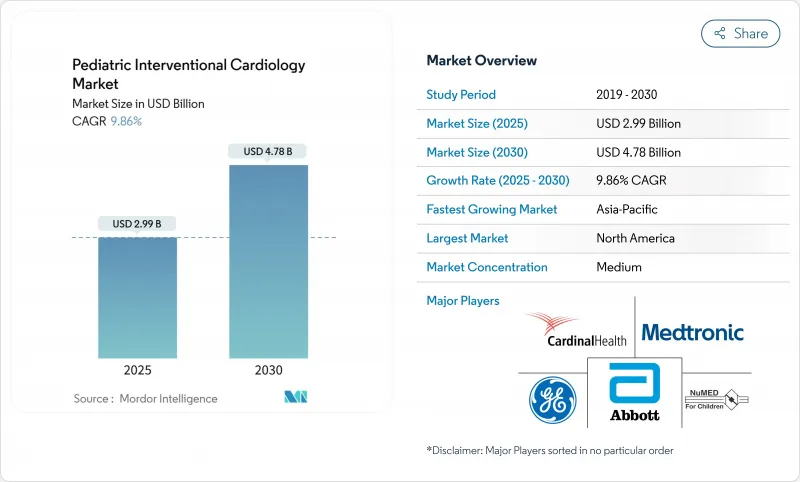

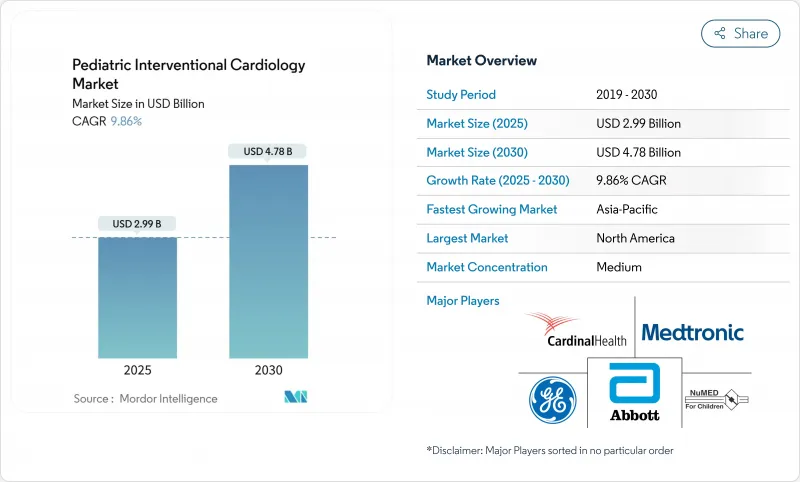

소아 심혈관 중재시술 시장 규모는 2025년에 29억 9,000만 달러, 예측기간(2025-2030년)의 CAGR은 9.86%를 나타내고, 2030년에는 47억 8,000만 달러에 달할 것으로 예측됩니다.

선천성 심장질환(CHD) 관리에서 낮은 침습 기술의 급속한 수용, 꾸준한 규제 당국의 승인, AI 강화 이미징으로의 전환이 성장을 뒷받침하고 있습니다. 북미가 가장 규모가 큰 지역 기반이 되는 것은 아니지만, 병원이 하이브리드형 카테라보 스위트를 취득하고 현지 제조업체가 저가의 소아용 기기를 도입함에 따라 아시아태평양이 가장 급속히 확대되고 있습니다. 임상 수요는 미국의 새로운 보험 데이터 세트에서 전체 출생의 1.95%로 추정되는 CHD 유병률 증가와 단발적인 수술에서 평생 카테터를 이용한 치료 모델로의 지속적인 전환으로 강화되고 있습니다. FDA가 승인한 Minima 스텐트 시스템과 같은 획기적인 제품은 어린이와 함께 확장되도록 설계되었으며 크기에 적합한 임플란트의 새로운 시대를 말합니다. 류마티스성 심장병을 90%의 정밀도로 검출하는 AI 탑재의 카테라보 소프트웨어는 수술의 신뢰성을 더욱 높입니다.

신생아 스크리닝 및 보험 데이터베이스에 따르면, CHD의 유병률은 소아 인구의 2%에 육박하는 기세이며, 과거 추정치보다 훨씬 높습니다. 출생전심 에코검사와 이중지표맥파 옥시메트리 프로그램의 강화에 의해 조기 발견의 감도는 상하이 시범 사업에서 조기 발견 민감도가 100%까지 향상되었습니다. 조기 진단이 생존 기간을 연장하고 평생에 걸쳐 카테터를 이용한 개입을 필요로하는 청년과 성인의 대규모 코호트를 만들어 내고 있습니다.

메드트로닉의 4.7 프랑스 옴니아 보안 ICD 리드는 시험에서 100% 제세동 성공률을 보였습니다. 풍선 확장 가능한 Minima 스텐트는 혈관 성장에 적응하고 주요 부작용없이 97.6%의 절차 성공을 달성했습니다. 흡수성 금속 스텐트와 RESILIA 조직 밸브는 8년 후에 99.3%의 열화가 없음을 나타내며 재개입 위험을 최소화하기 위한 것입니다. 이러한 기술은 역사적으로 부족했던 소아 크기의 하드웨어를 직접 목표로 합니다.

