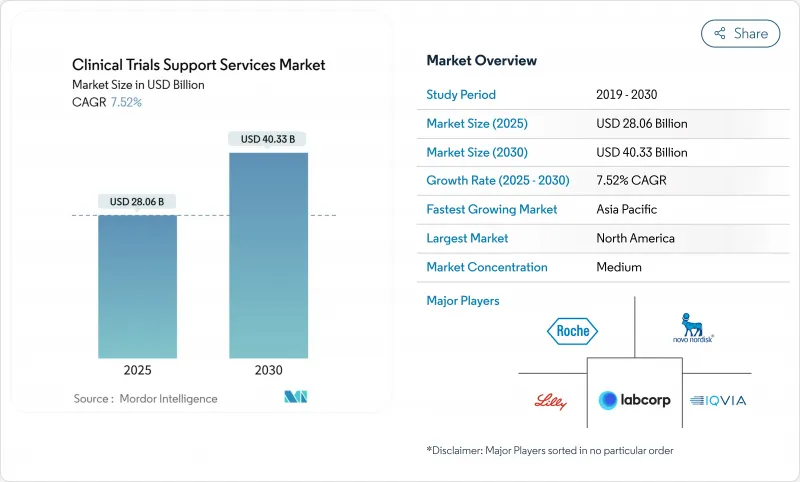

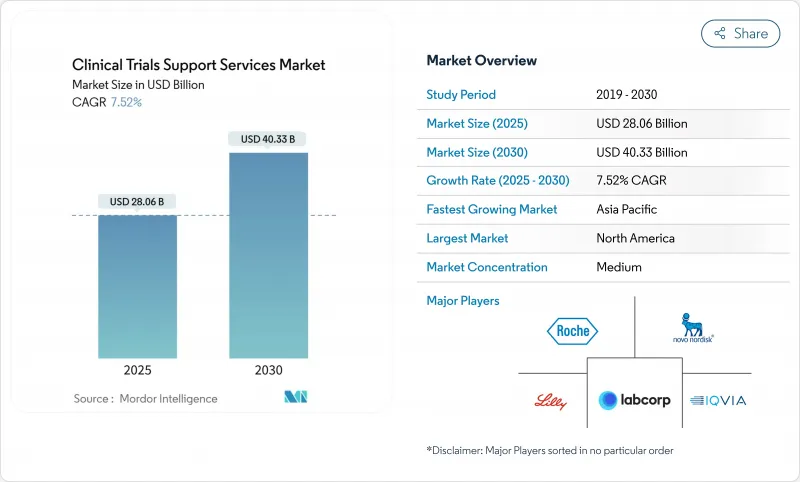

임상시험 지원 서비스 시장 규모는 2025년 280억 6,000만 달러에 이르고, 2030년에는 CAGR 7.52%를 나타내 403억 3,000만 달러에 달할 것으로 예측됩니다.

확대 배경에는 연구개발 파이프라인 확대, 전문 아웃소싱 모델에 대한 수요 증가, 환자 등록 타임라인 단축을 위한 인공지능 채택 확대 등이 있습니다. 스폰서는 데이터 프라이버시, 공급망 무결성, 실제 증거 생성을 조화시킬 수 있는 엔드 투 엔드 파트너를 더욱 중시합니다. 업데이트된 CONSORT 2025 가이드라인과 같은 규제 이니셔티브는 통합된 품질 시스템을 갖춘 공급자에게 유리한 투명성 요구 사항을 늘리고 있습니다. 신흥 시장 참가 기업에 의해 임상 업무가 재조합되어 기업 인수의 물결에 의해 암 영역 등의 복잡한 치료 영역에서 대기업 벤더가 규모의 우위성을 획득하고 있습니다.

세계 의약품 스폰서는 코디네이션 갭을 줄이고 어카운터빌리티를 높이기 위해 공급업체 목록을 통합합니다. 풀 서비스 파트너는 프로토콜 설계, 데이터 관리 및 규제 당국에 대한 신청을 하나의 계약으로 통합하여 사이클 시간과 관리 오버헤드를 줄입니다. AI 모델을 임상 워크플로우에 통합하는 엔비디아와 IQVIA 협업과 같은 기술 제휴는 공급업체의 시설 식별, 전자 소스 검토 및 부작용 감지 자동화를 지원합니다. 이 접근법은 집계적인 전문 지식과 지속적인 데이터 검토가 중요한 종양학 및 희귀질환 프로그램에 특히 가치가 있습니다. 바이오테크놀러지 기업은 자본의 제약과 스케쥴의 전복에 대처하면서 초기 단계의 자산을 중요한 시험으로 전환하기 위해 이러한 통합된 서비스를 점점 이용하고 있습니다.

