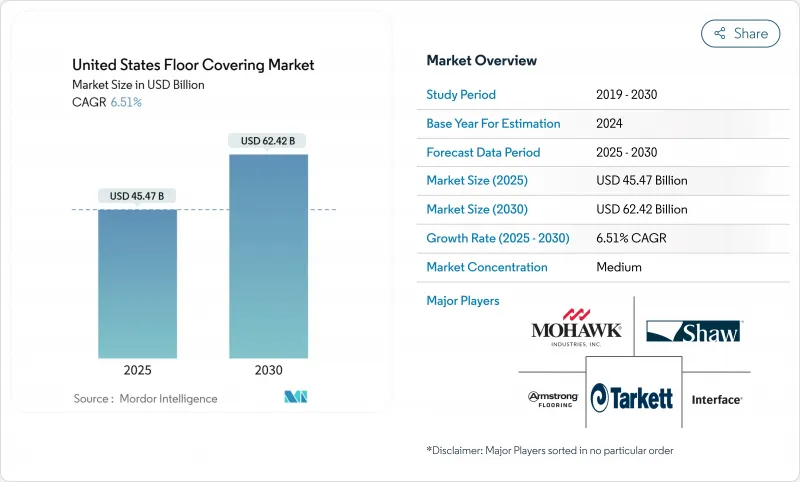

미국의 바닥재 시장의 규모는 2025년에 454억 7,000만 달러, 2030년에는 624억 2,000만 달러에 이를 전망이며, CAGR 6.51%로 확대될 것으로 예측되고 있습니다.

미국의 바닥재 시장의 현재 기세를 뒷받침하는 것은 주택 개보수 활동, 탄성 제품의 혁신, 선벨트 지역의 강력한 인구 증가입니다. 수요는 세금 혜택이 있는 상업시설의 보수 활동에 의해 강화되어 높은 차입비용에 따른 손실을 상쇄합니다. 대규모 제조업체는 방수성과 내상성이 뛰어난 기술에 주력하며, E-Commerce에 의한 소비자 직접 판매는 급속하게 시장 모델을 바꾸고 있습니다. 지속적인 원재료 인플레이션과 심각한 시공업체 부족은 미국 바닥재 시장의 밝은 전망을 약화시키는 주요 비용 압력이 되고 있습니다.

비과세대상이 확대됨에 따라 지금까지 바닥의 교체가 지연된 정부기관과 비영리시설에 대한 수요가 발생합니다. 보수 공사는 팬데믹 후의 인테리어의 재구성과 연동되어 있기 때문에 방음 성능과 차열 성능 모두를 실현하는 바닥재의 업그레이드가 가장 높은 우선순위를 갖게 되었습니다. 설계 회사는 세금 스케줄에 따라 입찰을 수행하므로 밀집한 상업 지구의 시공업자에게 안정적인 수주가 발생하고 있습니다. 이 변화는 에너지 목표를 충족시키면서 재활용 소재를 통합한 고급 탄성 타일 카펫과 타일 카펫 플랫폼을 지원합니다.

하이브리드 워크 모델은 좌석 계획의 변경 시 들어 올려 다시 깔 수 있는 모듈식 바닥재 수요를 자극하고 있습니다. 타일 카펫은 임대 재협상 시 사업자가 신속한 해결책을 요구하면서 대유행 전의 상업 예측을 웃도는 수량을 달성하였습니다. 디자이너는 발의 편안함과 의자 바퀴 등에 대한 내구성의 균형을 고려한 제품을 선정합니다. 흡음 시스템은 오픈 공간의 소음을 줄이고 웰빙 인증을 지원합니다. 설치 영역이 좁은 경우 다운타임을 최소화하는 클릭 결합 시스템이 선호되며, 이는 공간 전환을 수익화하는 코워킹 제공업체가 갖는 특별한 특징입니다. 따라서 공급업체는 리드 타임을 연장하지 않고도 신속한 맞춤화를 가능하게 하는 염료 용융 인쇄 기술에 투자하고 있습니다.

상업용 부동산 거래량은 2023년에는 37% 감소하였고, 2024년에는 추가로 14% 감소하였습니다. 개발자의 투기적인 신축이 연기되어 대규모 코어 쉘 프로젝트의 바닥재 수요가 억제됩니다. 기존 오피스 빌딩의 공실은 리노베이션 사이클을 연장하고 임대인을 전반적인 플로어 교체보다는 단계적인 업그레이드로 이동시킵니다. 소매업의 설비투자도 전자상거래가 재량 지출을 받아들이면서 신중해지고 있습니다. 따라서 미국의 바닥재 시장은 제한된 예산 내에서 진행되는 리노베이션 프로그램에 중점을 둡니다. 공급업체는 가치 엔지니어링 라인을 대출 지원과 함께 번들로 제공하지만 게이트웨이 도시의 수량 부족은 계속해서 전반적인 성장을 억제하고 있습니다.

