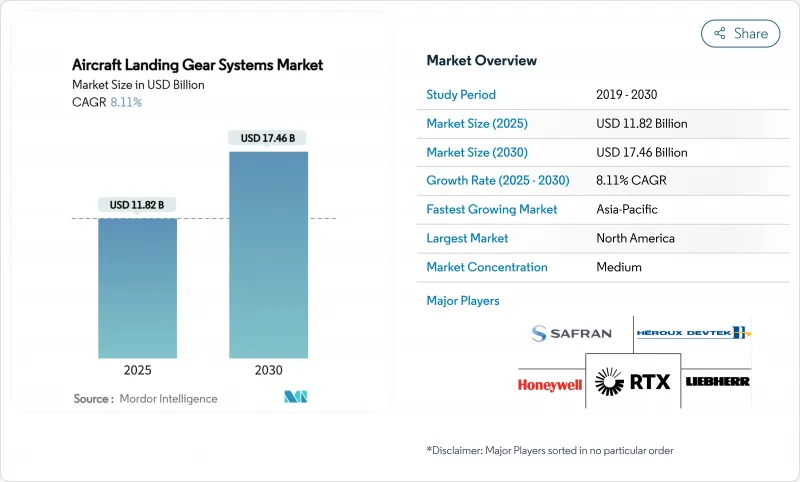

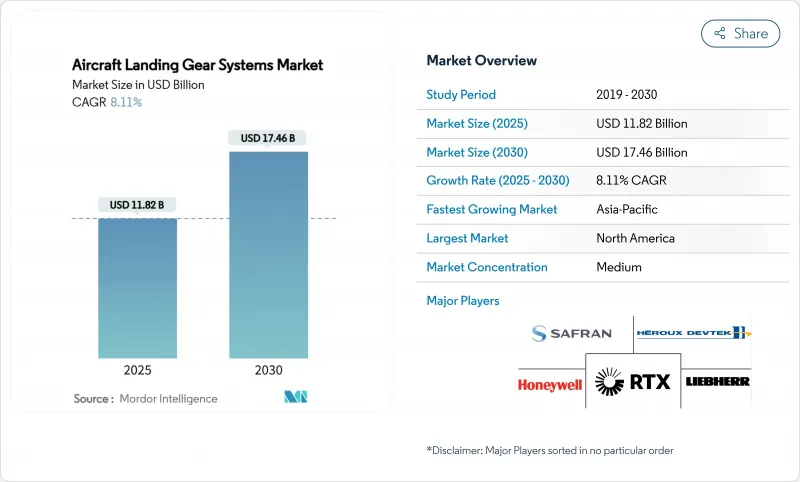

항공기 착륙장치 시스템 시장 규모는 2025년에 118억 2,000만 달러로 평가되었고, 2030년에 174억 6,000만 달러에 이를 것으로 예측되며, CAGR 8.11%로 성장할 전망입니다.

기체 교체 프로그램, 장거리 여행의 회복, 전기 구동 기술의 부상이 수요를 촉진하고 있습니다. 상업용 항공기 제조사들은 기록적인 주문 잔고를 처리하기 위해 생산을 가속화하고 있으며, 국방부들은 전술 기체를 현대화하고 있습니다. 항공사들은 기어 가용성을 보장하고 자본 노출을 낮추는 관리형 유지보수 계약으로 전환하고 있으며, 도시 항공 이동성(UAM) 프로토타입은 새로운 경량 및 고주기 틈새 시장을 개척하고 있습니다. 동시에 티타늄, 탄소섬유, 고정밀 주물 분야의 공급망 압박으로 인해 OEM 업체들은 핵심 단조품의 이중 조달을 추진하고 현지 생산 능력에 투자하고 있습니다.

항공기 제조사들은 티타늄 합금과 탄소섬유 복합재를 활용해 착륙장치 무게를 최대 30%까지 줄이고 있으며, 이는 연료 소모 감소와 항속 거리 연장으로 직접 연결됩니다. 도호쿠 대학이 개발한 티타늄-알루미늄 초탄성 합금은 -269°C에서 127°C까지 강도를 유지하여 극한 작동 환경에서의 적용 범위를 넓히고 있습니다. 보잉과 에어버스 와이드바디 기체는 이미 50% 이상의 CFRP 함량을 가진 기체를 채택했으며, 중국과 인도를 중심으로 한 지역 공급망은 수요에 부응하기 위해 탄소섬유 생산량을 확대하고 있습니다. 2024년 위조 티타늄 사건은 완전한 소재 추적성의 중요성을 부각시켰다. 군용 프로그램은 우수한 파단 인성을 위해 AerMet 310과 같은 초고강도 강재를 선호하며, 이는 소재 선택의 다양화를 더욱 촉진하고 있습니다.

