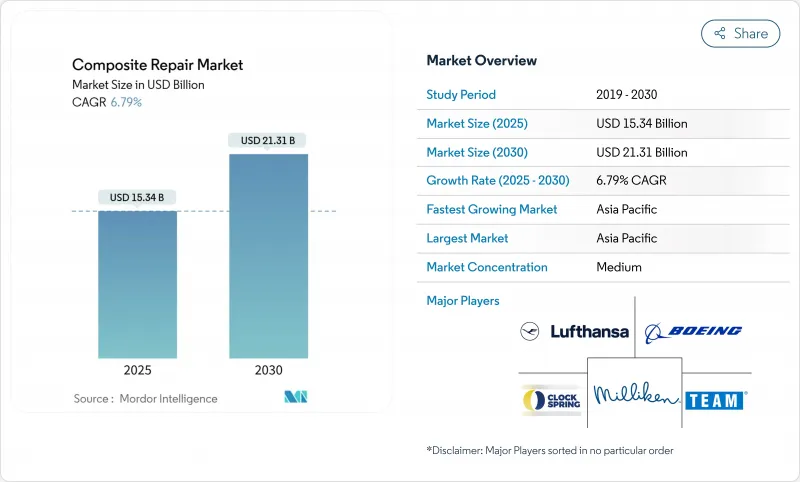

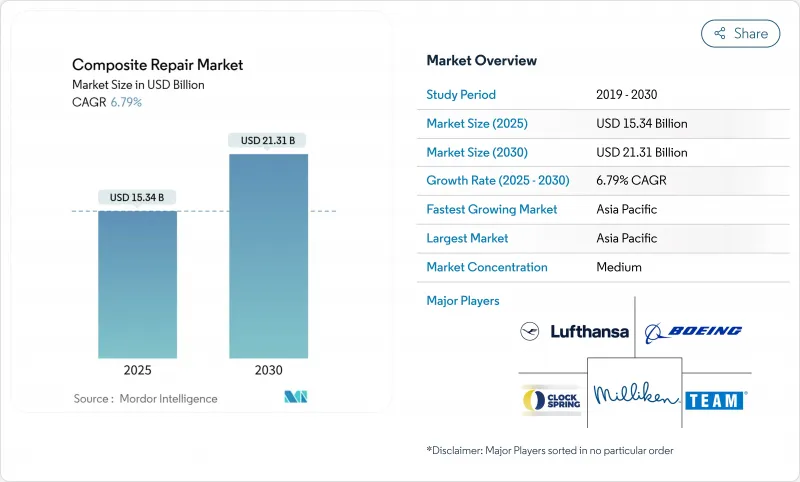

세계의 복합재 수리 시장은 2025년 153억 4,000만 달러에 이르고, 2030년에는 213억 1,000만 달러로 성장할 것으로 예측되며, 기간 중 CAGR은 6.79%로 예상됩니다.

자산 소유자가 비용이 많이 드는 교환으로 인해 다운타임을 억제하면서 구조적 성능을 회복하는 효율적인 복합재 수리로 중심을 옮기기 때문에 성장이 계속되고 있습니다. 구조 수리는 깊은 인증의 전문지식에 뒷받침되는 앵커 부문인 것에 변함이 없지만, 풍력, 해양, 수송의 각 자산에서 예방보수가 지지됨에 따라 외관보수가 가장 급속히 진전하고 있습니다. 항공우주가 가장 큰 최종 사용자 점유율을 유지하는 한편, 해상 풍력은 육상으로 이동할 수 없는 블레이드의 현장 작업에 대한 수요를 증가시키고 있습니다. 디지털 트윈 통합, 자동화, ASME PCC-2 및 ISO 24817과 같은 표준은 품질을 확보하고, 위험을 억제하며, 중요한 인프라에서 채택 확대를 지원합니다.