스폰서는 아시아태평양 허브로 활동을 전환하여 40-60%의 비용 절감을 달성하고 동시에 치료받지 않은 집단에 액세스하여 모집을 가속화할 수 있습니다. 중국의 3SBio가 60억 달러의 라이선싱 계약을 획득한 것은 이 지역이 늦은 임상시험을 실시할 때 고도화되고 있음을 보여줍니다. 인도의 CDSCO와 같은 각국의 규제 당국은 계속 승인의 합리화를 진행하고, 시험 시작까지의 리드 타임을 단축하고 있습니다. 그럼에도 불구하고이 지역의 기세를 유지하기 위해서는 인프라 격차와 임상 책임 의사의 훈련이 성공의 결정이 될 것입니다.

데이터 거버넌스의 의무화는 복잡성과 비용을 증가시킵니다. HIPAA의 온라인 추적 지침의 일부를 취소한 미국 연방 판결은 디지털 채용 도구의 불확실성을 돋보이게 합니다. 다국적 프로그램은 예산의 15-20%를 컴플라이언스 전문가, 안전한 호스팅, 동의 관리 플랫폼으로 향하게 하는 경우가 많습니다. 의료 조직의 44%는 데이터 거버넌스 보고서를 작성하는 데 어려움을 겪고 있으며 전문 리스크 관리 소프트웨어에 대한 수요가 증가하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

3단계는 규제 당국에 안전성과 효능을 입증하는 매우 중요한 역할을 반영하여 2024년 45.52%의 최대 판매 점유율을 차지했습니다. 이러한 후기 단계에서는 수천 명의 참가자, 여러 지역, 엄격한 데이터 무결성 검사를 수행하는 경우가 많으며 고급 모니터링 및 실시간 분석이 필요합니다. 스폰서는 통계적 타당성을 손상시키지 않으면서 수정을 가능하게 하는 적응적 디자인 요소를 점차 통합하고 있습니다. 그 규모에도 불구하고, 단계 III의 비용 압력은 프로토콜 설계를 최적화하고 현장 방문을 줄이기 위해 위험 기반 모니터링을 활용하는 동기 부여가되었습니다.

1상 시험의 CAGR은 2030년까지 가장 빠른 9.25%를 나타낼 전망입니다. 이는 벤처기업의 지원을 받은 바이오테크놀러지 기업이 새로운 치료법을 인간 초임상시험으로 추진하기 때문입니다. 블랙핀 바이오(BlackfinBio)와 같은 유전자 치료 진출 기업은 고급 바이러스 벡터와 복잡한 용량 증가 체계에 의존하는 유전성 경련 대 마비의 1/2 단계 프로토콜에서 식품 의약국의 허가를 확보했습니다. 이러한 급증에는 약동학 모델링, 센티넬 투여 및 중앙 집중식 안전 모니터링 전문 지식을 갖춘 서비스 파트너가 필요합니다. 제1상과 제II상을 교차하는 적응적이고 원활한 접근법이 인기를 끌고 있으며, 기존의 위상의 정의가 더욱 모호해지고, 유연하고 기술 대응력이 있는 벤더 수요가 높아지고 있습니다.

2024년 임상시험 지원 서비스 시장 규모에서는 환자의 모집과 유지가 28.53%의 점유율을 차지했으며, 등록에 관한 근본적인 과제가 부각되었습니다. 공급업체는 AI 도구를 도입하여 환자를 매칭하고, 탈락 위험을 예측하며, 어드히어런스 지표를 개선하기 위해 참여 컨텐츠를 조정합니다. CAGR 10.35%로 성장하는 규제·컨설팅 서비스는 FDA의 M13A 생물학적 동등성 프레임워크와 같은 세계 가이던스 변화에 대응하여 자료 작성과 전략적 조언 수요를 깊게 합니다. 지역별 전문 지식을 갖춘 공급자는 현지 문서를 국제 표준에 맞추어 승인을 가속화할 수 있습니다.