주요 공급사들은 중앙 유압 회로를 분산형 전기-유압식 액추에이터로 대체하여 배관 복잡성을 줄이고, 유지보수 시간을 대폭 단축하며, 시스템 중량을 낮추고 있습니다. 콜린스 에어로스페이스는 eBrake 수요 충족을 위해 스포캔 소재 탄소 브레이크 공장에 70,000평방피트(약 6,500㎡)를 증설하는 데 2억 달러를 투자하여 생산 능력을 50% 증대했습니다. 클린 항공 전기식 앞바퀴 착륙장치 시스템 시제기는 완전 전기식 조향 및 수납 모듈을 검증하며 무유압 구조로 나아가고 있습니다. 인증 팀은 이제 새로운 고장 모드를 평가해야 하지만, 전기식 솔루션은 향후 항공기를 위한 모듈식 업그레이드와 원활한 확장성을 약속합니다.

항공우주 수요 증가로 인해 대형 300M 및 Ti-6-4 빌릿을 중심으로 단조 리드 타임이 12개월 이상으로 연장되었습니다. 전 세계 항공우주용 탄소섬유 사용량 22,000톤에 비해 중국은 약 7,000톤만 생산하여 가격 상승과 복합재 스파 생산 지연을 초래하는 공급 격차를 발생시키고 있습니다. OEM 업체들은 이중 조달 및 자체 단조 라인 구축으로 위험을 완화하고 있으나, 숙련된 인력 부족과 인증 심사 문제로 신속한 규모 확대가 제한되고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

2024년 상업용 플랫폼 항공기 착륙장치 시스템 시장 규모는 좁은 동체 제트기가 43.55%의 시장 점유율을 차지하며 가장 컸습니다. 항공사들이 노후화된 기단을 교체하고 연료 소비 절감을 추구했기 때문입니다. 에어버스의 주문 잔고는 예상되는 단일 통로 항공기 인도량의 40%를 차지하여 2030년까지 지속적인 물량을 시사합니다. 대륙간 노선 재개로 와이드바디 프로그램이 안정적 생산을 재개했으며, 화물기 전환 수요로 트윈아일 라인도 가동률이 유지되었습니다. 군사 수요는 정부 차원의 전투기 및 급유기 함대 재구축과 기존 항공기 수명 연장으로 8.85% CAGR을 기록하며 더 빠르게 증가하고 있습니다. 미국 국방부는 2018년부터 2023년까지 전술 항공기 운영에 572억 달러를 배정했습니다. 아시아 전역에서 일본, 인도, 한국은 착륙장치 조립에 현지 부품을 명시한 자체 개발 전투기를 도입하며 공급망 지도를 다각화하고 있습니다. 비즈니스 제트기와 회전익기 부문은 여전히 틈새 시장이지만, 대량 생산 항공기로 이전되는 전기기계 구동 및 적층 제조 기술의 중요한 시험장 역할을 합니다.

상업 운영사가 구매 물량을 주도하겠지만, 군수 프로그램은 특히 부식 방지 합금 및 자동 수납 진단 분야에서 연구개발 지출 비중이 더 커질 전망입니다. 블렌디드 윙 바디 시제기가 개발되면서 기어 위치 하중이 변화함에 따라, 군용 시제기가 선행 도입하는 스프링 스트럿 혁신이 촉진됩니다. 이러한 기술 확산은 상용화 시기를 단축하며 항공기 착륙장치 시스템 시장 전반을 지원합니다.

2024년 항공기 착륙장치 시스템 시장 점유율에서 메인 언더캐리지 유닛이 63.45%를 차지했으며, 이는 구조적 중량, 복잡한 트럭 어셈블리, 고가 브레이크 팩을 반영한 결과입니다. 트윈 에이슬 설계는 560톤 이상의 착륙 중량을 요구할 수 있어, 견고한 열처리 강재, 중복 충격 흡수 장치, 다중 휠 보기(bogies)가 필요합니다. 디지털 브레이크 바이 와이어 업그레이드와 탄소/탄소 디스크는 정비소를 바쁘게 하며, 모든 A-체크 주기마다 애프터마켓 수익을 유지합니다.

