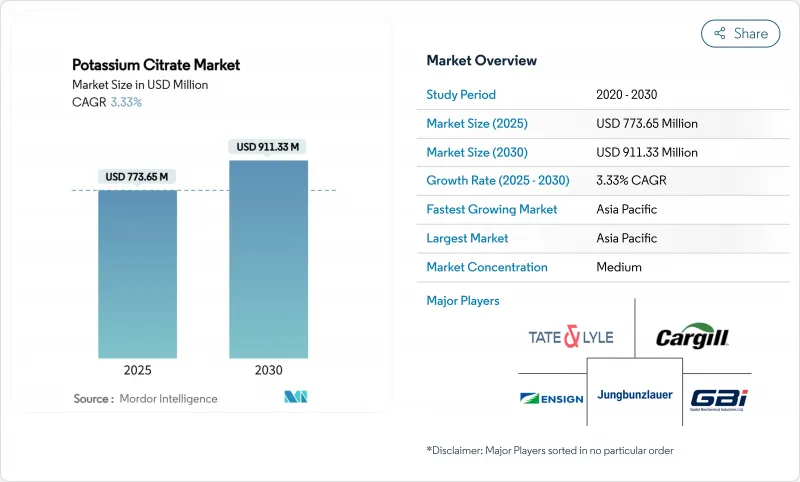

세계의 구연산칼륨 시장은 2025년에는 7억 7,365만 달러로 추정되고, 2030년에는 9억 1,133만 달러에 이를 것으로 예측되며, 예측 기간 동안 CAGR 3.33%로 성장할 것으로 전망됩니다.

이 부드럽고 일관된 성장 궤도는 가공 식품에 대한 나트륨 감소 노력에서 신장 건강 관리를 위한 특수 의약 제제에 이르기까지 다수의 고가치 용도에서 이 화합물의 확고한 지위를 반영합니다. 구연산칼륨 시장의 바닥 견고성은 구연산칼륨이 식품 첨가물과 의약품 원약이라는 두 가지 기능을 겸비한 독특한 특성을 가지며, 건강 지향 제형을 계속 우선하는 2개의 견조한 최종 용도 분야의 교차점에 위치하고 있기 때문입니다. 특히 2024년 8월에 발표된 FDA의 2단계 나트륨 감축 지침은 평균 나트륨 섭취량을 하루 2,750mg까지 줄이는 것을 목표로 하고 있으며, 규제 기세는 시장 역학을 크게 증폭시킵니다. 식품 가공업자는 제품의 기능성을 유지하면서 규제 목표를 달성하기 위해 나트륨 기반 첨가물을 칼륨 대체품으로 대체하는 경향이 강해지고 있으며, 이 노력은 구연산칼륨 제조업체에 직접적인 이익을 가져다줍니다. 동시에, 음료 분야에서는 제품의 안정성과 기호성 향상을 위해 pH 조정제를 중시하는 경향이 강해지고 있으며, 특히 전해질 밸런스가 가장 중요한 기능성 음료나 스포츠 음료의 카테고리로, 새로운 수요 벡터가 태어나고 있습니다.

식품 시스템의 나트륨 감소에 대한 세계적인 노력은 구연산칼륨 시장의 성장을 뒷받침하고 있습니다. 규제 기관이 나트륨 소비를 줄이는 것을 제안하는 동안 구연산칼륨은 유력한 대안으로 주목 받고 있습니다. 구연산칼륨은 나트륨을 포함하지 않기 때문에 기존의 나트륨계 첨가물을 대체할 수 있어 완충작용, 유화작용, 미네랄 강화 등 중요한 기능을 유지할 수 있습니다. 이것은 오랫동안 나트륨 염이 필수적이었던 가공 식품에서 특히 중요합니다. 미국 질병 예방관리센터의 데이터(2024년 1월)는 이 문제를 돋보이게 합니다. 이 과다 복용은 심각한 건강 문제로 이어집니다. 2021년 8월부터 2023년 8월까지 미국 성인 고혈압률은 47.7%에 이르렀고 남성은 50.8%, 여성은 44.6%로 연령에 따라 상승합니다. 규제 상황은 변화하고 있으며, 업계에서는 2026년까지의 준수를 목표로, 나트륨 삭감 대책을 명확하게 추진하고 있습니다. 이 긴급성은 신뢰할 수 있는 나트륨 대체품으로서 구연산칼륨 수요를 밀어 올리고 있습니다. 구연산칼륨은 현재의 식품 제제에 쉽게 통합될 수 있으므로 제조업체는 복잡한 조정을 할 필요가 없습니다. 따라서 제품의 품질과 보존 안정성이 보장되고 건강 기준도 준수됩니다. 소비자의 건강 의식 증가, 나트륨과 심혈관 위험 사이의 확고한 역학적 관련성, 나트륨 규제의 강화는 구연산칼륨의 다양한 식품 용도에 대한 채택 확대에 박차를 가하고 있습니다.

