Spinal Fusion Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801935

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 150 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

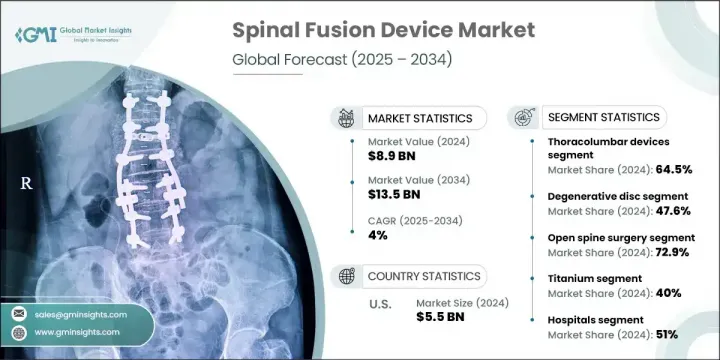

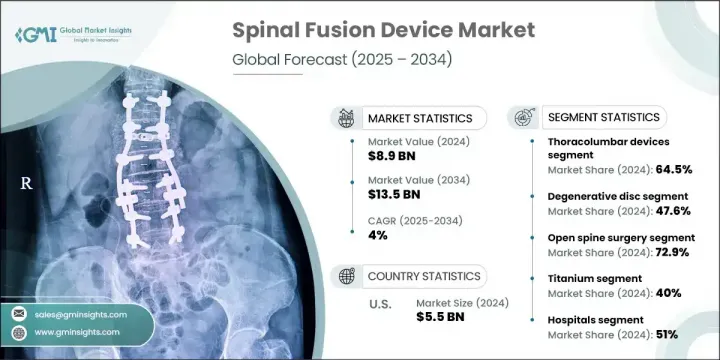

세계 척추 고정 기기 시장은 2024년 89억 달러로 평가되었으며 CAGR 4%로 성장하여 2034년 135억 달러에 이를 것으로 추정됩니다.

시장의 상승세는 척추질환 증가, 대상 환자 증가, 보다 고도로 저침습적인 고정술을 개발하기 위한 연구개발에 대한 지속적인 투자에 의해 추진되고 있습니다. 긍정적인 전망과는 달리, 일부 신흥국에서는 상환의 선택지가 한정되어 있어 시장의 본격적인 확대에는 과제가 남습니다. 그럼에도 불구하고, 척추 외과 수술의 진보와 세계의 고령화율의 상승은 계속해서 수요를 높이고 있습니다. 특히 수술 중 영상 진단, 로봇 공학, 내비게이션 등의 기술 진화는 수술 합병증의 경감과 치료 성적의 향상에 도움이 되고 있습니다.

흉추 장치 부문은 2024년에 64.5%의 점유율을 차지했는데, 이는 흉추와 요추 모두에서 수술적 안정화가 필요한 요추 변성 질환 및 척추 손상의 빈도가 높기 때문입니다. 이 부문의 성장은 노인의 충격성이 높은 외상과 척추 변성의 비율이 증가하는 것이 큰 요인이 되었습니다. 게다가, 척추 골절과 척추 미끄럼증과 같은 증상은 안정성과 회복을 향상시키는 정밀 공학 장비를 사용합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034

시작금액

89억 달러

예측 금액

135억 달러

CAGR

4%

2024년에는 퇴행성 추간판 질환 분야가 47.6%의 점유율을 차지했습니다. 이 이점은 노화에 따른 추간판 변성 사례의 급증과 침습성이 낮은 척추고정술의 광범위한 채택에 기인합니다. 추간판 관련 문제를 경험하는 노인이 증가함에 따라 효율적이고 위험이 낮은 치료에 대한 요구가 계속 증가하고 있습니다. 조기 발견, 환자 의식, 낮은 침습 수술에 대한 신뢰가 높아지면서도 이 부문의 성과를 높이는 데 중요한 역할을 합니다.

미국의 척추 고정 기기 시장 규모는 2024년에 55억 달러의 수익을 올렸습니다. 이 성장은 혁신적인 수술 도구와 수술이 널리 받아들여지고 있는 것 외에, 노인 환자 증가와 척추 질환의 부담이 큰 것에 기인하고 있습니다. 이 지역은 견고한 건강 관리 시스템, 고급 수술 인프라, 최신 척추 임플란트 및 내비게이션 시스템의 호의적인 채택으로 이익을 얻고 있습니다. 2021년 시장 규모는 42억 달러, 2022년에는 47억 달러로 임상 수요와 기술 향상으로 매년 꾸준히 증가하고 있습니다.

세계 척추 고정 기기 시장의 선두 기업은 Stryker, Globus Medical, Medtronic, NuVasive, DePuy Synthes 등 입니다. 시장 존재를 강화하기 위해 척추 고정 기기의 주요 제조업체는 로봇 지원 수술, AI 탑재 네비게이션 시스템, 저 침습 제품 개발에 많은 투자를 하고 있습니다. 이 회사들은 R&D 및 적극적인 인수를 통해 제품 포트폴리오를 확장하고 엔드 투 엔드 척추 솔루션을 제공합니다. 또한 병원 및 수술센터와의 전략적 파트너십을 통해 고급 장비의 신속한 도입이 가능합니다. 일부 기업은 고성장 시장에 더 나은 서비스를 제공하기 위해 생산 현지화와 판매망 강화를 추진하고 있습니다. 지속적인 외과의사 교육 프로그램과 디지털 플랫폼의 통합은 지역 전반에 걸쳐 수술의 정확성과 도입률을 더욱 향상시킵니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

