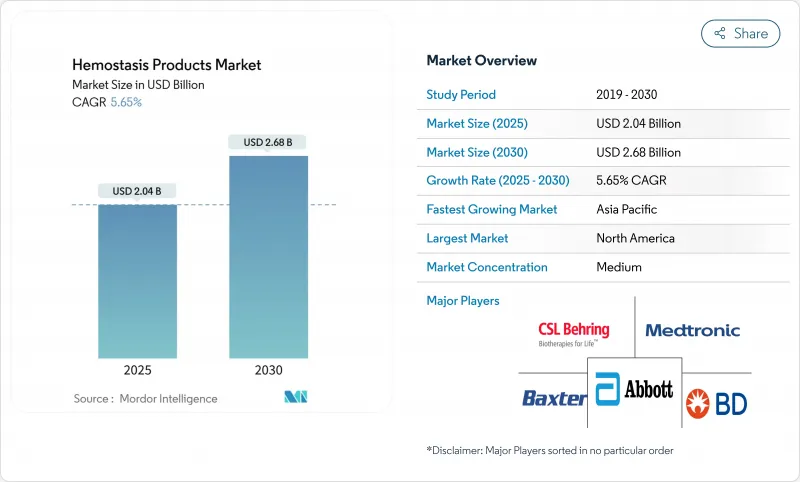

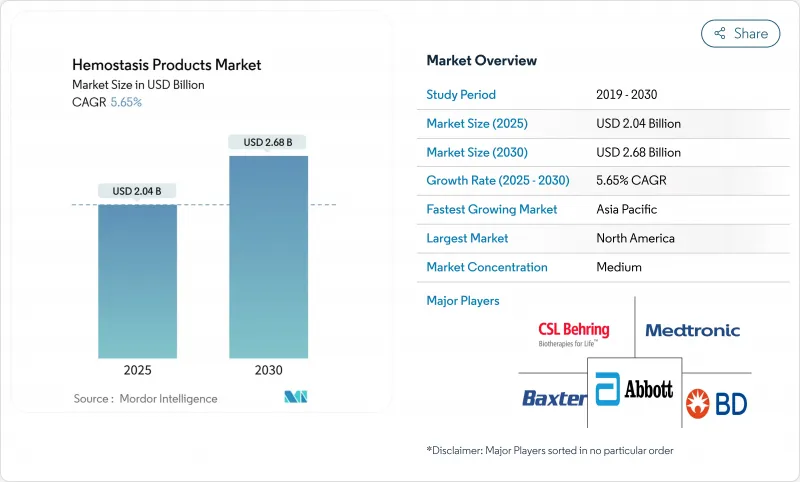

지혈 제품 시장은 2025년에 20억 4,000만 달러에 이를 전망으로, 2030년에는 26억 8,000만 달러로 확대될 것으로 예측되며, CAGR은 5.65%로 예상됩니다.

외상, 응급의료, 저침습 수술에 있어서 신속한 출혈 컨트롤에 대한 꾸준한 수요가 치료시간을 단축하고 수혈의 필요성을 줄이는 합성약제와 활성약제로 지혈 제품 시장을 이동시키고 있습니다. FDA가 승인한 심각한 출혈에 대한 Traumagel과 같은 차세대 솔루션에 대한 규제적인 승인은 견고한 임상 파이프라인을 확인하고 제품 출시를 가속화합니다. 병원은 수술실에서 효율성이 입증된 약물을 선호하며, 외과의사는 제한된 영역에서 정확한 적용을 제공하는 액체 및 스프레이 형식을 선호합니다. 출혈 관리의 모든 영역에서 포트폴리오를 추구하는 주요 의료 기술 기업의 통합은 차별화된 기술의 전략적 가치를 보여줍니다. 한편, 허리케인과 관련된 공급 부족으로 인해 중요한 자원에 대한 단일 시설 제조의 취약성이 드러났기 때문에 정책 입안자는 공급의 탄력성을 조사하기 시작했습니다.

