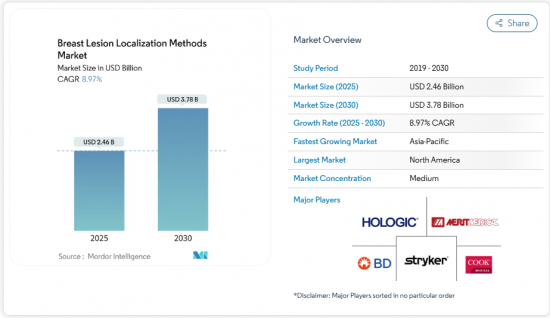

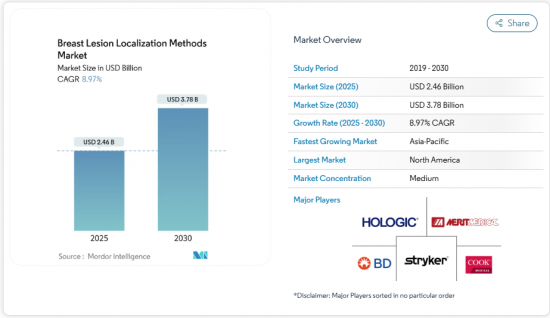

유방 병변 국소화 시장 규모는 2025년에 24억 6,000만 달러로 평가되고, 2030년에는 37억 8,000만 달러에 달하며, CAGR 8.97%를 나타낼 것으로 예측됩니다.

유방암 이환율 상승, 검진 프로그램 확대, 무선 시드, 고주파, 레이더 시스템으로의 명확한 전환이 주요 확대 요인입니다. 특히 자기 현지화는 철사에 의한 당일 수술의 제약을 없애고 외래 유방 온존 수술로의 이동을 뒷받침합니다. 방사성 동위 원소를 사용하지 않는 유럽의 움직임과 같은 날 퇴원을 장려하는 북미의 상환 인센티브가 무선 솔루션의 매력을 높이고 있습니다. 아시아태평양에서는 전국적인 검진 캠페인이 대규모 도시 인구에서 조기 단계의 비촉지 병변을 확인하기 때문에 수량적으로 큰 상적을 기대할 수 있습니다.

유방암 진단 건수 증가는 유방 병변 국소화 시장의 수술 건수 증가에 직결하고 있습니다. 선진국의 인구 고령화와 중국, 인도, 동남아시아의 정부 자금에 의한 유방 조영술 프로그램의 보급에 의해 지금까지 발견되지 않았던, 촉지할 수 없는 병변이 대량으로 발견되고 있습니다. 뭄바이, 상하이, 방콕 도시의 검진센터는 기록적인 검출률을 보고하고 있으며, 종양이 작은 경우에는 과도한 조직 절제를 피하기 위해 보다 정확한 위치를 지정해야 합니다. 조기 발견은 유방 온존 수술 후보자의 비율도 증가하고 정확한 병변 마킹 수요가 더욱 높아집니다. 이미지 감도가 증가함에 따라 수술에서 발생하는 병변의 평균 크기는 계속 줄어들고 있으며 신뢰할 수 있는 수술 전 위치 확인이 필수적입니다.

유방절제술과 BCS의 종양학적 동등성을 입증하는 임상적 증거는 더 나은 미용적 결과와 함께 유방 온존 수술에 대한 세계적인 축족을 가속화하고 있습니다. 중국의 BCS 사용률은 10년 이내에 1.53%에서 11.88%로 상승해 일본은 40% 가까운 채용을 유지하고 있습니다. 보다 젊고, 충분한 지식을 가진 환자가 적극적으로 유방 온존을 요구하게 되었고, 병원은 정확한 국소화를 중심으로 수술의 워크플로우를 재검토하게 되었습니다. 유럽에서는 환자의 불편함과 일정 병목 현상을 줄이기 위한 노력으로 와이어를 대체하는 자기 시드의 도입이 진행되고 있습니다. 네오애쥬번트 화학요법은 종양을 축소시킴으로써 BCS 후보의 풀을 더욱 확대시키지만, 그 이익은 외과의가 잔존 병변의 마진을 타겟으로 할 수 있도록 고정밀 병변 마킹이 조건이 됩니다.