클린 라벨 및 건강 중시 처방에 대한 소비자 선호도의 진화에 힘입어 식품 및 음료 업계는 큰 변화를 맞이하고 있으며, 구연산칼륨 시장에도 현저한 영향을 미치고 있습니다. 구연산칼륨은 공업적으로 합성되었지만 천연 발생 구연산과의 관련성으로 인해 소비자에게 호의적으로 받아 들여지고 있습니다. 면밀한 소비자 조사에 의하면, 천연 소재나 영양가가 높은 소재에 대한 지향이 강해지고 있는 것이 밝혀지고 있습니다. 이러한 추세는 특히 유럽의 천연 식품 첨가물 시장에서 두드러지며, 규제 체계가 천연 유래 또는 천연 공정에 의한 원료를 권장하는 경향을 강화하고 있습니다. 제조업체 각사는 구연산칼륨의 위치를 능숙하게 바꾸고, 전통적인 식품 보존과의 결합을 강조하는 것과 동시에, 심혈관계의 건강이나 전해질 밸런스에 필수적인 칼륨원으로서의 역할을 강조하고 있습니다. 2023년 설문조사에 따르면 미국 응답자의 약 26%가 '천연 염화'를 건강한 식품의 첫 번째 지표로 간주합니다. 이것은 직선적이고 자연적인 제형에 대한 소비자 수요가 증가하고 있음을 뒷받침합니다.

구연산칼륨의 의약품 용도 분야에서 규제 요구 사항이 점점 복잡해지고 개발 기간이 늘어나 제조업체의 컴플라이언스 비용이 증가하고 있습니다. 의약품 등급 구연산칼륨에 대한 FDA의 의약품 마스터 파일 요구 사항은 제조 공정, 불순물 프로파일 및 안정성 데이터의 광범위한 문서화를 요구하며, 고가치 의약품 시장 진입을 목표로하는 소규모 공급업체에게는 장벽이 되고 있습니다. USP의 모노그래프 요건은 의약품 용도에 99.5% 이상의 엄격한 순도 기준이 지정되어 있어 고급 제조 공정과 품질 관리 시스템이 필요해 제조 비용이 상승합니다. 국제적인 하모나이제이션 노력은 장기적으로는 유익하지만, 제조업체가 주요 시장 간에 서로 다른 요구사항을 극복해야 하기 때문에 단기적으로는 컴플라이언스의 복잡성을 낳습니다. 특히 구연산칼륨이 다른 유효 성분과 상호작용하는 제제는 규제 상황이 엄격해지고 대규모 안정성 시험 및 적합성 시험이 필요합니다. 이러한 컴플라이언스 요건은 기존 규제 인프라를 보유한 의약 제조업체에게 유리하지만, 시장 진입 장벽을 형성하고 프리미엄 부문의 경쟁력을 제한합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

