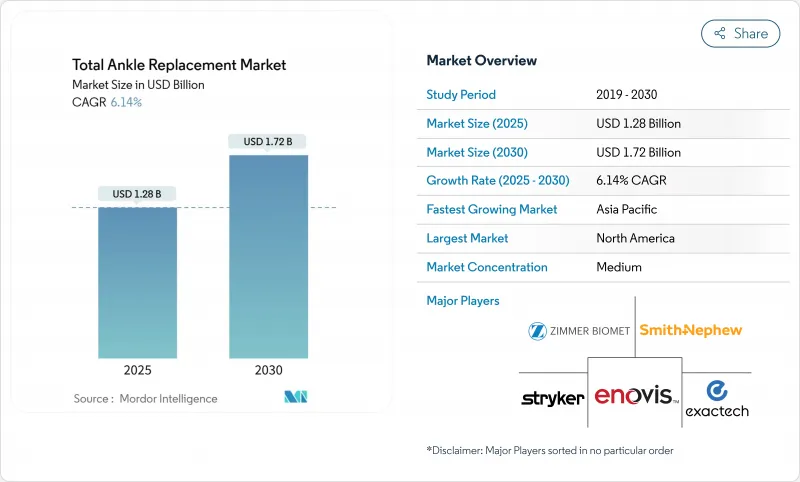

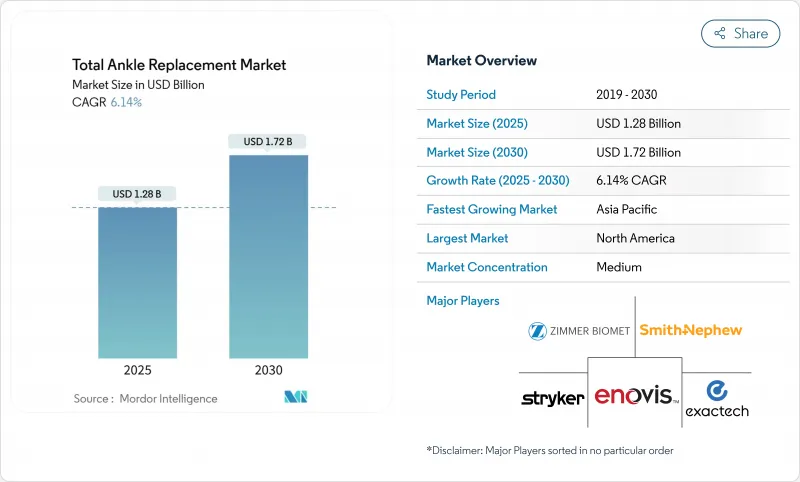

발목관절 전치환술 시장 규모는 2025년에 12억 8,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 6.14%로 성장할 전망이며, 2030년에는 17억 2,000만 달러에 달할 것으로 예측되고 있습니다.

이 성장은 4세대 임플란트가 생존 기간을 연장하고, 재치환 위험을 줄이며, 외과의사가 원래 발목의 바이오메카닉을 모방한 디자인을 선택할 수 있게 됨으로써, 이 수술이 틈새 치료에서 말기 발 관절염의 주류 옵션으로 변화하고 있음을 보여줍니다. 환자 전용 3D 프린팅 컴포넌트, 스마트 기기, 로봇 가이드가 정확도를 향상시키고 임상 가이드라인이 젊고 활동적인 집단에 운동 온존 수술을 추천하게 되었기 때문에 그 채용률은 상승하고 있습니다. CMS가 2024년에 발목관절 전치환술을 입원환자만의 목록에서 제외하고, 병원과 외래수술센터가 같은 날 퇴원의 프로토콜을 중심으로 케어 경로를 재조합하도록 촉구했기 때문에 외래환자로의 이행이 진행되고 있습니다. 짐머 바이오멧이 2025년 파라곤 28을 11억 달러로 인수한 후에도 경쟁 정보에 의한 압박은 여전히 높고, 제조업체는 점유율을 지키기 위해 임플란트에 디지털 플래닝 소프트웨어, 인공지능 대응 센서, 밸류 기반 서비스 계약을 번들하고 있습니다. 보험 상환은 여전히 중요한 요소입니다. 민간 지급기관은 이 수술의 비용 대비 유용성을 고정술과 비교하여 인식하고 있지만, 신흥 시장에서는 여전히 고가의 장비 가격, 제한된 외과의사 훈련, 일관성 없는 보험 적용을 고민하고 있습니다.