미국에서는 CHD 치료를 위한 병원 지출이 연간 98억 달러를 초과합니다. CHD를 가진 여성의 임신 비용은 1례당 평균 24,290달러이며, 정상적인 산과 의료에 비해 큰 부담이 되고 있습니다. CMS는 2025년 CT 혈관 조영술을 178.02달러에서 357.13달러로 인상했지만 신흥국의 자기 부담액은 여전히 높아 도입이 늦어지고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

폐쇄 기구는 심방 중격 결손과 심실 중격 결손을 밀봉하는 범용성의 높이로 2024년에는 소아 심혈관 중재시술 시장 점유율의 32.31%를 획득했습니다. 소아 심혈관 중재시술 시장에서 클로저 장치의 사용량은 큰 비율을 차지하고 있으며, 100%의 임플란트 성공률을 기록한 Occlutech Atrial Flow Regulator 등의 제품에 지지되고 있습니다. 풍선 카테터는 좁은 병변을 더 빨리 수축시키면서 횡단하는 1.2mm 프로파일로 진화를 계속하고 차세대 아테렉토미 도구는 혈관 외상을 최소화하면서 칼슘을 제거합니다.

경 카테터 심장 판막은 CAGR 13.89%에서 가장 빠르게 성장하는 분야입니다. Edwards사의 EVOQUE 삼첨판과 Abbott사의 Tendyne 시스템 등의 기기는 흉골절개 없이 역류나 석회화에 대응할 수 있게 되어 밸브 솔루션의 소아 심혈관 중재시술 시장 규모를 2자리 확대했습니다. 흡수성 금속 스텐트는 소아가 성장함에 따라 미래의 재개입을 피하기 위한 것이며, AI와 MRI 지침을 통합한 영상 진단 장치는 대상 사례의 방사선 노출을 0으로 삼고 있습니다. 이러한 진보가 함께 새로운 병원과 외래 센터가 복잡한 구조 심장 프로그램에 진출하고 있습니다.

북미는 2024년 매출액의 41.91%를 차지했으며, 소아용 기기 허가에서 FDA의 리더십, 성숙한 상환, 선천성 프로그램에 대한 자금 사업 자금에 힘을 쏟았습니다. 이 지역의 소아 인터벤션 심장 병학 시장 규모는 민간 보험 회사가 AI 유도 절차를 수락하고 Breakhrough Device Designation과 같은 규제 패스웨이가 승인 기간을 단축함에 따라 꾸준히 확대되고 있습니다. 캐나다는 복잡한 신생아를 3차 의료시설로 유도하는 소개 네트워크를 통해 미국의 능력을 보완하고, 멕시코는 낮은 수술 관세로 국경을 넘은 환자를 끌어들이고 있습니다.

유럽은 독일, 프랑스, 영국에서 일관된 공공 건강 관리와 집중된 외과적 전문 지식으로 인해 큰 점유율을 차지합니다. 소형 심장 판막의 조기 도입과 신생아의 펄스 옥시메트리 스크리닝 루틴은 EU 회원국의 소아 심혈관 중재시술 시장을 뒷받침하고 있습니다. 공동 임상 등록은 실제 세계의 데이터 작성을 가속화하고 제조업체가 시판 후 허가를 확보하는 데 도움이 됩니다.

아시아태평양은 CAGR 12.53%에서 가장 빠르게 성장하고 있습니다. 중국 신생아 스크리닝 프로그램은 중요한 CHD의 100% 감도를 달성하고 수술 건수를 증가시킨 반면, 일본은 경 카테터 폐동맥 판막 치환술로 선도하고 있습니다. 인도의 심장센터는 비용제약에 직면하면서도 저가격의 폐쇄기구의 국내 생산에 힘입어 소아 카테터 검사 사례를 연간 2배로 늘리고 있습니다. 인도네시아, 베트남, 태국에서는 정부 보험의 확대가 절차 수요를 끌어내고 있습니다.

중동 및 아프리카와 남미는 후진을 숭배하고 있지만 기세를 보이고 있습니다. 걸프 국가는 전문 병원에 엄청난 투자를 하고 있으며 남아프리카의 소아 심장 전문 유닛은 지역 소개의 허브 역할을 합니다. 브라질과 아르헨티나에서는 관민보험 모델 하에서 소아 카테터 검사실에의 접근을 확대하고 있지만, 환율 변동이 당면의 규모 확대를 억제하고 있습니다. 신흥 지역 전반에 있어서, 휴대형 심 에코 검사와 원격 상담 플랫폼이, 원격지의 진료소까지 전문의의 전문지식을 넓히고 있습니다.

