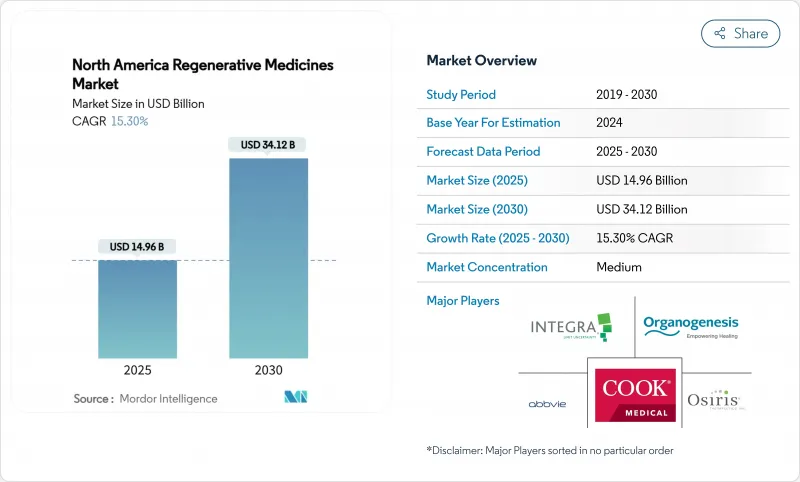

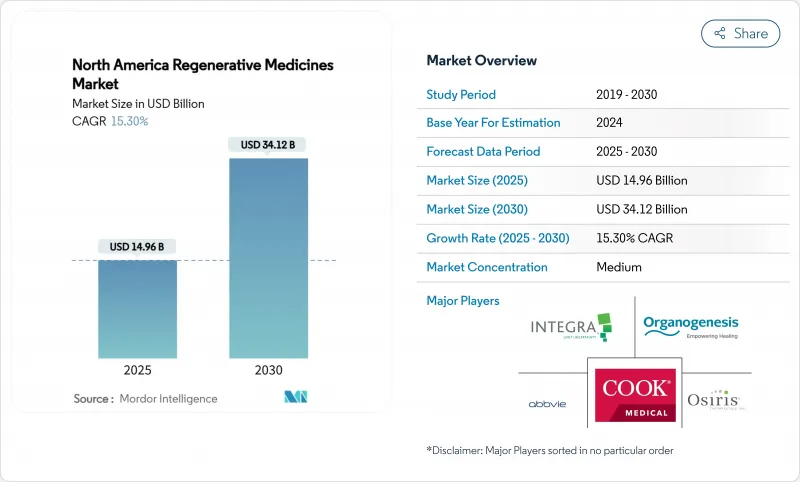

북미의 재생 의학 시장 규모는 2025년에 149억 6,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 15.30%를 나타낼 것으로 예측되며, 2030년에 341억 2,000만 달러에 달할 전망입니다.

변형성 관절증, 혈우병 A, 재발성 다발성 골수종 등 과거에는 학술적 환경에 한정되어 있던 치료법이 현재는 부담이 큰 질환에 대한 상환을 확보할 수 있게 되어 상업적 채택이 가속화되고 있습니다.2024년 총 매출의 84.11%를 미국이 차지하는 가운데, 멕시코는 규제 현대화와 의료 관광 흐름이 맞물리면서 대륙 내 최고 성장 궤도를 보이고 있습니다. 세포 치료제는 물량 측면에서 여전히 주도권을 유지하지만, 특히 바이러스 벡터 생산 분야에서 제조 규모의 경제가 실현되면서 유전자 치료제가 가장 가파른 매출 증가세를 보이고 있습니다. 배치 관리 및 지적 재산권 보호 필요성에 힘입어 자체 생산 시설에 대한 전략적 투자가 증가하면서 북미 재생의학 시장 전반에 걸쳐 입지 선정 패턴이 재편되고 있습니다.

