중동의 엔지니어링 플라스틱 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

Middle East Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1693825

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

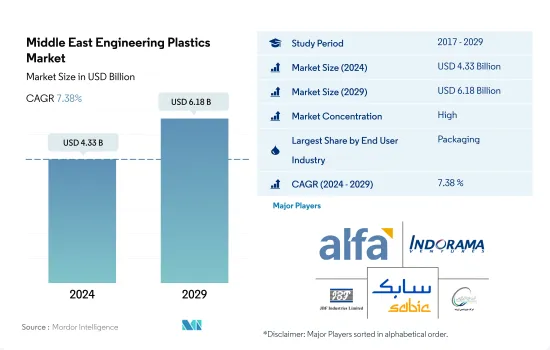

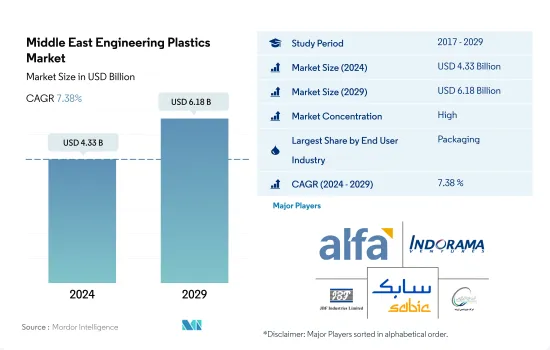

중동의 엔지니어링 플라스틱 시장 규모는 2024년에 43억 3,000만 달러에 달했고, 2029년에는 61억 8,000만 달러에 이르고, 예측 기간(2024-2029년)의 CAGR은 7.38%를 나타낼 것으로 예상됩니다.

엔지니어링 플라스틱 수요는 포장 산업이 주류로

중동은 2022년 엔지니어링 플라스틱의 세계 소비량의 3.5%를 차지했습니다.

중동 포장산업은 2022년 시장에서 가장 큰 점유율을 차지했는데, 이는 소비자가 편의식품과 온더고의 라이프스타일로 크게 이동하고 있는 것 외에도 레이디트윗 식품에 대한 선호 가 높아져 식품포장재료 수요를 견인하고 있기 때문입니다. 예측 기간 동안 CAGR은 7.32%를 나타낼 전망입니다. 플라스틱 포장의 생산량은 2022년 4,753킬로톤에 대해 2029년에는 6,765킬로톤에 이를 것으로 예측됩니다.

이 지역의 전기 및 전자산업은 엔지니어링 플라스틱에 있어서 가장 급성장하고 있는 산업입니다. IoT(사물인터넷) 디바이스 등의 기술 진보가 향후의 전자기기 수요를 견인할 것으로 예측됩니다. 아랍에미리트의 전기 및 전자 부문의 수익은 예측 기간(2023-2029년) 동안 8.96%의 연평균 성장률을 나타내고 2029년까지 730억 달러의 예상 시장 가치에 도달할 것으로 예상됩니다.

사우디아라비아의 포장·전자산업이 시장 수요를 끌어올립니다.

중동은 2022년 엔지니어링 플라스틱의 세계 소비량의 3.5%를 차지했습니다.

사우디아라비아는 2022년 엔지니어링 플라스틱 소비량에서 가장 큰 시장 점유율을 차지했습니다.

또한 사우디아라비아는 수익면에서도 급성장하고 있는 국가입니다. 국가의 전기 및 전자 산업으로 인해 예측 기간 동안 가치 측면에서 7.66 %의 연평균 성장률을 기록 할 것으로 예상됩니다. 전자 시장의 상승은 향후 EP 수요를 끌어올릴 것으로 예측됩니다.

아랍에미리트(UAE)은 전기 및 전자산업에 의해 2번째로 급성장하고 있는 국가입니다.

중동의 엔지니어링 플라스틱 시장 동향

정부와 민간기업에 의한 투자 확대

중동에서는 사우디아라비아가 전기 및 전자산업의 주요시장 중 하나로 급부상하고 있습니다. 따라서 이 지역의 전기 및 전자 제품 생산은 매출 기준으로 2017년부터 2019년까지 18%의 연평균 성장률을 기록했습니다.

2020년에는 COVID-19의 대유행으로 리모트 워크나 홈 엔터테인먼트용 소비자용 전자기기 제품 수요가 증가했습니다. 샤르네트워크를 통해 새로운 판매자를 발견할 수 있게 되었습니다.

전기 및 전자생산은 예측기간 중(2023-2029년)에 금액으로 8.51%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 동쪽에도 5G 무선 기술을 팔고 있습니다. 사우디아라비아는 비전 2030 구상에 따라 5G 네트워크를 도입했습니다.

중동의 엔지니어링 플라스틱 산업 개요

중동의 엔지니어링 플라스틱 시장은 상당히 통합되어 있으며 상위 5개 기업에서 91.59%를 차지하고 있습니다.

Rabigh Refining and Petrochemical Company(Petro Rabigh)

SABIC

Saudi Methacrylates Company(SAMAC)

Shahid Tondgooyan Petrochemical Company

Sipchem Company

Tabriz Petrochemical Company.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

The Middle East Engineering Plastics Market size is estimated at 4.33 billion USD in 2024, and is expected to reach 6.18 billion USD by 2029, growing at a CAGR of 7.38% during the forecast period (2024-2029).

Packaging industry to dominate the demand for engineering plastics

The Middle East accounted for 3.5% of the global consumption of engineering plastics in 2022. Engineering plastics find applications in several industries like packaging, automotive, electrical and electronics, and building and construction.

