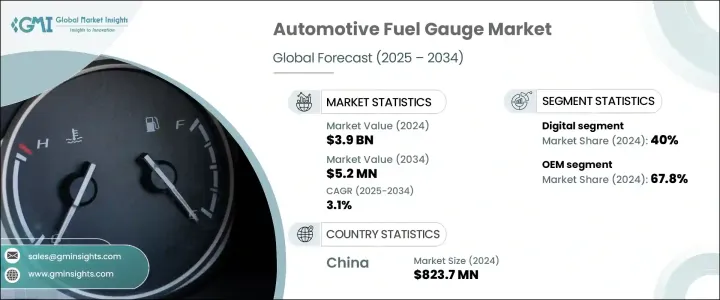

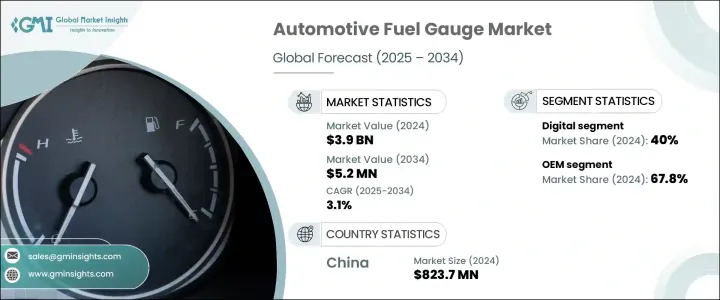

세계의 자동차용 연료계 시장은 2024년에는 39억 달러로 평가되었고, 텔레매틱스와 통합된 첨단 연료계 시스템에 대한 수요를 수반하는 차량과 차량의 디지털화에 의해 2034년에는 52억 달러에 달할 것으로 예측되며, CAGR 3.1%로 성장할 전망입니다.

차량 관리자는 비용을 최적화하고 유지보수 일정을 수립하며 운전자 행동을 모니터링하기 위해 실시간 연료 데이터에 지속적으로 액세스해야 합니다. 텔레매틱스를 통해 연결된 이러한 스마트 게이지를 사용하면 연료 잔량을 즉시 업데이트하고, 연료 도난이나 누출과 같은 문제를 식별하며, 급유 필요성에 대한 알림을 보낼 수 있습니다. 이러한 통합은 예측 유지보수를 지원하고 운영 중단 시간을 줄여 물류, 대중교통, 공유 모빌리티 서비스에서 매우 중요한 시스템이 될 수 있습니다.

센서 설계의 기술 발전으로 자동차용 연료계의 성능이 크게 향상되었습니다. 정전식, 초음파, 저항식 등 최신 센서는 다양한 작동 조건에서 더 나은 정확도, 더 빠른 응답 시간, 더 뛰어난 내구성을 제공합니다. 이러한 센서는 바이오 연료와 에탄올 혼합물을 포함한 다양한 탱크 크기와 연료 유형에 맞게 조정됩니다. 이렇게 향상된 정밀도는 오판독을 줄이고 신뢰할 수 있는 연료 데이터를 보장하며, 이는 개인 및 차량 운영 모두에 매우 중요합니다. 또한 센서 소형화로 인해 소형 차량 설계의 통합성이 향상되어 전반적인 기능이 향상되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 39억 달러 |

| 예측 금액 | 52억 달러 |

| CAGR | 3.1% |

자동차용 연료계 시장은 아날로그, 하이브리드 디스플레이, 헤드업 디스플레이, 디지털 옵션 등 기술별로 세분화됩니다. 2024년에는 디지털 부문이 40%의 시장 점유율로 선두를 차지했으며, 2034년까지 3.7%의 연평균 성장률로 성장할 것으로 예상됩니다. 이러한 성장은 차량의 전기화 증가, 스마트 대시보드 통합에 대한 수요, 연료 또는 에너지 사용량의 정확한 실시간 모니터링에 대한 소비자의 선호에 의해 촉진되고 있습니다. 디지털 연료계는 배터리 주행 거리, 충전 상태, 에너지 흐름에 대한 자세한 정보를 제공하는 전기 및 하이브리드 모델을 포함한 최신 차량에 필수적입니다.

판매 채널 측면에서 OEM 부문은 2024년 67.8%의 점유율을 차지했으며 2025년부터 2034년까지 2.8%의 연평균 성장률을 보일 것으로 예상됩니다. 새로 제조되는 차량에 연료계가 표준 부품으로 통합되면서 OEM 부문이 여전히 지배적인 위치를 차지하고 있습니다. 이러한 게이지들은 디지털 계기판과 차량 진단 시스템에 통합되어 최신 엔진 관리 및 배기가스 기술과의 호환성을 보장합니다. 주요 게이지 제조업체는 자동차 생산업체와 직접 협력하여 특정 차량 아키텍처 및 대시보드 레이아웃에 맞는 맞춤형 솔루션을 설계합니다.