유럽연합(EU)의 의료기기 규제는 증거 요건을 확대하고 적합성 평가를 장기화하기 위해 무선 플랫폼 출시를 최대 4년 늦춥니다. 혁신적인 국소화 기술은 미국 510(k) 규칙에서 전제 장비가 없는 경우가 많으며, 실질적인 동등성을 입증하기 위해 더 큰 임상 데이터 세트가 필요합니다. 신흥국은 현지화된 안전성 시험을 요구하는 추가 등록층을 도입하여 중견 공급업체를 압박하고 있습니다. 규제 당국의 전문 팀을 가진 대기업은 이러한 장애물을 극복하고 있지만 추가 비용은 하류로 흐르기 때문에 자원이 제한된 환경에서의 채용이 지연될 수 있습니다. 각 지역이 시판 후 감시를 강화하는 가운데 제조업체는 여전히 리콜 위험에 노출되어 임상의의 신뢰를 손상시킬 수 있습니다.

와이어 지침은 2024년 유방 병변 국소화 시장 점유율의 35.76%를 차지했으며, 이에 따라 정착된 지위, 낮은 초기 비용 및 보편적인 가용성을 반영했습니다. 철사의 사용은 입증된 장비를 선호하고 엄격한 자본 규정 하에서 운영되는 대규모 공립 병원에서 뿌리깊습니다. 그러나, 자기 시드의 채용은 급속히 증가하고 있으며, CAGR 10.11%를 나타낼 전망입니다. 무작위화 연구에서 환자 불안의 감소, 스케줄링의 단순화, 수술 지연의 감소가 보고되고 있기 때문입니다. 규제당국이 방사선을 사용하지 않는 환경을 선호하는 유럽에서는 방사성방식이 후퇴하고 독일에서는 2028년에 금지가 예정되어 있기 때문에 수요가 자기 시스템이나 레이더 시스템으로 향할 가능성이 높습니다. LOCalizer 및 레이더 기반 SAVI SCOUT과 같은 RFID 태그는 전리 방사선을 사용하지 않고 정확한 깊이 검출을 제공하고 워크플로의 편리성과 마진 정확도의 균형을 중시하는 유선 외과 의사의 지지를 얻고 있습니다. PACS 아키텍처와 원활하게 통합된 시드 배치 이미지 소프트웨어를 병원이 방사선실을 개조함으로써 유방 병변 국소화 시장은 이익을 얻고 있습니다. 자기 플랫폼에서는 콘솔 진단용 검출 프로브의 번들화가 진행되고 있어 여러 수술 팀에 자본 비용을 분산시키는 부문 횡단적인 이용이 가능해지고 있습니다. 제품 포트폴리오가 성숙함에 따라 공급업체는 콘솔 업그레이드에 대한 지속적인 투자를 보장하고 일상적인 수익원을 창출하는 보완적인 일회용 제품을 강조합니다.

마그네틱 시드를 이용한 국소화는 시드가 거의 감지되지 않고 몇 주간 안정된 상태를 유지하므로 환자의 불편함을 최소화하며 수술 건수가 많은 시설에서도 유연하게 수술 일정을 잡을 수 있습니다. 자기시스템의 유방 병변 국소화 시장 규모에서는 2030년까지 수익이 대폭 증가할 것으로 예측되고 있습니다. 와이어 디바이스 설계자는 보다 가늘고 내변색성이 있는 와이어나 통합된 이미징 마커로 대항하고 있지만, 이러한 점진적인 미세 조정은 와이어 프리 옵션 워크플로우의 우위성을 상쇄할 수 없습니다. 레이더 시스템은 실시간 현장 지침을 활용하여 시각적 및 청각적인 신호를 제공하여 절차 시간을 단축합니다. 방사선 부서는 종종 혼합 모달 포트폴리오를 채택합니다. 즉, 비용 중시의 경우에는 와이어를 사용하고, 복잡한 사례나 미용 우선의 경우는 시드로 이행함으로써 하이브리드한 수요 패턴을 만들어내고 있습니다. 마그네틱 프로브와 형광 및 초음파 시각화를 통합하는 공급업체는 3차 센터에서 임상 평가가 시작된 차세대 영상 유도 수술 양식에 대해 자사 제품의 미래를 입증하는 것을 목표로 하고 있습니다.

