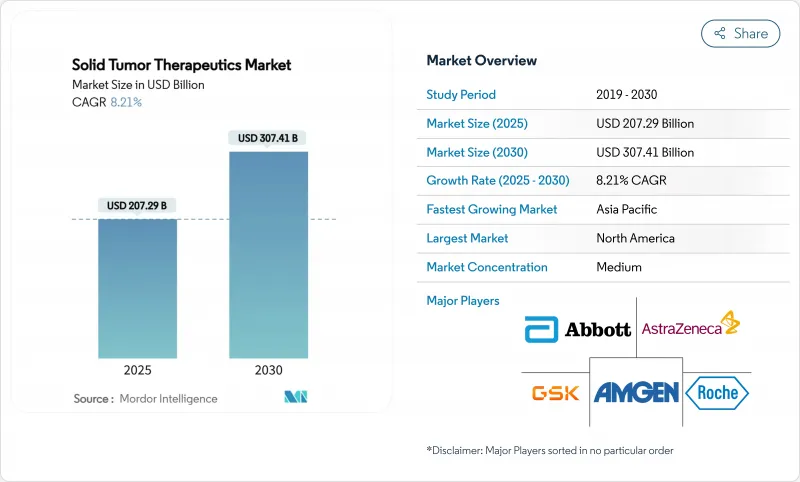

고형 종양 치료제 시장 규모는 2025년에 2,072억 9,000만 달러, CAGR 8.21%를 나타내고 2030년에는 3,074억 1,000만 달러로 확대될 것으로 예측되고 있습니다.

항체 약물 복합체, 면역관문억제제의 조합, 바이오마커 주도형 요법과 같은 혁신적인 기술로 임상 옵션이 확대되고 환자층이 확대되고 있습니다. 2050년까지 연간 3,200만명의 암 환자가 새롭게 발생할 것으로 예측되는 암 이환율의 상승이 장기적인 수요를 유지하는 한편, 미국에서는 밸류 베이스의 상환 시험, 유럽에서는 아웃컴에 연동한 계약이 실시되어, 지불측의 신뢰가 높아지고 있습니다. 북미는 강력한 지적재산권 보호를 통해 가격면에서 리더십을 유지하고 있지만 아시아태평양은 규제 당국의 승인이 가속화되어 기술 혁신의 차이를 줄이고 있습니다. 주요 다국적 기업과 중견 생명 공학 기업의 통합으로 경쟁 포지셔닝이 재구성되고 AI를 활용한 탐색 파트너십에 대한 투자로 전임상시험의 타임라인이 단축되고 있습니다.

고형 종양 치료제 시장은 2050년까지 매년 3,200만명이 새롭게 진단될 것으로 예측되는 암 부담 증가와 직접적인 수요 상관관계가 있습니다. 고형암은 이러한 사례의 약 85%를 차지하고 있으며, 도시화와 라이프스타일 변화가 위험요인을 악화시키기 때문에 아시아태평양이 가장 급증하고 있습니다. 중국만으로 세계 이환율의 30% 가까이를 차지하고 있기 때문에 다국적 기업은 지방 상환 제도에 맞추어 시장 진출 계획을 세울 필요에 육박하고 있습니다. 미국과 서유럽에서는 인구의 고령화가 진행되고 있어 동시에 신규 치료의 대상이 되는 환자수도 증가하고 있습니다. 이러한 역학적 패턴을 종합하면 고형 종양 치료제 시장에 차세대 치료제 후보가 꾸준히 유입되고 있습니다.

항체 약물 복합체(ADC)는 가장 역동적인 모달리티로, 후기 ADC 자산의 80%가 고형암을 표적으로 하고 있기 때문에 2023년 매출 100억 달러에서 2033년에는 390억 달러로 성장할 것으로 예상됩니다. HER2 저하 유방암에 대한 트라스투주맙 델크스테칸과 폐암에 대한 데이터 포타맙 델크스테칸과 같은 획기적인 승인은 화학요법에 대해 50% 이상의 무증상 생존기간의 연장을 실현하고 있습니다. PD-1 억제제와 CTLA-4 제형 및 표준 화학요법을 병용한 치료는 5년 전체생존율(OS) 18%를 보였으며, 단독 화학요법의 11% 대비 생존 이점을 나타냈다. 알고리즘이 주도하는 약제 설계 플랫폼이 성숙함에 따라 기업은 AI와의 제휴에 10억 달러 이상을 채워 약물 발견의 타임라인을 단축하고 있습니다. 이러한 과학적 진보는 고형 종양 치료제 시장의 장기적인 확장에 대한 자신감을 강화하고 있습니다.

