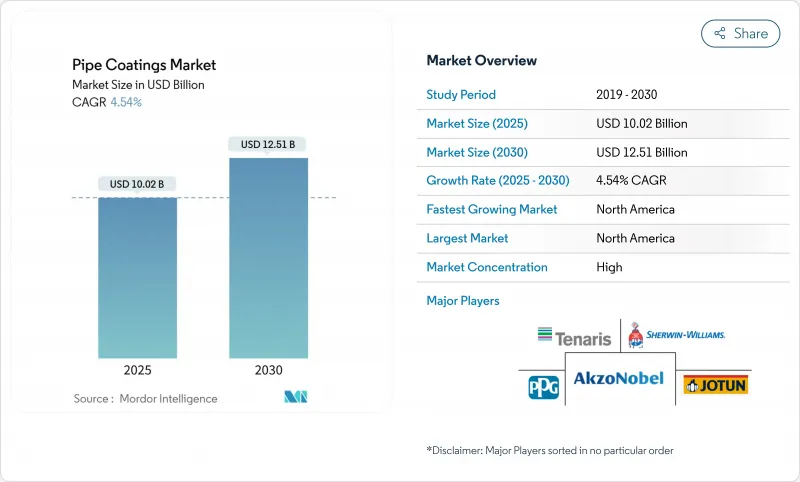

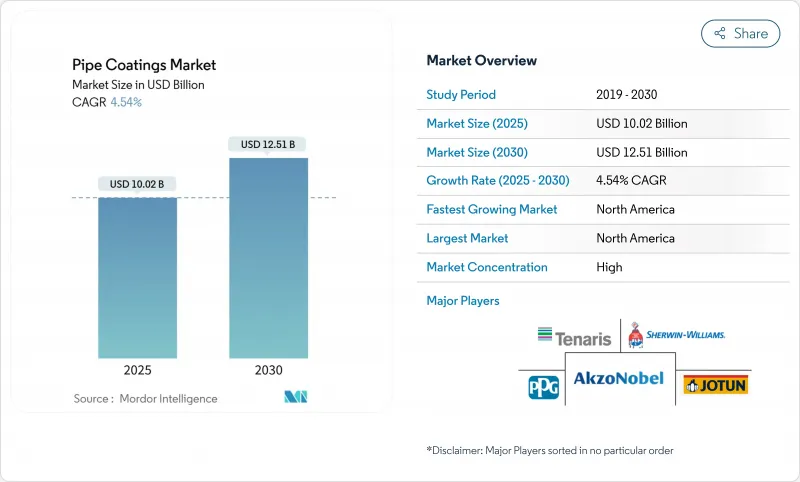

세계의 파이프 코팅 시장 규모는 2025년 100억 2,000만 달러로 추정되고, 2030년까지 125억 1,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 4.54%로 확대될 것으로 보입니다.

신규 파이프라인에 대한 투자 증가, 꾸준한 자산 유지보수 일정, 안전규칙의 엄격화로 석유, 가스, 물, 산업 분야에서 보호 마감제 수요가 유지되고 있습니다. 북미의 셰일 조성과 유럽의 LNG 및 수소 계획에 의해 능력 증강은 견조하게 추이해, 아시아태평양의 도시 확대가 장기적인 구조 성장을 견인합니다. 2액형 폴리우레탄 스프레이 시스템, 그래핀 강화 수성 옵션, 저온 경화 파우더 등 기술의 진보로 용도가 확대되고 라이프사이클 비용이 저하되고 있습니다. 지속가능성의 압력은 조달팀을 수계 및 분말 솔루션으로 향하게 하지만, 입증된 성능이 가장 중요한 가혹한 환경에서는 용매계가 발판을 유지하고 있습니다. 경쟁 심화의 핵심은 고성능 화학물질이며 세계 공급업체는 해외, 고압 및 수소 서비스 주문을 보장하기 위해 전문 라인을 확장하고 있습니다.

북미 사업자들은 신규 파이프라인과 레거시 파이프라인의 건설을 급격히 진행하고 있으며, 황화수소, 이산화탄소, 미생물의 공격을 견디는 견고한 코팅에 대한 수요가 높아지고 있습니다. 아르헨티나의 Vaca Muerta 유전의 생산 능력은 Oleoductos del Valle의 확장에 의해 2025년에는 2배인 54만 B/D가 될 것으로 예상되고 있으며, 그에 필적하는 유지보수의 기간은 단축되어 재코팅의 간격은 좁아지고 있습니다. 포뮬레이터는 두꺼운 에폭시 층과 내마모성 우레탄 오버코트로 대응하여 현장에서 원 패스 도포가 가능하므로 오퍼레이터 다운타임이 단축됩니다.

부식 비용은 자기 수복성, 피막 하 부식 내성, 검사 사이클의 연장을 갖춘 라이닝의 채용을 자산 소유자에게 압박하고 있습니다. 에폭시 씰 코트와 결합된 이액형 폴리우레탄 시스템은 강력한 접착력과 불침투성 표면을 보여주며 좁은 공간에서 신속한 스팟 수리를 가능하게 합니다. 한번의 고장이 안전성과 생산 업타임을 위태롭게 하는 해양 라인에서는 융착 에폭시, 내마모성 오버코트, 외측의 폴리에틸렌 랩을 조합한 다층 구조가 지정되게 되어 있습니다.