2024년에는 순도 99% 이상을 자랑하는 고순도 구연산칼륨 부문이 42.44% 시장 점유율을 차지했습니다. 이 동향은 특히 고급 의약품과 틈새 식품 용도에서 초정제 제제에 대한 의욕이 높아지고 있음을 부각하고 있습니다. 엄격한 규제 기준과 제제 정밀도의 가장 중요성이 수요 급증의 주요 요인이 되었습니다. 의약품과 같이 미량의 불순물이라도 안전성이나 치료 효과를 손상시킬 수 있는 분야에서는 순도를 중시하는 것이 매우 중요합니다. 구연산칼륨은 특히 신장 치료와 서방형 의약품에서 활성 성분과 완충제의 두 가지 역할을 담당합니다. 이 부문의 이점은 순도와 엄격한 품질 기준에 대한 업계의 흔들림없는 헌신을 뒷받침합니다. 한편, 순도 98-99%의 층은 식품 가공이나 기능적 성능이 중요하지만 초고순도가 필수 조건이 아닌 일부 공업 용도에서 틈새 존재가 되고 있습니다.

한편, 순도 98% 미만의 부문은 가장 급속히 확대되고 있어 현저한 CAGR 4.64%를 자랑하고 있습니다. 그 성장 궤도를 뒷받침하는 것은 절대 순도보다 비용 효율과 일관된 운영을 우선하는 대량 생산 용도에서의 매력입니다. 주요 촉진요인으로는 동물영양학, 벌크푸즈 생산, 다양한 분야에서 pH 조정 등에서의 사용이 급증하고 있는 것을 들 수 있습니다. 이에 대응하기 위해, 제조업체 각사는 방향 전환을 도모해, 필수 불가결한 기능 요구를 충족시키고, 초정제라고 하는 비교적 높은 느낌을 회피한, 보다 저비용의 구연산칼륨 제제를 전개하고 있습니다. 이러한 순도 기호의 차이는 성숙해지고 있는 시장 상황을 그려내고 있습니다. 구연산칼륨은 일반적인 제품에서 최종 사용자의 다양한 수요에 부응하는 맞춤형 솔루션으로 진화하고 있습니다. 이러한 진화는 기술 혁신에 박차를 가할 뿐만 아니라 공급망의 적응성과 경쟁력을 높여주며, 고급품 및 저가 제품 모두의 시장 부문에 걸쳐 있습니다.

2024년 아시아태평양은 31.32%의 점유율을 차지했으며, 최대 지역 시장으로 떠올랐을 뿐만 아니라 2030년까지 예측 CAGR 5.44%로 급성장을 보일 전망입니다. 이 성장의 주요 요인은이 지역의 식품 가공 인프라의 확대 및 도시 주민의 건강 의식 증가에 있습니다. 현재 진행중인 무역 조사와 안티덤핑의 심사는 구연산염 생산에 있어서 중국의 주도적 역할을 부각하고 있습니다. 인도에서는 제약 부문이 급성장하고 제네릭 의약품 제조에 필수적인 고순도 구연산칼륨에 대한 수요가 증가하고 있습니다. 동시에 인도에서는 가공식품 산업이 확대되고 있어 식품 등급의 용도로 큰 생산 기회가 있습니다. 한편, 일본과 호주는 기능성 식품이나 영양 보조 식품 등 고급 용도에 주력함으로써 이 지역의 성장을 견인하고 있습니다.

북미는 성숙하고 있지만, 수요를 다시 형성하는 규제적 대처가 주요 원동력이 되어 진화를 이루고 있습니다. FDA에 의한 나트륨 감축에 대한 지침은 나트륨 대체품으로서 구연산칼륨에 대한 일관된 수요에 박차를 가했습니다. 동시에 북미의 첨단 제약 부문은 특수 치료 용도에 맞는 고순도 등급에 대한 안정적인 수요를 보장합니다. 주목해야할 것은 캐나다가 중국과 나란히 무역조사에 관여함에 따라 이 지역 공급망이 서로 얽혀 있어 가격과 제품의 가용성에 영향을 미치는 경쟁력학이 발생하고 있다는 것입니다. 또한 멕시코에서는 식품 가공 부문이 급성장하고 있으며, 특히 전통적인 식품에 감염의 선택을 요구하는 건강 지향 소비자 수요가 높아지고 있습니다.