북미는 성숙한 검진 인프라, BCS의 높은 보급률, 유리한 상환구조로 2024년 유방 병변 국소화 시장에서 41.32%의 점유율을 유지했습니다. 미국에서는 메디케어 유방 조영술 보험이 환자의 자기 부담 없이 적용되기 때문에 국소화를 필요로 하는 조기 발견의 유입이 끊임없습니다. 민간 보험사도 이 혜택을 받아 교외의 외래센터에서의 검사건수 증가를 가속시키고 있습니다. 캐나다의 각 주는 이동식 영상 진단 장치를 확충하고, 농촌 지역의 접근성을 향상시키고, 자본 예산이 부족한 지역에서의 전선 수요를 뒷받침하고 있습니다. 멕시코 세구로 대중 개혁은 유방 조영술을 기본 혜택 패키지에 통합하고 멕시코 시티의 3차 병원이 RFID 플랫폼을 시험적으로 도입함에 따라 시드 수입을 점차 자극하고 있습니다. 이 지역 전체에서 유방 절제술의 64%가 외래로 전환하고 있으며 유연한 스케줄링을 지원하는 시드 흡수가 강화되었습니다. 510(k) 패스웨이는 감지기 개선이 발생할 때 업그레이드를 가속화하기 때문에 시장 진출기업은 FDA 승인 제품을 선호합니다.

유럽은 환자의 안전과 환경에 대한 배려를 중시하는 규제에 힘입어 2030년까지 연평균 복합 성장률(CAGR) 8.56%를 나타낼 전망입니다. 독일에서는 신청중인 방사선 방호 규제에 의해 방사성 시드에서 자기 및 레이더 방식으로의 이행이 가속화됩니다. 영국의 국민보건서비스는 2025년에 자기정위법의 파일럿시험을 채용하여 대기시간 단축과 환자보고에 의한 쾌적성의 향상을 실증해 지역적 관심을 높이고 있습니다. 프랑스와 이탈리아는 진단 관련 그룹 예산 내에서 자기 시스템의 비용 효과를 평가하고, 스페인은 EU 구조 기금을 활용하여 지방 병원을 개조하고 있습니다. 의료기기 규정에 따라 공급업체는 임상 증거 자료를 확충해야 하지만 조기 준수는 경쟁 우위를 가져옵니다. 범유럽 대리점 계약으로 물류 네트워크가 통합되어 발트해와 발칸 반도의 소규모 시장에서도 제품의 입수성이 향상되고 있습니다.

아시아태평양은 CAGR 9.78%를 나타내 가장 급성장하고 있는 지역으로 유방암 이환율의 급상승과 병원 수용 능력 확대가 뒷받침되고 있습니다. 중국의 지방 검진 프로그램은 BCS율의 비약적 상승에 공헌해, 베이징과 상하이의 톱암 센터에서 자기 시드의 대량 조달의 방아쇠가 되었습니다. 인도에서는 주 수준의 관민 파트너십이 이동식 유방 X선 촬영 버스에 자금을 제공하고 있지만, 무선 태그의 채용은 1급 대도시 병원에 집중하고 있습니다. 일본은 BCS의 보급률 40%를 유지해 기술의 발사대가 되고 있습니다. 일본의 외과의사는 비교 연구를 발표했고, 이웃 한국과 대만에 영향을 미치고 있습니다. 호주는 메디케어 베네핏 일정에 따른 상환경로가 무선태그를 인정하고 있기 때문에 레이더 정위 기술을 받아들이고 있습니다. 태국과 베트남을 포함한 동남아시아 국가들은 외부 공여자로부터의 보조금이 자본 구매를 상쇄하고 기술 보급을 보다 광범위한 의료 시스템 강화에 얽히게 함으로써 시드로 축족을 옮기고 있습니다. 유방 병변 국소화 업계는 현지 수술량과 언어 요구에 맞추어 트레이닝 모듈을 조정하고 학회와 제휴하여 시드 설치 커리큘럼을 표준화하고 있습니다.