수심 3,000m로 도포되는 코팅은 정수압과 온도차를 견디기 때문에 기존 사양에서는 대응할 수 없습니다. 파이프라인 및 위험물 안전관리국의 지원에 의한 조사에서는 해저 설치시의 충격 손상을 완화하기 위해, 희생 복합층과 조합한 두꺼운 폴리머 랩을 검토하고 있습니다. 또한 접근상의 제약도 검사를 복잡하게 하고, 처음으로 코팅의 무결성을 확인할 때의 난이도를 높이고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

에폭시 및 폴리우레탄 제품은 2024년 파이프 코팅 시장 규모의 40.76%를 차지했고, 2030년까지 CAGR은 4.91%로 전체 시장을 상회할 것으로 예측됩니다. 에폭시 수지는 그릿 블래스트 처리된 강철에 대한 접착성이 입증되었으며, 폴리우레탄의 탑 코트는 내마모성과 자외선 안정성을 제공합니다. 현장 작업자에게는 750 미크론의 도막을 원패스로 형성할 수 있는 듀얼 컴포넌트 스프레이 리그가 선호되고 있어 라이브 라인의 턴어라운드 타임을 단축하고 있습니다.

폴리에틸렌과 폴리프로필렌은 수분 확산이 적고 기계적 유연성으로 인해 송수 및 지역 난방 분야에서 인기를 얻고 있습니다. 그 주변에서는 시멘트계 랩이나 아스팔트 에나멜이 견고한 기계적 보호에 도움이 되고 있지만, 환경상의 제약이 한층 더 보급을 억제하고 있습니다. 융착 에폭시와 내마모성 오버레이를 결합한 가교 다층 솔루션은 현재 방향 드릴 섹션과 같은 충격이 큰 영역을 보호하고 있으며, 하이브리드 시스템이 성능의 기준선을 계속 향상시키고 있음을 보여줍니다.

2024년 파이프 코팅 시장 점유율에서는 외부 마감이 78.19%를 차지했으며, 이는 사업자가 매설 강재를 토양 유래의 염화물 공격이나 미주 전류로부터 보호하는 것을 우선했기 때문입니다. 이 카테고리는 북미와 유럽의 파이프라인 그리드의 노후화에 따라 2030년까지 연평균 복합 성장률(CAGR) 5.18%를 보일 것으로 예측되고 있습니다. 에폭시 수지의 프라이머와 접착 타이를 포함한 3층 폴리에틸렌 랩은 습윤 매립 조건 하에서 접착성과 기계적 강인성을 겸비하기 때문에 여전히 주류입니다.

내부 라이닝은 수익 풀이 작은 것, 유량 효율과 H2S에 의한 공식의 완화가 자본 지출을 정당화하는 경우 예산을 획득하고 있습니다. 저전단 에폭시 라이닝은 유효 처리 능력을 높이고 펌프의 에너지 절약을 가능하게 하여 수년 이내에 설치 비용을 상쇄할 수 있습니다. 향후 성장은 정유소의 디보틀 네킹과 마찰 손실을 정량화하는 스마트 피깅 데이터에 달려 있으며, 사워 서비스의 수집 라인 외에도 내부 코팅 프로그램을 확대하도록 소유자를 설득할 예정입니다.

북미는 2024년 매출의 31.54%를 차지하고 2030년까지 연평균 복합 성장률(CAGR)은 가장 빠른 5.31%가 될 것으로 예측됩니다. 이 지역은 셰일 가스 생산량 증가, 장거리 가스 통로 확장, 2025년 누설 감지 규칙 등 안전 규제 강화로 이익을 얻고 있습니다. 파이프라인 소유자는 원격지에서 미래의 굴착 작업을 최소화하는 고경도 우레탄 탑 코트와 자가 복구 에폭시에 더 큰 예산을 할당합니다.

아시아태평양의 성장을 이끌고 있는 것은 중국, 인도, 인도네시아로, 수도, 에너지, 화학용 파이프라인이 증가하고 있습니다. 코팅 공급자는 우기의 습기 속에서 확실히 경화하고 열대균류에 저항하는 시스템을 설계해야 합니다. 현지 분체 제조업체는 중국의 5개년 계획 하에서의 메가 인프라 계획에 대응하기 위해, 선취 창고의 주문에 응할 수 있도록 생산 능력을 증강하고 있습니다.

유럽에서는 새로운 LNG 및 가스 수입 파이프가 여전히 발전하고 있는 반면, 수소 파일럿 통로에서는 새로운 내침투성 층이 요구되고 있습니다. 코팅 제형 제조업체는 테스트 랩과 제휴하여 수십분 동안 수소 분자를 100bar의 압력으로 가두는 폴리머-금속 복합 장벽을 검증합니다.

The Pipe Coatings Market size is estimated at USD 10.02 billion in 2025, and is expected to reach USD 12.51 billion by 2030, at a CAGR of 4.54% during the forecast period (2025-2030).

