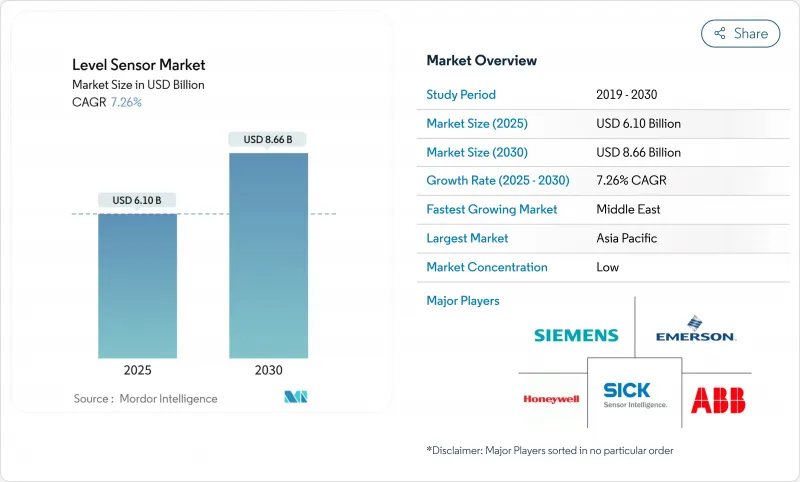

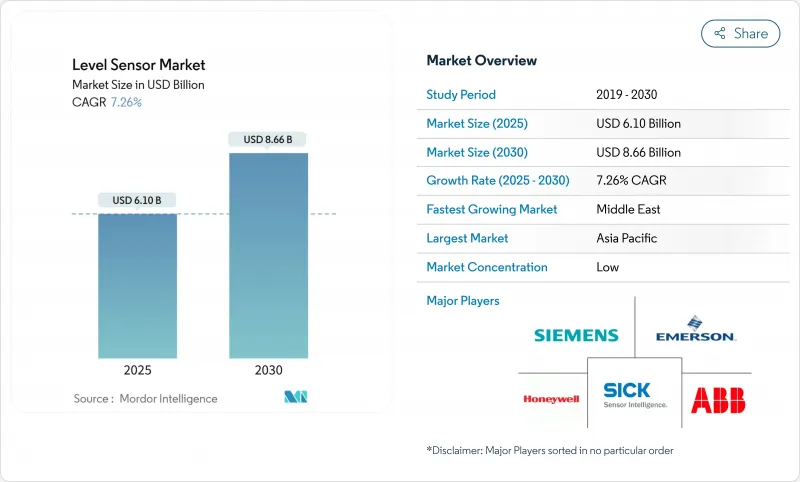

레벨 센서 시장 규모는 2025년에 61억 달러로 평가되며 CAGR 7.26%를 나타내 2030년에는 86억 6,000만 달러에 달할 것으로 예상됩니다.

산업 디지털화 프로그램, 세계 까다로운 안전 의무, 까다로운 용도에서 고주파 80GHz 레이더 플랫폼으로의 급속한 전환이 성장을 추진하고 있습니다. 아시아태평양의 해수 담수화 및 폐수 메가 프로젝트에 대한 공공 부문의 왕성한 지출이 유닛 수요를 가속화하고 있는 한편, 북미에서는 카스트디 트랜스퍼 업그레이드가 초고정도 레이더 설계의 프리미엄 가격을 강화하고 있습니다. 제조업체 각사는 또한 IoT 대응 트랜스미터와 자기 진단 기능을 포함한 제품 믹스를 확대해, 예지 보전 전략에 대응하려고 하고 있습니다. 세계 리더는 보완적인 센싱, 커뮤니케이션, 분석 기능을 결합한 인수와 제휴를 통해 포트폴리오를 강화하고 있어 경쟁의 격렬함이 증가하고 있습니다.