The Middle Eastern packaging industry occupied the largest share of the market in 2022, attributed to a significant shift of consumers toward convenience food and on-the-go lifestyles, along with an increase in preference for ready-to-eat food, driving the demand for food packaging materials. The emerging trend of online shopping from e-commerce websites also serves as a driving factor in the packaging industry. The market is expected to record a CAGR of 7.32% in terms of value during the forecast period. Plastic packaging production is expected to reach 6,765 kilotons by 2029 compared to 4,753 kilotons in 2022.

The region's electrical and electronics industry is the fastest-growing industry for engineering plastics. It is likely to record a CAGR of 9.91% in terms of value during the forecast period (2023-2029). Technological advancements like artificial intelligence, the advent of 5G, and IoT (Internet of Things) devices are expected to drive the demand for electronics in the future. The revenue from the electrical and electronics segment in the United Arab Emirates is expected to register a CAGR of 8.96% during the forecast period (2023-2029) and reach a projected market value of USD 73 billion by 2029. The United Arab Emirates is the fastest-growing country in the market, and it is expected to record a CAGR of 10.1% in terms of value, making it the fastest-growing country in the Middle East.

Packaging and electronics industry in Saudi Arabia to boost market demand

The Middle East accounted for 3.5% of the global consumption of engineering plastics in 2022. Engineering plastics find applications in several industries like automotive, electrical and electronics, building and construction, etc.

Saudi Arabia occupied the largest market share in terms of consumption of engineering plastics in 2022. This can be attributed to the packaging industry, which is likely to register a CAGR of 7.67% in terms of value during the forecast period. Packaging material consumption has increased due to increased demand for ready-to-eat convenience foods and the emerging trend of on-the-go lifestyles. The country's food and beverage industry is the largest in the Middle East, with a valuation of around USD 45 billion in 2021. The plastic packaging production volume in the country is projected to reach around 3.01 million tons in 2029 from 2.15 million tons in 2023.

Saudi Arabia is also the fastest-growing country in terms of revenue. It is predicted to register a CAGR of 7.66% in terms of value during the forecast period owing to the country's electrical and electronics industry. The rising electronics market will drive the demand for EP in the future. The consumer electronics industry in the country is projected to reach a market volume of around USD 6.73 billion by 2027 from USD 3.99 billion in 2023.

The United Arab Emirates is the second-fastest growing country owing to its electrical and electronic industry. As a result of technological advancements, the demand for electronics is expected to rise during the forecast period. The electronics industry in the country is projected to reach a market volume of around USD 3.32 billion by 2027 from USD 2.41 billion in 2023.

Middle East Engineering Plastics Market Trends

Growing investments from the government and private players

In the Middle East, Saudi Arabia is quickly emerging as one of the key markets for the electrical and electronics industry. Aside from the oil and gas industry, the country has a sizable consumer base and a broad range of industrial pursuits, contributing to the rapid annual increase in production for the electrical and electronics industry. Thus, electrical and electronics production in the region registered a CAGR of 18% from 2017 to 2019 in revenue terms.

In 2020, the demand for consumer electronics for remote working and home entertainment increased due to the COVID-19 pandemic. In 2020, Saudi Arabia registered the highest smartphone penetration rate, around 97%, in the world, which enabled approximately 60% of Saudi customers to discover new sellers through social networks. Saudi Arabia faced a higher rate of e-commerce growth, nearly 60% (between 2019 and 2020), mainly due to the pandemic. The revenue from electrical and electronics production increased by 1.8% compared to the previous year.

Electrical and electronic production is expected to witness a CAGR of 8.51% in value during the forecast period (2023-2029). The major driving component behind the growth is likely to be the growing investments from the government and the manufacturers like Samsung. Samsung has also been pitching its 5G wireless technology to the Middle East. Saudi Arabia implemented a 5G network in line with the Vision 2030 initiative. All such factors are expected to boost electronics production over the forecast period in the region.

Middle East Engineering Plastics Industry Overview

The Middle East Engineering Plastics Market is fairly consolidated, with the top five companies occupying 91.59%. The major players in this market are Alfa S.A.B. de C.V., IVL Dhunseri Petrochem Industries Private Limited (IDPIPL), JBF Industries Ltd, SABIC and Shahid Tondgooyan Petrochemical Company (sorted alphabetically).

4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

4.5 Regulatory Framework

4.5.1 Saudi Arabia

4.5.2 United Arab Emirates

4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Electrical and Electronics

5.1.5 Industrial and Machinery

5.1.6 Packaging

5.1.7 Other End-user Industries

5.2 Resin Type

5.2.1 Fluoropolymer

5.2.1.1 By Sub Resin Type

5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

5.2.1.1.3 Polytetrafluoroethylene (PTFE)

5.2.1.1.4 Polyvinylfluoride (PVF)

5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

5.2.1.1.6 Other Sub Resin Types

5.2.2 Liquid Crystal Polymer (LCP)

5.2.3 Polyamide (PA)

5.2.3.1 By Sub Resin Type

5.2.3.1.1 Aramid

5.2.3.1.2 Polyamide (PA) 6

5.2.3.1.3 Polyamide (PA) 66

5.2.3.1.4 Polyphthalamide

5.2.4 Polybutylene Terephthalate (PBT)

5.2.5 Polycarbonate (PC)

5.2.6 Polyether Ether Ketone (PEEK)

5.2.7 Polyethylene Terephthalate (PET)

5.2.8 Polyimide (PI)

5.2.9 Polymethyl Methacrylate (PMMA)

5.2.10 Polyoxymethylene (POM)

5.2.11 Styrene Copolymers (ABS and SAN)

5.3 Country

5.3.1 Saudi Arabia

5.3.2 United Arab Emirates

5.3.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 Alfa S.A.B. de C.V.

6.4.2 Celanese Corporation

6.4.3 Ghaed Basir Petrochemical Products Company (GBPC)