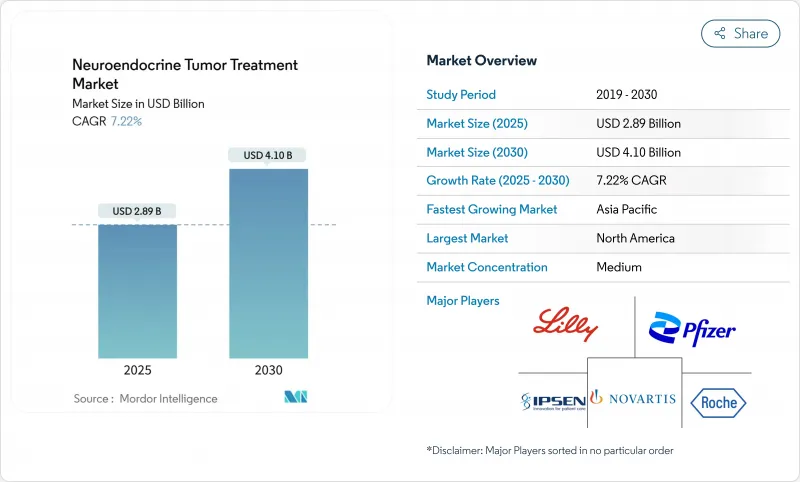

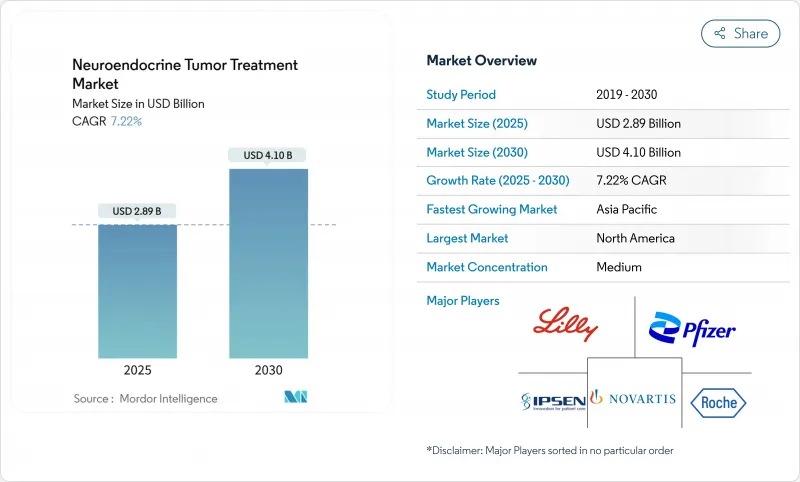

신경내분비종양 치료 시장은 2025년에 28억 9,000만 달러에 다다를 것으로 예상되며, 2030년에는 41억 달러에 이를 전망으로, CAGR 7.22%로 확대될 것으로 예측됩니다.

의료용 동위원소 가운데 특히 루테튬 177의 급속한 생산 능력 증진으로 기존 공급 병목 현상을 해소하고, 병원은 펩티드 수용체 방사성 핵종 요법(PRRT)을 최우선으로 채용할 수 있게 되었습니다. 또한 PRRT 지침, 희귀 질병 의약품의 우대 조치, NETTER-2의 데이터 질 개선으로 임상 수용이 계속 확대되고 있습니다. 투자자는 수직 통합 방사성 의약품 플랫폼을 지원하고, NETest와 같은 액체 생체활동 기술은 진단을 선명하게 하며 환자를 표적 약물에 적응시키는 데 도움을 줍니다. 의료 시스템은 ITM의 NOVA 플랜트와 큐륨의 네덜란드 사이트와 같은 대규모 거래에서 동위원소 공급 체인이 확장 가능하다는 것을 확신하고 있습니다.

영상진단의 꾸준한 개선과 인구의 고령화에 의해 이환율 상승으로 네덜란드에서는 2024년에 약 1,000건의 신규진단이 실시되었습니다. 의료제도는 NET전문센터를 시작하여 동위원소 능력에 자금을 제공함으로써 대응하고 있습니다. 임상 팀은 조기 병변을 감지하고 PRRT 및 표적 치료제의 후보자층이 확산되고 있습니다. 업계 조사에서 장기 치료가 필요한 소화기 췌장 NET 환자는 EU와 미국 전체에서 350,000명으로 추정됩니다. 이를 위해 통합 클리닉은 증가하는 사례 수를 효율적으로 관리하기 위해 표준화된 패스웨이를 채택합니다.

