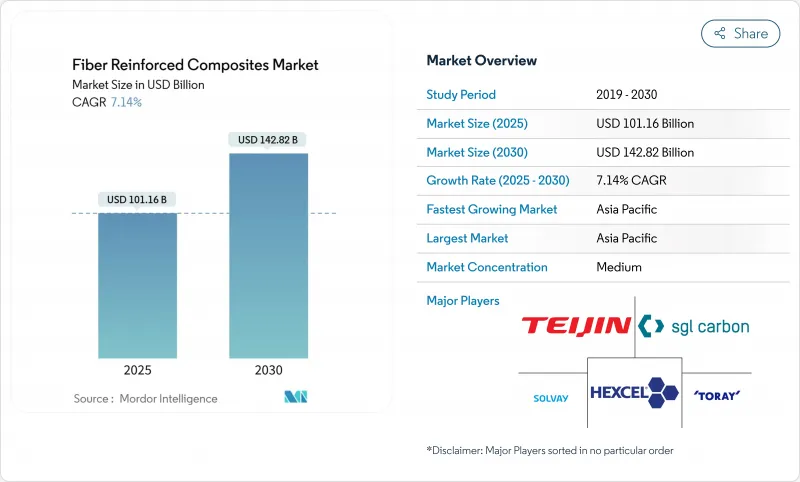

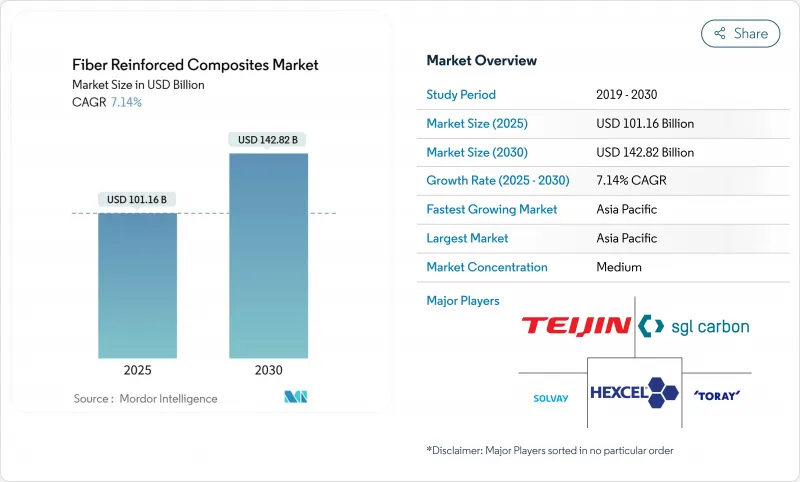

섬유 강화 복합재료 시장은 2025년에 1,011억 6,000만 달러에 이르고, 2030년에는 CAGR 7.14%를 나타내 1,428억 1,000만 달러로 확대될 것으로 예측되고 있습니다.

특히 보잉 787과 에어버스 A350 플랫폼 등 구조중량의 50% 이상을 복합재료에 할당하는 항공계획이 견조한 수요를 창출하고 있습니다. 기업평균연비 준수와 전기차 항속거리 성장을 추구하는 자동차 제조업체는 경량 카본 라미네이트 채용을 가속화하고, 풍력 부문은 100m급 블레이드를 목표로 섬유 강화 복합재료 시장을 더욱 확대시킵니다. 공정 자동화는 경쟁력을 강화하고 자동화된 섬유 배치 라인은 노동력 부족과 일관성 문제를 해결합니다. 지역별로는 아시아태평양이 중국의 대규모 제조 능력을 배경으로 선도하고 있지만, 인도의 신흥 항공우주 생태계가 규모를 확대해도 현지의 과잉 생산 능력 압력은 여전히 남아 있습니다.

상업 프로그램에서는 15-20%의 연비 삭감을 확보하기 위해 복합재 함유율 50%를 목표로 하고 있으며, eVTOL 설계에서는 이 비율을 한층 더 높이고 있습니다. 헥셀의 민간항공우주사업 매출은 와이드바디의 제조율에 따라 2024년에 21.3% 급증했지만, 공급망 경직이 눈앞의 납품을 억제하고 있습니다. NASA의 HiCAM 이니셔티브는 열경화성 수지와 열가소성 수지의 몸체 생산율을 두 배로 늘리는 것을 목표로 하며 구조물 수요의 상승을 시사합니다. 액체 수소 추진을 위한 완전 복합 극저온 탱크에 대한 병렬 R&D는 섬유 강화 복합재료 시장에 새로운 하위 부문을 제공합니다. 이러한 변화가 상반되어 항공우주는 중기 성장의 기폭제가 됩니다.

