective care. At the same time, stricter infection-control rules continue to drive recurring investments in sterilization equipment, instrument tracking, and autoclave upgrades.

Global epidemiological studies show continuing growth in untreated decay and gum infection, particularly among aging adults and children in emerging economies. The resulting clinical workload sustains demand for basic restorative items, endodontic files, and periodontal instruments. National oral-health campaigns in India and Indonesia are bringing more first-time patients into clinics, expanding routine prophylaxis volumes and boosting sales of prophylaxis pastes and sealants. This mounting preventive-care demand indirectly strengthens the dental equipment market

AI algorithms integrated into cone-beam CT and intraoral imaging platforms flag minute lesions, quantify bone levels, and auto-generate treatment plans that dentists can share chairside. Early adopters report 10-20% growth in case acceptance when AI visuals accompany explanations, sparking an upgrade cycle across mid-size practices. Overjet's regulatory-cleared software now processes millions of radiographs per month, signalling rapid normalization of AI diagnostics and reinforcing the dental equipment market.

Insurers often classify laser gum surgery and caries ablation as elective, shifting costs to patients and slowing adoption despite shorter healing times and improved clinical outcomes. Manufacturers respond with hybrid devices that allow dentists to toggle between conventional and laser modes to remain within coverage limits.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Dental consumables captured 43.12% of the dental equipment market in 2025 thanks to their recurring use in every clinical visit. Steady demand for impression materials, composites, burs, and anesthetics shields this segment from macro-economic cycles. Bioceramic implants and bio-active restoratives are gaining traction as ageing populations seek durable, naturally coloured options. Conversely, equipment sales, while smaller in absolute value, are rising faster. Diagnostic scanners, digital radiography panels, chairside mills, and diode lasers together are projected to grow at a 6.05% CAGR through 2031, fuelled by AI software updates and subscription models that smooth cash flows for clinics. Bundled service contracts and cloud licences increasingly define revenue for manufacturers, signalling a pivot from hardware outright sales to lifetime value. The dental equipment market size for high-value equipment is therefore widening faster than historic averages, offering suppliers diversified growth beyond consumables.

The Dental Equipment Market Report Segments the Industry Into by Product (Operatory and Treatment Center Equipment, Dental Laboratory Equipment, Dental Lasers, Diagnostic Dental Equipment), by Treatment (Orthodontic, Endodontic, Peridontic, Prosthodontic), by End User (Hospitals, Clinics, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, South America).

North America remains the largest contributor to dental equipment revenue due to high per-capita expenditure, insurance penetration, and widespread adoption of AI imaging and CAD/CAM fabrication. U.S. insurers reimburse intraoral scans for aligner case submission, reinforcing digital uptake. Workforce shortages and rising labour costs, however, encourage practices to automate documentation and sterilisation, raising demand for integrated software suites.

Europe ranks second, with Germany, France, and the United Kingdom leading purchases of premium implant systems and low-dose CBCT units. Sustainability regulations accelerate replacement of mercury-based amalgam separators and single-use plastics, pushing clinics toward eco-designed tools. EU conformity updates under the Medical Device Regulation have lengthened certification lead times, favouring established suppliers that possess the resources to comply.

Asia-Pacific is the fastest-growing region. Japan's public insurance now reimburses select CAD/CAM crowns, lifting scanner installations, while South Korean clinics advertise fully digital smile design to regional tourists. India's urban centres witness rapid expansion of mid-market chains offering clear aligner packages priced for the rising middle class. China continues to invest in domestic 3-D printer brands and zirconia block manufacturing, aiming to reduce import dependency. Overall, the dental equipment market size in Asia-Pacific is expected to double across the decade, driven by both volume and technology mix upgrades.