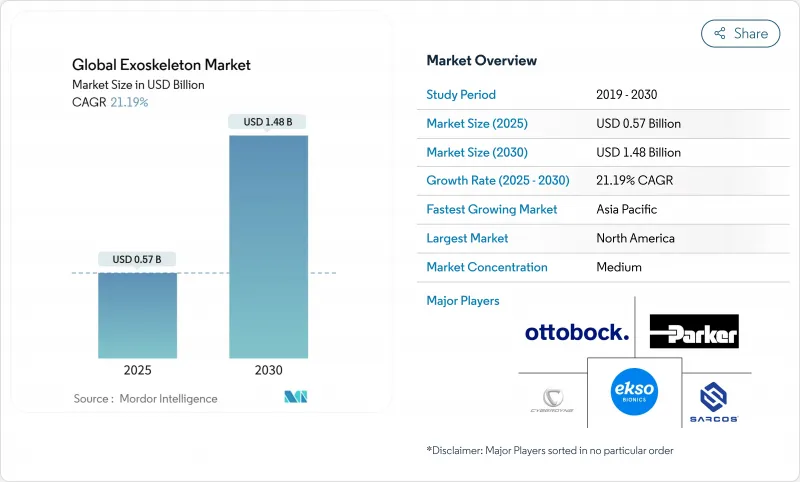

세계의 외골격 시장 규모는 2025년에 5억 7,000만 달러로 추정되고, 2030년에는 14억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년) CAGR 21.19%로 성장할 전망입니다.

초기 의료 파일럿에서 대규모 프로그램으로, 산업 인체 공학 프로젝트는 단일 라인에서 기업 전개로, 방위 기관은 프로토타입을 한정 생산으로 이행하는 등 급속한 채용이 진행되고 있습니다. 제어 소프트웨어에 내장된 인공지능(AI)은 장치의 응답성을 재구성하고 있습니다. 검토를 받은 연구에 따르면 반복 리프트 중 등근 활동이 최대 35%까지 줄어들어 부상 클레임을 직접 줄이는 효과가 있습니다. 가벼운 컴포지트, 파워 웨이트 액추에이터 및 배터리 에너지 밀도의 병렬 향상으로 평균 유닛 질량이 약 30% 감소되었으며 장착 시 편안함과 세션 시간이 향상되었습니다. 미국 메디케어가 2024년 1월 개인용 외골격을 장비 급여 대상으로 분류하기로 결정함으로써 개인 부담 도입이 진행되어 독일, 한국, 일본의 유사한 정책에 영향을 주었습니다. 경쟁의 심각성은 소프트웨어 중심의 진출 기업이 설계 승리를 확보함에 따라 상승하고 있습니다. NVIDIA가 2025년에 Ekso Bionics를 Connect 프로그램에 추가하기로 결정한 것은 지속적인 차별화에 가속 컴퓨팅의 재능이 필수적임을 보여줍니다.

한편, 65세 이상의 노인 비율은 2030년까지 세계 인구의 16%를 보일 것으로 예측되고 있으며, 이동 보조 장비에 대한 수요가 높아지고 있습니다. 대조 임상시험은 조기 외골격의 개입이 기존 치료에 비해 기능 회복을 최대 30% 향상시키는 것으로 나타났으며, 신속한 전개의 임상적 근거를 강조하고 있습니다. 의료 시스템 관리자는 로봇 치료를 처리량 도구로 파악하기 시작했습니다. 단위는 더 적은 치료사와 더 길고 작업에 특화된 세션을 허용합니다. 뇌졸중, 다발성 경화증, 외상성 뇌 손상과 같은 여러 신경 질환의 확고한 증거는 지불 측의 신뢰를 강화하고 보험 적용 결정에 대한 경로를 원활하게 합니다.

2025년 조사에 따르면 치료사의 80%가 외골격이 수작업을 보완함으로써 신체적 부담이 경감되어 처리 능력이 향상되었다고 보고했습니다. 임상 벤치마크에 따르면, 쉘터링 암스 인스티튜트에서는 12주간의 구조화된 로봇 치료에 의해 SCI 후 보행 속도가 25-40% 향상되었으며 BSW 재활에서는 뇌졸중 환자의 보행 대칭성이 기존 프로그램에 비해 32% 개선되었습니다. 이러한 결과는 시험 예산 조직에서 다기관 조달로의 전환을 뒷받침합니다. 자동차 공장 및 물류 시설의 산업 기술 팀은 의학적 실증에 편승하여 상반신 유닛을 조달하여 어깨 부상과 잔업비 지불을 억제합니다.