고령이며 활동적인 성인으로의 인구통계학적 변화는 골관절염의 발병률을 증가시키고 발목관절 전치환술 시장에 박차를 가하고 있습니다. 외상이 주요 병인이기 때문에 스포츠 참여와 교통사고로 인한 부상이 증가함에 따라 질병 부담이 증가합니다. 임상 연구에 따르면 수술 후 스포츠 복귀율은 31.1%에서 85.4%로 상승하여 최신 임플란트가 노인의 운동 능력과 자립성을 유지하는 것으로 확인되었습니다. 따라서 다국적 의료 시스템은 발목관절 전치환술을 마지막 수단이 아닌 삶의 질을 높이기 위한 개입으로 자리매김하고 관절염의 케어패스에 통합하여 장기적인 수요를 촉진하고 있습니다.

네비게이션 플랫폼 및 로봇 플랫폼은 절제 정밀도를 향상시키고 연부 조직의 손상을 최소화하고 학습 곡선을 단축함으로써 무릎 관절 성형술의 교훈을 발목에 반영합니다. 미국에서는 무릎관절치환술의 약 13%가 이미 로봇을 사용하고 있으며, 주요 정형외과 센터에서는 발목에도 비슷한 워크플로우를 도입하고 있습니다. 로봇 공학은 뼈를 보존하고 침전을 줄이는 측면 접근법을 지원하며, 수술 중 센서는 임플란트의 정렬을 실시간으로 정량화합니다. 이러한 장점으로 인해 이전에는 고정술이 예정되어 있던 변형 사례에도 적응이 퍼지고 외래 프로토콜의 매력이 늘어남과 동시에 발목관절 전치환술 시장이 가속되고 있습니다.

장기 데이터에서 10년 재치환술률은 10.9% 가까이, 20년 재치환술률은 13.5%이며, 인공 고관절 치환술이나 인공 슬관절 치환술보다 상당히 높습니다. 인공관절 주위 감염의 위험은 1%에서 14%이며 발목의 연부 조직 포피는 상처 치유를 복잡하게 합니다. FDA는 2024년에 16.1% 이상의 고장률로 힌터맨 H3 시스템에 경고를 내리고 경계가 필요하다고 강조했습니다. 외과의사는 적응증의 엄격화, 수술 전 최적화의 연장, 양측 증례의 제한 등으로 대응하고 있지만, 이들 모두는 인공 발목관절 전치환술 시장의 수술 건수의 성장을 억제하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

INBONE II와 INFINITY 플랫폼의 2024년 매출 점유율은 33.74%로 발목관절 전치환술 시장에서 가장 큰 점유율을 차지했습니다. 이 회사의 모듈형 경골 줄기는 짧은 골간부 포스트에서 긴 수내 부문까지 맞춤형 고정을 제공하며, 이 접근법은 재치환 및 골다공증 사례의 초기 안정성을 향상시킵니다. 7년 생존율은 95.9%로 중기 성능의 신뢰성을 뒷받침합니다. 경쟁업체와의 차별화의 중심은 설치 시간과 방사선 노출을 줄이는 통합된 환자별 가이드와 간소화된 기구 세트이며, 이는 외래 환경에서 중요한 이점입니다. 병행하여 실시되는 임상 프로그램은 시상면과 관상면의 움직임이 거의 네이티브임을 나타내는 투시운동학적 데이터를 수집하여 지불자에게 제출하는 근거 패키지를 강화함과 동시에 인공족관절 전치환술 시장에서의 리더십을 더욱 견고하게 하고 있습니다.

CAGR은 2030년까지 연평균 복합 성장률(CAGR) 8.96%로 추이하였으며, 폴리에틸렌 제형, 거골 돔 곡률, 간소화된 측면 접근 기구의 획기적인 진보에 힘입어 초기 결과 등록에 따르면 2년 후 환자 만족도는 98%이며, 외과의사는 지역 병원의 학습 곡선을 줄이는 단순화된 골절제술을 보고했습니다. VANTAGE, STAR, SALTO Talaris는 각기 다른 베어링 철학과 지역별 상환의 발판을 활용하여 충실한 지지를 유지하고 있습니다. Paragon 28의 3D 프린팅 APEX 시스템은 산화 및 마모에 견딜 수 있는 다공성 해면체 표면과 비타민 E 안정화 라이너를 추가합니다. 향후 예측에서 설계 혁신은 임상가가 임플란트의 건강 상태를 원격으로 모니터링할 수 있는 스마트 센서 통합 및 MRT 적합 합금에 달려 있으며, 재수술을 촉진하고 제조업체에 2차 수익원을 가져올 것으로 보입니다.

