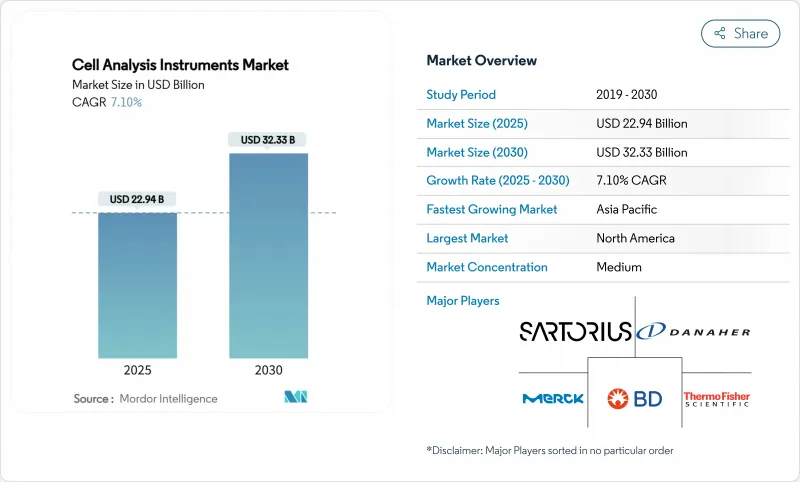

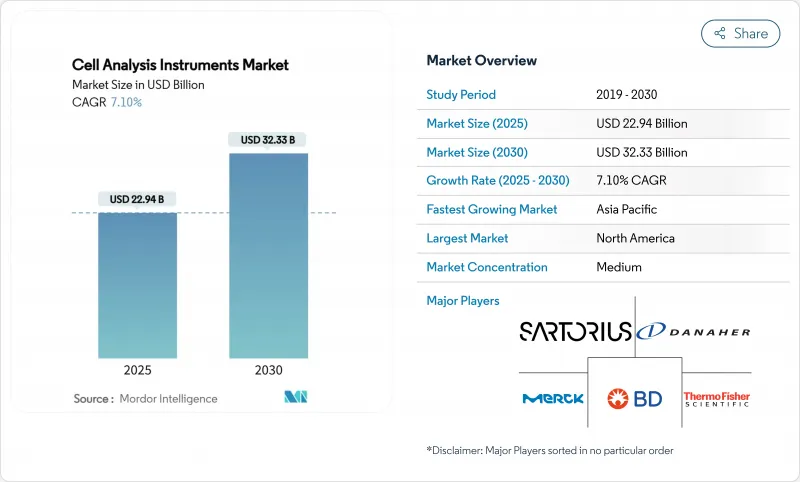

세포 분석기 시장은 2025년에 229억 4,000만 달러에 이를 전망이며, 2030년에는 323억 3,000만 달러로 확대될 것으로 예측되며, CAGR은 7.1%로 견조하게 추이할 전망입니다.

만성질환 관리가 조기분자 검출, 인공지능(AI) 기반 이미징, 그리고 중규모 실험실에서도 보급된 대규모 싱글셀 시퀀싱 워크플로우로 인해 수요가 높아질 전망입니다. 소모품은 연구실의 일상 업무를 유지하는 데 필수이며 이미 2024년 매출의 절반 가까이를 차지하였습니다. 한편, 장비의 혁신을 통해 대용량 스펙트럼 및 자동화 기능이 일상화될 전망입니다. 지역적으로는 북미가 국립위생연구소(NIH)와 국립과학재단(NSF)의 관대한 기기 보조금으로 구매 페이스를 유지하고 있는 반면 아시아태평양은 바이오 제조 능력 확대를 배경으로 두 자릿수의 성장을 기록하고 있습니다. 미국 식품의약국(FDA)은 2025년 멀티플렉스 항균제 감수성 세포 분석 시스템을 클래스 II 기기로 분류하여 고급 분석 플랫폼에 대한 신뢰를 보였습니다. Thermofisher Scientific사가 여러 해에 걸쳐 시행한 400억-500억 달러의 확장 예산과 같은 M&A는 규모와 포트폴리오의 폭이 장기적인 경쟁 우위를 결정한다는 것을 뒷받침하고 있습니다.