물류 혁신도 성장을 뒷받침합니다. 파나소닉 빅셀 컨테이너는 mRNA와 세포 치료의 선적에 필수적인 기능인 무전원으로 10 일 동안 깊은 냉동 온도를 유지합니다. 통합 제조 및 포장 준비는 후원자가 공급망의 위험을 줄이고 대륙을 넘어 시험 약물의 무결성을 보장하는 데 도움이 됩니다. 첨단 바이오 분석 실험실은 동반진단 및 멀티오믹스 엔드포인트에 대응하는 분석의 제공을 확대하고 엔드 투 엔드 서비스 제안을 강화합니다.

아시아태평양의 CAGR은 11.62%를 나타내, 10년 후까지는 기존의 중심지를 추월할 것으로 보입니다. 정부의 우대 조치, 미치료 인구의 많음, 윤리 승인 프로세스의 신속화에 의해 지금까지 구미의 시설에서 행해지고 있던 퍼스트 인 인간 시험이 주목받고 있습니다. 중국과 같은 국가는 복잡한 생물학적 제제를 관리할 수 있는 고처리량 1상 시험 시설을 건설하고, 일본 기술 기업은 임상 책임 의사의 데이터 입력 작업을 완화하는 맞춤형 AI 에이전트를 제공합니다.

북미는 여전히 임상시험 지원 서비스 시장 점유율의 38.82%를 차지하고 있으며, 이는 식품의약국의 구조화된 피드백기구와 시험책임 의사밀도의 높이에 지지되고 있습니다. 그러나 이 지역은 임금 상승과 임상시험 직원의 불타는 증후군에 시달리고 있습니다. FDA의 자원 제약으로 인해 신청 심사 기간이 장기화될 우려가 있으며, 시험 개시가 지연될 수 있기 때문에 스폰서는 지역을 다양화할 필요가 있습니다.

유럽은 엄격한 과학적 수준과 전문 연구 책임 의사에 대한 접근으로 평가되고 있지만 일반 데이터 보호 규정 준수의 복잡성과 에너지 비용 상승이 특히 초저온 물류 예산을 압박하고 있습니다. 남미와 중동, 아프리카는 양국어를 구사하는 임상 책임 의사, 인프라 개선, 비용 절감에 도움이 되며, Ⅱ상 및 Ⅲ상 시험 등록에 차지하는 비율이 증가하고 있습니다. 이러한 지역에서의 장기적인 성공은 시설 인증, 사이버 보안 데이터 플랫폼, 지역 특유의 환자 참여 전략에 대한 지속적인 투자에 달려 있습니다.

The clinical trial support services market size reached USD 28.06 billion in 2025 and is forecast to climb to USD 40.33 billion by 2030 at a 7.52% CAGR.

Expansion is driven by growing R&D pipelines, rising demand for specialized outsourcing models, and wider adoption of artificial intelligence that shortens patient enrollment timelines. Sponsors are placing greater emphasis on end-to-end partners capable of harmonizing data privacy, supply-chain integrity, and real-world evidence generation. Regulatory initiatives such as the updated CONSORT 2025 guideline are increasing transparency requirements, which favors providers with integrated quality systems. Emerging-market participation is reshaping clinical operations, and a wave of acquisitions is giving larger vendors scale advantages in complex therapeutic areas such as oncology.

Global drug sponsors are consolidating vendor lists to cut coordination gaps and boost accountability. Full-service partners combine protocol design, data management, and regulatory filing under a single contract, lowering cycle times and administrative overhead. Technology alliances-such as NVIDIA's collaboration with IQVIA that embeds AI models into clinical workflows-help vendors automate site identification, electronic source review, and adverse-event detection. The approach is especially valuable for oncology and rare-disease programs, where multidisciplinary expertise and continuous data review are critical. Biotech firms, managing capital constraints and accelerated timelines, increasingly rely on these integrated offerings to convert early-stage assets into pivotal studies.