정가는 50,000-150,000달러로, 서비스 계약에 따라 연간 5,000-10,000달러가 가산됩니다. 투자대효과는 노동재해 예방과 입원기간 단축에 의존하지만 공공 예산이 대부분을 차지하는 신흥 시장에서는 제약이 있어 대수는 억제되고 있습니다. 벤더는 그 후, 사용 시간마다 과금하는 리스나 로보틱스 아즈 아 서비스 모델에 축족을 옮기고 있는데, 북미 이외에서는 이러한 스키마는 아직 시작되었습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

전동 카테고리는 2024년에 84.22%의 매출을 획득하여 복잡한 보행, 계단 승강, 수하물 운반을 지원하는 모터 구동 어시스트로부터 혜택을 받고 있습니다. 이것은 대부분의 재활 프로토콜과 방어 프로토타입의 골격을 형성합니다. 그러나 허리 부담을 줄이는 스프링식 장비와 같은 수동적 장비는 물류기업이 물류센터에 수백대를 배치하고 있기 때문에 2030년까지 연평균 복합 성장률(CAGR)은 22.82%를 기록했습니다. 2025년에는 수동적 허리 외골격이 골판지 박스의 하역 중에 등 신근의 활동을 35% 삭감할 수 있음을 검토 시험으로 확인하여 산업 보건 예산에 통합할 예정입니다. 파워드 힙 조인트와 패시브 스파이널 서포트의 조합으로 에너지 수요와 부품 수를 줄일 수 있습니다.

비용 차이는 여전히 두드러지며 패시브 모델의 소매 가격은 파워드 모델의 1/3입니다. 제조업체 각사는 선진적인 복합재료 및 엘라스토머제의 토션 엘리먼트를 활용하는 것으로, 어시스트 토크를 유지하면서 경량화를 도모해, 패시브 모델을 엄격한 조달 제한의 범위 내에 거두고 있습니다. 센서가 브레이스 프레임에 직접 내장됨으로써 패시브 유닛은 인체공학적 분석을 기업 대시보드에 제공하기 시작하여 동력식과의 데이터 갭을 채우고 있습니다. 파워드 시스템이 고부하 치료로 유용성을 유지하더라도, 수동형은 예산에 민감한 구매자로부터 점유율 확대를 흡수할 수 있습니다.

이동형 외골격은 2024년 세계 매출의 68.34%를 차지했지만, 이것은 다양한 지형을 횡단하는 능력을 반영하고 있어 일상생활의 자립, 창고 작업, 보병 기동에 대응하는 것입니다. 배터리 혁신으로 작동 시간은 6-8시간으로 이전 모델보다 40% 길어져 완전한 진료 이동 및 연속 생산 사이클을 지원합니다. 이용자는 시선의 높이에서의 대화에 의한 심리적인 이점을 들고 있어, 이것은 재택 환경에서의 어드히어런스를 높이는 요인이 되고 있습니다. 거치형 시스템은 현재는 작지만 제한된 운동 학습 단계에서 높은 반복성 훈련을 제공할 수 있기 때문에 2030년까지 연평균 복합 성장률(CAGR)은 24.23%를 기록할 전망입니다. 의료 센터에서는 치료사가 증강현실(AR) 오버레이로 보행 운동을 미세 조정하는 갠트리 프레임에 설치하여 신경 가소성의 개입을 가속시킵니다.

교체 가능한 모듈을 사용하면 하나의 인클로저에서 디딜방아 장착형과 지상형으로 전환할 수 있어 이동형과 거치형의 격차를 모호하게 할 수 있습니다. 이러한 유연성은 다양한 환자 그룹에 걸쳐 자본을 상각하려는 중형 재활 체인에 매력적입니다. 공급업체는 난간, 하네스, 디딜방아 플레이트와 같은 플러그 앤 플레이 추가 기능을 제공합니다.

북미는 2024년 외골격 시장 수익의 40.33%를 차지했으며, 성숙한 지급자 생태계와 풍부한 벤처 자금에 의해 지원되고 있습니다. 메디케어의 고정상환율 91,032달러는 척수손상 환자의 구매 편의성을 극적으로 개선하여 퇴역군인 건강관리 센터와 레벨 i 외상 병원에 장비 출하를 증가시켰습니다. 미국에서는 자동차 조립 회사와 택배 물류 회사를 포함한 산업계 고용주가 부상으로 인한 가동 중지 시간을 막기 위해 상반신 외의를 시험적으로 도입하고 있으며, 이러한 프로젝트는 점차 틀 계약으로 전환하고 있습니다. 캐나다도 비슷한 궤도를 따르고 있으며, 각 국가의 산재위원회는 보험금 청구의 감소와 생산성 향상을 평가하는 시험 프로그램을 맡고 있습니다.