암, 심혈관 질환, 대사성 질환의 환자 수가 증가함에 따라 의료 시스템은 조기 발견을 우선시할 수 없게 되었고 증상이 나타나기 전에 미묘한 표현형의 변화를 발견할 수 있는 고처리량 세포 프로파일링 플랫폼에 대한 수요가 높아지고 있습니다. FDA가 2024년에 승인한 혈액 기반 분석인 Shield는 대장암의 검출 정밀도가 83%이며, 멀티파라메트릭 세포 분석이 주류의 스크리닝을 어떻게 지원하는지를 실증하고 있습니다. AI로 강화된 병리 조직 검사 알고리즘은 수작업보다 훨씬 효율적으로 유방 침윤성 종양의 패턴을 파악합니다. 2030년까지 35-45세 여성의 70%를 스크리닝해야 하는 자궁경부암 프로그램에서는 병리의 부족을 보완하기 위해 자동 슬라이드 리더가 채용되고 있습니다. 이러한 이용 사례는 임상 채용이 기술을 검증하고 나아가 세포 분석기 시장에 대한 추가 투자를 불러일으키는 피드백 루프를 형성합니다.

2024년에는 미국에서 1,200건이 넘는 세포치료와 유전자 치료의 임상시험이 실시되었기 때문에 스펙트럼 분류기, 대용량 이미저, 인프로세스 관리용 GMP 등급의 유동세포측정기 구입이 촉진될 전망입니다. 로슈사가 포세이다 세라퓨틱스사를 10-15억 달러에 인수한 케이스는 스케일 업시에 엄격한 세포 표현형 판정을 필요로 하는 동종 CAR-T 플랫폼의 확보를 서두르고 있는 상황을 부각시키고 있습니다. Tenpoint Therapeutics는 2025년 후반까지 첫 인간 망막세포 치료 연구를 계획하고 있으며, 분석 수요는 종양학 이외에도 확산되고 있습니다. 개발제조위탁기관(CDMO)은 소규모 바이오테크놀러지 기업의 능력 격차를 메우고 여러 고객을 수용하기 위한 분석 제품군을 구축함으로써 장비 판매를 강화하고 있습니다. 그 결과, 세포 분석기 시장에서는 GMP 환경에 최적화된 장비 플랫폼과 소모품 키트가 모두 성장하고 있습니다.

최첨단 스펙트럼 플로우 사이토미터, 대용량 이미저, 매스사이트 메트리 플랫폼은 가격이 50만 달러 이상인 경우가 많으며, 많은 교육 병원이나 공립 대학에서는 가격이 상승하고 있습니다. NIH는 이 갭을 메우기 위해 단품으로 75만-200만 달러를 지급하는 하이엔드 기기 보조금을 시도하고 있습니다. 하지만 대상이 되는 제안의 수는 여전히 이용 가능한 자금을 훨씬 웃돌고 있으며, 이는 바이오 래드의 2025년 1분기 학술용 매출액이 전년 동기 대비 5.4% 감소하였기 때문에 명확히 드러났습니다. 공동 이용 코어는 이용률을 향상시키지만 대기 시간을 늘리고 때로는 실험 일정에 지장을 초래합니다. 환율변동과 수입세는 신흥국 시장에서의 비용을 증폭시키고, 출하대수를 감소시키며, 수요가 급증하고 있는 세포 분석기 시장의 확대를 지연시킵니다.

소모품은 2024년 매출의 59.35%를 차지하였고 실험실이 장비 수명주기를 통해 분석 키트, 시약 및 일회용 카트리지를 재주문하므로 예측 가능한 마진을 제공합니다. BD FACSDiscover S8 스펙트럼 분류기는 고속 이미징과 기존 형광 기법을 결합하여 이 카테고리에서 최초로 표현형 기반 정렬을 실현했습니다. 요코가와의 CellVoyager CQ3000은 sCMOS 카메라를 이용한 오가노이드의 라이브 3D 이미징을 제공하여 단일 플레이트 분석 능력을 확대합니다. 새로운 광로와 온보드 AI가 프로토콜을 단축하기 때문에 연구실은 일반적인 7년간의 감가상각 곡선보다 빠르게 구식 하드웨어를 교환할 수 있고 이는 기기의 CAGR을 12.25%까지 높였습니다. 분광 광도계, 마이크로어레이 및 고급 현미경은 컴플라이언스 문서화를 자동화하는 클라우드 기반 분석 대시보드에 연결되어 공급업체를 세포 분석기 시장에 더 깊게 확립하게 하는 정기적인 소프트웨어 구독을 보장합니다.

2차 효과는 소모품 수요를 더욱 강화합니다. 인공지능 보조 분석에서는 한 번의 분석으로 더 많은 바이오마커를 다중화하는 경우가 많아 시약 풀스루가 증가합니다. 스펙트럼 유동 세포 계측법은 좁은 발광 병에 최적화된 독자적인 염료 패널을 필요로 하기 때문에 기술의 채택은 직접적인 소모품 판매로 이어집니다. 이러한 요인을 종합하면 소모품이 판매의 주축으로 지속되는 반면, 고액의 하드웨어가 세포 분석기 업계의 연간 수익을 좌우하는 요인으로 유지됩니다.

