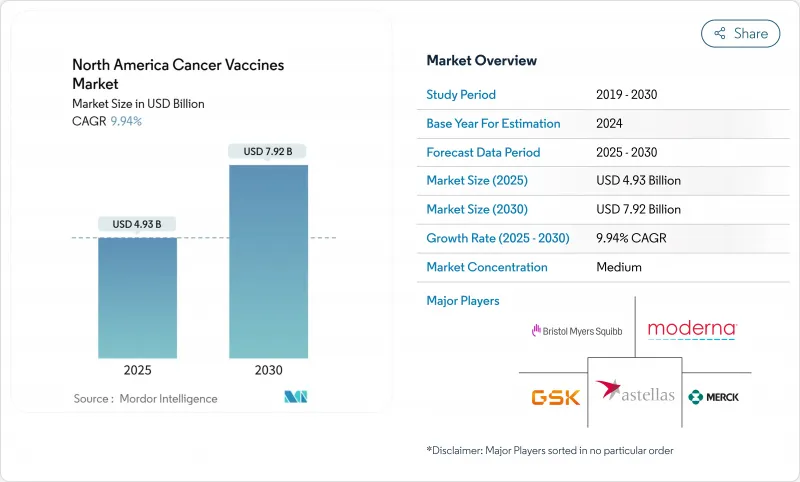

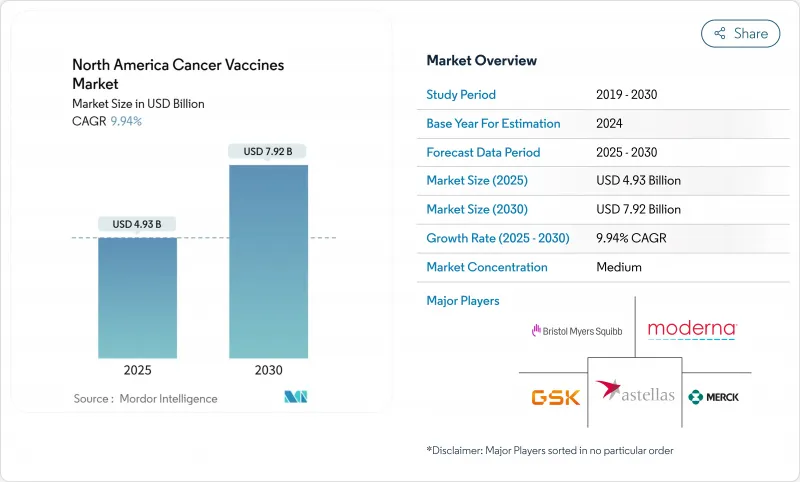

북미의 암 백신 시장은 2025년에는 49억 3,000만 달러가 되고, 2030년에는 79억 2,000만 달러에 이를 것으로 예측되며, CAGR은 9.94%를 나타낼 전망입니다.

mRNA 플랫폼의 임상적 성공 증가, 공적 자금 지원, 보다 광범위한 상환 정책을 통해 치료 백신은 실험 상황에서 정밀 종양학 도구의 주류로 전환하고 있습니다. 미국암협회는 2025년에 204만명 이상의 암이 새롭게 진단될 것으로 예상하고 있으며, 예방·치료 백신접종 프로그램의 대상 인구가 확대되고 있습니다. 특히 흑색종을 대상으로 하는 mRNA 주도 파이프라인은 획기적인 치료법의 지정에 따라 기세를 늘리고 있으며, 병원 시스템은 개별화 제품의 리드 타임을 단축하는 POC(Point-of-Care) 제조 허브에 투자하고 있습니다. 한편 메디케어 메디케이드 서비스센터(CMS)에 의한 보험 적용 결정이 강화되어 백신 기반의 처방이 보험 상환되는 의사의 신뢰가 향상되고 있습니다.

조기 발견 프로그램은 백신 기반의 개입이 유익한 단계에서 암을 확인하고 있습니다. 미국에서는 2025년에 204만명 이상의 신규 암 증례가 발생할 것으로 예측되고 있으며, 이는 200만명의 대대를 넘는 역사적인 사건입니다. 캐나다에서는 2024년에 24만 7,100명이 새로 고통을 받고 남성의 이환율이 여성의 이환율을 상회했으며, 성별에 특화된 백신 캠페인의 여지가 있었습니다. 브리티시 컬럼비아 주에서는 HPV를 기반으로 한 검진을 통해 자궁 경부 병변의 조기 발견이 가능해지고 예방 및 치료 백신의 임상 가치 제안이 강화되었습니다. 고위험자에 대한 정기적인 피부 영상 진단은 마찬가지로 mRNA 백신이 효과를 나타내는 단계에서 흑색 종을 발견합니다. 이환율의 상승과 스크리닝의 향상이 함께, 치료 가능한 환자층이 확대되고, 북미의 암 백신 시장은 2자리 가까운 속도로 성장하고 있습니다.