블레이드의 길이가 100 미터를 넘게 되고, 무게를 줄이지 않고 강성을 유지하기 위해 탄소 스퍼 캡이 필요합니다. 미국의 빅 어댑티브 로터 프로젝트는 이러한 궤적을 명확하게 보여주며, 천연섬유와 합성 섬유의 하이브리드 혼합 섬유는 라이프 사이클의 지속가능성을 향상시킵니다. 다우의 새로운 폴리 우레탄 - 탄소 인발 라인은 90% 인라인 경화를 달성하고 대형 라미네이트의 처리량을 향상시킵니다. 세계의 생산 능력은 2030년까지 981GW에 달할 것으로 예상되지만, 사용한 블레이드의 재활용은 아직 해결되지 않은 채로 서큘러 이코노미의 혁신이 요구되고 있습니다.

맨체스터 대학의 리그닌 기반 전구체는 3-5배의 비용 절감 가능성을 시사하고 있습니다. 기존 AFP 시스템의 가격은 300만-600만 달러이지만, 모듈식 리스 모델이라면 진입 장벽이 낮습니다. SGL 탄소의 섬유 판매량이 35.2% 감소한 것은 변동하는 상품 가격에 민감하다는 것을 보여줍니다. 재생 탄소섬유는 훨씬 적은 에너지만 필요하기 때문에 기계적 특성을 유지하면서 압력을 완화할 수 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

2024년에는 건설, 자동차, 풍력에너지 분야의 비용 효율성과 견고한 공급망에 견인되었으며, 유리 섬유는 61.87%의 점유율로 시장을 독점했습니다. 탄소섬유의 점유율은 작지만 항공우주산업과 고성능 자동차산업에서 수요 증가에 힘입어 2030년까지의 CAGR은 8.04%를 나타낼 것으로 예측됩니다. 내충격성과 열안정성으로 알려진 아라미드 섬유는 주로 보호구와 항공우주 부품에 사용됩니다. 붕소 섬유는 비용이 많이 드는 것, 특수한 항공우주 용도에 이용되고 있습니다. 천연섬유의 채용은 합성 섬유와 천연섬유를 결합한 하이브리드 복합재료를 통해 증가하고 있으며, 성능을 유지하면서 환경면에서의 이점을 제공합니다. 예를 들어, 대나무 섬유와 사이잘 대마 섬유는 풍력 터빈의 블레이드에 사용됩니다.

제조업의 진보는 섬유 생산의 경제성을 변화시키고 있습니다. CARBOWAVE 프로젝트는 마이크로웨이브 어시스트 탄소섬유 생산을 도입하여 에너지 소비를 최대 70% 줄이고 비용 구조와 환경에 미치는 영향을 변화시킬 수 있습니다. 사우디아라비아는 항공우주, 자동차, 건설용도를 목표로 하는 그래핀 강화 탄소섬유 제조를 위한 최초의 산업 규모시설을 설립하여 2030년까지 16억 달러를 넘는 수익이 전망되고 있습니다. 현무암 섬유는 지속 가능한 대체 섬유로서 대두되고 있으며, 천연섬유 복합재료에 비해 우수한 기계적 특성과 내환경성을 갖추고 있습니다. 또한 탄소섬유보다 비용면에서 우수하기 때문에 가혹한 환경에서 내구성이 요구되는 해상 풍력 용도에 적합합니다.

2024년에는 폴리머 시스템이 수익의 70.45%를 차지한 반면, 금속 매트릭스 옵션은 CAGR 7.50%를 나타낼 것으로 예측되었으며, 섬유 강화 복합재료 시장, 특히 항공우주 열 관리 응용 분야에서 지속적인 중요성이 강조되었습니다. GE가 개발한 세라믹 매트릭스 복합재료는 제트 엔진의 작동 온도를 높이고 연료 효율을 최대 20% 향상시킵니다. 게다가 극초음속 재돌입이나 핵융합로에 노출되는 부품에는 2,000℃에서의 내구성이 불가결한 탄소-탄소 재료가 빠뜨릴 수 없습니다.