세계적으로 수술 수는 증가하는 경향에 있으며 남아시아에서만 16억 명의 환자가 의료 서비스 접근 부족에 직면하고 있습니다. 손상 통제 및 소생 가이드라인의 갱신은 기도 관리보다 출혈 통제를 우선시하고, 실혈 사망률이 65% 감소하면서 신속한 국소 약물에 대한 최전선 수요가 확대되고 있습니다. 군 현장 의료에서 특히 합동 외상 시스템은 조기 혈액 제제의 사용을 정상화하고 있으며, 이러한 프로토콜은 민간 외상 네트워크에 보급되고 있습니다. 이러한 변화는 교통사고에서의 트리아지부터 고급 수술실에 이르기까지 환자 관리의 모든 단계에 출혈 컨트롤을 통합하여 지혈 제품 시장을 확대하고 있습니다. 진단제, 국소 젤, 농축 인자를 결합한 통합 키트를 제공하는 공급업체는 합리적인 조달을 요구하는 병원의 수요를 흡수할 것으로 보입니다.

자가조립 펩티드 하이드로겔은 수 초 안에 지혈에 도달하고 시각화를 위해 투명성을 유지하며 동물 조직과 관련된 병원체 전파 위험을 억제합니다. 순차 가교형 피브린 접착제는 15초 이내에 이중 메쉬 씰을 형성하여 중합에 수 분이 소요되는 기존의 피브린 실란트를 능가합니다. 공유결합적으로 반응하는 미립자는 동맥압 하에서도 강화 혈전을 형성하여 전임상 모델에서 20초 이하의 조절을 달성하였습니다. 식물 유래 Traumagel의 FDA 승인은 생물학적 활성제의 상업적 경로를 제시합니다. 이 혁신의 웨이브는 지효성 혈장 기반 약물을 대신하여 최신 수술 워크플로우에 원활하게 통합하는 민첩한 제형을 제공하여 지혈 제품 시장을 활성화합니다.

FDA는 최근 점탄성 응고 분석기를 클래스 II로 전환하여 장비 제조업체에 품질 시스템과 임상 데이터에 대한 부담을 강요하고 있습니다. 유럽의 의료기기 규제는 심사 대기를 길게 하고, 소규모 기업의 제품 출시를 지연시키며, 지혈 제품 시장을 규제 인프라를 가지고 있는 기존 기업으로 이동시키고 있습니다. CMS의 새로운 번들 규칙은 자기 혈액 유래 드레싱 재료의 적용 범위를 좁힐 수 있으며, 병원은 확실한 결과로 인해 비용이 많이 드는 지출을 정당화해야 할 필요가 없습니다.

수액요법은 2024년에 지혈 제품 시장 점유율의 35.55%를 차지했으며, 이는 농축인자가 대출혈이나 혈우병 관리에 있어서 여전히 필수적인 요소이기 때문입니다. 그러나 유전자 치료와 FXIa 억제제의 진전에 따라 수요는 두드러지고 있습니다. 지혈 제품 시장은 속도, 접착성, 면역원성의 성능 갭에 대응하는 합성 및 생체 모방형의 활성 실란트로 이동하고 있습니다.

첨단 제품은 2030년까지 연평균 복합 성장률(CAGR) 10.25%로 성장해 시장 확대의 페이스를 잡을 것으로 예측됩니다. FDA에 의한 VISTASEAL과 식물 유래 Traumagel의 승인은 신규 활성제의 승인에 대한 규제 당국의 의욕을 나타냅니다. 다국적 기업이 기술 접근을 위해 신흥 기업을 인수하고, Stryker사가 49억 달러를 투자하여 Inari사를 인수함으로써 말초 혈관 영역이 확대되는 등 경쟁의 강도가 증가하고 있습니다.

