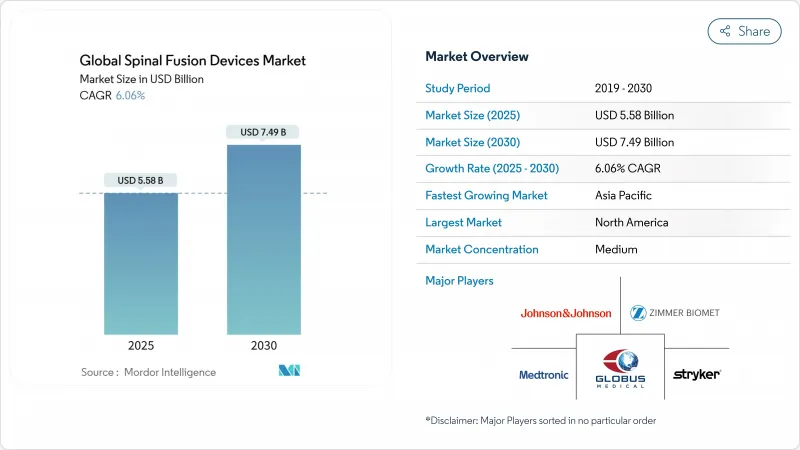

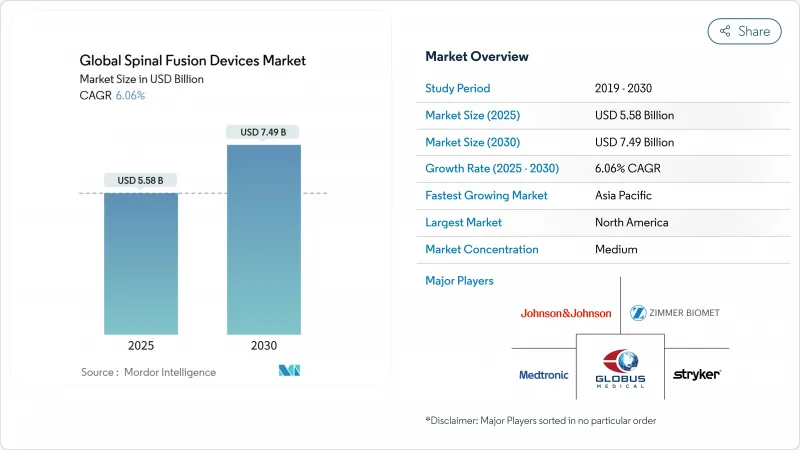

척추 고정 기기 시장 규모는 2025년 55억 8,000만 달러로 추정되고, 2030년에는 74억 9,000만 달러로 상승할 전망이며, CAGR 6.06%로 성장할 것으로 예측됩니다.

견고한 수요는 인구 역학의 고령화, 퇴행성 척추 질환 증가, 저침습 및 인공지능 대응 수술 플랫폼의 채택 가속에 기인합니다. 병원과 외래수술센터(ASC)는 메디케어가 외래로 상환되는 고정술 건수를 4배 이상으로 늘려 수술 건수를 확대하고 있어 케이스 믹스의 꾸준한 전환이 강화되고 있습니다. 3D 프린터로 제작한 환자 전용 케이지의 FDA 인가가 급속히 내려지고, 최신 로봇 시스템에 의한 96.99%의 스크류 설치 정밀도가 달성됨으로써, 경쟁사와의 차별화가 격화하고 있습니다. 이와 병행하여, 일괄 지불에 대한 지불자의 이동이 가격 설정을 압박하고 있지만, 가치 주도형 임플란트의 개발에도 박차를 가하고 있어, 모든 제품 클래스의 기술 혁신이 자극되고 있습니다.