The breast lesion localization methods market size was valued at USD 2.46 billion in 2025 and is forecast to reach USD 3.78 billion by 2030, advancing at an 8.97% CAGR.

Rising breast-cancer incidence, expanding screening programs, and a clear migration toward wire-free seed, radiofrequency, and radar systems are the primary expansion catalysts. Magnetic localization in particular eliminates the same-day surgery constraint of wires, supporting the shift toward outpatient breast-conserving surgery. European movement away from radioactive isotopes and North American reimbursement incentives for same-day discharge reinforce the appeal of wireless solutions. Asia-Pacific provides significant volume upside as national screening campaigns identify earlier-stage, non-palpable lesions in large urban populations.

Escalating breast-cancer diagnoses are translating directly into higher procedure volumes for the breast lesion localization methods market. Population aging in developed countries and the proliferation of government-funded mammography programs in China, India, and Southeast Asia are unveiling large pools of previously undetected, non-palpable lesions. Urban screening centers in Mumbai, Shanghai, and Bangkok are reporting record detection rates, and smaller tumors require more precise localization to avoid excessive tissue removal. Earlier detection also increases the proportion of candidates for breast-conserving surgery, further boosting demand for accurate lesion marking. As imaging sensitivity grows, the average lesion size encountered in surgery continues to fall, making reliable pre-operative localization indispensable.

Clinical evidence demonstrating oncologic equivalence between mastectomy and BCS, coupled with better cosmetic outcomes, has accelerated the global pivot toward conservation procedures. China's BCS usage climbed from 1.53% to 11.88% within ten years, and Japan sustains near-40% adoption. Younger, well-informed patients actively seek breast preservation, prompting hospitals to overhaul surgical workflows around precise localization. Europe leads the embrace of magnetic seeds as wire replacements, driven by initiatives to curtail patient discomfort and scheduling bottlenecks. Neoadjuvant chemotherapy further enlarges the pool of BCS candidates by shrinking tumors, yet that benefit is contingent upon highly accurate lesion marking so surgeons can target residual disease margins.

The European Union Medical Device Regulation extends evidence requirements and lengthens conformity assessments, delaying wireless platform launches by up to four years. Innovative localization technologies often lack predicate devices under the U.S. 510(k) rule, necessitating larger clinical data sets to prove substantial equivalence. Emerging economies introduce additional registration layers that demand localized safety testing, straining mid-sized vendors. Larger corporations with dedicated regulatory teams navigate these hurdles but pass added costs downstream, potentially slowing adoption in resource-limited settings. As regions tighten post-market surveillance, manufacturers remain exposed to recall risks that can erode clinician confidence.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Wire guidance held 35.76% of the breast lesion localization methods market share in 2024, reflecting its entrenched status, low upfront cost, and universal availability. Wire use persists in large public hospitals that prioritize proven instruments and operate under tight capital controls. Yet, magnetic seed adoption is rising swiftly, propelled by 10.11% CAGR, as randomized studies report lower patient anxiety, simplified scheduling, and reduced operative delays. Radioactive methods are retreating in Europe where regulators favor radiation-free environments, and Germany's planned 2028 ban will likely redirect demand to magnetic and radar systems. RFID tags such as LOCalizer and radar-based SAVI SCOUT offer accurate depth detection without ionizing radiation, gaining favor among breast surgeons who balance workflow convenience with margin precision. The breast lesion localization methods market benefits as hospitals retrofit radiology suites with seed placement imaging software that integrates seamlessly with PACS architectures. Magnetic platforms increasingly bundle console-agnostic detection probes, enabling cross-department utilization that spreads capital cost across multiple surgical teams. As product portfolios mature, vendors highlight complementary disposables that generate recurring revenue streams, ensuring continued investment in console upgrades.

