북미의 위성 버스 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 성장 예측

North America Satellite Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693950

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

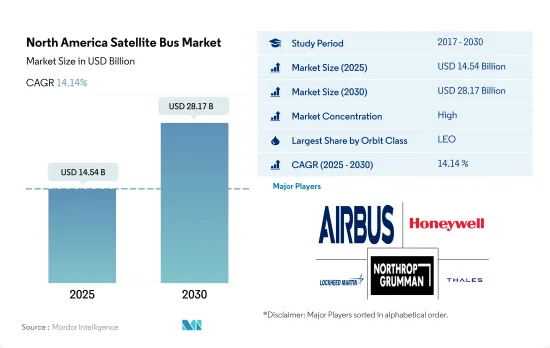

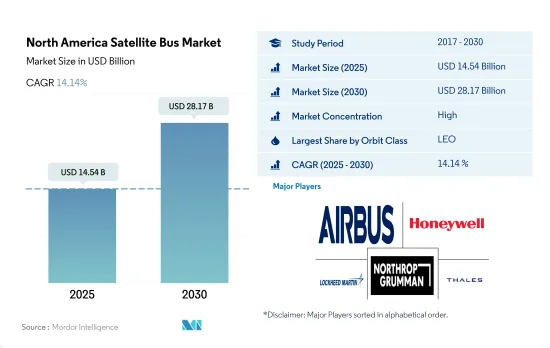

북미 위성 버스 시장 규모는 2025년에 145억 4,000만 달러로 추정되고, 2030년에는 281억 7,000만 달러에 이를 전망이며 예측 기간(2025-2030년) 동안 CAGR 14.14%를 보일 것으로 예측됩니다.

다양한 위성 용도로 LEO 궤도에 대한 위성 발사가 증가하여 시장 수요를 견인

북미의 위성 버스 시장은 통신이나 네비게이션에서 원격 탐사나 과학 연구까지 폭넓은 용도로 발생하는 위성 기반 서비스에 대한 수요 증가가 시장을 견인하고 있습니다.

LEO 위성은 지구 관측, 원격 탐사, 과학 연구 등의 용도로 수요가 있습니다. Boeing 502 Phoenix, Lockheed Martin LM 400, Northrop Grumman GeoStar-3 등 다양한 기업이 제공하는 버스 솔루션이 존재합니다.

대용량 데이터 전송, 세계 커버리지, 고화질 방송 기능의 요구가 GEO 위성 수요를 견인하고 있습니다. Boeing 702, Lockheed Martin A2100, Maxar Technologies 1300-class 등 다양한 기업이 통신 및 방송 미션을 위한 혁신적인 솔루션을 제공합니다.

MEO 위성은 통신 및 네비게이션 등의 용도로 사용됩니다. Lockheed Martin사의 LM2100 등은 통신과 네비게이션의 미션에 첨단 솔루션을 제공합니다.

북미 위성 버스 시장 동향

연료 효율과 운영 효율 향상에 대한 동향이 나타나고 있습니다.

위성 버스(또는 우주선 버스)는 위성과 우주선의 본체이자 구조 부품이며 그 안에 페이로드와 모든 과학 기기가 탑재됩니다. 위성 통신은 5G 인프라에 필수적인 요소가 될 것으로 예측됩니다. 지상과 위성 간의 원활한 연결성을 제공하기 위해 위성 운송망은 전체 통신 지도에 통합되어 있습니다.

중국은 우주 기반의 능력 증강을 향해 엄청난 자원을 투입하고 있습니다. 중국의 스타트업 SpaceWish의 초소형 위성이 CZ-2C(3) 로켓에 탑재되어 LEO에 발사되었습니다.

초소형 위성의 자발적인 개발은 인도의 산업이 힘을 쏟고 있는 부문 중 하나입니다. Exseed Space는 ExseedSAT 1이라고 명명된 초소형 위성을 발사하여 무선 아마추어에게 중요한 통신을 제공했습니다. 이번 발사로 인도 최초의 민간 소유 위성이 우주에 진출하게 되었습니다.