저침습 척추 수술은 고정술의 성공률을 동등하게 유지하면서 입원 기간의 단축, 절개창의 축소, 합병증 발생률의 저하를 실현함으로써 오랜 개복 수술을 뒤집고 있습니다. 경추체적 요추체간 고정술에 관한 메타분석에서는 수혈 횟수가 적고 합병증 발생률은 개복 수술의 14.97%에 비해 4.83%인 것으로 확인되었습니다. 로봇 내비게이션은 스크류의 정확도를 96% 이상으로 높여 장비 제조업체에게 임플란트, 내비게이션, 수술 중 이미지의 번들화를 촉구하고 있습니다. 현재, 휄로우십 프로그램은 이러한 기술을 우선시하고 있으며, 로봇 지원 워크플로우에 익숙한 외과의의 파이프라인을 확보하고 있습니다. 병원은 또한 환자의 회복을 가속화하여 침대 회전율을 향상시키고 임상 성적과 가치 기반 구매를 직접 일치시키는 데 활용합니다.

앉아있는 라이프 스타일, 비만 및 진단의 엄밀화로 요추 추간판 변성의 이환율은 지난 60년간 90% 이상으로 상승했습니다. 보다 조기 영상 진단을 통해 시기 적절한 수술을 소개할 수 있으며, 다층병으로의 진행을 피할 수 있습니다. 의료경제학적 분석에 따르면 조기 고정술은 만성 통증의 지출을 감소시키는 것으로 입증되었으며, 지불자는 그에 따라 보험 적용을 확대하고 있습니다. 임상 등록은 조기 요추 단층 고정술이 재수술의 빈도를 줄이고 질 조절 생존 수명을 증가시키는 것으로 확인되었습니다. 장치 제조업체는 단층 상태에 최적화된 확장 가능한 케이지 및 생물학적 제제 포트폴리오를 확장하여 대응합니다.

번들 지불 파일럿은 에피소드의 총 비용에 상한을 설정하기 때문에 의료 제공업체는 임플란트의 성능과 가격을 비교 검토해야 할 필요가 없습니다. 경추 고정술의 수술 중 비용은 7,574달러에 이르고, 그 69%는 하드웨어와 관련이 있습니다. 병원은 재수술 책임을 최소화하는 플랫폼을 지원하고 수량 계약을 재협상합니다. 제조업체는 보험료 태그를 지키기 위해 질 조정 생존년당 비용을 10만 달러 이하로 나타내는 증거 서류를 발행하게 되었습니다. 가치를 명확히 할 수 없는 기업은 척추 고정 기기 시장에서 점유율 저하의 위험이 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

요추 고정 기기는 2024년 척추 고정 기기 시장 점유율의 43.68%를 차지했고, 척추 미끄럼증이나 추간판 변성증에 대한 주력 솔루션으로서의 역할을 확고히 하고 있습니다. 요추 고정 기기 시장 규모는 입원과 외래 채널 모두에 수요가 지속되어 CAGR 5.8%로 확대될 것으로 예측됩니다. 인터바디 케이지는 97%의 고정 성공률을 보장하는 3D 프린팅 티타늄 격자 덕분에 7.02%의 성장률로 두드러집니다. 외과의사는 신경을 과도하게 후퇴시키지 않고 디스크의 높이와 시상면의 균형을 회복시키는 확장 가능한 케이지를 선호하고 사용합니다. 경추판과 스크류는 경추전방추간판 절제술과 고정술에 안정적인 지지를 얻고 있으며, 그 긴 안전성 기록이 뒷받침하고 있습니다. 흉추 시스템은 틈새 외상 및 변형 요구를 충족하지만 재고 효율성을 위해 모듈 구조로 전환하고 있습니다. 페디클 스크류의 기술 혁신은 현재 내비게이션 인서션과 토크 제한 드라이버에 중점을 두어 위치 불량을 줄이고 있습니다. 세포성 골 이식편을 포함한 생물학적 이식편 대체물은 98.5%의 융합을 실현하여 장골 능숙한 이식편에 대한 의존도를 좁히고 있습니다.