The Pediatric Interventional Cardiology Market size is estimated at USD 2.99 billion in 2025, and is expected to reach USD 4.78 billion by 2030, at a CAGR of 9.86% during the forecast period (2025-2030).

Rapid acceptance of minimally invasive techniques for congenital heart defect (CHD) management, steady regulatory approvals, and the shift toward AI-enhanced imaging are propelling growth. North America remains the largest regional base, yet Asia-Pacific is expanding fastest as hospitals acquire hybrid cath-lab suites and local manufacturers introduce lower-cost pediatric devices. Clinical demand is reinforced by rising CHD prevalence estimated at 1.95% of all births in new U.S. insurance datasets and by a continuing move from episodic surgery to lifelong catheter-based care models. Breakthrough products such as the FDA-cleared Minima Stent System, designed to expand with the child, signal a new era of size-appropriate implants. AI-powered cath-lab software that detects rheumatic heart disease with 90% accuracy further boosts procedural confidence.

Newborn screening and insurance databases show CHD prevalence nearing 2% of pediatric populations, far higher than historic estimates. Enhanced prenatal echocardiography and dual-index pulse-oximetry programs have lifted early-detection sensitivity to 100% in Shanghai pilots. Earlier diagnosis extends survival, creating larger cohorts of adolescents and adults who continue to require catheter-based interventions across their lifespans.

Advances in materials and engineering have cut device diameters to as little as 1.6 mm, exemplified by Medtronic's 4.7 French OmniaSecure ICD lead, which demonstrated 100% defibrillation success in trials. The balloon-expandable Minima Stent adapts to vessel growth, achieving 97.6% procedural success without major adverse events. Absorbable metal stents and RESILIA tissue valves, which showed 99.3% freedom from deterioration at eight years, aim to minimize re-intervention risk. Such technology directly targets historic shortages of child-sized hardware.

Hospital expenditures for CHD care surpass USD 9.8 billion annually in the United States. Pregnancy costs for women with CHD average USD 24,290 per case, a material burden versus routine obstetrics. Although CMS boosted 2025 CT angiography payments from USD 178.02 to USD 357.13, out-of-pocket exposure in emerging economies remains high, slowing adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Closure devices captured 32.31% of pediatric interventional cardiology market share in 2024 thanks to their versatility in sealing atrial and ventricular septal defects. Their usage underpins a sizeable slice of pediatric interventional cardiology market volume, buoyed by products such as the Occlutech Atrial Flow Regulator, which posted 100% implant success. Balloon catheters keep evolving toward 1.2 mm profiles that cross tight lesions with faster deflation, while next-generation atherectomy tools remove calcium with minimal vessel trauma.

Transcatheter heart valves represent the fastest-growing segment, climbing at a 13.89% CAGR. Devices including Edwards' EVOQUE tricuspid valve and Abbott's Tendyne system now address regurgitation and calcification without sternotomy, expanding the pediatric interventional cardiology market size for valve solutions by double digits. Absorbable metal stents aim to obviate future re-interventions as children grow, and imaging consoles integrating AI and MRI guidance are cutting radiation exposure to zero for eligible cases. Collectively, these advances draw new hospitals and ambulatory centers into complex structural heart programs.

The Pediatric Interventional Cardiology Market Report Segments the Industry Into Device Type (Closure Devices, and More), Procedure (Catheter-Based Valve Implantation, Congenital Heart Defect Correction, and More), End User (Children's Hospitals & Specialty Centres, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 41.91% of 2024 revenue, propelled by FDA leadership in clearing pediatric devices, mature reimbursement, and substantial philanthropic funding for congenital programs. The pediatric interventional cardiology market size in the region expands steadily as private insurers accept AI-guided procedures and as regulatory pathways such as Breakthrough Device Designation trim approval times. Canada complements U.S. capacity through referral networks that funnel complex neonates to tertiary centers, while Mexico draws cross-border patients with lower procedural tariffs.

Europe commands a sizeable share due to cohesive public healthcare and concentrated surgical expertise in Germany, France, and the United Kingdom. Early adoption of miniaturized heart valves and routine newborn pulse-oximetry screening boost the pediatric interventional cardiology market across EU member states. Joint clinical registries accelerate real-world data generation, helping manufacturers secure post-market authorizations.

Asia-Pacific is the fastest grower at 12.53% CAGR. China's newborn screening programs have achieved 100% sensitivity for critical CHDs and lifted operative volumes, while Japan leads in transcatheter pulmonary valve replacements. Indian cardiac centers face cost constraints yet double pediatric cath-lab cases annually, supported by domestic production of lower-price closure devices. Government insurance expansions in Indonesia, Vietnam, and Thailand are unlocking procedure demand.

Middle East & Africa and South America trail but show momentum. Gulf nations invest heavily in specialty hospitals, and South Africa's dedicated pediatric cardiac units serve as regional referral hubs. Brazil and Argentina widen pediatric cath-lab access under public-private insurance models, though currency volatility tempers immediate scale. Across emerging regions, portable echocardiography and tele-consult platforms extend specialist expertise to remote clinics.