노즈 기어 물량은 적지만 성장세는 더 강해 2030년까지 연평균 9.55% 성장률을 기록할 전망입니다. 전기식 조향 액추에이터가 무게 절감을 주도하고, 모듈식 전기-기계식 잭스크류 어셈블리는 현장 교체 가능 유닛 수를 대폭 줄입니다. 클린 에비에이션의 노즈 기어 시제품은 기체당 수 킬로그램을 절감할 수 있는 전기-정수압식 수납 방식을 검증했습니다. 비즈니스 제트기 제조사들이 초기 도입자로 나서고 있으며, 리브헤르가 NBAA-BACE 2024에서 공개한 고신뢰성 노즈 기어 프로토타입은 eVTOL 및 지역 제트기 수주 확보를 위한 발판을 마련했습니다.

북미는 2024년 매출의 37.89%를 차지하며 최대 지역 기여자로 남아 있습니다. 보잉의 렌턴 및 에버렛 생산라인, 콜린스의 스포캔 브레이크 공장, 프랫 앤 휘트니의 착륙장치 가공 센터는 민간 및 국방 주문을 공급하는 밀집된 공급망의 핵심을 이루고 있습니다. 미국 국방 예산은 고강도 정비 주기를 보장하며, 캘리포니아와 텍사스를 중심으로 부상하는 항공 이동성 생태계는 곧 수천 개의 경량 선박 세트가 필요할 것입니다. 2024년 FAA의 위조 티타늄 조사 등 규제 감독 강화로 주요 업체들은 금속 시험을 내부에서 수행하는 비중을 늘리고 있습니다.

아시아태평양 지역은 중국, 인도, 동남아시아의 급증하는 항공 수요를 바탕으로 연평균 8.32% 성장률로 가장 빠르게 확장 중입니다. 에어버스는 향후 20년간 전 세계 제트기 인도량의 45%가 이 지역에 집중될 것으로 전망하며, 중국항공기제조그룹(COMAC)의 C919 인증은 자국 내 공급망 구축을 가속화하고 있습니다. 중국의 탄소섬유 생산은 여전히 산업용 등급에 치우쳐 있어 국제 프리프레그 전문 기업과의 합작 투자를 촉진하고 있습니다. 항공우주 산업의 오랜 전통을 가진 일본과 한국은 지역 제트기와 전투기 프로그램을 지원하는 초고성형성(SPF) 가공 설비를 확장 중입니다.

유럽은 사프란 랜딩 시스템즈, 리버 에어스페이스, 주요 에어버스 공장을 보유하며 강력한 기술 우위를 유지합니다. EU의 지속가능성 규제는 착륙장치 하드웨어의 전기화 로드맵과 수명 주기 영향 공개를 촉진합니다. 폴란드와 체코의 동유럽 클러스터는 정밀 가공 하위 조립품에 대한 투자를 유치합니다. 중동, 라틴 아메리카, 아프리카 운영사들은 규모는 작지만 전략적 거점 역할을 하며, 지리적 이점을 활용해 장거리 허브 앤 스포크 네트워크와 유연한 MRO 가용성이 필요한 전세기 부문을 지원합니다.

The aircraft landing gear systems market size stands at USD 11.82 billion in 2025 and is forecasted to reach USD 17.46 billion by 2030, advancing at an 8.11% CAGR.

Fleet renewal programs, the return of long-range travel, and the rise of electric-actuation technologies are fuelling demand. Commercial airframers are accelerating production to work through record backlogs, while defense ministries are modernizing tactical fleets. Airlines are shifting to managed maintenance agreements that guarantee gear availability and lower capital exposure, and urban-air-mobility prototypes are opening new low-weight, high-cycle niches. At the same time, supply-chain pressures around titanium, carbon fiber, and high-precision castings are forcing OEMs to dual-source critical forgings and invest in local capacity.

Airframers are deploying titanium alloys and carbon-fiber composites to trim landing-gear weight by up to 30%, translating directly into lower fuel burn and longer range. A titanium-aluminum super-elastic alloy developed by Tohoku University maintains strength from -269°C to 127°C, widening its applicability across extreme operating environments. Boeing and Airbus wide-bodies already feature airframes with more than 50% CFRP content, and regional supply chains across China and India are scaling carbon-fiber output to keep pace with demand. The 2024 investigation into counterfeit titanium underscored the importance of full material traceability. Military programs favour ultra-high-strength steels such as AerMet 310 for superior fracture toughness, further diversifying material choices.

Leading suppliers are replacing central hydraulic circuits with distributed electro-hydrostatic actuators to reduce pipeline complexity, slash maintenance hours, and lower system weight. Collins Aerospace invested USD 200 million to add 70,000 sq ft at its Spokane carbon-brake plant, boosting capacity by 50% to meet eBrake demand. The Clean Aviation Electrical Nose Landing Gear System demonstrator validates full electric steering and retraction modules, moving towards zero-hydraulic architectures. Certification teams must now evaluate new fault modes, but electric solutions promise modular upgrades and smoother scalability for future aircraft.