암치료제 개발기간의 중앙값은 여전히 10-15년으로, I상부터 승인까지의 실패율은 90%를 넘고 있습니다. FDA의 2021년 가치 지향 지침은 능동 비교 데이터를 요구하고 있으며 시험의 복잡성을 높이고 있습니다. 병용 요법은 종양 유형에 걸친 멀티암 시험을 필요로 하고 자원을 더욱 확장하고 있습니다. 중국의 우선심사 채널에 따라 승인까지의 일수는 263.5일로 단축되었으며, 신청서류에는 여전히 광범위한 유효성 증거가 필요하며 상업화가 최대 3년 지연될 수 있습니다. 이 누적 효과는 고형 종양 치료제 시장의 단기 성장 속도를 약화시킵니다.

유방암은 2024년 매출의 25.67%를 차지했고 고형 종양 치료제 시장 규모의 최대 비중을 차지합니다. 트라스투주맙 델크스테칸에 의해 가능해진 HER2 저가 분류는 치료가능 그룹을 60% 확대하여 수익 성장을 가속시켰습니다. 제2위의 폐암은 스테이지 III의 EGFR 유전자 변이 질환에 있어서 오시멜티닙이 무증악 생존 기간 중앙값 39.1개월을 달성한 것이 기여했습니다.

전립선암은 2030년까지의 CAGR이 가장 빠른 10.34%가 될 것으로 예측되며, 이는 빈 전이 상황에서 무증악 생존 기간을 연장하는 전이 지향의 접근에 뒷받침되고 있습니다. 대장암 치료 프로그램에서는 전층 소작 요법이 평가되고, 자궁 경부암 치료 프로그램에서는 HPV 백신 접종이 유병률 패턴을 변화시키고 있습니다. 췌장 및 신경내분비 종양의 혁신은 종양 치료 분야에서 새로운 면역조절제에 이르기까지 고형 종양 치료제 업계 전반의 수익원을 다양화하고 있습니다.

프리미엄 가격, 폭넓은 보험 적용, 깊은 임상시험 네트워크가 신규 약제의 급속한 보급을 지원했기 때문에 북미가 2024년에 42.43%의 점유율을 획득하여 매출을 견인했습니다. 고액 약제에 대한 지불측의 감시는 강해지고 있는 것, 암 진료의 통합이 계속되고 있기 때문에 판매업자의 협상력은 강해지고 있습니다.

유럽은 여전히 2위를 차지하고 있으며 독일, 영국, 프랑스가 EMA의 협조적인 틀 아래 첨단 치료법 채택을 주도하고 있습니다. 기준가격과 의료기술평가의 재검토가 약가 인플레이션을 억제하고 있기 때문에 제조업체는 고형종양치료시장에 매력적인 이익을 유지하기 위한 비밀할인 협상을 강요하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 9.54%로 가장 급성장하는 지역으로 중국이 발견과 상업화의 허브로 변모를 이루었으며 2024년에는 228개의 신약이 승인되었으며, 그 37%가 항종양제였습니다. 일본의 혁신자들이 신규 상환 목록에 포함된 신약의 71%를 확보했고, 일본과 인도는 효율적인 스타트업 타임라인과 미치료 인구를 배경으로 시험 투자를 획득했습니다. 중동 및 아프리카와 남미는 장기적으로는 상승 여지가 있는 것, 한정된 인프라와 예산 프레임이 단기적인 성장을 제약하고 있습니다. 전반적으로 고형 종양 치료제 시장에서 균형 잡힌 노출을 요구하는 기업의 경우 지역 다양화가 필수적입니다.

The solid tumor therapeutics market size stood at USD 207.29 billion in 2025 and is forecast to advance to USD 307.41 billion by 2030, reflecting an 8.21% CAGR.

Robust innovation in antibody-drug conjugates, immune-checkpoint inhibitor combinations, and biomarker-driven regimens is expanding clinical options and broadening patient pools. Rising cancer prevalence-projected at 32 million new cases annually by 2050-sustains long-term demand, while value-based reimbursement pilots in the United States and outcome-linked contracts in Europe are strengthening payer confidence. North America preserves pricing leadership through strong intellectual-property protections, yet Asia-Pacific is closing the innovation gap as regulatory agencies accelerate approvals. Consolidation among large multinational companies and mid-cap biotech firms is reshaping competitive positioning, and investment in AI-enabled discovery partnerships is shortening pre-clinical timelines.