척추질환의 유병률 증가

기술적 진보

외상 및 상해 건수 증가

고령화 인구 증가와 낮은 침습 수술 수요 증가

업계의 잠재적 위험 및 과제

엄격한 규제 시나리오

척추 수술의 고액 비용

시장 기회

외래수술센터(ASC)의 성장

로봇 수술과 내비게이션 지원 수술 도입 증가

성장 가능성 분석

규제 상황

기술의 상황

현재의 기술 동향

네비게이션 시스템과 로봇 시스템의 통합

PEEK 및 티탄 케이지의 보급

신흥기술

3D 프린팅과 척추 임플란트의 진보

센서 통합형 스마트 임플란트

장래 시장 동향

갭 분석

Porter's Five Forces 분석

PESTEL 분석

밸류체인 분석

상환 시나리오

소비자 행동 분석

비교 분석 : 전방 접근 및 후방 접근

제4장 경쟁 구도

소개

기업 매트릭스 분석

기업의 시장 점유율 분석

세계

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추정 및 예측 : 제품 유형별, 2021년-2034년

주요 동향

흉곽 장치

페디클 나사

추간체 고정 장치(IBFD)

Rods

Plates

기타 흉추 장치

경추고정장치

추간체 고정 장치(IBFD)

Plates

Rods

Hooks

기타 경추 장치

제6장 시장 추정 및 예측 : 질환 유형별, 2021년-2034년

주요 동향

변성 추간판

척추 변형

외상과 골절

척추 종양

기타 질병의 유형

제7장 시장 추정 및 예측 : 수술별, 2021년-2034년

주요 동향

개흉 척추 수술

저침습 척추 수술

제8장 시장 추정 및 예측 : 재료 유형별, 2021년-2034년

주요 동향

티타늄

폴리에테르에테르케톤(PEEK)

코발트 크롬

스테인레스 스틸

기타 재료

제9장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

주요 동향

병원

외래수술센터(ASC)

정형외과 클리닉

기타 용도

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

ATEC

B. Braun

Captiva Spine

ChoiceSpine

DePuy Synthes

Globus Medical

K2M

Life Spine

Medtronic

NuVasive

Orthofix

Premia Spine

Stryker

Xtant Medical

Zimmer Biomet

SHW

영문 목차

영문목차

The Global Spinal Fusion Device Market was valued at USD 8.9 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 13.5 billion by 2034. The market's upward momentum is fueled by the rising number of spinal disorders, a growing pool of target patients, and ongoing investments in R&D to develop more advanced and minimally invasive fusion procedures. Despite the positive outlook, limited reimbursement options in several emerging countries remain a challenge for full market scalability. Nevertheless, advancements in spinal surgery and the rise in aging populations worldwide continue to elevate demand. Technological evolution, particularly in intraoperative imaging, robotics, and navigation, is helping reduce surgical complications and improve outcomes.

The thoracolumbar devices segment held 64.5% share in 2024, owing to the high frequency of lumbar degenerative disorders and spinal injuries that necessitate surgical stabilization in both the thoracic and lumbar spine. Growth in this segment is largely driven by increasing rates of high-impact trauma and spine degeneration among older adults. Additionally, conditions like spinal fractures and spondylolisthesis are being addressed with precision-engineered devices to improve stability and recovery.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$8.9 Billion

Forecast Value

$13.5 Billion

CAGR

4%

In 2024, the degenerative disc disorder segment held a 47.6% share. This dominance is attributed to a surge in cases of age-related disc degeneration and the broader adoption of less invasive spinal fusion methods. As more elderly individuals experience disc-related issues, the need for efficient, lower-risk treatment continues to climb. Earlier detection, patient awareness, and growing trust in minimally invasive procedures also play vital roles in boosting the segment's performance.

US Spinal Fusion Device Market generated USD 5.5 billion in 2024. This growth stems from an increasing number of geriatric patients and a high burden of spinal disorders, along with broader acceptance of innovative surgical tools and techniques. The region benefits from a robust healthcare system, advanced surgical infrastructure, and favorable adoption of modern spinal implants and navigation systems. The market was valued at USD 4.2 billion in 2021 and USD 4.7 billion in 2022, showing steady annual increases fueled by clinical demand and technological improvements.

Top companies in the Global Spinal Fusion Device Market include Stryker, Globus Medical, Medtronic, NuVasive, and DePuy Synthes. To strengthen their market presence, leading spinal fusion device manufacturers are investing heavily in robotic-assisted surgery, AI-powered navigation systems, and minimally invasive product development. These firms are expanding their product portfolios through R&D and targeted acquisitions to offer end-to-end spinal solutions. Strategic partnerships with hospitals and surgical centers are also enabling quicker adoption of advanced devices. Several companies are localizing production and strengthening distribution networks to better serve high-growth markets. Continuous surgeon training programs and digital platform integration are further enhancing procedural precision and adoption rates across geographies.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Product type trends

2.2.2 Disease type trends

2.2.3 Surgery trends

2.2.4 Material type trends

2.2.5 End use trends

2.2.6 Region trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing prevalence of spinal diseases

3.2.1.2 Technological advancements

3.2.1.3 Rise in number of trauma and injury cases

3.2.1.4 Rising geriatric population coupled with high demand for minimally invasive procedures

3.2.2 Industry pitfalls and challenges

3.2.2.1 Stringent regulatory scenario

3.2.2.2 High cost of spinal procedures

3.2.3 Market opportunities

3.2.3.1 Growth of ambulatory surgical centers (ASCs)

3.2.3.2 Increasing adoption of robotic and navigation-assisted surgery

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East and Africa

3.5 Technology landscape

3.5.1 Current technological trends

3.5.1.1 Integration of navigation and robotic systems

3.5.1.2 Widespread use of PEEK and titanium cages

3.5.2 Emerging technologies

3.5.2.1 3D Printing, and advances in spinal implants