사업자는 파이프라인, 항공기 및 산업 플랜트를 교체하는 대신 연장되어 있으며 복합 랩은 자산을 중단하지 않고 이 전략을 수행하는 데 도움이 됩니다. TD Williamson은 2024년 12월 Petro-Line을 인수하여 PETROSLEEVE 기술을 포트폴리오에 추가하여 북미의 무결성 의무에 맞는 라이브 파이프라인 보강을 가능하게 했습니다. HJ3는 탄소섬유 랩을 사용하여 고속도로의 다리 기둥을 교체 비용의 절반으로 복구하고 공공 인프라에 경제적인 이점을 보여주었습니다. 해상 풍력 발전의 블레이드 교환에는 1기당 약 20만 달러가 필요하지만, 복합재에 의한 보수는 평균 3만 달러이며, 소유자에게 있어서 수명 연장은 설득력이 있는 것이 되고 있습니다.

복합재 중첩은 용접 기반 금속 수리와 비교하여 열간 가공 허가를 피하고 보험료를 줄이고 작업 수를 줄입니다. ASME PCC-2 가이던스에서는 복합재는 열간 작업의 70-80%를 배제할 수 있어 안전성과 생산성을 대폭 개선할 수 있다고 지적하고 있습니다. 호주 해군은 프리게이트함의 갑판용 탄소섬유 오버레이의 내구성이 15년이라고 보고하고 있으며, 해상에서의 장기간의 내구성을 증명하고 있습니다. Seaka의 2024년 매출은 117억 6,000만 스위스 프랑을 기록했으며, 그 원인은 다운타임을 최소화하고 자산의 수명을 연장하는 인프라 보수용 수지였습니다. 예산에 제약이 있는 소유자가 복합재를 선택하기 때문에 이러한 경제성이 성장에 1.5포인트 기여합니다.

학술적인 돌파구는 미래의 수리 수요를 줄일 수 있는 미세 균열을 자율적으로 막는 복합재를 보여줍니다. 와세다 대학은 2025년 4월 1.50GPa의 경도를 유지하면서 가열 후 치유하는 실록산 필름을 발표했습니다. Texas A&M의 Diels-Alder 폴리머는 내탄성과 자기 복구 기능을 결합하여 방위산업에서 관심을 모으고 있습니다. 이러한 개념은 여전히 상업화 전이지만, 애프터마켓 판매량을 줄이고 2029년 이후 CAGR을 0.7포인트 떨어뜨릴 수 있는 미래 시나리오를 보여줍니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

소유자가 항공기, 파이프라인, 풍력 블레이드의 내력 회복을 우선하기 위해 2024년 복합재 수리 시장 점유율은 구조 보수가 44.56%를 차지했습니다. 이 분야는 특히 복합재의 1차 구조가 정밀한 스카프 형상과 통제된 경화 프로파일을 필요로 하는 항공우주 분야에서 정평이 있는 공급자에게 유리한 엄격한 인증 프로토콜로부터 이익을 얻고 있습니다. 사업자는 안전한 서비스 간격을 연장하고 자본 집약적인 교환을 연기하기 위해 이러한 수리를 채택하여 복합재 수리 시장에서 이 분야의 리더십을 강화하고 있습니다.

코스메틱 리페어는 2030년까지 연평균 복합 성장률(CAGR) 7.66%로 성장하여 표면 침식이 확대되기 전에 대처하는 조기 단계 개입으로의 시프트를 반영하고 있습니다. Belzona 코팅과 같은 풍력 터빈의 최첨단 처리는 코스메틱 리페어가 공기 역학 손실을 줄이고 더 큰 구조적 캠페인을 피하는 방법을 보여줍니다. 예지보전 툴이 표면상의 경미한 결함을 일찍 깨닫게 되면서, 코스메틱 카테고리에 수반되는 복합재 수리 시장 규모는 확대되고, 서비스 제공업체는 엄격한 운전 중지 기간에 맞춘, 빠른 경화로 현장 친화적인 시스템의 개발을 장려하게 됩니다.

핸드 레이업 공법은 2024년 복합재 수리 시장 점유율의 38.55%를 차지했으며, 이식성과 최소한의 설비 요구사항이 있었습니다. 현장 팀은 날씨, 모양, 액세스 등의 과제로 자동화된 접근이 불가능한 경우, 핸드 레이업에 의존하는 경우가 많습니다. CompositePatch의 5분 긴급 키트는 신속한 선체 밀폐가 비용이 많이 드는 다운타임을 방지하는 해상 사고의 이점을 보여줍니다.