NETest 리퀴드 바이옵시는 기존의 크로모그라닌 A 측정법보다 정확하게 미세 잔존 병변을 추적하는 것으로 ENETS 센터 오브 엑셀런스에서 검증되었습니다. 고해상도 PET/CT와 결합하여 임상의는 종양의 생물학과 치료 반응을 거의 실시간으로 파악할 수 있습니다. 이 통합은 조기 치료 전환을 지원하고 현재 유럽에서 미국까지 퍼져있는 정밀 종양학 프로그램을 지원합니다. 이 업그레이드는 NET 치료에서 오랜 장벽이었던 진단 지연을 줄여줍니다.

루타세라 점적에는 차폐된 치료실, 방사선 모니터링, 전문 직원이 필요하며, 치료비 총액은 약가를 훨씬 웃돕니다. 유럽의 의료기술평가기관에서는 약물을 처방전에 추가하기 전에 비용 대 QALY의 결과를 조사하도록 되어 있습니다. 환자를 통합하고 중복을 줄이고 비용 효율성을 향상시키기 위해 통합 허브가 출현하고 있습니다.

소마토스타틴 유사체는 증상 대조군과 종양 안정화를 위한 오랜 사용을 반영하여 2024년 신경내분비종양 치료 시장에서 44.23%의 점유율을 유지했습니다. PRRT는 (177Lu)Lu-Oxodotreotide 커뮤니티에서의 보급에 힘입어 CAGR 10.32%로 성장할 것으로 예측되며 주요 성장 엔진으로서 두드러지고 있습니다. PRRT 프로토콜은 이탈리아 핵의학회의 새로운 가이드라인에 의해 통일되어 유럽에서의 보급을 뒷받침하고 있습니다. 제조의 병행적인 진보는 신뢰할 수 있는 동위원소의 흐름을 보장하고 기세를 더욱 유지하고 있습니다.

현재는 PRT와 소마토스타틴 유사체의 병용이나 연구 중의 DNA 수복 억제제와 PRT의 병용과 같은 병용 요법이 임상적으로 선호되어 치료 가능한 환자층이 확대되고 있습니다. 화학요법은 저분화암에 대해 여전히 사용되며 면역요법과 화학요법을 병용하는 새로운 임상시험을 통해 고악성도 암에 있어서의 시너지 효과를 탐구하고 있습니다. 에베로리무스와 카보잔티닙으로 대표되는 표적 치료는 방사성 핵종 치료에 적합하지 않은 환자에게 개별화된 옵션을 제공하며, 신경내분비종양 치료 시장이 다변화를 계속하고 있음을 강조합니다.

2024년 신경내분비종양 치료 시장의 규모는 북미가 39.87%의 점유율로 가장 높았습니다. 고가의 트레이서에 대한 메디케어의 개별 지불과 FDA의 적시 승인 실적이 조기 도입을 지원하고 있습니다. 미국의 주요 암센터에서는 이미 PRRT와 표적 치료제과 체크포인트 억제제를 통합한 임상시험이 실시되고 있으며, 캐나다에서는 보편적인 제도에 의해 PRRT의 주요 적응증이 전국적으로 환급되고 있습니다.

유럽에서는 EMA의 희귀 질병 치료제 패스웨이와 희귀 질병 치료제에 대한 액세스를 간소화하는 조정된 지불자 프레임워크의 혜택을 누리고 있습니다. 큐륨사의 네덜란드 Lu-177 라인을 필두로 현지 동위원소 생산 능력은 공급의 안전성을 강화하고 있습니다. 독일, 프랑스, 영국은 ENETS 인증 센터의 치밀한 네트워크를 구축하여 국경을 넘어 일관된 품질을 확보하고 있습니다. 남유럽 국가들은 EU의 통합 기금과 교육 프로그램 공유를 통해 능력을 확대하고 있습니다.

아시아태평양의 CAGR은 10.06%로 가장 높으며, 일본에서의 진단약의 신속한 규제 클리어런스와 중국의 종양학 인프라 정비가 그 원동력이 되고 있습니다. 호주는 Pharmaceutical Benefits Scheme 하에서 PRRT에 보조금을 내고 한국과 인도는 유럽의 동위원소 기업과 제휴를 맺고 있습니다. 지역 제조업체는 수입 지연을 피하기 위해 국내 공급망에 투자하여 신경내분비종양 치료 시장의 확대를 더욱 가속화하고 있습니다.