연방 정부 기관은 선진 백신 과학을 전염병 대책에 머무르지 않는 국가 안보 우선 순위로 자리 매김하고 있습니다. 미국 보건사회복지성은 2025년 1월 팬데믹 인플루엔자 대책으로서 5억 9,000만 달러를 Modernna사에 공여했지만 같은 제조 라인은 암 페이로드에도 활용했습니다. BARDA의 가속기 네트워크 2.0은 벤처 캐피탈의 위험을 줄이기 위해 암 백신을 포함한 즉각적인 치료제에 여러 해의 보조금을 제공합니다. 미국 국립암 연구소는 2024년도에 425만 달러를 암 면역 예방 네트워크(Cancer Immunoprevention Network)에 계상하여 초기 연구에 자금을 제공했습니다. ARPA-H의 APECx 프로그램은 인공지능을 항원 탐색에 적용하고 개발주기를 수년에서 수개월로 단축하려고 합니다. 공적자본과 비공개자본을 거듭함으로써 공개회사는 신속하게 제조규모를 확대할 수 있어 북미 암 백신 시장의 장기적인 확대를 지원할 수 있습니다.

화학·제조·관리(CMC) 규칙은 각 환자마다 변화하는 제품에 엄격합니다. Coalition for Epidemic Preparedness Innovations는 안정성과 분석 검토만으로 일정에 18-24개월을 추가할 수 있다고 지적합니다. 개인화된 mRNA 배치는 개별적으로 무균성 및 역가 검사를 통과해야 하며 제조 기간은 4-6주 동안 길어집니다. 미국 식품의약국은 신항원 예측에 사용되는 AI 알고리즘에 대한 지침을 초안 중 규제상의 모호함을 초래하고 있습니다. 품질관리에 관한 깊은 전문지식을 가진 기업은 오버헤드를 흡수할 수 있지만, 소규모 진입기업은 고전을 강요받을 수 있어 북미 암 백신 시장의 단기적인 성장을 억제하는 요인이 되고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

2024년 북미의 암 백신 시장은 성숙한 공급망과 수십년에 걸친 규제 당국과의 친화성을 배경으로 유전자 재조합 제제가 45.54%의 점유율로 견인했습니다. 그러나 이 부문은 2030년까지 연평균 복합 성장률(CAGR) 10.71%를 나타내는 mRNA 백신에 기세를 빼앗길 것으로 예측됩니다. Moderna와 Merck의 V940은 흑색종 재발 위험을 49% 줄인다는 것을 보여주고 FDA의 돌파 상태를 획득했습니다. BioNTech의 BNT111과 같은 다른 mRNA 후보는 체크포인트 억제제와 함께 사용하여 상당한 연주 효율을 나타냅니다. 합성 RNA는 세포 배양의 병목을 피할 수 있기 때문에 생산자는 새로운 적응증으로 빠르게 축발을 옮길 수 있습니다.

자동화와 AI가 엔드 투 엔드 워크플로우에 통합되어 개발 사이클이 수년에서 12개월 미만으로 단축되었습니다. 바이러스 벡터와 DNA 플랫폼은 틈새 역할을 계속하고 있지만, 면역 원성과 확장 성의 한계에 직면하고 있습니다. 홀 셀과 수지상 세포에 의한 접근법은 개별화 처리와 관련된 비용이 높습니다. 이러한 현실이 밝혀짐에 따라 자본은 RNA 전문가에게 재분배되어 북미 암 백신 시장의 중기적인 확대를 지원하고 있습니다.

2024년 매출은 90.56%를 차지하고 예방법이 여전히 우세했지만, 이는 주로 CMS가 확실히 커버하고 있는 전국적인 HPV 프로그램에 의한 것입니다. 그러나 치료 제품은 어쥬번트나 네오애쥬번트에서의 역할이 실세계의 근거에 의해 검증되어 CAGR 10.84%를 나타낼 전망입니다. 캐나다의 최신 지침은 9세에서 20세까지의 단일 용량 HPV 일정을 승인하고 보험 적용을 개선하고 치료 조종사에 대한 예산을 확보했습니다.

마운트 사이나이의 PGV001 시험은 여러 종양 유형에서 참가자의 거의 절반으로 5년생존을 유지합니다. Vvax001은 자궁 경부 상피내 신생물 병변을 94% 감소시켰습니다. 의료 시스템의 조종사는 예방과 치료 전략을 결합하는 경우가 많으며 평생 면역 경로를 가정합니다. 이러한 시장개척은 치료용 주사의 강력한 성장 전망을 강화하고 2030년을 향해 북미 암 백신 시장의 확대를 지속시킵니다.

북미의 암 백신 시장은 기술별(유전자 재조합 백신, 기타), 치료법별(예방 백신, 치료 백신), 암 종별(자궁경부암(HPV), 흑색종, 기타), 전달 경로별(근육내, 정맥내, 기타), 지역별(미국, 캐나다, 멕시코)로 분류됩니다. 시장 및 예측은 금액(달러)으로 제공됩니다.

The North America cancer vaccines market is valued at USD 4.93 billion in 2025 and is forecast to reach USD 7.92 billion by 2030, advancing at a solid 9.94% CAGR.