북미는 2024년 매출의 43.24%를 차지했으며, CMS 적용 범위, 높은 외과의 밀도, 프리미엄 임플란트에 대한 소비자의 지불 의향에 의해 세계의 임상 가이드라인 개발의 중심이 되고 있습니다. 미국의 의사는 연간 1만 1,000건 이상의 발관절 치환술을 실시하고 있으며, 얼라인먼트를 최적화하기 위해 인대 재건술 등을 병용하는 경우가 많습니다. 캐나다는 온타리오와 앨버타의 공공 자금으로 운영되는 전문센터를 통해 기여하고 있지만, 멕시코의 민간 부문은 중미에서 운동 기능 온존 수술을 요구하는 의료 관광객을 받아들이고 있습니다.

유럽은 여전히 2위의 클러스터이며, 독일, 프랑스, 영국은 엄격한 CE 마크 요구사항과 비용 효과 임계값 하에서 그 수를 선도하고 있습니다. 각국의 의료제도는 장기적인 재치환율을 정사하는 의료기술 평가를 실시하고 있으며, 제조업체는 검토를 받은 생존율의 데이터를 공표하도록 장려하고 있습니다. 스칸디나비아 국가들은 유럽의 상환 협상에 영향을 미치는 레지스트리의 견해를 공유합니다.

인구 고령화 및 가처분소득 증가로 고도의 정형외과 의료에 대한 수요가 높아지는 가운데 아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 10.92%로 가장 급성장이 전망되는 지역입니다. 중국은 상하이와 베이징에서 휄로우십 프로그램을 강화하고, 일본은 국민 모두 보험제도를 활용하여 특정 기술을 커버하며, 인도 Tier-1 병원은 국내 의료 관광객을 유치하고 있습니다. 외상의 다발과 당뇨병 인구의 많음이 함께 관절염의 부담이 증가하고, 발목관절 전치환술 시장에 비옥한 확대 통로를 만들어 내고 있습니다. 중동 및 아프리카와 남미에서는 민간 병원 체인이 전문 지식을 수입하고 있기 때문에 급속히 보급이 진행되고 있지만, 환율 변동 및 자기 부담의 역학이 당면 수술 건수를 억제하고 있습니다.

The Total Ankle Replacement Market size is estimated at USD 1.28 billion in 2025, and is expected to reach USD 1.72 billion by 2030, at a CAGR of 6.14% during the forecast period (2025-2030).

This growth shows the procedure's transformation from a niche therapy to a mainstream option for end-stage ankle arthritis as fourth-generation implants extend survivorship, reduce revision risk, and allow surgeons to select designs that mimic native ankle biomechanics. Adoption is rising as patient-specific 3D-printed components, smart instrumentation, and robotic guidance improve accuracy, while clinical guidelines now recommend motion-preserving surgery for younger and more active cohorts. Outpatient migration advances because CMS removed total ankle arthroplasty from the inpatient-only list in 2024, prompting hospitals and ambulatory surgical centers to re-organize care pathways around same-day discharge protocols. Competitive pressure remains high after Zimmer Biomet's USD 1.1 billion acquisition of Paragon 28 in 2025, and manufacturers continue to bundle implants with digital planning software, artificial-intelligence-enabled sensors, and value-based service agreements to protect share. Reimbursement remains a critical factor; although commercial payers increasingly recognize the procedure's cost-utility versus fusion, emerging markets still wrestle with high device prices, limited surgeon training, and inconsistent insurance coverage.

The demographic shift toward older, more active adults elevates the incidence of ankle osteoarthritis and fuels the total ankle replacement market. Trauma is the leading etiology, so the disease burden grows as sports participation and road traffic injuries increase. Clinical studies show postoperative return-to-sport rates climbing from 31.1% to 85.4%, confirming that modern implants maintain mobility and independence among seniors. Multinational health systems, therefore, position total ankle arthroplasty as a quality-of-life intervention rather than a last resort, embedding it into arthritis care pathways and driving long-term demand.