북미는 2024년 매출액의 40.63%를 차지하였으며, NIH의 하이엔드 기기 보조금(1건당 75만-200만 달러)과 NSF의 2025년도 생명공학 예산(4억 2,100만 달러)에 의해 뒷받침되고 있습니다. 강력한 벤처 자금, 성숙한 바이오 의약품 클러스터, 조기 도입 문화가 다른 지역보다 일찍 실험실에 AI 대응 분석 플랫폼을 도입하도록 촉구했습니다. 시마즈 제작소의 새로운 멕시코 자회사는 2028년까지 150%의 사업 성장을 목표로 하고 있으며, 이는 장비 벤더가 시장에 자신이 있음을 보여주고 있습니다. 북미의 현재 세포 분석기 시장 규모는 고급 장비, 바이오프로세스 분석 및 클라우드 연결 데이터 서비스를 전문으로 하는 공급업체를 지원합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 11.91%로 가장 높은 성장률을 보일 전망입니다. 중국은 동남아시아의 바이오파마 투자를 목표로 세계의 희토류 생산량의 90%를 지배하고 있어 광학 부품 공급 확보에 영향을 미칩니다. 쿼드 바이오 제조 허브가 되고자 하는 인도의 야망으로 인도는 폐쇄형 GMP 분석 스위트 수요에 대응하게 됩니다. 일본의 니콘과 요코가와 전기는 최첨단 이미저를 공급하여 국내 도입으로 피드백됩니다. 그 결과, 세포 분석기 시장은 아시아의 다양한 경제권에서 제조비용의 우위성과 미개척의 대규모 임상분야 모두로부터 혜택을 누릴 수 있습니다.

유럽은 독일, 영국, 프랑스에 제약 기업이 집중되어 있기 때문에 견고한 설립 기반을 유지하고 있습니다. 조정된 연구 자금과 IVDR의 전개로 수요는 완만하면서도 안정된 궤도를 보이고 있습니다. 동유럽 국가들은 유럽연합의 구조기금을 이용하여 연구소 인프라를 현대화하고 향후 유닛 성장 포켓을 만들고자 합니다. 한편, 중동 및 아프리카에서는 병리실과 생명과학 교육시설의 근대화가 시작되고 있으며 주로 기술이전계약과 함께 시행되고 있습니다. 이 지역은 정부가 탄화수소 주도 경제에서 다각화됨에 따라 세계의 세포 분석기 시장에서 점유율이 작지만 상승하고 있습니다.

The cell analysis instruments market is valued at USD 22.94 billion in 2025 and is forecast to advance to USD 32.33 billion by 2030, translating into a steady 7.1% CAGR.

Demand rises as chronic disease management shifts toward early molecular detection, artificial-intelligence (AI) driven imaging, and large-scale single-cell sequencing workflows that are now affordable for mid-sized laboratories. Consumables keep laboratories operational on a daily basis and already account for nearly half of 2024 revenue, while instrument innovation pushes spectral, high-content, and automation features into routine bench work. Geographically, North America continues to set the purchasing pace through generous National Institutes of Health (NIH) and National Science Foundation (NSF) instrumentation grants, whereas Asia-Pacific registers double-digit growth on the back of expanding biomanufacturing capacity. Regulatory clarity is improving; the US Food and Drug Administration (FDA) in 2025 classified multiplexed antimicrobial susceptibility cell-analysis systems as Class II devices, signalling confidence in advanced analytical platforms. Mergers and acquisitions-such as Thermo Fisher Scientific's multi-year USD 40-50 billion expansion budget-underscore how scale and portfolio breadth will determine long-term competitive advantage.

Growing cancer, cardiovascular, and metabolic disorder caseloads force health systems to prioritise early detection, pushing demand for high-throughput cellular profiling platforms that can uncover subtle phenotypic changes before symptoms manifest. The FDA's 2024 approval of the Shield blood-based assay-with 83% colorectal cancer detection accuracy-demonstrates how multiparametric cell analysis supports mainstream screening. AI-enhanced histopathology algorithms now outperform manual reads in identifying invasive breast-tumour patterns. Cervical-cancer programmes that must screen 70% of women aged 35-45 by 2030 are adopting automated slide readers to compensate for pathologist shortages. These use cases cement a feedback loop in which clinical adoption validates technology and, in turn, draws further investment into the cell analysis instruments market.