노인 인구의 확대는 재생의학 솔루션에 대한 임상적 시급성을 증폭시키고 있습니다. 5,400만 명 이상의 미국인이 관절염을 앓고 있으며, 2040년까지 이 수치가 7,800만 명에 달할 것으로 예상되어 북미 재생의학 시장 내 정형외과 수요를 주도하고 있습니다. 심혈관 및 신경퇴행성 질환의 동시적 급증은 치료적 수요를 더욱 가중시켜, 관련 기업들이 노화 관련 적응증에 대해 FDA의 재생의학 선진치료제(RMAT) 지정을 추진하도록 촉진하고 있습니다. 생산성 손실과 직접적 의료비로 측정되는 누적 경제적 부담은 평생 비용을 상쇄하는 치료 옵션을 보장하려는 지불자의 의지를 강화합니다. 이러한 역학적 요인들은 종합적으로 세포, 유전자 및 조직공학적 치료법 전반에 걸친 파이프라인 활동에 상당한 추진력을 더하고 있습니다.

자금 조달 속도는 성숙한 혁신 주기를 강조합니다. 미국 국립보건원(NIH)은 2024 회계연도 재생의학 프로젝트에 28억 달러를 배정했으며, 이는 2023년 대비 23% 예산 증가다. 동시에 캐나다 전략혁신기금은 첨단 치료제 생산 허브 3곳 건설을 위해 12억 캐나다 달러(8억 9,000만 달러)를 투입하며 국내 생산 역량 확보와 기술 이전 협약 유치를 도모하고 있습니다. 벤처 투자자들도 명확한 규제 경로를 확보한 후기 단계 자산에 자금을 집중하는 추세를 보여 북미 재생의학 시장 내 단기 수익 실현에 대한 확신을 시사합니다.

전문 클린룸 건설 비용은 평방피트당 평균 2,000달러로 기존 생물학적 제제 시설의 4배에 달하며, 숙련된 인력 부족 현상이 지속되고 있습니다. 2024년 재생의학 기업의 3분의 2가 채용 어려움을 호소했습니다. 수동 공정 단계는 배치 변동성을 증폭시키며, 업계 조사에 따르면 생산량의 15%가 출시 규격 외로 분류되어 단일클론 항체에서 관찰된 실패율의 5배에 달합니다. 자동화가 진전되고 있지만, 자본 집약도는 북미 재생의학 시장 전반에 걸친 확대 적용을 가로막는 막대한 장벽으로 남아 있습니다.

2024년 세포 치료제는 암 및 정형외과 분야의 확립된 보험 적용 혜택을 바탕으로 42.61%의 북미 재생의학 시장 점유율로 매출 1위를 차지했습니다. 반면 유전자 치료제는 2023년 이후 바이러스 벡터 비용을 35% 절감한 제조 효율성 덕분에 24.81%의 연평균 복합 성장률(CAGR) 전망을 기록했습니다.

2024년 파이프라인 전반에서 후보물질의 43%가 현재 다중 재생 모달리티를 결합하고 있으며, 이는 복합 구조체로의 전략적 전환을 반영합니다. 이러한 하이브리드 제품 3종이 2025년 초 FDA 승인을 획득하며, 범주 경계를 허무는 솔루션에 대한 규제 당국의 개방성을 확인시켜 북미 재생의학 시장 확대 가능성을 시사합니다.

동종 이식 치료법은 즉시 사용 가능한 확장성과 확립된 유통망 덕분에 2024년 북미 재생 의학 시장 규모의 55.85%를 차지했습니다. 자가 이식 접근법은 공정 최적화로 정맥 채취부터 이식까지 소요 시간이 2023년 28일에서 2025년 초 14일로 단축되며 21.17%의 연평균 성장률(CAGR)로 격차를 좁혀가고 있습니다.

자기 CAR-T는 혈액 악성 종양에서 임상 우위를 유지하고 있는 반면, 동종 CAR-T는 심혈관계의 긴급 상황에서 신속한 전개가 가능합니다. 2025년 3월에 자가 목표를 동종 제조와 연결하는 하이브리드 소싱 모델은 최초의 승인을 받아 북미의 재생 의학 시장을 더욱 다양화하고 있습니다.

북미의 재생 의학 보고서는 제품 유형(세포 치료, 유전자 치료, 기타), 세포 기원(자기 유래, 기타), 공급원(성체 줄기 세포, 기타), 용도(정형외과·근골격계, 기타), 최종 사용자(병원·외과 센터, 기타), 지역(북미, 유럽, 아시아태평양, 기타)으로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

The North America Regenerative Medicines Market size is estimated at USD 14.96 billion in 2025, and is expected to reach USD 34.12 billion by 2030, at a CAGR of 15.30% during the forecast period (2025-2030).

