ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

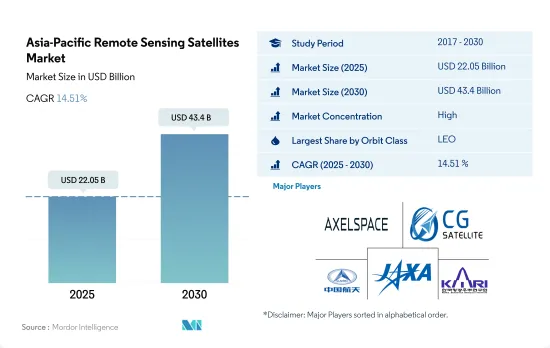

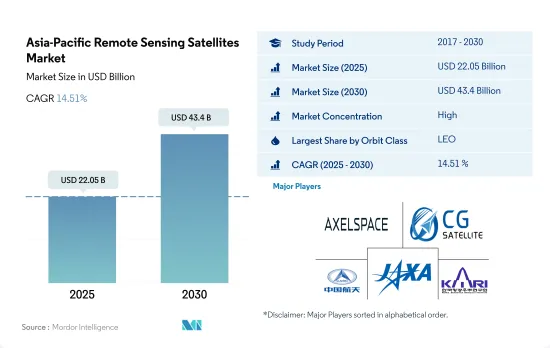

아시아태평양의 원격 탐사 위성 시장 규모는 2025년에는 220억 5,000만 달러로 추정되며, 2030년에는 434억 달러에 이를 것으로 예측되고, 예측 기간(2025-2030년) 동안 CAGR 14.51%로 성장할 전망입니다.

LEO 위성이 시장 수요를 크게 견인

아시아태평양에서는 지구저궤도(LEO), 지구중궤도(MEO), 정지궤도(GEO) 등 폭넓은 위성 궤도에 대응하는 위성 버스 수요가 대폭 증가하고 있습니다.

LEO 위성은 지구 관측, 기상 예보, 통신 등 다양한 용도로 이용되고 있습니다.

MEO 위성은 GPS나 갈릴레오와 같은 세계 네비게이션이나 측위 서비스에서 점점 중요성이 높아지고 있습니다.

GEO 위성은 텔레비전이나 인터넷 등의 통신 및 방송 서비스에서 특히 중요합니다.

아시아태평양 원격 탐사 위성 시장 동향

위성의 소형화 수요 증가가 시장을 견인

소형 위성은 계산, 전자기기의 소형화, 패키징 기술의 진보를 활용하여 선진적 임무 수행 능력을 제공합니다.

아시아태평양 수요는 주로 중국, 일본, 인도가 견인하고 있으며, 이들 국가는 매년 가장 많은 소형 위성을 제조하고 있습니다. 기업과 초소형 위성 개발 프로젝트에 대한 지속적인 투자가 이 지역의 수익 성장을 밀어올릴 것으로 예측됩니다.

중국은 우주 기반의 능력 증진을 위해 많은 자원을 투자하고 있습니다. SpaceWish의 초소형 위성이 CZ-2C(3) 로켓으로 LEO에 발사되었습니다.

싱가포르는 초소형 위성 제조의 선두주자이며 과학 미션용으로 매년 여러 모델이 설계되고 있습니다. SpooQy-1 NanoSat은 싱가포르 국립대학의 양자기술센터(CQT)가 고안한 것으로 양자 얽힘의 물리 현상을 실증하기 위해서 설계되어 추후 우주 공간에서의 양자 통신과 2030년까지 200억 달러 상당의 투자를 불러올 가능성이 있습니다.

시장에서 투자 기회 증가는 우주 프로그램에 대한 지출을 촉진

아시아태평양에서 우주 관련 활동 증가를 고려하여 위성 제조업체는 급속히 상승하는 시장의 가능성을 이용하기 위해 생산 능력을 강화하고 있습니다. 중국은 시설의 강화를 포함해 2021-2025년까지 우주탐사의 우선순위를 발표했습니다.