Navigation and robotic platforms translate lessons from knee arthroplasty to the ankle by improving resection accuracy, minimizing soft-tissue disruption, and shortening learning curves. About 13% of United States knee replacements already use robotics, and leading orthopedic centers now deploy similar workflows for ankles. Robotics supports lateral approaches that conserve bone and mitigate subsidence, while intraoperative sensors quantify implant alignment in real time. These advantages widen candidacy to deformity cases previously slated for fusion and enhance the appeal of outpatient protocols, together accelerating the total ankle replacement market.

Long-term datasets reveal 10-year revision rates near 10.9% and 20-year rates at 13.5%, materially higher than hip or knee arthroplasty. Periprosthetic infection risks run from 1% to 14%, and ankle soft-tissue envelopes complicate wound healing. The FDA flagged the Hintermann H3 system in 2024 for failure rates exceeding 16.1%, underscoring vigilance requirements. Surgeons respond by tightening indications, extending preoperative optimization, and limiting bilateral cases, all of which temper procedure volume growth within the total ankle replacement market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

INBONE II and INFINITY platforms combined for a 33.74% revenue share in 2024, giving them the most significant stake in the total ankle replacement market. Their modular tibial stems provide customizable fixation ranging from short metaphyseal posts to long intramedullary segments, an approach that improves initial stability in revision and osteoporotic cases. Seven-year survivorship of 95.9% underscores dependable mid-term performance, and global users passed 48,000 implants by 2024. Competitive differentiation centers on integrated patient-specific guides and streamlined instrumentation sets that cut setup time and radiation exposure, advantages prized in ambulatory settings. Parallel clinical programs collect fluoroscopic kinematic data that illustrate near-native sagittal and coronal plane motion, bolstering evidence packages for payer submissions and further fortifying leadership in the total ankle replacement market.

CADENCE rose on an 8.96% CAGR trajectory through 2030, propelled by breakthroughs in polyethylene formulation, talar dome curvature, and streamlined lateral approach instrumentation. Early outcome registries show 98% patient satisfaction at two years, and surgeons report simplified bone resections that trim learning curves for community hospitals. VANTAGE, STAR, and SALTO Talaris retain loyal followings, each leveraging distinct bearing philosophies and regional reimbursement footholds. Paragon 28's 3D-printed APEX system adds porous trabecular surfaces and vitamin E stabilized liners to resist oxidation and wear. Over the forecast, design innovations will hinge on smart sensor integration and MRT-compatible alloys that let clinicians monitor implant health remotely, fueling repeat procedures and secondary revenue streams for manufacturers.

The Total Ankle Replacement Market Report is Segmented by Design (HINTEGRA, STAR, SALTO / SALTO Talaris, and More), Bearing Type (Mobile-Bearing Systems, Fixed-Bearing Systems, Hybrid / Semi-Constrained), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 43.24% of revenue in 2024 and anchors global clinical guideline development, driven by CMS coverage, high surgeon density, and consumer willingness to pay for premium implants. United States physicians perform more than 11,000 ankle replacements annually and frequently combine procedures such as ligament reconstruction to optimize alignment. Canada contributes through publicly funded specialist centers in Ontario and Alberta, whereas Mexico's private sector captures medical tourists from Central America seeking motion-preserving procedures.

Europe remains the second-largest cluster, with Germany, France, and the United Kingdom leading volumes under stringent CE-mark requirements and cost-utility thresholds. National health systems conduct health-technology assessments that scrutinize long-term revision rates, encouraging manufacturers to publish peer-reviewed survivorship data. Scandinavian countries share registry insights that influence broader European reimbursement negotiations.

Asia-Pacific is the fastest-growing region at a 10.92% CAGR to 2030 as aging populations and rising disposable income heighten demand for advanced orthopedic care. China ramps fellowship programs in Shanghai and Beijing, Japan leverages universal insurance to cover select technologies, and India's tier-1 hospitals attract domestic medical tourists. The combination of heavy trauma incidence and large diabetes populations increases arthritis burden, creating a fertile expansion corridor for the total ankle replacement market. Middle East and Africa plus South America show nascent uptake as private hospital chains import expertise, though currency fluctuations and out-of-pocket dynamics temper near-term procedure counts.