재료 과학의 지속적인 발전으로 응력 차폐를 약화시키면서 뼈 통합을 촉진하는 다공성 PEEK와 마그네슘 합금이 사용되고 있습니다. 일 단위로 생산되는 환자 고유의 임플란트는 내부 플레이트의 커버리지 및 하중 분담 특성을 개별적으로 설정할 수 있습니다. 공급업체는 케이지와 이식편을 번들로 패키징하고 ASC의 물류를 단순화합니다. 그럼에도 불구하고 가치 분석위원회는 단가를 조사하고 임상 우월성과 비용 효과를 모두 보여주는 플랫폼으로 병원을 유도하고 있으며,이 균형은 척추 고정 기기 시장 전체의 승자가 결정됩니다.

2024년 척추 고정 기기 시장 규모는 저침습 수술이 62.37%를 차지하였고, 영상 진단, 내비게이션, 관형 리트랙터가 조직 파괴를 억제하게 됨에 따라 2030년까지의 CAGR은 6.34%로 성장할 전망입니다. 개복 수술은 중증의 변형 교정에 있어서 그 역할을 유지하고 있지만, 로봇 지침에 의해 학습 곡선이 단축되기 때문에 점유율은 축소 경향에 있습니다. 실시간 3D 이미지는 경피 페디클 스크류의 궤도가 2mm 이하의 어긋남으로 가능하게 되어 신경학적 위험을 줄였습니다. 한편, 단일 위치 척추 기술은 환자의 반전을 제한하고 마취 시간을 단축합니다. 병원은 이러한 효율성을 이용하여 보다 많은 사례를 외래환자로 퇴원시킬 수 있기 때문에 ASC의 도입이 촉진되어 진료보수의 역학이 재구성됩니다.

척추 고정 기기 시장은 ASC의 처리량에 맞는 컴팩트한 장치 세트, 무균 팩 임플란트, 일회용 네비게이션 어레이를 지원합니다. 교육 센터는 혼합 현실 시뮬레이터로 시체 실험실을 강화하고 외과 의사의 역량을 향상시킵니다. 지불자는 합병증의 발생률이 낮음을 평가하고 일괄 상환 인상을 통해 저침습 경로에 보상합니다. 증거가 성숙함에 따라, 규제 당국은 안전성이 분명히 향상된 키트에 대해 더 짧은 클리어런스 경로를 허용하게 되고, 저침습 접근법이 척추 치료의 주류에 더 정착될 수 있습니다.

북미는 2024년 세계 매출의 46.23%를 차지했고, 2030년까지 연평균 복합 성장률(CAGR) 5.37%로 성장할 전망입니다. 메디케어 58개의 ASC 대상 척추 척수 코드를 통해 외래 센터의 수술 건수는 연간 15.7% 증가하여 저비용 의료 시설로 향하는 척추 고정 기기 시장 동향을 지지하고 있습니다. FDA의 획기적인 지정은 상품화를 촉진하고 이 지역의 혁신에 있어 리더십을 강화하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 6.95%로 가장 빠르게 성장하고 있으며, 병원 인프라 업그레이드, 가처분소득 증가, 휄로우십 훈련을 받은 척추외과의 밑단 확대가 그 요인이 되고 있습니다. 중국의 클래스 III 등록 요건은 길지만, 현지와의 제휴가 시장 접근을 용이하게 해, 지방의 입찰에서는 비용 대비 효과가 높고, 게다가 기술적으로 선진적인 국산 임플란트가 선호되는 경우가 많습니다. 일본과 한국은 인구 동태 고령화에 의해 시장 규모를 확대하고, 인도의 민간병원 체인은 의료 투어리즘을 캡처하기 위해 내비게이션 시스템을 수입하고 있습니다.