폴리카보네이트, PEKK, PEEK 등의 래피드 사이클 열가소성 플라스틱은 재활용 가능하고 1분 프레스 성형이 가능하기 때문에 인기를 끌고 있습니다. 코베스트로는 가전 분야를 대상으로 한 연속 섬유 폴리카보네이트 패널을 발표했습니다. 또한 NREL은 생산 비용 효율을 유지하면서 석유화학계 수지에 비해 온실가스 배출량을 40% 줄이는 바이오기반 에폭시를 입증했습니다. 미쓰비시화학은 또한 1,500℃의 고온에 견디는 세라믹 복합재를 개발해 JAXA의 로켓 사양에 적합시켜, 방위·우주 분야에서 새로운 수익 기회를 창출했습니다.

아시아태평양은 2024년 매출의 41.05%를 차지했고 CAGR은 8.38%를 나타낼 전망입니다. 중국의 HRC는 상숙에 3,380만 달러를 투자해 열경화성 수지와 열가소성 수지의 연속 생산을 확대하고, 인도의 키네코 엑셀은 고아의 거점에서 인발 성형 카본 플랑크를 베스타스에 공급하고 있습니다. 대만의 Swancor는 해외 프로젝트를위한 수지 플레이트 공급을 현지화하고 지역 밸류체인을 심화시킵니다.

북미는 정착한 항공우주 기반과 연비규제를 활용하여 수요를 유지하고 있습니다. GKN 에어로 스페이스는 멕시코 치와와의 조립 능력을 두 배로 늘렸으며 걸프 스트림과 혼다 제트 프로그램에 대응하기 위해 200명의 고용을 늘렸습니다. 사프란은 케레타로에서 LEAP 엔진의 생산 능력을 확대하고 복합재 제조 기지로서 멕시코의 상승을 강조했습니다. 매사추세츠 공과대학(MIT)의 연구자는 탄소나노튜브에 의한 '나노스티치'를 개발하여 층간 전단을 62% 향상시켜 더욱 경량화를 시사했습니다.

유럽에서는 재활용 의무화와 저탄소 소재 혁신이 추진되고 있습니다. Clean Sky 2 FRAMES 프로젝트는 PEEK와 PEKK의 윙 스킨의 크세논 플래시 램프 AFP 가열을 검증하고 Strata와 솔베이는 UAE 알 아인에 보잉 777X 부품용 MENA 최초의 프리프레그 공장을 개설했습니다. 2024년 브라질 복합재 매출은 5.6% 증가한 5억 6,000만 달러로 남미 전체에 잠재적인 성장 가능성을 보였습니다.

The fiber reinforced composites market reached USD 101.16 billion in 2025 and is projected to advance to USD 142.81 billion by 2030, registering a 7.14% CAGR.

Robust demand originates from aviation programmes that allocate more than 50% of structural weight to composites, notably the Boeing 787 and Airbus A350 platforms. Automakers pursuing Corporate Average Fuel Economy compliance and electric-vehicle range gains accelerate adoption of lightweight carbon laminates, while the wind sector's push toward 100-meter blades further enlarges the fiber reinforced composites market. Process automation deepens competitiveness, with automated fiber placement lines resolving labour shortages and consistency challenges. Regionally, Asia-Pacific leads on the back of China's large-scale manufacturing capacity, although local overcapacity pressures linger even as India's nascent aerospace ecosystem scales.

Commercial programmes target 50% composite content to secure 15-20% fuel-burn reductions, and eVTOL designs push that ratio even higher. Hexcel's commercial aerospace revenue jumped 21.3% in 2024 on wide-body build rates, yet supply chain tightness tempers near-term deliveries. NASA's HiCAM effort aims to multiply output rates for thermoset and thermoplastic fuselages, signaling a structural demand uplift. Parallel R&D on fully composite cryogenic tanks for liquid-hydrogen propulsion opens new sub-segments for the fiber reinforced composites market. Together, these shifts cement aerospace as a medium-term growth catalyst.

Blade lengths now exceed 100 meters, demanding carbon spar caps to retain stiffness without weight penalties. The U.S. Big Adaptive Rotor project underscores this trajectory, while hybrid natural-synthetic fibre blends improve lifecycle sustainability. New polyurethane-carbon pultrusion lines from Dow achieve 90% in-line cure, boosting throughput for oversized laminates. Global capacity is forecast to reach 981 GW by 2030, yet recycling end-of-life blades remains unresolved, inviting circular-economy innovation.