2022년 일본의 예산안에 따르면 일본의 우주예산은 14억 달러를 돌파하였으며, 이는 11개 부처의 우주활동에 대한 투자가 포함되어 있습니다. 인도는 제3자 발사 서비스의 세계적 리더이며 새로운 발사 플랫폼의 연구 개발 프로그램도 여러가지 진행 중입니다.

한국의 우주계획은 타국이 핵심기술 이전에 소극적이기 때문에 진전이 늦어지고 있습니다. 아시아태평양 국가들은 최근 우주 기술에 대한 투자를 시작하고 있습니다.

아시아태평양 원격 탐사 위성 산업 개요

아시아태평양의 원격 탐사 위성 시장은 상당히 통합되어 있으며 상위 5개 기업에서 96.77%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

위성의 질량

위성의 소형화

우주 개발에의 지출

규제 프레임워크

호주

중국

인도

일본

뉴질랜드

싱가포르

한국

밸류체인과 유통채널 분석

제5장 시장 세분화

위성 질량

10-100kg

100-500kg

500-1,000kg

10kg 이하

1,000kg 이상

궤도 클래스

GEO

LEO

MEO

위성 서브시스템

추진 하드웨어와 추진제

위성 버스 및 서브시스템

태양전지 어레이와 전원 하드웨어

구조, 하네스, 기구

최종 사용자

상업

군사 및 정부

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Airbus SE

Axelspace Corporation

Chang Guang Satellite Technology Co. Ltd

China Aerospace Science and Technology Corporation(CASC)

Esri

GomSpaceApS

IHI Corp

ImageSat International

Indian Space Research Organisation(ISRO)

Japan Aerospace Exploration Agency(JAXA)

Korea Aerospace Research Institute(KARI)

Lockheed Martin Corporation

Maxar Technologies Inc.

Mitsubishi Heavy Industries

Northrop Grumman Corporation

Planet Labs Inc.

Spire Global, Inc.

Thales

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The Asia-Pacific Remote Sensing Satellites Market size is estimated at 22.05 billion USD in 2025, and is expected to reach 43.4 billion USD by 2030, growing at a CAGR of 14.51% during the forecast period (2025-2030).

LEO satellites are significantly driving market demand

The Asia-Pacific region has seen a significant increase in the demand for satellite buses to accommodate a wide range of satellite orbits, including low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary orbit (GEO).

LEO satellites have become increasingly popular for various applications, including Earth observation, weather forecasting, and communication. The demand for LEO satellites has been particularly strong in China, where companies such as Spacety and Chang Guang Satellite Technology Co. Ltd are offering satellite buses for LEO missions. China has been active in this market with the launch of its Gaofen series satellites.

MEO satellites have become increasingly important for global navigation and positioning services such as GPS and Galileo. In the Asia-Pacific region, Japan has been a leader in this field, with the launch of the Michibiki series of MEO navigation satellites. China has also been investing in MEO satellites with the launch of the Beidou system.

GEO satellites are particularly important for communication and broadcasting services, such as television and the Internet. The demand for GEO satellites has been particularly strong in India, where companies such as ISRO and Antrix Corporation Ltd have been developing advanced satellite buses for communication missions. China has also been investing heavily in GEO satellites, with the launch of the Zhongxing series of satellites.

Rising demand for satellite miniaturization is driving the market

Miniature satellites leverage advances in computation, miniaturized electronics, and packaging to produce sophisticated mission capabilities. As microsatellites can share the ride to space with other missions, they offer a considerable reduction in launch costs.

The demand from Asia-Pacific is primarily driven by China, Japan, and India, which manufacture the largest number of small satellites annually. Though the launches have decreased over the last three years, the satellite market in these countries continues to hold huge potential. Ongoing investments in startups and nano and microsatellite development projects are expected to boost the revenue growth of the region. From 2017 to 2022, more than 550 nano and microsatellites were placed into orbit by various players in the region.