유럽의 CAGR 5.80%는 신제품의 출시를 약간 지연시키는 MDR 대응 비용에 의해 완만해진 균형 잡힌 성장을 반영하고 있습니다. 특히 북유럽과 독일에서는 국민 의료 서비스가 외래 환자로의 전환을 촉구하고 있지만 가격 통제가 프리미엄 장비의 이익률에 영향을 미치고 있습니다. 남미에서는 브라질과 아르헨티나가 제3차 의료센터를 업그레이드하고 저침습 기술을 채용함으로써 CAGR 6.12%로 전진할 전망입니다. 중동 및 아프리카는 걸프 국가의 전문 병원에 대한 투자를 배경으로 CAGR 6.46%로 추이하고 있지만, 외과의 부족이 이 지역 전체의 보급을 억제하고 있습니다. 전반적으로, 척추 고정 기기 시장은 세계적으로 확대되고 있지만, 성장 벡터는 상환 환경, 외과 의사의 밀도, 규제 속도에 따라 크게 달라집니다.

The spinal fusion devices market size is estimated at USD 5.58 billion in 2025 and is projected to climb to USD 7.49 billion by 2030, delivering a 6.06% CAGR.

Robust demand stems from demographic aging, rising degenerative spine disorders, and accelerating adoption of minimally invasive and AI-enabled surgical platforms. Hospitals and ambulatory surgery centers (ASCs) are scaling procedure volumes as Medicare has more than quadrupled the number of fusion procedures reimbursed in outpatient settings, reinforcing steady case-mix migration. Rapid FDA clearances for 3-D-printed patient-specific cages and the 96.99% screw-placement accuracy achieved by contemporary robotic systems are intensifying competitive differentiation. In parallel, payers' shift toward bundled payments is pressuring pricing but is also catalyzing the development of value-driven implants, stimulating technological innovation across every product class.

Minimally invasive spine surgery is overturning long-standing open procedures by delivering shorter hospital stays, smaller incisions, and lower complication rates while maintaining equal fusion success. Meta-analyses of transforaminal lumbar interbody fusion confirm fewer transfusions and a 4.83% complication rate versus 14.97% for open surgery. Robotic navigation drives screw accuracy beyond 96%, prompting device manufacturers to bundle implants, navigation, and intra-operative imaging. Fellowship programs now prioritize these techniques, ensuring a pipeline of surgeons fluent in robot-assisted workflows. Hospitals also leverage the faster patient recovery to improve bed turnover, directly aligning clinical performance with value-based purchasing.

Sedentary lifestyles, obesity, and greater diagnostic scrutiny have raised lumbar disc degeneration incidence to more than 90% in individuals past 60 years. Earlier imaging enables timely surgical referral, averting progression to multilevel disease. Health-economic analyses prove that early fusion lowers chronic pain expenditure, and payers are expanding coverage accordingly. Clinical registries confirm that early single-level lumbar fusion reduces re-operation frequency and boosts quality-adjusted life years. Device makers respond by broadening portfolios of expandable cages and biologics optimized for single-level pathology.

Bundled-payment pilots cap total episode cost, forcing providers to weigh implant performance against price. Cervical fusion intra-operative expenses reach USD 7,574, with 69% tied to hardware. Hospitals renegotiate volume contracts, favoring platforms that minimize re-operation liability. Manufacturers now issue evidence dossiers showing cost per quality-adjusted life year below USD 100,000 to defend premium tags. Firms unable to articulate value risk share erosion in the spinal fusion devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Lumbar fusion devices generated 43.68% of the 2024 spinal fusion devices market share, cementing their role as workhorse solutions for spondylolisthesis and disc degeneration. The spinal fusion devices market size for lumbar instrumentation is projected to expand at a 5.8% CAGR as demand persists across both inpatient and outpatient channels. Interbody cages stand out with a 7.02% growth rate thanks to 3-D-printed titanium lattices that secure 97% fusion success. Surgeons favor expandable cages that restore disc height and sagittal balance without excessive nerve retraction. Cervical plates and screws maintain consistent uptake for anterior cervical discectomy and fusion, underscored by their long safety record. Thoracic systems meet niche trauma and deformity needs but are turning to modular constructs for inventory efficiency. Pedicle screw innovation now focuses on navigated insertion and torque-limiting drivers, reducing mal-position. Biologic graft substitutes, including cellular bone allografts, realize 98.5% fusion, narrowing reliance on iliac crest autografts.