유럽은 독일, 프랑스, 북유럽을 중심으로 매출 2위를 차지했습니다. 독일의 BARMER 보험 적용 결정은 850만 명의 수혜자를 포괄하여 법정 보험 가입자의 거의 절반에 환불을 통한 접근을 가져왔습니다. 연구 협력은 Horizon Europe의 보조금을 받고 활발히 진행되고 있으며, 아헨, 취리히, 제노바의 로봇 연구소와 임상 파트너가 연결되어 있습니다. 바이에른 주 자동차 제조업체 각 회사는 근골격계에 대한 노출 임계값을 준수하기 위해 생산 라인에 어깨를 지원하는 외골격을 도입하고 있습니다. 진화하는 ExosCE 인증 경로는 의료 및 기계 지침을 하나의 문서로 통합하고 승인 일정을 단축하여 제품 배포를 용이하게 합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 23.78%로 가장 급성장하고 있는 클러스터입니다. 한국의 제조업체인 WIRobotics사는 2025년에 미국에서 WIM 보행 어시스트 로봇을 발매해, 이 지역의 수출 의욕을 강조한 mobihealthnews.com. 메이드 인 차이나 2025 아젠다는 재활 로봇 공장에 조성금 인센티브를 주고, 한편 일본의 고령화 사회는 공공 연구 개발을 지원 모빌리티로 향하게 합니다. 진료 보상이 불투명한 부분도 있지만, 일렉트로닉스나 조선 분야의 산업계의 고객은 배상 청구를 억제하기 위해 요추 서포트 슈트를 대량으로 조달하고 있습니다. 싱가포르와 호주 관민 파트너십은 외골격과 스마트 홈 생태계를 통합하는 도시 노화 이니셔티브에 중점을 둡니다.

The Global Exoskeleton Market size is estimated at USD 0.57 billion in 2025, and is expected to reach USD 1.48 billion by 2030, at a CAGR of 21.19% during the forecast period (2025-2030).

Rapid adoption is unfolding as early medical pilots convert into scaled programs, industrial ergonomics projects expand from single lines to enterprise roll-outs, and defense agencies move prototypes into limited-rate production. Artificial intelligence (AI) embedded within control software is reshaping device responsiveness, with peer-reviewed studies showing up to a 35% cut in back muscle activity during repetitive lifts, a jump that directly lowers injury claims. Parallel gains in lightweight composites, power-to-weight actuators, and battery energy density have trimmed average unit mass by roughly 30%, improving wearer comfort and session duration. The reimbursement breakthrough in the United States Medicare's January 2024 decision to classify personal exoskeletons under the brace benefit has triggered private-payer adoption and influenced similar policy moves in Germany, South Korea, and Japan. Competitive intensity is climbing as software-centric entrants secure design wins; NVIDIA's 2025 decision to place Ekso Bionics in its Connect program signaled that accelerated computing talent is now indispensable for sustained differentiation.

Spinal cord injuries affect 294,000 individuals in the United States, with 17,000 new cases added annually, creating a sizeable candidate pool for robotic gait systems, while the share of people aged >= 65 is projected to reach 16% of the global population by 2030, elevating demand for mobility aids.Controlled clinical trials show that early exoskeleton intervention can lift functional recovery by up to 30% versus traditional therapy, underscoring the clinical rationale for rapid roll-out. Health-system administrators are starting to view robotic therapy as a throughput tool: units permit longer, more task-specific sessions with fewer therapists, an outcome that directly expands revenue capacity without proportionate head-count growth. Robust evidence across multiple neurological conditions stroke, multiple sclerosis, traumatic brain injury reinforces payer confidence, smoothing the path toward coverage decisions.

Hospital groups face chronic staffing gaps as rehabilitation workloads climb; surveys from 2025 show 80% of therapists reporting reduced physical strain and higher throughput when exoskeletons supplement manual assistance. Clinical benchmarking demonstrates 25-40% boosts in post-SCI walking speed after 12 weeks of structured robotic therapy at Sheltering Arms Institute, while stroke patients at BSW Rehabilitation enjoyed 32% better gait symmetry compared with conventional programs. These outcomes support a shift from pilot budgeting to multi-site procurement. Industrial engineering teams in automobile and logistics facilities are piggy-backing on medical proof points, sourcing upper-body units to curb shoulder injuries and overtime payments.