Commercial adoption is accelerating as therapies that were once confined to academic settings now secure reimbursement for high-burden conditions such as osteoarthritis, hemophilia A and relapsed multiple myeloma. The United States accounts for 84.11% of total 2024 revenue, while Mexico delivers the highest growth trajectory on the continent as regulatory modernization and medical-tourism flows converge. Cell therapies retain leadership on volume, yet gene therapies deliver the steepest revenue ramp as manufacturing economies of scale materialize, particularly in viral-vector production. Heightened strategic investment in in-house manufacturing, spurred by the need for batch-control and intellectual-property protection, is reshaping site-selection patterns throughout the North America regenerative medicine market.

An expanding cohort of older adults is amplifying the clinical urgency behind regenerative solutions. More than 54 million Americans live with arthritis, and projections place the figure at 78 million by 2040, driving orthopedic demand within the North America regenerative medicine market. Parallel surges in cardiovascular and neurodegenerative conditions add to the therapeutic backlog, prompting sponsors to pursue FDA's Regenerative Medicine Advanced Therapy (RMAT) designation for age-related indications. The cumulative economic burden, measured in lost productivity and direct medical expenditure, intensifies payer willingness to underwrite curative options that offset lifetime costs. Collectively, these epidemiological factors add substantial momentum to pipeline activity across cell, gene and tissue-engineered modalities.

Funding velocity underscores the maturing innovation cycle. The National Institutes of Health allocated USD 2.8 billion to regenerative-medicine projects for fiscal-year 2024, a 23% budgetary rise over 2023. Simultaneously, Canada's Strategic Innovation Fund committed CAD 1.2 billion (USD 890 million) to construct three advanced-therapy manufacturing hubs, a move designed to anchor domestic capacity and attract technology transfer agreements. Venture investors are mirroring the trend by preferentially channeling capital toward late-stage assets with defined regulatory pathways, signaling confidence in near-term revenue realization within the North America regenerative medicine market.

Specialized clean-room construction averages USD 2,000 per square foot, quadruple that of conventional biologics facilities, and skilled-labor shortages persist, with two-thirds of regenerative-medicine firms citing hiring difficulties in 2024. Manual processing steps amplify batch variability; industry surveys place 15% of runs outside release specifications, five-times the failure rate observed for monoclonal antibodies. While automation is advancing, capital intensity remains a formidable hurdle stifling wider roll-out across the North America regenerative medicine market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cell therapies led the revenue tables in 2024 with 42.61% North America regenerative medicine market share, benefitting from established reimbursement in oncology and orthopedics. Gene therapies, however, post a 24.81% CAGR outlook, propelled by manufacturing efficiencies that have trimmed viral-vector costs by 35% since 2023.

Across 2024 pipelines, 43% of candidates now blend multiple regenerative modalities, reflecting a strategic pivot toward combination constructs. Three such hybrid products gained FDA clearance in early 2025, confirming regulatory openness to category-blurring solutions that will likely enlarge the North America regenerative medicine market.

Allogeneic therapies commanded 55.85% of the North America regenerative medicine market size in 2024, aided by off-the-shelf scalability and established distribution chains. Autologous approaches are closing the gap, advancing at 21.17% CAGR as process optimization compresses vein-to-vein timelines from 28 days in 2023 to 14 days in early 2025.

Efficacy differentials remain indication-specific: autologous CAR-T retains a clinical edge in hematologic malignancies, whereas allogeneic constructs offer rapid deployment in cardiovascular emergencies. Hybrid sourcing models, marrying autologous targeting with allogeneic manufacturing, received their first approval in March 2025, further diversifying the North American regenerative medicine market.

The North America Regenerative Medicine Report is Segmented by Product Type (Cell Therapies, Gene Therapies, and More), Origin of Cells (Autologous, and More), Source (Adult Stem Cells, and More), Application (Orthopedics & Musculoskeletal, and More), End User (Hospitals & Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).