사우디아라비아와 아랍에미리트(UAE)의 적극적인 디지털 경제 지출은 실시간 재고 대시보드 및 예측 유지보수 모델에 공급하는 네트워크화된 레벨 트랜스미터 수요를 높이고 단말기 운영을 현대화하고 있습니다. Vision 2030 프로그램은 AI 및 5G 예산을 산업용 IoT로 향하게 하여 레벨 데이터를 ERP 및 배출 감시 시스템과 원활하게 통합할 수 있도록 합니다. 사업자가 기존의 플로트 게이지에서 SIL 인증 레이더 플랫폼으로 전환하고 있기 때문에 지역 밀착형 서비스 허브를 갖춘 공급업체는 평균을 초과하는 주문량을 목격하고 있습니다.

아시아태평양의 막식 해수 담수화 라인과 고급 생물학적 폐수 처리 설비 계획은 약물 주입 및 슬러지 공정을 관리하기 위해 정밀하고 부식성이 높은 수준의 감지가 필요합니다. 플랜트에는 현재 에너지 최적화를 위해 연속 레벨 데이터를 활용하는 AI 모듈이 내장되어 있어 고염분 매체용으로 평가된 레이더나 초음파 계기의 채용이 진행되고 있습니다. 세계 해수 담수화 용량의 46%를 차지하는 중동에 대한 병행 투자는 장기적인 장비 수요를 강화합니다.

유도로 부근의 고전자계가 전자 레벨 신호를 왜곡하고, 비용이 많이 드는 재교정 사이클을 촉진하고, 급속하게 성장하는 인도의 철강 섹터에 있어서의 레이더 센서의 도입을 제한하고 있습니다. 벤더는 다층 차폐 및 디지털 필터링을 테스트하고 있지만 가격에 민감한 사업자는 견고하고 저렴한 솔루션이 등장할 때까지 업그레이드를 연기하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

2024년 레벨 센서 시장 점유율은 포인트 디바이스가 58%를 차지하며 오버필 및 드라이런 세이프 가드의 바이너리 제어에 선호되었습니다. 연속 측정 제품은 출하량이 적은 것, 운전 자본 및 에너지 사용을 줄이기 위해 운영자가 실시간 재고 추적을 추구하고 있기 때문에 매년 8% 성장하고 있습니다. 연속 플랫폼을 위한 레벨 센서 시장 규모는 분석 대응 송신기의 채택과 함께 2030년까지 30억 달러 이상에 달할 것으로 예상됩니다. 스위칭 기능과 연속 기능을 하나의 인클로저에 융합한 하이브리드 기기는 공간에 제약이 있는 스키드로의 전환을 승리해, 공급자의 차별화를 넓히고 있습니다.

80GHz 레이더로의 전환은 거품, 수증기, 먼지와 싸우는 물, 화학 및 식품 공장에서 지속적인 부문 도입의 원동력이되었습니다. 통합 진단은 현재 축적에 플래그를 지정하고 사전 세척 프롬프트를 제공하고 가동 시간을 향상시킵니다. IO-Link 및 무선 프로토콜을 연속 게이지에 통합한 공급업체는 기계 제조업체가 스마트 센서 아키텍처를 표준화함에 따라 OEM 설계의 승리를 얻습니다.

접촉식 기술은 2024년 매출의 64%를 차지했고 기계적인 간편함이 평가된 정압식 프로브와 자왜식 프로브가 그 기둥이 되었습니다. 그러나 비접촉식은 식품, 의약품, 부식성 액체에 있어서의 오염이 없는 계측 수요를 타고 매년 8.2%씩 확대하고 있습니다. 레이더식과 초음파식은 접액부에 기인하는 다운타임을 회피하고, 블루투스 대응 유닛은 모바일 앱에 의한 시운전을 용이하게 합니다. 비접촉 플랫폼은 현재 레벨 센서 시장 규모의 3분의 1 가까이를 차지하고 있으며, 2029년까지 고가치 화학 및 에너지 프로젝트에서 접촉식 선적을 초과할 것으로 예측되고 있습니다.