카펫과 러그는 집합 주택이나 사무실에서의 방음 효과로 2024년 미국 바닥재 시장의 36.01%를 차지하였습니다. 그러나 탄성 바닥재는 CAGR 7.91%와 미국 바닥재 시장 전체를 2.3포인트 가까이 웃도는 성장이 예측됩니다. 고급 비닐 타일과 리지드 코어 컬렉션은 방수 성능과 유지 보수 용이성을 실현하면서 채용되고 있습니다. 이 시프트는 엔트리 레벨의 가격대에서 현장 마감재나 세라믹 등의 비탄성 경질 표면으로부터 점유율을 이동시킵니다. 주목할 만한 것은 Mohawk의 PureTech로 대표되는 PVC 프리 탄성 소재가 지속 가능성을 중시하는 구매자들 사이에서 널리 받아들여지고 있다는 것입니다.

2024년에는 탄성 바닥재가 탄산칼슘 충전재의 비용 안정화에 의해 뒷받침되면서 리폼 성수기의 적극적인 판촉 가격 설정으로 이어졌습니다. 그 결과 SPC 클릭 결합판은 소셜 플랫폼을 통해 판매되는 소비자 직접 판매 번들에서 크게 인기를 얻었습니다. 제조업체 각사는 장기 보증의 대상이 되는 독자적인 마모층으로 수익을 확대해, 장기적 가치를 중시하는 주택 소유자의 공감을 모으고 있습니다.

미국의 바닥재 시장은 제품 유형별(카펫과 러그, 탄성 바닥재 럭셔리 비닐 타일(LVT), 기타), 최종 사용자별(주택, 상업 사무실), 유통 채널별(바닥재 전문 소매점, 대형 홈 센터 등), 지역별(북동부, 남동부 등)으로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

The US flooring market is valued at USD 45.47 billion in 2025 and is forecast to reach USD 62.42 billion by 2030, expanding at a 6.51% CAGR.

Residential renovation activity, resilient product innovation, and strong population growth in Sunbelt states underpin the current momentum of the US flooring market. Demand is reinforced by tax-advantaged commercial retrofits that offset the drag from high borrowing costs. Scale manufacturers concentrate on waterproof and scratch-resistant technologies, while direct-to-consumer e-commerce rapidly reshapes go-to-market models. Sustained raw-material inflation and an acute installer shortage remain the key cost pressures that temper the otherwise upbeat outlook of the US flooring market.

Expanded eligibility for tax-exempt entities unlocks demand from government and nonprofit facilities that have historically delayed floor replacements. Retrofits dovetail with post-pandemic reconfiguration of interiors, so flooring upgrades that deliver both acoustic and thermal performance rise to the top of specification lists. Design firms are aligning bids with tax schedules, creating a steady backlog for installers in dense commercial districts. The change supports premium resilient and carpet-tile platforms that incorporate recycled content while meeting energy targets.

Hybrid work models catalyze demand for modular flooring that can be lifted and re-laid when seating plans change. Carpet tile volumes surpassed pre-pandemic commercial forecasts as operators seek quick-turn solutions during lease renegotiations. Resimercial aesthetics blend soft textures with hard-surface accents so designers specify collections that balance underfoot comfort with chair-castor durability. Acoustic backing systems mitigate noise in open plans and support wellness certifications. Smaller installation zones favour click-lock systems that minimize downtime, a feature prized by co-working providers that monetize space churn. Suppliers are therefore investing in dye-infusion print technologies that enable rapid customization without extending lead times.

Transaction volumes in commercial real estate fell 37% in 2023 and a further 14% in 2024 . Developers defer speculative ground-ups, curbing floor covering demand in large core-shell projects. Vacancies in legacy office towers extend retrofit cycles, pushing landlords to phase upgrades rather than execute full-floor replacements. Retail capital expenditure is similarly cautious as e-commerce captures discretionary spending. The US flooring market thus shifts focus toward refurbishment programs that can proceed under constrained budgets. Suppliers bundle value-engineered lines with financing support, yet volume shortfalls in gateway cities continue to temper overall growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Carpets and rugs retained 36.01% of the US flooring market in 2024 due to acoustic benefits in multifamily housing and offices. However, resilient flooring is forecast to grow at a 7.91% CAGR, almost 2.3 percentage points above the overall US flooring market. Luxury vinyl tile and rigid core collections spearhead adoption because they deliver waterproof performance and easy maintenance. The shift pulls share from non-resilient hard surfaces such as site-finished wood and ceramic in entry-level price tiers. Notably, PVC-free resilient lines led by Mohawk's PureTech have broadened acceptance among sustainability-focused buyers.

In 2024, the resilient category also benefited from cost stabilization in calcium carbonate fillers, supporting aggressive promotional pricing during peak remodeling season. As a result, SPC click-lock planks featured prominently in direct-to-consumer bundles marketed through social platforms. Manufacturers augment margins through proprietary wear layers that qualify for extended warranties, a feature that resonates with homeowners concerned about long-term value.

The US Floor Covering Market Segments Into by Product Type (Carpet and Rugs, Resilient Flooring Luxury Vinyl Tile (LVT), and More), End-User (Residential, and Commercial Office), Distribution Channel (Specialty Flooring Retailers, Big-Box Home Centers, and More), Region (Northeast, Southeast, and More). The Market Forecasts are Provided in Terms of Value (USD).