China is investing significant resources toward augmenting its space-based capabilities. The country has launched the largest number of nano and microsatellites in the Asia-Pacific region. In April 2022, Chinese startup SpaceWish's nanosatellite was launched into LEO aboard the CZ-2C (3) rocket. XINGYUAN-2 is a 6U remote sensing CubeSat that weighs approximately 7.5 kg.

Singapore has become a pioneer in the fabrication of nanosatellites, with several models being designed each year for scientific missions. The SpooQy-1 NanoSat, which was launched by JAXA in 2019, is the brainchild of the Centre for Quantum Technologies (CQT) at the National University of Singapore. The 3,000 cm3 satellite weighs just 2.6 kg and is designed to demonstrate the physical phenomenon of quantum entanglement in space, which, if proven, may unlock quantum communications in space and attract investments worth USD 20 billion by 2030.

Rising investment opportunities in the market are driving spending on space programs

Considering the increase in space-related activities in the Asia-Pacific region, satellite manufacturers are enhancing their production capabilities to tap into the rapidly emerging market potential. The prominent countries in Asia-Pacific that possess a robust space infrastructure are China, India, Japan, and South Korea. China National Space Administration announced space exploration priorities for the 2021-2025 period, including enhancing national civil space infrastructure and ground facilities. As a part of this plan, the Chinese government established China Satellite Network Group Co. Ltd for the development of a 13,000-satellite constellation for providing satellite internet services.

In 2022, according to the draft budget of Japan, the space budget of the country was over USD 1.4 billion, which included investment for space activities of 11 government ministries. These activities include the development of the H3 rocket, Engineering Test Satellite-9, and the nation's Information Gathering Satellite (IGS) program. India has become a global leader in third-party launch services and has several ongoing R&D programs for new launch platforms. The proposed budget for India's space programs for FY22 was USD 1.83 billion.

South Korea's space program has seen slow progress as other countries are reluctant to transfer core technologies. In 2022, the Ministry of Science and ICT announced a space budget of USD 619 million for manufacturing satellites, rockets, and other key space equipment. Many Southeast Asian countries have also recently started investing in space technology. As of March 2021, the Indonesian government had secured USD 545 million to continue the fabrication of the Very High Throughput Satellite (SATRIA), using a Public Private Partnership (PPP) scheme.

Asia-Pacific Remote Sensing Satellites Industry Overview

The Asia-Pacific Remote Sensing Satellites Market is fairly consolidated, with the top five companies occupying 96.77%. The major players in this market are Axelspace Corporation, Chang Guang Satellite Technology Co. Ltd, China Aerospace Science and Technology Corporation (CASC), Japan Aerospace Exploration Agency (JAXA) and Korea Aerospace Research Institute (KARI) (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Satellite Mass

4.2 Satellite Miniaturization

4.3 Spending On Space Programs

4.4 Regulatory Framework

4.4.1 Australia

4.4.2 China

4.4.3 India

4.4.4 Japan

4.4.5 New Zealand

4.4.6 Singapore

4.4.7 South Korea

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Satellite Mass

5.1.1 10-100kg

5.1.2 100-500kg

5.1.3 500-1000kg

5.1.4 Below 10 Kg

5.1.5 above 1000kg

5.2 Orbit Class

5.2.1 GEO

5.2.2 LEO

5.2.3 MEO

5.3 Satellite Subsystem

5.3.1 Propulsion Hardware and Propellant

5.3.2 Satellite Bus & Subsystems

5.3.3 Solar Array & Power Hardware

5.3.4 Structures, Harness & Mechanisms

5.4 End User

5.4.1 Commercial

5.4.2 Military & Government

5.4.3 Other

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 Airbus SE

6.4.2 Axelspace Corporation

6.4.3 Chang Guang Satellite Technology Co. Ltd

6.4.4 China Aerospace Science and Technology Corporation (CASC)