The solid tumor therapeutics market has a direct demand correlation with the escalating burden of cancer, which is projected to hit 32 million new diagnoses each year by 2050. Solid tumors represent around 85% of these cases, with Asia-Pacific registering the steepest uptick as urbanization and lifestyle shifts aggravate risk factors. China alone accounts for nearly 30% of worldwide incidence, prompting multinational companies to tailor market-entry plans toward provincial reimbursement schemes. Population aging in the United States and Western Europe is simultaneously growing the pool of patients eligible for novel therapies. Taken together, these epidemiological patterns ensure a steady inflow of candidates for next-generation treatments within the solid tumor therapeutics market.

Antibody-drug conjugates (ADCs) have become the most dynamic modality, expanding from USD 10 billion sales in 2023 to an estimated USD 39 billion by 2033 as 80% of late-stage ADC assets target solid tumors . Breakthrough approvals such as trastuzumab deruxtecan for HER2-low breast cancer and datopotamab deruxtecan for lung cancer are delivering progression-free survival gains exceeding 50% versus chemotherapy. Combining PD-1 inhibitors with CTLA-4 agents and standard chemotherapy has yielded five-year overall-survival rates of 18% in metastatic NSCLC compared with 11% for chemotherapy alone. As algorithm-driven drug-design platforms mature, companies are allocating over USD 1 billion to AI partnerships to compress discovery timelines. These scientific strides are reinforcing confidence in the long-run expansion of the solid tumor therapeutics market.

Median development timelines for an oncology asset still span 10-15 years, while failure rates exceed 90% from Phase I to approval. The FDA's 2021 value-oriented guidance demands active-comparator data, raising trial complexity. Combination regimens require multi-arm studies across tumor types, further stretching resources. Although China's priority-review channel has trimmed approval to 263.5 days, dossiers still need expansive efficacy evidence that can delay commercialization by up to three years. The cumulative effect tempers the near-term growth velocity of the solid tumor therapeutics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Breast cancer retained 25.67% of 2024 revenue, giving it the largest slice of the solid tumor therapeutics market size. HER2-low classifications enabled by trastuzumab deruxtecan enlarged the treatable group by 60%, accelerating revenue growth. Lung cancer, the second-largest segment, benefited from osimertinib's 39.1-month median progression-free survival in stage III EGFR-mutated disease.

Prostate cancer is projected to log the fastest 10.34% CAGR through 2030, buoyed by metastasis-directed approaches that enhance progression-free intervals in oligometastatic settings. Colorectal programs are evaluating total-ablative therapy, and cervical-cancer dynamics are shifting as HPV vaccination alters prevalence patterns. Innovation in pancreatic and neuroendocrine tumors, ranging from tumor-treating fields to novel immunomodulators, is diversifying revenue sources across the solid tumor therapeutics industry.

The Solid Tumor Therapeutics Market Report is Segmented by Cancer Type (Breast Cancer, Lung Cancer, and More), Drug Type (Carboplatin, Cisplatin, and More), Administration Route (Intravenous, Oral, Subcutaneous, Intratumoral, Other Administration Routes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America led revenue with a 42.43% slice in 2024 as premium pricing, broad insurance coverage and deep clinical-trial networks supported rapid uptake of novel agents. Continued consolidation of oncology practices is strengthening distributor bargaining clout, although payer scrutiny of high-cost drugs is intensifying.

Europe remains the second-largest region, with Germany, the United Kingdom and France spearheading adoption of advanced therapies under coordinated EMA frameworks. Reference-pricing and health-technology-assessment reviews temper list-price inflation, compelling manufacturers to negotiate confidential discounts that still preserve attractive margins for the solid tumor therapeutics market.

Asia-Pacific is the fastest-growing region at 9.54% CAGR through 2030 as China transforms into a discovery and commercialization hub, having approved 228 new medicines in 2024, 37% of which were antineoplastics. Domestic innovators secured 71% of new reimbursement-list inclusions, while Japan and India captured trial investments due to efficient start-up timelines and treatment-naive populations. Middle East & Africa and South America offer long-run upside, yet limited infrastructure and budget caps constrain near-term growth. Collectively, geographical diversification is vital for companies seeking balanced exposure within the solid tumor therapeutics market.