레이더의 진보는 가장 두드러진다 : FMCW 아키텍처는 80GHz의 주파수를 활용하여 내부 구조를 탐색하는 얇은 빔을 실현합니다. 공급업체는 또한 교반기가 있는 탱크에서 거짓 에코를 제거하는 펌웨어의 진보를 추진하고 있습니다. 초음파는 특히 지자체의 수도 프로젝트 등 비용 감도가 성능을 능가하는 분야에서는 견인력을 유지하고 있지만 레이더의 가격 하락에 따라 점유율은 저하 경향이 있습니다.

아시아태평양은 2024년에 45%의 수익으로 레벨 센서 시장을 선도했습니다. 중국의 광범위한 산업 자동화와 인도와 동남아시아의 설비투자의 가속을 지지하는 배터리 전기자동차의 밸류체인만으로도 전해액, 슬러리, 용제탱크용으로 수천 개의 내약품성 레이더 게이지가 필요합니다. 도시화가 진행되는 지역의 폐수 인프라에서는 AI 주도의 제어 루프에 연결된 연속 센서의 주문이 증가하고 있습니다. 현지 생산 및 판매 후 네트워크에 투자하는 공급업체는 Tier2 및 Tier3 도시의 점유율을 확대합니다.

중동은 2025-2030년의 CAGR이 9%를 나타낼 전망입니다. 비전 2030 및 ADNOC 하류 프로젝트와 관련된 탱크 팜 자동화 프로그램, 더욱 기록적인 해수 담수화 용량 증가는 SIL 정격 레이더와 스마트 포인트 스위치에 대한 수요를 다년간 유지합니다. 인도 중동 유럽 경제 회랑과 같은 물류 회랑에서는 새로운 터미널과 파이프라인이 재고 모니터링을 필요로 하므로 센서 주문이 증가합니다.

북미에서는 80GHz 레이더에 의한 보관·이송 탱크의 근대화가 수익상 중요한 용적 계산을 위해 계속되고 있으며, 혈암 관련 수처리 사업에서는 퇴적물이나 탄화수소에 내성이 있는 초음파 장치나 레이더 장치가 채용되고 있습니다. 유럽의 화학 공업 단지는 SIL-3 업그레이드와 지속가능성 지표를 우선시하고 인증 레이더 유닛과 클라우드 대응 진단에 대한 수요를 끌어 올리고 있습니다. 남미의 광업과 펄프 사업은 점차 확대되는 반면, 현지 OEM은 국제 SIL 표준을 충족하는 비용면의 장애물에 직면해, 당면의 보급은 완만해집니다.

The level sensors market size is valued at USD 6.1 billion in 2025 and is forecast to reach USD 8.66 billion by 2030, advancing at a 7.26% CAGR.

Growth is propelled by industrial digitization programs, stringent global safety mandates, and the rapid shift to high-frequency 80 GHz radar platforms in demanding applications. Strong public-sector spending on desalination and wastewater megaprojects across Asia-Pacific is accelerating unit demand, while custody-transfer upgrades in North America reinforce premium pricing for ultra-high-accuracy radar designs. Manufacturers are also widening their product mix with IoT-ready transmitters and embedded self-diagnostics to align with predictive-maintenance strategies. Competitive intensity is rising as global leaders strengthen portfolios through acquisitions and alliances that combine complementary sensing, communications, and analytics capabilities.

Aggressive digital-economy spending in Saudi Arabia and the UAE is modernizing terminal operations, elevating demand for networked level transmitters that feed real-time inventory dashboards and predictive-maintenance models. Vision 2030 programs funnel AI and 5G budgets toward industrial IoT, allowing level data to integrate seamlessly with ERP and emissions-monitoring systems. Suppliers with localized service hubs are seeing above-average order volumes as operators migrate from legacy float gauges to SIL-certified radar platforms.