Accelerating aerospace demand has lengthened forging lead times past 12 months, especially for large 300M and Ti-6-4 billets. China produces only about 7,000 MT of aerospace-grade carbon fiber against global use of 22,000 MT, leaving a gap that drives prices higher and slows composite spar production. OEMs fund dual-sourcing and in-house forging lines to mitigate exposure, yet skilled-labor shortages and certification audits restrict rapid scale-up.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The aircraft landing gear systems market size for commercial platforms remained the largest in 2024, driven by narrowbody jets that captured 43.55% market share as carriers renewed ageing fleets and chased fuel-burn savings. Airbus's backlog covers 40% of projected single-aisle deliveries, implying sustained volume through 2030. Widebody programs resumed steady output as intercontinental routes reopened, and freight conversions kept twin-aisle lines busy. Military demand is rising faster, posting an 8.85% CAGR as governments recapitalise fighter and tanker fleets and extend lifecycles on legacy aircraft. The US Department of Defense allocated USD 57.2 billion to tactical-aircraft operations between 2018 and 2023. Across Asia, Japan, India, and South Korea are inducting indigenous fighters that specify local content in landing-gear assemblies, diversifying the supplier map. Business-jet and rotorcraft segments remain niche yet important incubators for electro-mechanical actuation and additive manufacturing practices that migrate to higher-volume airliners.

Commercial operators will continue to dominate procurement volumes, but military programs will account for a larger share of R&D spending, particularly in corrosion-resistant alloys and automatic retraction diagnostics. As blended-wing-body demonstrators proceed, gear-position loads shift, encouraging spring-strut innovations that military prototypes often adopt first. The spillover accelerates technology maturity, shortening the time to commercial adoption and supporting the broader aircraft landing gear systems market.

Main undercarriage units sustained 63.45% of the aircraft landing gear systems market share in 2024, reflecting their structural heft, complex truck assemblies, and high-value brake packs. Twin-aisle designs can impose landing weights above 560 tons, demanding robust heat-treated steels, redundant shock absorbers, and multi-wheel bogies. Digital brake-by-wire upgrades and carbon/carbon discs keep repair shops busy, sustaining aftermarket revenues at every A-check cycle.

Nose gear volumes are lower, yet growth is stronger, tracking a 9.55% CAGR to 2030. Electric steering actuators spearhead weight cuts, and modular electro-mechanical jackscrew assemblies slash line-replaceable-unit counts. Clean Aviation's nose-gear demonstrator validates electro-hydrostatic retraction methods that can shave several kilograms per shipset. Business-jet makers are early adopters; Liebherr's high-reliability nose-gear prototype, unveiled at NBAA-BACE 2024, positions the company to capture both eVTOL and regional-jet awards.

The Aircraft Landing Gear Systems Market Report is Segmented by Aircraft Type (Commercial Aviation, Military Aviation, and General Aviation), Gear Position (Nose Landing Gear and Main Landing Gear), Material (High-Strength Steel Alloys, Titanium Alloys, Composites, and More), End-User (OEM and Aftermarket (MRO)) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America remained the largest regional contributor with 37.89% of 2024 revenue. Boeing's Renton and Everett lines, Collins's Spokane brake factory, and Pratt & Whitney landing-gear machining centers anchor a dense supplier footprint that feeds civil and defense orders. US defense budgets guarantee high-tempo overhauls, and the emerging air-mobility ecosystem centred in California and Texas will soon require thousands of lightweight shipsets. Regulatory scrutiny, including a 2024 FAA probe into counterfeit titanium, has tightened oversight, nudging primes to in-source more metallurgical testing.

Asia-Pacific is the fastest-expanding arena, rising at an 8.32% CAGR on the back of burgeoning traffic in China, India, and Southeast Asia. Airbus forecasts that the region will absorb 45% of global jet deliveries over two decades, and COMAC's C919 certification accelerates indigenous supply chains. China's carbon-fiber output remains skewed to industrial grades, encouraging joint ventures with international prepreg specialists. Japan and South Korea, with long aerospace pedigrees, are scaling super-plastic-forming operations that support regional jet and fighter programs.

Europe retains a strong technology edge, housing Safran Landing Systems, Liebherr-Aerospace, and major Airbus plants. EU sustainability mandates incentivise electrification roadmaps and life-cycle impact disclosures for landing-gear hardware. Eastern European clusters in Poland and the Czech Republic attract investment for precision-machined sub-assemblies. Middle-East, Latin American, and African operators form smaller but strategic nodes, leveraging geographic positioning to serve long-haul hub-and-spoke networks and charter segments that require flexible MRO availability.