유럽은 클린 라벨 및 천연 성분의 동향의 최전선에 있으며 구연산칼륨은 합성 첨가물을 대체하는 천연 성분으로 인기를 끌고 있습니다. 천연 보존료를 중시하는 EU의 규제 자세는 특히 유기농 식품과 고급 식품 분야에서 구연산칼륨 시장 가치를 높이고 있습니다. 또한 유럽의 정교한 화장품 산업은 지속가능성에 중점을 두고, 퍼스널케어 제품에서 EDTA의 대안으로 구연산칼륨을 채택하는 경향을 강화하고 있습니다.

The global potassium citrate market stands at USD 773.65 million in 2025 and is projected to reach USD 911.33 million by 2030, expanding at a CAGR of 3.33% during the forecast period.

This moderate yet consistent growth trajectory reflects the compound's entrenched position across multiple high-value applications, from sodium reduction initiatives in processed foods to specialized pharmaceutical formulations for renal health management. The market's resilience stems from potassium citrate's unique dual functionality as both a food additive and active pharmaceutical ingredient, positioning it at the intersection of two robust end-use sectors that continue to prioritize health-conscious formulations. Regulatory momentum significantly amplifies market dynamics, particularly through the FDA's Phase II sodium reduction guidance issued in August 2024, which targets average sodium intake reduction to 2,750 mg per day. This initiative directly benefits potassium citrate manufacturers, as food processors increasingly substitute sodium-based additives with potassium alternatives to meet regulatory targets while maintaining product functionality. Simultaneously, the beverage sector's growing emphasis on pH control agents for product stability and taste enhancement creates additional demand vectors, particularly in functional and sports drink categories where electrolyte balance remains paramount.

Global efforts to reduce sodium in food systems are propelling the growth of the potassium citrate market. With regulatory bodies advocating for reduced sodium consumption, potassium citrate stands out as a viable substitute. Being sodium-free, it can replace conventional sodium-based additives, preserving crucial functions like buffering, emulsification, and mineral fortification. This is especially vital in processed foods, where sodium salts have long been essential. Data from the Centers for Disease Control and Prevention (January 2024) highlights the issue: Americans average 3,400 milligrams of sodium daily, well above the federal recommendation of 2,300 milligrams for teens and adults. This overconsumption is linked to serious health concerns. From August 2021 to August 2023, adult hypertension in the U.S. hit 47.7%, with men at 50.8% and women at 44.6%, and rates climbing with age . The regulatory landscape is shifting, with a clear push for sodium-reduction measures in the industry, aiming for compliance by 2026. This urgency boosts the demand for potassium citrate as a reliable sodium alternative. Potassium citrate can be easily incorporated into current food formulations, sparing manufacturers from intricate adjustments. This ensures product quality and shelf stability while adhering to health standards. Heightened consumer health awareness, solid epidemiological links between sodium and cardiovascular risks, and tightening regulatory sodium limits fuel the growing adoption of potassium citrate in various food applications.

Driven by evolving consumer preferences for clean-label and health-centric formulations, the food and beverage industry is undergoing a significant transformation, with notable repercussions for the potassium citrate market. While potassium citrate is industrially synthesized, it enjoys a favorable consumer perception, largely due to its association with naturally occurring citric acid. In-depth consumer studies reveal a growing inclination towards ingredients perceived as natural or those that offer pronounced nutritional advantages. This trend is particularly evident in the European natural food additives market, where regulatory frameworks are increasingly endorsing ingredients sourced from natural origins or processes . Manufacturers have adeptly repositioned potassium citrate, emphasizing its ties to traditional food preservation and its role as a potassium source, vital for cardiovascular health and electrolyte balance. Highlighting this trend, the International Food Information Council's 2023 research found that about 26% of U.S. respondents view "natural and low-sodium" as the foremost indicator of healthy food . This underscores a rising consumer demand for straightforward, natural formulations.