More than 1,200 active US cell- and gene-therapy trials in 2024 propel purchases of spectral sorters, high-content imagers, and GMP-grade flow cytometers for in-process control. Roche's USD 1.0-1.5 billion acquisition of Poseida Therapeutics highlights the rush to secure allogeneic CAR-T platforms that require rigorous cell phenotyping during scale-up. Tenpoint Therapeutics plans first-in-human retinal cell therapy studies by late 2025, widening analytical demand beyond oncology. Contract development and manufacturing organisations (CDMOs) fill capability gaps for smaller biotechs, bolstering instrument sales as they build analytical suites to serve multiple clients. Consequently, the cell analysis instruments market sees growth in both instrument platforms and consumable kits optimised for GMP environments.

State-of-the-art spectral flow cytometers, high-content imagers, and mass cytometry platforms often list above USD 500,000, pricing out many teaching hospitals and public universities. NIH attempts to bridge the gap with High-End Instrumentation grants that award USD 750,000-2 million for single items. Yet the number of eligible proposals still far exceeds available funds, evidenced by Bio-Rad's 5.4% year-over-year decline in academic sales during Q1 2025. Shared-use cores improve utilisation but lengthen queue times, occasionally compromising experimental timelines. Currency swings and import levies amplify costs in developing markets, dampening unit shipments and slowing cell analysis instruments market penetration where unmet medical need is rising fastest.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Consumables generated 59.35% of 2024 revenue and deliver predictable margins because laboratories reorder assay kits, reagents, and disposable cartridges throughout an instrument's life cycle. Flagship instrument launches nevertheless propel top-line growth; the BD FACSDiscover S8 spectral sorter marries high-speed imaging with traditional fluorescence to enable phenotype-based sorting, a first for the category. Yokogawa's CellVoyager CQ3000 offers live 3-D imaging of organoids using sCMOS cameras, broadening single-plate analytical capacity. As new optical paths and on-board AI shorten protocols, laboratories replace older hardware earlier than the typical seven-year depreciation curve, supporting a 12.25% CAGR for instruments. Spectrophotometers, microarrays, and advanced microscopes plug into cloud-based analytic dashboards that automate compliance documentation, securing recurring software subscriptions that anchor vendors deeper into the cell analysis instruments market.

Second-order effects further reinforce consumable demand. AI-assisted assays often multiplex more biomarkers per run, increasing reagent pull-through. Spectral flow cytometry requires proprietary dye panels optimised for narrow emission bins, converting technique adoption directly into consumable sales. Collectively, these drivers ensure that consumables remain the volume backbone, while big-ticket hardware remains the swing factor in annual revenue for the cell analysis instruments industry.

The Cell Analysis Instruments Market Report is Segmented by Product (Instruments [Microscopes, Flow Cytometers, and More], and Consumables), Application (Cell Counting, Cell Viability, Cell Identification, and More), End-User (Academic and Research Institutes, Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retains leadership with 40.63% of 2024 revenue, anchored by NIH High-End Instrumentation grants of USD 750,000-2 million per award and USD 421 million in NSF biotechnology budget for fiscal 2025. Robust venture funding, a mature biopharma cluster, and early-adopter culture pushed laboratories to adopt AI-enabled analytical platforms ahead of other regions. Canada's federal innovation funds and Mexico's burgeoning contract-manufacturing footprint add to regional demand; Shimadzu's new Mexican subsidiary aims for 150% business growth by 2028, signalling instrument vendors' confidence in the market. The current cell analysis instruments market size for North America supports vendors specialising in premium instrumentation, bioprocess analytics, and cloud-connected data services.

Asia-Pacific registers the highest growth rate at 11.91% CAGR through 2030. China's pivot toward Southeast Asian biopharma investments and control of 90% global rare-earth output influences supply security for optical components. India's ambition to become a Quad biomanufacturing hub positions the region for demand in closed, GMP-compliant analytical suites. Japan's Nikon and Yokogawa supply cutting-edge imagers that feed back into domestic adoption, while South Korea invests heavily in precision-medicine infrastructure. Consequently, the cell analysis instruments market enjoys both manufacturing cost advantages and large untapped clinical segments across Asia's diverse economies.

Europe maintains a solid installed base thanks to clustered pharma activity in Germany, the United Kingdom, and France. Coordinated research funding, combined with IVDR roll-out, ensures a stable if moderate demand trajectory. Eastern European nations look to EU structural funds to modernise laboratory infrastructure, creating future unit-growth pockets. Meanwhile, the Middle East and Africa begin to modernise pathology labs and life-science education facilities, often bundled with technology-transfer agreements. These regions contribute a small but rising share of the global cell analysis instruments market as governments diversify away from hydrocarbon-driven economies.