The neuroendocrine tumor treatment market is valued at USD 2.89 billion in 2025 and is forecast to reach USD 4.10 billion by 2030, expanding at a 7.22% CAGR.

Rapid capacity additions for medical isotopes, especially Lutetium-177, remove past supply bottlenecks and let hospitals adopt peptide receptor radionuclide therapy (PRRT) as a first-line option. Forthcoming PRRT guidelines, orphan-drug incentives and positive NETTER-2 data continue to widen clinical acceptance. Investors are backing vertically integrated radiopharmaceutical platforms, while liquid biopsy technologies such as NETest sharpen diagnosis and help match patients to targeted agents. Health systems also gain confidence from large deals-ITM's NOVA plant and Curium's Netherlands site-showing that the isotope supply chain can now scale.

Steadily improving imaging and population aging lift incidence, with Dutch registries counting nearly 1,000 new diagnoses in 2024. Health systems answer by launching specialist NET centers and funding isotope capacity. Clinical teams now detect earlier-stage disease, which broadens the candidate pool for PRRT and targeted agents. Industry surveys estimate 350,000 gastro-enteropancreatic NET patients across the EU and US who need long-term care. Multidisciplinary clinics thus adopt standardized pathways to manage rising caseloads efficiently.

NETest liquid biopsy tracks microscopic residual disease more accurately than legacy chromogranin A assays and is being validated across ENETS Centers of Excellence. When paired with high-resolution PET/CT, clinicians gain a near-real-time view of tumor biology and treatment response. This integration supports earlier therapy switches and underpins precision oncology programs now spreading from Europe to the United States. The upgrade shortens diagnostic delays, a long-standing barrier in NET care.

Lutathera infusions require shielded suites, radiation monitoring and specialist staff, pushing total treatment costs well above the drug price. Health technology assessment bodies in Europe now scrutinize cost-per-QALY results before adding agents to formularies. Multidisciplinary hubs are emerging to pool patient volumes, cut duplication and improve cost-effectiveness.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Somatostatin analogs retained 44.23% share in the neuroendocrine tumor treatment market during 2024, reflecting long-standing use for symptom control and tumor stabilization. PRRT, buoyed by community uptake of [177Lu]Lu-Oxodotreotide, is projected to log a 10.32% CAGR and stands out as the primary growth engine. PRRT protocols gained uniformity through the Italian Association of Nuclear Medicine's new guidelines, encouraging broader European uptake. Parallel advances in manufacturing assure a reliable isotope stream, further sustaining momentum.

Clinical preference now shifts toward combination regimens-PRRT plus somatostatin analogs, or PRRT alongside DNA-repair inhibitors under investigation-thereby widening the addressable population. Chemotherapy preserves its role for poorly differentiated carcinomas, while emerging immunotherapy-chemotherapy trials explore synergy in high-grade disease. Targeted therapy, led by everolimus and cabozantinib, offers individualized options for patients unsuitable for radionuclide therapy, underscoring how the neuroendocrine tumor treatment market keeps diversifying.

The Neuroendocrine Tumor Treatment Market Report is Segmented by Treatment Modality (Somatostatin Analogs (SSAs), Targeted Therapy, Chemotherapy, and More), Indication (Gastrointestinal, Pancreas, Lung and More), End User (Hospitals, Specialty/Oncology Clinics, and More), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 39.87% share of the neuroendocrine tumor treatment market size in 2024. Medicare's separate payment for high-cost tracers and the FDA's track record of timely approvals underpin early adoption. Major US cancer centers already integrate PRRT with targeted and checkpoint inhibitors in trial settings, while Canada's universal system reimburses core PRRT indications nationally.

Europe benefits from the EMA's orphan-drug pathway and coordinated payer frameworks that streamline access to rare-disease therapies. Local isotope capacity, notably Curium's Netherlands Lu-177 line, strengthens supply security. Germany, France and the United Kingdom host dense networks of ENETS-accredited centers, ensuring consistent quality across borders. Southern European nations expand capabilities through EU cohesion funds and shared training programs.

Asia-Pacific posts the highest 10.06% CAGR, powered by Japan's swift regulatory clearance of diagnostic agents and China's oncology infrastructure build-out. Australia subsidizes PRRT under the Pharmaceutical Benefits Scheme, while South Korea and India establish partnerships with European isotope firms. Regional manufacturers invest in domestic supply chains to avoid import delays, further accelerating neuroendocrine tumor treatment market penetration.