오토클레이브를 통한 수리는 운영자가 고부하 부품에 항공우주 등급의 품질을 요구하기 때문에 예측 CAGR은 8.03%입니다. 항공사는 엔진 카울과 비행 제어면을 오토클레이브 수리 공장에 의뢰하여 오리지널 제조품과 동등한 품질 수준을 회복시키고 있습니다. 항공기가 성장함에 따라 오토클레이브 서비스의 복합재 수리 시장 규모가 상승할 것으로 보입니다. 진공 주입 및 자동 섬유 배치는 MRO 센터에 로봇을 공급하는 Ingersoll Machine Tools와 같은 장비 제조업체가 박차를 가하고 진보를 계속하고 있습니다.

아시아태평양은 거대한 제조거점, 확장되는 해상 풍력 파이프라인, 야심찬 인프라 업데이트 계획을 통해 최대의 복합재 수리 시장을 독점하고 있습니다. 중국의 풍력 OEM은 15MW급 터빈을 배치하여 현장에서 블레이드 수리 기술 수요를 촉진하고 있습니다. 인도와 동남아시아에서는 도로, 철도, 항만 프로젝트가 전도된 일정에 맞추어 복합 강화를 통합하고 있기 때문에 한 자릿수의 높은 성장을 기록하고 있습니다.

북미는 노후화된 에너지망과 견조한 민간항공기에 지지되고 있습니다. 파이프라인 사업자는 처리 능력을 유지하면서 부식을 줄이기 위해 ASME 표준의 탄소 오버랩을 적용하고 미국의 MRO 기업은 광폭동체 나셀의 오토클레이브 설비에 투자하고 있습니다. 이 지역은 또한 Great Plains의 풍력 발전소에서 블레이드의 예측 수리를 위한 디지털 트윈 배치를 시험적으로 도입하고 있습니다.

유럽은 연구 개발을 촉진하는 국가의 인센티브로 기술 중심주의를 유지하고 있습니다. 독일의 항공우주 클러스터는 열가소성 스카프리스 패칭에 종사하고 덴마크는 블레이드 로봇 공학을 개척하고 있습니다. Lufthansa Technik의 12억 유로 확장은 복합재 MRO의 리더십에 대한 현지 헌신을 강조합니다. 유럽의 복합재 수리 시장의 성장률은 설치 기반이 성숙하고 있지만, 보다 정교한 유지 관리가 요구되기 때문에 한 자리 대 중반에서 안정적입니다. 라틴아메리카, 중동, 아프리카는 성숙한 지역에서 입증된 기술을 채택하면서 국내 기술자 파이프라인을 육성하고 있으며, 전체적으로 소규모이면서 급속히 진보하고 있는 블록을 형성하고 있습니다.

The composite repair market stood at USD 15.34 billion in 2025 and is forecast to rise to USD 21.31 billion by 2030, delivering a 6.79% CAGR.

Growth continues as asset owners pivot from costly replacements to efficient composite repairs that restore structural performance while curbing downtime. Structural repairs remain the anchor segment, supported by deep certification expertise, yet cosmetic repairs are advancing fastest as preventive maintenance gains favor across wind, marine, and transportation assets. Aerospace keeps the largest end-user share, while offshore wind drives incremental demand for in-situ blade work that cannot be moved onshore. Digital twin integration, automation, and standards such as ASME PCC-2 and ISO 24817 ensure quality, contain risk, and underpin expanding adoption across critical infrastructure.

Operators extend pipelines, aircraft, and industrial plants instead of replacing them, and composite wraps help execute this strategy without shutting down assets. T.D. Williamson's purchase of Petro-Line in December 2024 brought PETROSLEEVE technology into its portfolio, enabling live pipeline reinforcement that meets North American integrity mandates . HJ3 restored a highway bridge column at half the replacement cost using carbon-fiber wraps, illustrating the economic benefit for public infrastructure. Offshore wind blade replacements cost about USD 200,000 each, yet composite repairs average USD 30,000, making life-extension compelling for owners.