Magnetic seed localization carries minimal patient discomfort because seeds are scarcely palpable and remain stable for weeks, allowing flexibility in scheduling surgery in high-volume centers. In the breast lesion localization methods market size for magnetic systems, revenue is projected to climb significantly by 2030. Wire device designers counter with thinner, kink-resistant wires and integrated imaging markers, but these incremental tweaks hardly offset the workflow superiority of wire-free options. Radar systems capitalise on real-time in-field guidance, providing visual and auditory cues that shorten procedure times. Radiology departments often adopt a mixed-modal portfolio-maintaining wires for cost-sensitive cases while transitioning complex or cosmetic priority cases to seeds-creating hybrid demand patterns. Vendors that integrate magnetic probes with fluorescence or ultrasound visualization aim to future-proof their products against next-generation image-guided surgery modalities now entering clinical evaluation at tertiary centers.

The Breast Lesion Localization Methods Market Report is Segmented by Localization Method (Wire-Guided Localization, Radioactive-Based Localization [RSL and ROLL], and More), Usage (Tumor Identification and More), End-User (Hospitals, Ambulatory Surgical Centers (ASCs), and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 41.32% share of the breast lesion localization methods market in 2024 owing to mature screening infrastructure, high BCS adoption, and favorable reimbursement structures. The United States extends Medicare mammography coverage with no patient copay, generating a consistent influx of early detections requiring localization. Private insurers mirror these benefits, accelerating procedural growth in suburban outpatient centers. Canadian provinces expand mobile imaging fleets, enhancing access in rural communities and boosting wire demand where capital budgets lag. Mexico's Seguro Popular reforms incorporate mammography in the basic benefit package, gradually stimulating seed imports as tertiary hospitals in Mexico City pilot RFID platforms. Across the region, 64% of mastectomies have shifted to outpatient settings, reinforcing seed uptake that supports flexible scheduling. Market participants prioritize FDA-cleared products because the 510(k) pathway expedites upgrades when incremental detector refinements emerge.

Europe advances at 8.56% CAGR through 2030 underpinned by regulatory emphasis on patient safety and environmental considerations. Germany's pending radiation-protection regulation accelerates the transition from radioactive seeds to magnetic and radar modalities. The United Kingdom's National Health Service adopted magnetic localization pilots in 2025 that demonstrate shorter wait times and higher patient-reported comfort, driving broader regional interest. France and Italy assess cost-effectiveness of magnetic systems within diagnosis-related group budgets, while Spain leverages EU structural funds to retrofit provincial hospitals. Under the Medical Device Regulation, suppliers must expand clinical evidence dossiers, but early compliance confers competitive advantage. Pan-European distributor agreements consolidate logistics networks, improving product availability even in smaller Baltic and Balkan markets.

Asia-Pacific represents the fastest-growing territory at 9.78% CAGR, propelled by sharp rises in breast-cancer incidence and expanding hospital capacity. China's provincial screening programs contributed to BCS rate leaps and triggered bulk procurement of magnetic seeds at top cancer centers in Beijing and Shanghai. India witnesses state-level public-private partnerships funding mobile mammography buses, yet adoption of wireless tags remains concentrated in tier-1 metropolitan hospitals. Japan maintains 40% BCS penetration and serves as a technology launchpad; its surgeons publish comparative studies that influence neighboring South Korea and Taiwan. Australia embraces radar localization technology because reimbursement pathways under the Medicare Benefits Schedule recognize wireless tags. Southeast Asian countries, including Thailand and Vietnam, pivot toward seeds when external donor grants offset capital purchases, intertwining technology diffusion with broader health-system strengthening. The breast lesion localization methods industry tailors training modules to local surgical volumes and language needs, partnering with academic societies to standardize seed placement curricula.