Sponsors achieve 40-60% cost relief by shifting activities to Asia-Pacific hubs while accessing treatment-naive populations that speed recruitment. China's 3SBio secured a USD 6 billion licensing deal that demonstrates the region's growing sophistication in late-phase execution. National regulators, such as India's CDSCO, continue to streamline approvals, trimming site-initiation lead times. Nonetheless, infrastructure gaps and investigator training remain success determinants for sustained regional momentum.

Data-governance mandates add complexity and cost. A U.S. federal ruling that vacated sections of the HIPAA online-tracking guidance highlights ongoing uncertainty for digital recruitment tools. Multinational programs often divert 15-20% of budgets to compliance experts, secure hosting, and consent-management platforms. Forty-four percent of healthcare organizations struggle with data-governance reporting, amplifying the demand for specialized risk-management software.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Phase III commanded the largest 45.52% revenue share in 2024, reflecting its pivotal role in proving safety and efficacy to regulators. These late-stage studies often involve thousands of participants, multiple geographic regions, and stringent data-integrity checks, demanding sophisticated monitoring and real-time analytics. Sponsors increasingly integrate adaptive design elements that allow modifications without compromising statistical validity. Despite its size, Phase III cost pressures motivate companies to optimize protocol designs and leverage risk-based monitoring to reduce on-site visits.

Phase I displays the fastest 9.25% CAGR through 2030 as venture-backed biotech firms push novel modalities into first-in-human trials. Gene therapy entrants such as BlackfinBio secured Food and Drug Administration clearance for Phase 1/2 hereditary spastic paraplegia study protocols that rely on advanced viral vectors and complex dose-escalation schemes. This surge requires service partners with expertise in pharmacokinetic modeling, sentinel dosing, and intensive safety surveillance. Adaptive seamless approaches that bridge Phase I and Phase II are gaining popularity, further blurring traditional phase definitions and heightening demand for flexible, technology-ready vendors.

Patient recruitment and retention dominated with 28.53% share of the clinical trial support services market size in 2024, highlighting persistent enrollment challenges. Vendors deploy AI tools to match patients, predict dropout risk, and tailor engagement content to improve adherence metrics. Regulatory and consulting services, growing at 10.35% CAGR, address global guidance shifts such as the FDA's M13A bioequivalence framework, which deepens demand for dossier preparation and strategic advice. Providers with region-specific knowledge can accelerate approvals by aligning local documentation with international standards.

Logistics innovations also propel growth. Panasonic's VIXELL container maintains deep-frozen temperatures for ten days without power, a vital feature for mRNA and cell-therapy shipments. Integrated manufacturing and packaging arrangements help sponsors mitigate supply-chain risks and ensure investigational product integrity across continents. Advanced bio-analytical labs expand assay offerings to accommodate companion diagnostics and multi-omics endpoints, strengthening end-to-end service propositions.

The Clinical Trial Support Services Market Report is Segmented by Phase (Phase I, Phase II, and More), Service Types (Clinical Trial Site Management, Patient Recruitment & Retention, and More), End User (Pharmaceutical Companies, Biotechnology Companies, and More), Therapeutic Area (Oncology, Cardiology, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific is advancing at an 11.62% CAGR and is set to overtake traditional hubs by the end of the decade. Government incentives, large treatment-naive populations, and faster ethics approval processes attract first-in-human studies that previously defaulted to Western sites. Countries such as China build high-throughput phase-I units capable of managing complex biologics, and technology firms in Japan deliver tailored AI agents that reduce data-entry workloads for investigators.

North America still accounts for the largest 38.82% clinical trial support services market share, supported by the Food and Drug Administration's structured feedback mechanisms and high investigator density. Yet the region wrestles with escalating wage inflation and burnout among site staff. Resource constraints at the FDA raise concerns that application review timelines could lengthen, potentially slowing study starts and prompting sponsors to diversify geography.

Europe is respected for rigorous scientific standards and access to specialist investigators, but General Data Protection Regulation compliance complexity and elevated energy costs pressure budgets, especially for ultra-low-temperature logistics. South America and the Middle East & Africa contribute a growing share of phase II and phase III enrollment, aided by bilingual investigators, improving infrastructure, and cost savings. Long-term success in these regions will depend on sustained investments in site accreditation, cyber-secure data platforms, and region-specific patient-engagement strategies.