각 우주 기관의 우주 개발비 증가는 위성 산업에 긍정적인 영향을 미칠 것으로 예측됩니다.

북미 우주 프로그램에 대한 정부 지출은 2021년 약 200억 달러에 달하였습니다. 이 지역은 세계 최대의 우주 기관인 NASA가 존재하는 우주 혁신과 연구의 진원지입니다. 우주 부문에 대한 대규모 투자는 다양한 다른 서브 시스템 부품 제조업체를 끌어들여 기회를 창출하고 있습니다.

이 지역에서는 2022년 미국 정부가 우주 프로그램에 240억 달러 가까이 투입하여 세계에서 가장 우주 개발비를 많이 투자한 나라가 되었습니다. 캐나다 정부에 따르면 미국과는 별도로 캐나다의 우주 부문은 캐나다의 GDP에 23억 달러를 기여하고 1만 명을 고용하고 있습니다. 캐나다 정부의 보고서에 따르면 캐나다 우주 관련 기업의 90%는 중소기업입니다. 캐나다 우주국(CSA)의 예산은 적정 수준이며 2022-2023년의 예산 지출 전망액은 3억 2,900만 달러였습니디ㅏ.

설문 조사 및 투자 조성과 관련하여, 이 지역의 정부와 민간 부문은 우주 부문의 연구와 혁신을 위한 전용 자금을 마련하고 있습니다. 각 기관은 의무적인 금전적 약속을 통해 이용 가능한 예산 자원을 지출합니다. 예를 들어, 2023년 2월까지 미국 항공우주국(NASA)은 연구 보조금으로 3억 3,300만 달러를 분배했습니다.

북미 위성 버스 산업 개요

북미의 위성 버스 시장은 상당히 통합되어 있으며 상위 5개사에서 71%를 차지하고 있습니다. 이 시장의 주요 기업은 Airbus SE, Honeywell International Inc., Lockheed Martin Corporation, Northrop Grumman Corporation, Thales입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

위성의 소형화

위성 질량

우주 개발에의 지출

규제 프레임워크

캐나다

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

용도

통신

지구 관측

네비게이션

우주 관측

기타

위성 질량

10-100kg

100-500kg

500-1,000kg

10kg 이하

1,000kg 이상

궤도 클래스

GEO

LEO

MEO

최종 사용자

상업

군사 및 정부

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Airbus SE

Ball Corporation

Honeywell International Inc.

Lockheed Martin Corporation

Nano Avionics

NEC

Northrop Grumman Corporation

Sierra Nevada Corporation

Thales

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The North America Satellite Bus Market size is estimated at 14.54 billion USD in 2025, and is expected to reach 28.17 billion USD by 2030, growing at a CAGR of 14.14% during the forecast period (2025-2030).

Increasing launches of satellites into LEO orbit for various satellite applications is driving the market demand

The North American satellite bus market is driven by the increasing demand for satellite-based services, with applications ranging from communication and navigation to remote sensing and scientific research.

LEO satellites are in demand for applications such as Earth observation, remote sensing, and scientific research. For LEO satellites, various companies offer a range of bus solutions, including the Boeing 502 Phoenix, the Lockheed Martin LM 400, and the Northrop Grumman GeoStar-3. These buses are designed to support a range of LEO applications. Between 2017 and 2022, approximately 3,021 satellites were launched into LEO.

The need for high-capacity data transmission, global coverage, and high-quality broadcasting capabilities drives the demand for GEO satellites. For GEO orbit, various companies offer innovative solutions for communication and broadcasting missions, including the Boeing 702, the Lockheed Martin A2100, and the Maxar Technologies 1300-class. These buses are designed to provide long-term, stable service for satellite-based services. Between 2017 and 2022, approximately 33 satellites were launched into GEO.