중국의 자동차용 연료계 시장은 2024년 54%의 점유율을 차지하고 승용차 및 상용차 생산에 힘입어 8억 2370만 달러를 창출하며 연료계 시장에서의 입지를 강화했습니다. 중국은 수직적으로 통합된 공급망의 이점을 통해 현지 제조업체가 효율적이고 비용 효율적으로 OEM 수요를 충족할 수 있습니다. 전기자동차(EV) 및 스마트 자동차 기술에 대한 중국의 막대한 투자와 더불어 이 지역의 자동차 생산량이 증가함에 따라 연료계와 같은 첨단 자동차 부품에 대한 수요가 더욱 증가하고 있습니다.

자동차용 연료계 산업의 주요 업체로는 앱티브(Aptiv), 보그워너, 보쉬, 콘티넨탈, 덴소 등이 있습니다. 자동차용 연료계 시장의 기업들은 시장 입지를 강화하기 위해 자동차 제조업체와의 전략적 협업을 통해 맞춤형 연료계 솔루션을 개발하는 데 주력하고 있습니다. 특히 센서 설계 및 텔레매틱스 통합과 같은 기술 발전에 많은 투자를 통해 정확도를 높이고 실시간 모니터링 기능을 제공합니다. 또한, 아시아태평양과 같은 신흥 시장에서의 입지를 확대하고 현지 제조 역량을 활용하여 비용을 절감하고 고급 연료 관리 시스템에 대한 수요 증가에 대응하는 데 주력하고 있습니다. 이러한 기업들은 차량의 전기화와 커넥티드 기술의 사용 증가에 집중함으로써 빠르게 진화하는 자동차 시장을 선도할 수 있는 입지를 다지고 있습니다.

The Global Automotive Fuel Gauge Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 3.1% to reach USD 5.2 billion by 2034, driven by the vehicles and fleet digitalization, with the demand for advanced fuel gauge systems integrated with telematics. Fleet managers need continuous access to real-time fuel data to optimize costs, schedule maintenance, and monitor driver behavior. These smart gauges, linked through telematics, can provide instant fuel level updates, identify issues such as fuel theft or leaks, and send alerts for refueling needs. This integration supports predictive maintenance and reduces operational downtime, making the systems crucial in logistics, public transportation, and shared mobility services.

Technological advancements in sensor design have greatly improved the performance of automotive fuel gauges. Modern sensors, including capacitive, ultrasonic, and resistive types, offer better accuracy, faster response times, and greater durability under various operating conditions. These sensors adapt to different tank sizes and fuel types, including biofuels and ethanol blends. This increased precision reduces false readings and ensures reliable fuel data, which is critical for both personal and fleet vehicle operations. Additionally, sensor miniaturization has improved integration in compact vehicle designs, enhancing overall functionality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 3.1% |

The automotive fuel gauge market is segmented by technology, including analog, hybrid display, head-up display, and digital options. In 2024, the digital segment took the lead with a 40% market share, expected to grow at a 3.7% CAGR through 2034. This growth is fueled by the increasing electrification of vehicles, the demand for smart dashboard integration, and consumers' preference for accurate and real-time monitoring of fuel or energy usage. Digital fuel gauges are essential for modern vehicles, including electric and hybrid models, providing detailed information on battery range, charge status, and energy flow.

In terms of sales channels, the OEM segment held 67.8% share in 2024 and is expected to grow at a CAGR of 2.8% from 2025 to 2034. The OEM sector remains dominant due to the incorporation of fuel gauges as standard components in newly manufactured vehicles. These gauges are integrated into digital instrument clusters and vehicle diagnostic systems, ensuring compatibility with modern engine management and emissions technologies. Key gauge manufacturers collaborate directly with automotive producers to design custom solutions that fit specific vehicle architectures and dashboard layouts.

China Automotive Fuel Gauge Market held 54% share in 2024 and generated USD 823.7 million, driven by passenger and commercial vehicle production, which has bolstered its position in the fuel gauge market. China benefits from a vertically integrated supply chain, enabling local manufacturers to meet OEM demand efficiently and cost-effectively. The growing volume of vehicle production in the region, coupled with China's significant investment in electric vehicles (EVs) and smart automotive technology, has further contributed to the rising demand for advanced automotive components like fuel gauges.

Key players in the automotive fuel gauge industry include Aptiv, BorgWarner, Bosch, Continental, and Denso. To strengthen their market position, companies in the automotive fuel gauge market focus on strategic collaborations with automotive manufacturers to develop tailored fuel gauge solutions. They invest heavily in technological advancements, particularly sensor design and telematics integration, to enhance accuracy and offer real-time monitoring features. Additionally, companies focus on expanding their presence in emerging markets like Asia Pacific, leveraging local manufacturing capabilities to reduce costs and cater to increasing demand for advanced fuel management systems. By focusing on the electrification of vehicles and increasing use of connected technologies, these companies are positioning themselves to lead in a rapidly evolving automotive market.