Rising clinical success of mRNA platforms, supportive public funding, and broader reimbursement policies are moving therapeutic vaccines from experimental status to mainstream precision-oncology tools. The American Cancer Society expects more than 2.04 million new cancer diagnoses in 2025, enlarging the eligible population for preventive and therapeutic vaccination programs. mRNA-driven pipelines, particularly for melanoma, are gaining momentum after breakthrough therapy designations, while hospital systems invest in point-of-care manufacturing hubs that shorten lead times for individualized products. Meanwhile, stronger coverage decisions by the Centers for Medicare & Medicaid Services (CMS) improve physician confidence that vaccine-based regimens will be reimbursed.

Early detection programs are identifying cancers at stages where vaccine-based interventions can add meaningful benefit. The United States expects more than 2.04 million new cancer cases in 2025, a historic first above the 2 million mark . Canada projects 247,100 new cases in 2024, with male incidence surpassing female levels, opening room for gender-specific vaccine campaigns . Provincial HPV-based screening in British Columbia is enabling earlier cervical lesion detection, which strengthens the clinical value proposition of both preventive and therapeutic vaccines. Routine skin imaging for high-risk individuals is likewise catching melanoma at stages where mRNA vaccines have shown benefit. Together, rising incidence and better screening broaden the pool of treatable patients, helping the North America cancer vaccines market grow at nearly double-digit speed.

Federal agencies are positioning advanced vaccine science as a national security priority that extends well beyond infectious-disease preparedness. The U.S. Department of Health and Human Services granted USD 590 million to Moderna in January 2025 for pandemic influenza work, but the same production lines can pivot to oncology payloads . BARDA's Accelerator Network 2.0 is channeling multi-year grants into rapid-response therapeutics, including cancer vaccines, which lowers venture-capital risk. The National Cancer Institute earmarked USD 4.25 million in FY2024 for the Cancer Immunoprevention Network to finance early research. ARPA-H's APECx program is applying artificial intelligence to antigen discovery, shrinking development cycles from years to months. With layered public and private capital, platform companies can scale manufacturing quickly, supporting the long-run expansion of the North America cancer vaccines market.

Chemistry, Manufacturing, and Controls (CMC) rules are rigorous for products that change from patient to patient. The Coalition for Epidemic Preparedness Innovations notes that stability and analytics reviews alone can add 18-24 months to timelines. Each personalized mRNA batch must pass individual sterility and potency checks, lengthening production by 4-6 weeks. The U.S. Food and Drug Administration is still drafting guidance on AI algorithms used in neoantigen prediction, introducing regulatory ambiguity. Firms with deep quality-control expertise can absorb the overhead, but smaller entrants may struggle, which tempers near-term growth in the North America cancer vaccines market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Recombinant products led the North America cancer vaccines market with 45.54% share in 2024, powered by mature supply chains and decades of regulatory familiarity. However, the segment is forecast to cede momentum to mRNA vaccines, which are expanding at a 10.71% CAGR through 2030. Moderna and Merck's V940 secured FDA breakthrough status after demonstrating a 49% risk reduction for melanoma recurrence. Other mRNA candidates, such as BioNTech's BNT111, are posting meaningful response rates when combined with checkpoint inhibitors. The shift underscores a structural advantage: synthetic RNA avoids cell-culture bottlenecks, letting producers pivot quickly to new indications.

Automation and AI are now embedded in end-to-end workflows, trimming development cycles from several years to under twelve months for follow-on products. Viral-vector and DNA platforms continue to play niche roles but face limits in immunogenicity and scalability. Whole-cell and dendritic approaches carry high costs tied to individualized processing. As these realities become clearer, capital reallocates toward RNA specialists, anchoring medium-term expansion of the North America cancer vaccines market.

Preventive modalities still dominate, accounting for 90.56% revenue in 2024, largely due to nationwide HPV programs with robust CMS coverage. Yet therapeutic products are accelerating at 10.84% CAGR as real-world evidence validates their role in adjuvant and neoadjuvant settings. Canada's updated guidelines endorse single-dose HPV schedules for ages 9-20, improving coverage while freeing budgets for therapeutic pilots.

Mount Sinai's PGV001 study maintains 5-year survival in almost half of participants across multiple tumor types. Vvax001 has shown a 94% reduction in cervical intraepithelial neoplasia lesions. Health-system pilots increasingly combine prophylactic and treatment strategies, envisioning lifetime immunization pathways. These developments reinforce strong growth prospects for therapeutic injections, sustaining the North America cancer vaccines market expansion toward 2030.

The North America Cancer Vaccines Market is Segmented by Technology (Recombinant Vaccines, and More), Treatment Method (Preventive Vaccines and Therapeutic Vaccines), Cancer Type (Cervical Cancer (HPV), Melanoma and More), Delivery Route (Intramuscular, Intravenous, and More), and Geography (United States, Canada, and Mexico). The Market and Forecasts are Provided in Terms of Value (USD).