복강경 포트와 로봇 암에서 투여할 수 있는 혼주 불필요 시스템에 대한 외과의의 기호를 반영하여 액체 및 스프레이 형식이 2024년 매출의 38.53%를 차지했습니다. 지혈 제품 시장 규모에서 이 부문은 복잡한 해부학적 구조에 맞게 유량을 조절하는 배터리 구동 어플리케이터와 같은 전달 장치의 기술 혁신으로부터 이익을 얻고 있습니다.

매트릭스 겔 시스템은 순차 가교 화학 반응으로 습윤 조직에서도 15초간의 밀봉을 실현하기 위해 CAGR 8.15%로 진전하고 있습니다. 초탄성 기재를 사용한 순간 접착 패치는 장기의 움직임을 방해하는 기존 패드 대비 장점으로 흉부와 심장 수복에 지혈 제품 업계를 확대하고 있습니다.

북미는 2024년 매출의 42.72%를 차지했으며, 높은 수술 수, 엄격한 임상시험 인프라, 합성 혈액 프로그램에 대한 대규모 국방 연구개발 자금에 의해 그 지위가 강화되었습니다. FDA(미국 식품의약국)의 패스트트랙 패스웨이와 국방생산법은 공급 충격 후 국내 생산의 회복력을 촉진하여 중요한 지혈제의 안정적인 지역 공급에 기여하고 있습니다.

유럽 시장은 안전성 벤치마킹을 계속하고 있으며, EMA에 의한 마스타시맙과 에파네스 옥토코그알파의 승인은 이 지역의 혈우병 치료제의 리더십을 뒷받침하고 있습니다. 그러나 남반구의 경제권에서는 광범위한 전개에 앞서 비용 효과가 중요하기 때문에 채용에 편차가 있습니다. 의료기기 규제 일정은 성숙한 품질 시스템을 가진 기업에게 유리하며, 연속 포트폴리오를 추구하는 중견 기업과 선도적 전략 기업 간의 제휴를 촉구하고 있습니다.

아시아태평양은 병원 인프라의 현대화와 대기 수술의 해소와 함께 지혈 제품 시장에서 가장 빠르게 성장하는 지역입니다. 일본이 발표한 보존 기간 2년의 인공 혈액은 이 지역의 혁신 능력을 강조하는 사례입니다. 남아시아의 수술에 대한 접근 격차는 국민 모두를 대상으로 한 보험 제도의 확대와 함께 잠재 수요로 이어질 수 있습니다. 현지의 제조 장려책이 혈장 분획이나 펩티드 합성 공장에 대한 투자를 유치해, 수입 의존도를 줄이고 세계적 공급을 다양화하고 있습니다.

The hemostasis products market reached USD 2.04 billion in 2025 and is forecast to advance to USD 2.68 billion by 2030, translating into a 5.65% CAGR.

Steady demand for rapid bleeding control in trauma, emergency care, and minimally invasive surgery is shifting the Hemostasis products market toward synthetic and active agents that shorten procedure time and reduce transfusion needs. Regulatory greenlights for next-generation solutions-such as FDA-cleared Traumagel for severe bleeding-confirm a robust clinical pipeline and accelerate product launches. Hospitals are prioritizing agents with proven operating-room efficiency, while surgeons favour liquid and spray formats that deliver precise coverage in confined fields. Consolidation among large med-tech firms seeking full-spectrum bleeding management portfolios underlines the strategic value of differentiated technology. Meanwhile, policymakers have begun scrutinising supply resilience after hurricane-linked shortages exposed the fragility of single-site manufacturing for critical inputs.

Global surgical caseload is climbing, with South Asia alone facing a 1.6 billion patient access deficit that is now a policy priority. Updated damage-control resuscitation guidelines place hemorrhage control ahead of airway management, cutting exsanguination mortality by 65% and expanding front-line demand for rapid topical agents. Military field medicine-particularly the Joint Trauma System-has normalised early blood-product use, and its protocols are diffusing into civilian trauma networks. These changes enlarge the Hemostasis products market by embedding bleeding control into every step of patient management, from roadside triage to advanced operating suites. Suppliers offering integrated kits that combine diagnostics, topical gels, and factor concentrates will capture hospitals seeking streamlined procurement.