Continued material science advances exploit porous PEEK and magnesium alloys that encourage osteointegration while dampening stress shielding. Patient-specific implants, produced in days, personalize endplate coverage and load-sharing characteristics. Vendors increasingly package cage-graft bundles, simplifying logistics for ASCs. Still, value-analysis committees scrutinize unit price, steering hospitals toward platforms demonstrating both clinical superiority and cost-effectiveness, a balance that will define winners across the spinal fusion devices market.

Minimally invasive procedures held 62.37% spinal fusion devices market size in 2024, posting a 6.34% CAGR through 2030 as imaging, navigation, and tubular retractors converge to curtail tissue disruption. Open surgery retains a role in severe deformity corrections yet faces shrinking share as robotic guidance abbreviates learning curves. Real-time 3-D imaging permits percutaneous pedicle screw trajectories with sub-2 mm deviation, lessening neurologic risk. Meanwhile, single-position spine techniques limit patient flips, shaving anesthesia time. Hospitals harness these efficiencies to qualify more cases for outpatient discharge, buoying ASC adoption and reshaping reimbursement dynamics.

The spinal fusion devices market responds with compact instrument suites, sterile-packed implants, and disposable navigation arrays tailored to ASC throughput. Training centers augment cadaveric labs with mixed-reality simulators, accelerating surgeon competency. Payers reward minimally invasive pathways via bundled reimbursement uplift for low complication incidence. As evidence matures, regulators may green-light shorter clearance paths for kits demonstrably improving safety, further embedding minimally invasive approaches into mainstream spine care.

The Spinal Fusion Devices Market Report is Segmented by Product Type (Cervical Fusion Devices, Thoracic Fusion Devices, and More), Type of Surgery (Open Spine Surgery and Minimally Invasive Spine Surgery), Surgical Approcah (TLIF, PLF, and Other Approaches), End-User (Hospitals and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 46.23% to global revenue in 2024 and should grow at 5.37% CAGR through 2030 as premium robotics and 3-D-printed implants penetrate both inpatient and outpatient settings. Medicare's 58 ASC-eligible spine codes have catalyzed a 15.7% annual procedure rise in ambulatory centers, underpinning the spinal fusion devices market trend toward lower-cost sites of care. FDA breakthrough designations expedite commercialization, reinforcing the region's innovation leadership.

Asia-Pacific is the swiftest climber with a 6.95% CAGR to 2030, leveraging hospital infrastructure upgrades, rising disposable incomes, and an expanding base of fellowship-trained spine surgeons. China's Class III registration requirements are lengthy, yet local partnerships ease market access, and provincial tenders often favor cost-effective, yet technologically advanced, domestically produced implants. Japan and South Korea add volume through aging demographics, while India's private hospital chains import navigated systems to capture medical tourism.

Europe's 5.80% CAGR reflects balanced growth moderated by MDR compliance costs that slightly slow new-product launches. National health services encourage outpatient migration, particularly in the Nordics and Germany, but pricing controls challenge premium device margins. South America advances at 6.12% CAGR as Brazil and Argentina upgrade tertiary centers and adopt minimally invasive techniques. Middle East and Africa post 6.46% CAGR on the back of Gulf States' specialist hospital investments, although surgeon shortages restrain broader regional uptake. Overall, the spinal fusion devices market is expanding worldwide, yet growth vectors differ markedly by reimbursement climate, surgeon density, and regulatory velocity.