Energy-intensive carbonisation drives elevated input costs, although lignin-based precursors from the University of Manchester suggest 3-5 X savings potential. Traditional AFP systems list at USD 3-6 million, but modular leasing models lower the entry barrier. SGL Carbon's 35.2% sales drop in fiber units shows sensitivity to volatile commodity pricing. Recycled carbon fibre, requiring far less energy, can relieve some pressure while preserving mechanical properties.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2024, glass fibers dominated the market with a 61.87% share, driven by cost efficiencies and robust supply chains in the construction, automotive, and wind energy sectors. While holding a smaller share, carbon fibers are projected to grow at a CAGR of 8.04% through 2030, supported by increasing demand in the aerospace and high-performance automotive industries. Aramid fibers, known for their impact resistance and thermal stability, are primarily used in protective equipment and aerospace components. Despite their higher costs, Boron fibers are utilized in specialized aerospace applications. The adoption of natural fibers is increasing through hybrid composites that combine synthetic and natural fibers, offering environmental benefits while maintaining performance. For example, bamboo and sisal fibers are used in wind turbine blades.

Advancements in manufacturing are transforming fiber production economics. The CARBOWAVE project has introduced microwave-assisted carbon fiber production, reducing energy consumption by up to 70%, potentially altering cost structures and environmental impacts. Saudi Arabia has established the first industrial-scale facility for graphene-enriched carbon fiber production, targeting aerospace, automotive, and construction applications, with projected revenues exceeding USD 1.6 billion by 2030. Basalt fibers are emerging as a sustainable alternative, offering superior mechanical properties and environmental resistance compared to natural fiber composites. Additionally, their cost advantages over carbon fibers make them suitable for offshore wind applications requiring durability in harsh environments.

In 2024, polymer systems accounted for 70.45% of the revenue, while metal matrix options are projected to achieve a 7.50% CAGR, highlighting their sustained importance in the fiber-reinforced composites market, particularly for aerospace thermal-management applications. Ceramic matrix composites developed by GE enhance jet engine operating temperatures, improving fuel efficiency by up to 20%. Additionally, carbon-carbon materials are critical for components exposed to hypersonic re-entry and fusion reactors, where endurance at 2,000 °C is essential.

Rapid-cycle thermoplastics, such as polycarbonate, PEKK, and PEEK, are gaining traction due to their recyclability and capability for one-minute press molding. Covestro has introduced continuous-fiber polycarbonate panels targeting the consumer electronics sector. Furthermore, NREL has demonstrated a bio-based epoxy that reduces greenhouse gas emissions by 40% compared to petrochemical-based resins while maintaining production cost efficiency. Mitsubishi Chemical has also developed a ceramic composite capable of withstanding temperatures of 1,500 °C, meeting JAXA specifications for launch vehicles and creating new revenue opportunities in the defense and space sectors.

The Fiber Reinforced Composites Market Report Segments the Industry by Fiber Type (Carbon Fibers, Glass Fibers and More), Matrix (Polymer Matrix Composites, Metal Matrix Composites, and More), Manufacturing Process (Pultrusion, Filament Winding, and More), End-User Industry (Aerospace and Defense, Automotive, and More) and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific generated 41.05% of 2024 sales and is set to post an 8.38% CAGR, ensuring that the fiber reinforced composites market remains anchored in the region. China's HRC invested USD 33.8 million in Changshu to expand serial thermoset and thermoplastic part output, while India's Kineco Exel now supplies pultruded carbon planks to Vestas from its Goa site. Taiwan's Swancor has localised resin plate supply for offshore projects, deepening the regional value chain.

North America leverages an entrenched aerospace base and fuel-economy regulation to maintain demand. GKN Aerospace doubled assembly capacity in Chihuahua, Mexico, adding 200 jobs to serve Gulfstream and HondaJet programmes. Safran expanded LEAP engine capacity in Queretaro, underscoring Mexico's rise as a composites manufacturing node. MIT researchers developed "nanostitching" with carbon nanotubes, lifting interlaminar shear by 62% and hinting at further light-weighting gains.

Europe champions recycling mandates and low-carbon material innovation. The Clean Sky 2 FRAMES project validated xenon flashlamp AFP heating for PEEK and PEKK wingskins, while Strata and Solvay opened the first MENA prepreg plant for Boeing 777X parts in Al Ain, UAE. Brazil's composites turnover rose 5.6% to USD 560 million in 2024, pointing to latent growth potential across South America.