Self-assembling peptide hydrogels reach hemostasis in seconds, remain transparent for visualisation, and avoid pathogen transmission risks tied to animal tissue. Sequential-crosslinking fibrin glues form dual-network seals within 15 seconds, outperforming legacy fibrin sealants that need minutes to polymerise. Covalently reactive microparticles create fortified clots even under arterial pressure, achieving sub-20-second control in preclinical models. FDA clearance of plant-derived Traumagel validates the commercial pathway for biomimetic actives. This innovation wave lifts the Hemostasis products market by replacing slow, plasma-based agents with agile formulations that integrate seamlessly into modern surgical workflows.

The FDA recently shifted viscoelastic coagulation analysers into Class II, adding quality-system and clinical-data burdens for device makers. Europe's Medical Device Regulation has lengthened review queues, delaying small-company launches and tilting the Hemostasis products market toward incumbents with regulatory infrastructure. Payment reform is equally challenging; new CMS bundling rules could narrow coverage for autologous blood-derived dressings, forcing hospitals to justify premium spend through hard outcomes.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Infusible therapies retained 35.55% of the Hemostasis products market share in 2024 because factor concentrates remain essential during major bleeds and hemophilia management. Demand, however, is plateauing as gene therapy and FXIa inhibitors progress. The Hemostasis products market is pivoting toward synthetic and biomimetic active sealants that address performance gaps in speed, adhesion, and immunogenicity.

Advanced offerings are projected to grow at 10.25% CAGR through 2030, setting the pace for market expansion. FDA approval of VISTASEAL and plant-based Traumagel illustrates regulatory willingness to endorse novel actives. Competitive intensity is rising as multinationals acquire start-ups for technology access, with Stryker's USD 4.9 billion Inari acquisition broadening peripheral vascular reach.

Liquid and spray formats captured 38.53% of 2024 revenues, reflecting surgeon preference for no-mix systems that can be deployed through laparoscopic ports or robotic arms. This slice of the Hemostasis products market size benefits from delivery-device innovation, including battery-powered applicators that modulate flow rates for complex anatomy.

Matrix-gel systems are advancing at 8.15% CAGR as sequential-crosslinking chemistries deliver 15-second seals even on moist tissue. Instantly adhesive patches using ultra-elastic substrates extend the Hemostasis products industry to thoracic and cardiac repairs where organ motion frustrates traditional pads.

The Hemostasis Products Market Report is Segmented by Product (Topical Hemostasis, Infusible Hemostasis, and Advanced Hemostasis), Formulation (Matrix & Gel, Powder, and More), Application (Trauma, Surgery, Myocardial Infarction, and More), End User (Hospitals, Clinics, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 42.72% of 2024 revenues, a position reinforced by high surgical density, rigorous clinical-trial infrastructure, and sizeable defence R&D funding for synthetic blood programmes. FDA fast-track pathways and the Defence Production Act have together promoted domestic production resilience after supply shocks, helping stabilise regional availability of critical hemostats.

European markets continue to set safety benchmarks; EMA approvals for marstacimab and efanesoctocog alfa confirm the region's leadership in hemophilia therapeutics. Adoption varies, however, with southern economies scrutinising cost-effectiveness before broad rollout. Medical Device Regulation timelines favour firms with mature quality systems, encouraging partnerships between mid-caps and large strategics seeking contiguous portfolios.

Asia-Pacific is the fastest growing area of the Hemostasis products market as hospital infrastructure modernises and elective surgery backlogs unwind. Japan's announcement of a two-year shelf-life synthetic blood underscores regional innovation capability. South Asia's surgical access gap creates latent demand likely to unlock as universal health-coverage schemes expand. Local manufacturing incentives are attracting investment into plasma fractionation and peptide synthesis plants, reducing import reliance and diversifying global supply.