Pharmaceutical applications of potassium citrate face increasingly complex regulatory requirements that extend development timelines and increase compliance costs for manufacturers. The FDA's drug master file requirements for pharmaceutical-grade potassium citrate demand extensive documentation of manufacturing processes, impurity profiles, and stability data, creating barriers for smaller suppliers seeking to enter high-value pharmaceutical markets. USP monograph requirements specify stringent purity standards exceeding 99.5% for pharmaceutical applications, necessitating sophisticated manufacturing processes and quality control systems that increase production costs. International harmonization efforts, while beneficial long term, create short-term compliance complexity as manufacturers must navigate varying requirements across major markets. The regulatory landscape becomes particularly challenging for combination products where potassium citrate interacts with other active ingredients, requiring extensive stability and compatibility testing. These compliance requirements favor established pharmaceutical suppliers with existing regulatory infrastructure while creating market entry barriers that limit competitive intensity in premium segments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2024, the high-purity potassium citrate segment, boasting purity levels more than 99%, commanded a dominant 42.44% market share. This trend highlights a growing appetite for ultra-refined formulations, particularly in premium pharmaceuticals and niche food applications. Stringent regulatory standards and the paramount importance of formulation precision primarily drive the surge in demand. In sectors like pharmaceuticals, where even minute impurities can jeopardize safety or therapeutic outcomes, this emphasis on purity is critical. Potassium citrate, in these settings, plays dual roles: as an active ingredient and a buffering agent, notably in renal health treatments and extended-release drugs. The segment's dominance underscores the industry's unwavering commitment to purity and stringent quality benchmarks. Meanwhile, the 98-99% purity tier finds its niche in food processing and select industrial applications, where functional performance is key, but ultra-high purity isn't a prerequisite.

Meanwhile, the segment with purity levels below 98% is witnessing the most rapid expansion, boasting a notable CAGR of 4.64%. Its growth trajectory is fueled by its attractiveness in high-volume applications that prioritize cost-effectiveness and consistent operations over absolute purity. Key drivers include its burgeoning use in animal nutrition, bulk food production, and pH regulation across diverse sectors. In response, manufacturers are pivoting, rolling out more budget-friendly potassium citrate formulations that fulfill essential functional needs, sidestepping the premium of ultra-refinement. This divergence in purity preferences paints a picture of a maturing market landscape. Potassium citrate has evolved from a generic commodity to a tailored solution, catering to varied end-user demands. Such an evolution not only sparks innovation but also enhances supply chain adaptability and competitive edge, spanning both premium and budget-conscious market segments.

The Potassium Citrate Market is Segmented by Purity (Less Than 98%, 98 - 99%, and More Than 99%), by Application (Food and Beverage, Industrial, Dietary Supplement, Personal Care and Cosmetics, and Others), and by Geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

In 2024, Asia-Pacific not only emerged as the largest regional market, holding a 31.32% share, but also showcased its rapid growth, boasting a 5.44% CAGR projected through 2030. This growth is largely attributed to the region's expanding food processing infrastructure and a heightened health consciousness among its urban populace. Ongoing trade investigations and antidumping reviews underscore China's leading role in citrate production. In India, the burgeoning pharmaceutical sector fuels the demand for high-purity potassium citrate, essential for generic drug manufacturing. Simultaneously, India's expanding processed food industry presents significant volume opportunities for food-grade applications. Meanwhile, Japan and Australia are driving regional growth by focusing on premium applications in functional foods and dietary supplements, with consumers willing to pay a premium for perceived health benefits.

North America, while mature, is undergoing an evolution, largely driven by regulatory initiatives reshaping demand. The FDA's guidance on sodium reduction has spurred a consistent demand for potassium citrate as a sodium substitute. Concurrently, North America's advanced pharmaceutical sector ensures a steady appetite for high-purity grades tailored for specialized therapeutic uses. Notably, Canada's involvement in trade investigations, alongside China, underscores the region's intertwined supply chains and the resultant competitive dynamics influencing pricing and product availability. Additionally, Mexico's burgeoning food processing sector amplifies the demand, especially for health-conscious consumers seeking reduced-sodium options in traditional foods.

Europe stands at the forefront of clean-label and natural ingredient trends, with potassium citrate gaining traction as a natural substitute for synthetic additives. The EU's regulatory stance, which leans towards natural preservatives, has elevated potassium citrate's market value, especially in organic and premium food sectors. Furthermore, Europe's sophisticated cosmetic industry is increasingly turning to potassium citrate as a preferred alternative to EDTA in personal care products. With a pronounced emphasis on sustainability,