Mounting investment in new pipelines, a steady asset maintenance schedule, and stricter safety rules sustain demand for protective finishes across oil and gas, water, and industrial segments. North America's shale build-out and Europe's LNG and hydrogen plans keep capacity additions steady, while Asia-Pacific's urban expansion drives long-term structural growth. Technology advances, such as dual-component polyurethane spray systems, graphene-enhanced water-based options, and low-temperature cure powders, are widening application windows and lowering life-cycle costs. Sustainability pressures steer procurement teams toward waterborne and powder solutions, yet solvent systems retain a foothold in harsher environments where proven performance records matter most. Competitive intensity centers on high-performance chemistries, with global suppliers scaling specialized lines to secure offshore, high-pressure, and hydrogen service orders.

North American operators are fast-tracking new and legacy pipelines, lifting demand for robust coatings that tolerate hydrogen sulfide, carbon dioxide, and microbial attack. With capacity in Argentina's Vaca Muerta field set to double to 540,000 bpd in 2025 because of Oleoductos del Valle's expansion, comparable maintenance windows are shortening, and re-coating intervals are tightening. Formulators respond with thicker epoxy layers and abrasion-resistant urethane overcoats that can be field-applied in a single pass, reducing downtime for operators.

Corrosion costs have put pressure on asset owners to adopt linings that self-heal, resist under-film corrosion, and extend inspection cycles. Dual-component polyurethane systems paired with epoxy seal coats show strong adhesion and an impermeable surface, enabling quick spot repairs in confined spaces. Offshore lines, where a single failure jeopardizes safety and production uptime, are now specified with multi-layer builds that combine fusion-bonded epoxy, abrasion-resistant overcoats, and outer polyethylene wraps.

Coatings applied at 3,000 m water depth endure hydrostatic pressures and temperature differentials that stretch legacy specifications. Research backed by the Pipeline and Hazardous Materials Safety Administration is examining thick polymer wraps combined with sacrificial composite layers to mitigate impact damage during seabed installation. Access constraints also complicate inspection, raising the stakes for first-time coating integrity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Epoxy and polyurethane products accounted for 40.76% of the pipe coatings market size in 2024 and are forecast to outpace the aggregate market at a 4.91% CAGR through 2030. Epoxies deliver proven adhesion over grit-blasted steel, while polyurethane top coats bring abrasion resistance and UV stability. Field crews favor dual-component spray rigs that can lay down a 750-micron build in one pass, shrinking turnaround time on live lines.

Polyethylene and polypropylene maintain traction in water transmission and district heating because of their low moisture diffusion and mechanical flexibility. At the fringes, cementitious wraps and asphalt enamel serve heavy-duty mechanical protection, yet environmental constraints are curbing further uptake. Cross-linked multilayer solutions that combine fusion-bonded epoxy with abrasion-resistant overlays now protect high-impact areas such as directional drill sections, demonstrating how hybrid systems continue to elevate performance baselines.

External finishes represented 78.19% of the pipe coatings market share in 2024 as operators prioritized safeguarding buried steel from soil-borne chloride attack and stray current. The category is predicted to post a 5.18% CAGR until 2030 as pipeline grids age in North America and Europe. Three-layer polyethylene wraps incorporating epoxy primers and adhesive ties remain a mainstay because they couple adhesion with mechanical toughness under wet backfill conditions.

Internal linings, although accounting for a smaller revenue pool, are winning budgets where flow efficiency and mitigation of H2S-induced pitting justify capital outlays. Low-shear epoxy linings can raise effective throughput or enable pump energy savings that offset installation expense within a few years. Future growth hinges on refinery debottlenecking and smart pigging data that quantify friction losses, convincing owners to extend internal coating programs beyond sour-service gathering lines.

The Pipe Coatings Market Report Segments the Industry by Material Type (Polyethylene and Polypropylene, Epoxy and Polyurethane, and More), Surface Location (External Pipe Coatings and Internal Pipe Coatings), Formulation (Powder, and More), End-User Industry (Oil and Gas, Water and Wastewater Treatment, Mining, Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

North America contributed 31.54% of 2024 revenue and is expected to post the fastest 5.31% CAGR through 2030. The region benefits from shale output growth, long-haul gas corridor expansions, and reinforced safety regulations such as the 2025 leak detection rule. Pipeline owners are allocating larger budgets to high-build urethane topcoats and self-healing epoxies that minimize future dig-ups in remote terrain.

Asia-Pacific's growth is driven by China, India, and Indonesia, adding pipelines for water, energy, and chemicals. Coating suppliers must engineer systems that cure reliably in monsoon humidity and resist tropical fungi. Local powder producers are installing extra capacity to satisfy build-ahead warehousing orders for mega-infrastructure plans under China's Five-Year Program.

Europe presents a two-speed pattern: new LNG and gas import pipes still move forward, while hydrogen pilot corridors demand novel permeation-resistant layers. Coating formulators are partnering with test labs to validate polymer-metal composite barriers capable of confining hydrogen molecules at 100 bar pressure for decades.