MEO satellites are used for applications such as communication and navigation. The demand for MEO satellites is driven by the need for high-capacity data transmission, improved navigation capabilities, and advanced imaging technologies. Companies like Airbus, The Boeing Company, and Lockheed Martin offer advanced solutions for communication and navigation missions, including the Airbus Eurostar Neo, the Boeing 702MP, and the Lockheed Martin LM 2100. Between 2017 and 2022, approximately seven satellites were launched into MEO. With such developments, the overall market is expected to grow by 17% during 2023-2029.

North America Satellite Bus Market Trends

The trend for better fuel and operational efficiency has been witnessed

A satellite bus (or spacecraft bus) is the main body and structural component of a satellite or spacecraft, in which the payload and all scientific instruments are held. Moreover, the growing utilization of commercial satellite platforms for dual (military and civil) purposes has boosted the satellite bus market. Satellite communications are envisioned to be an essential part of the 5G infrastructure. In order to provide seamless connectivity between terrestrial and satellite, the satellite transport conduit is being integrated into the overall communication map. This will result in new opportunities for extending satellite services in urban and rural areas.

China is investing significant resources toward augmenting its space-based capabilities. The country has launched the largest number of nano and microsatellites in Asia-Pacific. In April 2022, Chinese startup SpaceWish's nanosatellite was launched into LEO boarding CZ-2C (3) rocket. XINGYUAN-2 is a 6U remote sensing CubeSat that weighs approximately 7.5 kg.

In addition, the indigenous development of nano and microsatellites has been one of the areas of emphasis for the industry in India. Many startups and universities are developing these satellites at various levels in the country. For instance, in December 2018, Exseed Space launched a nanosatellite named ExseedSAT 1 to provide vital communication for radio amateurs. This was India's first privately owned satellite into space. Countries like Australia, Malaysia, South Korea, and Singapore are also investing in the development of nano and microsatellites.

The increasing space expenditures of different space agencies are expected to impact the satellite industry positively

Government's spending on space programs in North America hit approximately around 20 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. Since, the major investments in this field attracts various other sub system and component manufacturers and creates opportunities for them.

In the region, in 2022, the US government spent nearly USD 24 billion on its space programs, making it the highest spender on space in the world. Apart from the United States, the Canadian space sector adds USD 2.3 billion to the Canadian GDP and employs 10,000 people, according to the Canadian government. The government reports that 90% of Canadian space firms are small- and medium-sized businesses. The Canadian Space Agency (CSA) budget is modest, and the estimated budgetary spending for 2022-23 was USD 329 million.

In terms of research and investment grant, the region's governments and the private sector have dedicated funds for research and innovation in the space sector. Agencies spend available budgetary resources by making financial promises called obligations. For instance, till February 2023, the National Aeronautics and Space Administration (NASA) distributed USD 333 million as research grants.

North America Satellite Bus Industry Overview

The North America Satellite Bus Market is fairly consolidated, with the top five companies occupying 71%. The major players in this market are Airbus SE, Honeywell International Inc., Lockheed Martin Corporation, Northrop Grumman Corporation and Thales (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Satellite Miniaturization

4.2 Satellite Mass

4.3 Spending On Space Programs

4.4 Regulatory Framework

4.4.1 Canada

4.4.2 United States

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application

5.1.1 Communication

5.1.2 Earth Observation

5.1.3 Navigation

5.1.4 Space Observation

5.1.5 Others

5.2 Satellite Mass

5.2.1 10-100kg

5.2.2 100-500kg

5.2.3 500-1000kg

5.2.4 Below 10 Kg

5.2.5 above 1000kg

5.3 Orbit Class

5.3.1 GEO

5.3.2 LEO

5.3.3 MEO

5.4 End User

5.4.1 Commercial

5.4.2 Military & Government

5.4.3 Other

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).