Composite overwraps avoid hot-work permits, lower insurance premiums, and reduce man-hours versus weld-based metallic repairs. ASME PCC-2 guidance notes that composites can eliminate 70-80% of hot work, materially improving safety and productivity. The Royal Australian Navy reports 15-year durability on carbon-fiber overlays for frigate decks, providing a long proof record at sea. Sika logged CHF 11.76 billion in 2024 sales, partly driven by infrastructure repair resins that extend asset life with minimal downtime. These economics contribute +1.5 points to growth as budget-constrained owners choose composite solutions.

Academic breakthroughs show composites that autonomously close micro-cracks, potentially lowering future repair demand. Waseda University released a siloxane film in April 2025 that heals after heating while retaining 1.50 GPa hardness. Texas A&M's Diels-Alder polymer combines ballistic resistance and self-repair functions, attracting defense interest. These concepts remain pre-commercial yet illustrate a future scenario that could reduce aftermarket volumes, trimming 0.7 points from the CAGR beyond 2029.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Structural repairs accounted for 44.56% of the composite repair market share in 2024 as owners prioritize restoring load-bearing capacity on aircraft, pipelines, and wind blades. The segment benefits from rigorous certification protocols that favor established providers, especially in aerospace where composite primary structures demand precise scarf geometry and controlled cure profiles. Operators adopt these repairs to extend safe service intervals and defer capital-intensive replacements, reinforcing segment leadership inside the composite repair market.

Cosmetic repairs are rising at a 7.66% CAGR to 2030, reflecting the shift to early-stage interventions that address surface erosion before it propagates. Wind turbine leading-edge treatments, such as Belzona coatings, exemplify how cosmetic activities cut aerodynamic losses and avoid larger structural campaigns. As predictive maintenance tools flag minor surface defects earlier, the composite repair market size attached to the cosmetic category will expand, encouraging service providers to develop fast-cure, field-friendly systems that align with tight outage windows.

The hand lay-up method held 38.55% of composite repair market share in 2024 because of its portability and minimal equipment requirement. Field teams often rely on hand lay-up when weather, geometry, or access challenges rule out automated approaches. CompositePatch's five-minute emergency kits illustrate the advantage in maritime incidents where rapid hull sealing prevents costly downtime.

Autoclave repairs exhibit an 8.03% forecast CAGR as operators insist on aerospace-grade quality for highly loaded components. Airlines route engine cowls and flight-control surfaces to autoclave shops to regain qualification levels equal to original builds. As fleets grow, the composite repair market size for autoclave services will climb because airlines favor centralized, repeatable quality over field expediency. Vacuum infusion and automated fiber placement continue to advance, spurred by equipment manufacturers such as Ingersoll Machine Tools that supply robotics to MRO centers.

The Composite Repair Market Report Segments the Industry by Product Type (Structural, Semi-Structural, and More), Repair Process (Hand Lay-Up, Vacuum Infusion, and More), Material Type (Carbon-Fibre Reinforced Polymer (CFRP), Aramid-Fibre Composites, and More), End-User Industry (Automotive, Wind Energy, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commands the largest composite repair market because of its immense manufacturing base, expanding offshore wind pipelines, and ambitious infrastructure renewal plans. China's wind OEMs deploy fleets of 15-MW class turbines, fueling demand for in-situ blade servicing technologies. India and Southeast Asia register high single-digit growth as road, rail, and port projects integrate composite strengthening to meet accelerated timelines.

North America follows, underpinned by an aging energy network and a robust commercial aviation fleet. Pipeline operators apply ASME-qualified carbon overwraps to mitigate corrosion while maintaining throughput, and MRO houses in the United States invest in autoclave capacity for wide-body nacelles. The region also pilots digital twin deployments for predictive blade repairs on Great Plains wind farms.

Europe remains technology-centric with state incentives that drive R&D. Germany's aerospace cluster works on thermoplastic scarf-less patching, and Denmark pioneers blade robotics. Lufthansa Technik's EUR 1.2 billion expansion underscores local commitment to composite MRO leadership. Composite repair market size growth in Europe stabilizes at mid-single digits as the installed base matures but demands more sophisticated upkeep. Latin America, the Middle East, and Africa collectively form a smaller yet rapidly advancing bloc, adopting proven techniques from mature regions while cultivating domestic technician pipelines.