Asia-Pacific capital plans for membrane desalination lines and advanced biological wastewater treatment require precise, corrosion-resistant level sensing to manage chemical dosing and sludge processes. Plants now embed AI modules that leverage continuous level data for energy optimization, lifting adoption of radar and ultrasonic instruments rated for high-salinity media. Parallel investments in the Middle East's 46% share of global desalination capacity reinforce long-term unit demand.

High electromagnetic fields near induction furnaces distort electronic level signals, driving costly recalibration cycles and limiting uptake of radar sensors in India's rapidly growing steel sector. Vendors are testing multilayer shielding and digital filtering, yet price-sensitive operators defer upgrades until robust, affordable solutions emerge.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Point devices dominated 2024 with a 58% level sensors market share, favored for binary control in overfill and dry-run safeguards. Continuous measurement products, though smaller in shipment volume, are growing 8% annually as operators pursue real-time inventory tracking to cut working capital and energy use. The level sensors market size for continuous platforms is projected to exceed USD 3 billion by 2030, alongside the adoption of analytics-ready transmitters. Hybrid instruments that fuse switching and continuous functions in a single housing are winning conversions in space-constrained skids, widening supplier differentiation.

The migration to 80 GHz radar is powering continuous segment uptake in water, chemical, and food plants that battle foam, vapor, and dust. Integrated diagnostics now flag buildup, offering predictive-cleaning prompts and elevating uptime. Suppliers that combine IO-Link or wireless protocols into continuous gauges capture OEM design wins as machine builders standardize on smart-sensor architectures.

Contact technologies retained 64% of 2024 revenue, anchored by hydrostatic and magnetostrictive probes valued for mechanical simplicity. Yet non-contact devices are expanding 8.2% each year, riding demand for contamination-free measurement in foods, pharmaceuticals, and corrosive liquids. Radar and ultrasonic models avoid downtime tied to wetted parts, and Bluetooth-enabled units ease commissioning via mobile apps. Non-contact platforms now represent nearly one-third of level sensors market size and are forecast to surpass contact shipments in high-value chemical and energy projects by 2029.

Radar progress is most visible: FMCW architectures leverage 80 GHz frequencies for narrow beams that navigate internal structures. Suppliers also push firmware advances that remove false echoes in agitator-equipped tanks. Ultrasonic retains traction where cost sensitivity tops performance, especially in municipal water projects, but its share edges lower as radar pricing falls.

Level Sensor Market is Segmented by Monitoring Type (Point Level Sensors and Continuous Level Sensors), Technology (Contant Sensors and Non-Contact Sensors), Sensor Technology (Capacitive, Conductive, Optical/Photoelectric and More), Component, Detection Medium, End-User Industry (Oil & Gas, Power Generation and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific led the level sensors market with 45% revenue in 2024, underpinned by extensive industrial automation in China and accelerating capital investment in India and Southeast Asia. Battery-electric vehicle value-chains alone require thousands of chemically resistant radar gauges for electrolyte, slurry, and solvent tanks. Regional wastewater infrastructure, buoyed by urbanization, fuels orders for continuous sensors tied to AI-driven control loops. Suppliers investing in localized manufacturing and aftersales networks deepen share across tier-2 and tier-3 cities.

The Middle East registers the fastest regional CAGR at 9% from 2025-2030. Tank-farm automation programs linked to Vision 2030 and ADNOC downstream projects, plus record desalination capacity additions, sustain multi-year demand for SIL-rated radar and smart point switches. Logistics corridors such as the India-Middle East-Europe Economic Corridor amplify sensor orders as new terminals and pipelines require inventory monitoring.

North America continues to modernize custody-transfer tanks with 80 GHz radar for revenue-critical volume calculations, while shale-related water-handling operations adopt ultrasonic and radar devices resistant to sediment and hydrocarbons. European chemical parks prioritize SIL-3 upgrades and sustainability metrics, boosting demand for certified radar units and cloud-enabled diagnostics. South American mining and pulp operations expand gradually, though local OEMs face cost hurdles meeting international SIL standards, moderating near-term penetration.