List prices range between USD 50,000-150,000, with service contracts adding USD 5,000-10,000 yearly, figures that strain smaller hospitals and mid-sized factories. The return-on-investment case hinges on preventing workplace injuries and shortening inpatient stays; however, constraints in emerging markets, where public budgets dominate spend, suppress unit volumes. Vendors are subsequently pivoting to leasing and robotics-as-a-service models that charge per usage hour, but these schemes remain nascent outside North America.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The powered category captured 84.22% revenue in 2024, benefitting from motor-driven assistance that supports complex gait, stair ascent, and load carriage. It forms the backbone of most rehabilitation protocols and defense prototypes. However, passive devices, such as spring-based braces that offload lower-back strain, are recording a 22.82% CAGR to 2030 as logistics firms deploy hundreds of units in distribution centers. In 2025, peer-reviewed trials confirmed passive lumbar exoskeletons could cut back-extensor activity by 35% during carton handling, bringing them into occupational health budgets. Hybrid designs are emerging: powered hip joints paired with passive spinal supports lower both energy demand and component count, pointing to a mid-term convergence of the two classes.

The cost delta remains pronounced, with passive models retailing for one-third of powered alternatives. Manufacturers leverage advanced composites and elastomeric torsion elements to maintain assistance torque while trimming weight, placing passive lines within stringent procurement caps. As sensors embed directly onto brace frames, passive units are starting to feed ergonomic analytics to enterprise dashboards, closing the data gap with their powered counterparts. These uptake catalysts position the passive cohort to absorb incremental share from budget-sensitive buyers, even as powered systems sustain utility in high-acuity therapy.

Mobile exoskeletons held 68.34% of 2024 global revenue, reflecting their ability to traverse varied terrain and therefore address daily-living independence, warehouse tasks, and infantry maneuvers. Battery innovations lifted operating time to 6-8 hours, 40% longer than older models, supporting full clinic shifts and continuous production cycles. Users cite psychological benefits from eye-level interaction, a factor boosting adherence in home settings. Stationary systems, although smaller today, clock a 24.23% CAGR through 2030 because they deliver high-repeatability training in constrained motor-learning phases. Medical centers position them on gantry frames where therapists fine-tune gait kinematics via augmented-reality overlays, a configuration that accelerates neuroplasticity interventions.

Interchangeable modules allow a single chassis to switch between treadmill-mounted and overground modes, blurring the mobile-stationary divide. This flexibility appeals to mid-sized rehabilitation chains seeking to amortize capital across varied patient cohorts. Vendors are consequently shipping plug-and-play add-ons, such as handrails, harnesses, and treadmill plates, that install without specialist tooling, reducing downtime.

The Exoskeleton Market Report is Segmented by Technology (Powered / Active and Passive), Mobility (Mobile and Stationary), Body Part (Upper Limb, Lower Limb, and Full Body), Component (Hardware, Software and Services), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 40.33% of 2024 exoskeleton market revenue, supported by a mature payer ecosystem and deep venture funding. Medicare's fixed reimbursement rate of USD 91,032 dramatically improved affordability for spinal cord injury patients, lifting device shipments to Veterans Health Administration centers and Level I trauma hospitals. U.S. industrial employers-including automotive assemblers and parcel logistics firms pilot upper-body exosuits to stem injury downtime, and these projects are progressively converting into framework agreements. Canada follows similar trajectories, with provincial workers' compensation boards underwriting pilot programs that assess claims reduction and productivity gains.

Europe ranks second in revenue, anchored by Germany, France, and the Nordics. Germany's BARMER coverage decision encompassed 8.5 million beneficiaries, bringing reimbursed access to nearly half of statutory-insured citizens. Research collaborations thrive under Horizon Europe grants, linking robotics labs in Aachen, Zurich, and Genoa with clinical partners. Industrial uptake is buoyed by strict ergonomic directives; automotive OEMs in Bavaria deploy shoulder-support exoskeletons on production lines to comply with musculoskeletal exposure thresholds. The evolving ExosCE certification path eases product rollout by combining medical and machinery directives into one dossier, shortening approval timelines.

Asia-Pacific is the fastest-growing cluster at 23.78% CAGR through 2030. South Korean manufacturer WIRobotics launched the WIM gait-assist robot in the United States in 2025, highlighting the region's export ambitions mobihealthnews.com. China's Made-in-China 2025 agenda attaches grant incentives to rehabilitation robotics factories, while Japan's ageing demographics funnel public R&D to assistive mobility. Despite pockets of reimbursement uncertainty, industrial customers in electronics and shipbuilding sectors procure lumbar-support suits en masse to curb compensation claims. Public-private partnerships in Singapore and Australia focus on urban ageing initiatives that integrate exoskeletons with smart-home ecosystems.