스페인의 데이터센터 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Spain Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693808

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

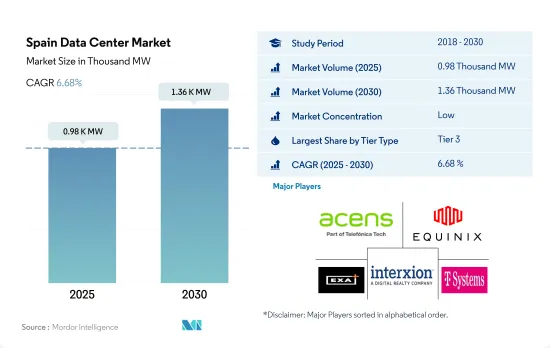

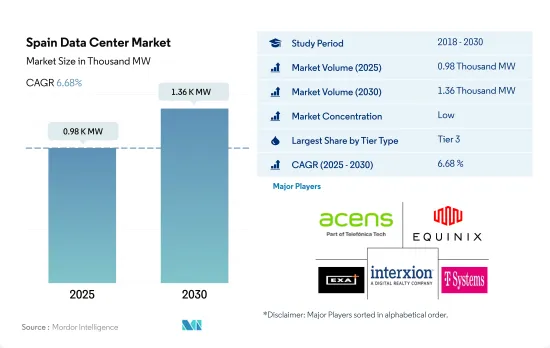

스페인의 데이터센터 시장 규모는 2025년 980MW에 달할 것으로 추정되고, CAGR 6.68%를 나타내 2030년에는 1,360MW에 이를 것으로 예측됩니다.

또한 2025년에는 9억 6,380만 달러의 코로케이션 수익을 달성하고, 2030년에는 17억 1,650만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 12.24%를 나타낼 것으로 전망됩니다.

Tier 3 데이터센터는 2023년에 수량 기준으로 대부분의 점유율을 차지했으며 예측 기간 동안 우위를 차지할 것으로 예측됩니다.

2023년, 스페인의 Tier 3 데이터센터의 IT 부하 용량은 481.89MW에 이르렀고, 그 후 CAGR 8.7%를 나타내 2029년에는 795.09MW를 넘을 것으로 예측됩니다. 한편, Tier 4 데이터센터는 CAGR 14.45%를 나타낼 전망입니다.

향후 몇 년 동안 Tier 1 및 2 시설은 점차 성장이 둔화되고 장기간의 부정기 정지로 인해 부정적인 성장을 보일 것으로 예측됩니다. 이러한 데이터센터는 Tier 3 및 Tier 4의 시설보다 저렴하지만, 그 능력의 낮음에서 최종 사용자는 점점 Tier 3과 Tier 4의 시설을 선택하게 되어 있습니다.

2029년에는 3단계와 4단계가 각각 58.8%와 40.5%의 점유율을 차지할 것으로 예측됩니다.

국내 디지털 결제 사용자 수는 2022년 3,235만 명에서 2027년까지 4,060만 명에 이를 것으로 예상되고 있습니다. 또한, 클라우드 기반의 서비스를 채용하는 기업이 늘어남에 따라, 최신 기술을 갖춘 코로케이션 스페이스를 제공하는 Tier 3과 Tier 4 시설 수요가 높아질 것으로 예측됩니다.

스페인의 데이터센터 시장 동향

스마트폰 소유율 상승과 앱 다운로드 수 증가가 시장 성장을 뒷받침

스페인의 스마트폰 사용자 수는 2022년에 4,251만명이었지만, 2029년에는 4,660만명에 달할 것으로 예상되며, 예측 기간 중 CAGR은 1.3%를 나타낼 것으로 전망됩니다.

앞으로 수년간 5G 기술이 스페인 전역에 보급되면 신기술을 이용할 수 있는 스마트폰을 가진 사람의 비율이 늘어날 것으로 예측됩니다. 스페인에는 4개의 통신 사업자가 있습니다. 모비스터(Movistar), 오렌지(Orange), Vodafone(Vodafone), 요이고(Yoigo)의 4개 회사는 5G 고객을 보유하고 있습니다. 5G 스마트폰과 5G요금 플랜에서 이러한 사업자의 네트워크를 이용하는 소비자는 9.6-10.6%의 시간을 5G 네트워크에 연결하여 보냈습니다.

팬데믹은 스페인의 디지털화로의 움직임을 가속화했습니다. 스페인인의 95.05%가 사용하는 소셜 미디어는 WhatsApp로 Instagram, Facebook, YouTube가 이에 이어졌습니다. 이러한 용도에 하루 3-4시간을 소비합니다. 비접촉 서비스를 유지하기 위해 공공기관과 민간 기업은 디지털 플랫폼으로 전환했습니다.

이 추세는 특히 금융 부문에서 두드러지며 스페인 사람들은 온라인 뱅킹에 대한 의존도를 높이고 있습니다. 예를 들어, 대유행 전 17.3%였던 은행 서비스 이용자의 36.4%가 현재는 온라인 뱅킹 용도를 매일 또는 거의 매일 이용하고 있습니다. 그 결과 스마트폰에서 발생하는 대량의 데이터로 인해 스페인의 데이터센터 수가 증가하고 있습니다.

FTTx 광대역과 광섬유 네트워크의 이용 증가가 시장 수요로 이어집니다.

동선 기반 인터넷 연결의 최대 속도는 62.8Mbps인 반면 광섬유 인터넷 연결의 최대 속도는 134.6Mbps입니다. 데이터센터의 고속화 노력의 목표는 보다 높은 네트워크 접속을 제공해, 대역폭 수요가 시시각각 변화하는 가운데, 단순하고 유연한 확장성을 실현하는 것입니다.

스페인에서는 2020년까지 DSL이 가장 널리 보급되었지만 그 이후에는 연결성이 떨어지고 있습니다. 2020년까지 84.9%의 가정이 FTTP 광대역 서비스에 액세스할 수 있게 되었으나, 이는 스페인 사업자가 FTTP 네트워크 인프라를 확대했기 때문에 FTTP 커버율은 4.6% 증가했습니다.

스페인의 광범위한 광섬유 네트워크의 대부분을 지배하는 것은 대형 통신 사업자 3사입니다. 하고 있기 때문에 스페인은 톱 클래스의 나라가 되고 있습니다.스페인의 국가 광대역 계획에서는 도시에서의 FTTP 커버율이 벌써 높은 것으로부터, 주로 농촌에 초점이 맞추어져 있어, 이것이 농촌의 FTTP 커버율과 확대의 원동력이 되고 있습니다.

스페인의 데이터센터 산업 개요

스페인의 데이터센터 시장은 세분화되어 있으며 상위 5개 기업에서 35.82%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 시장 전망

IT 부하 용량

바닥 공간 증가

코로케이션 수익

설치된 랙

랙 공간 활용

해저 케이블

제5장 주요 산업 동향

스마트폰 사용자수

스마트폰 1대당 데이터 트래픽

모바일 데이터 속도

광대역 데이터 속도

광섬유 접속 네트워크

규제 프레임워크

스페인

밸류체인과 유통채널 분석

제6장 시장 세분화

핫스팟

마드리드

기타 중동 및 아프리카

데이터센터의 규모

대규모

초대규모

중규모

메가규모

소규모

티어 유형

Tier 1 및 2

Tier 3

Tier 4

흡수량

비이용

이용

코로케이션 유형별

하이퍼스케일

소매

도매

최종 사용자별

BFSI

클라우드

전자상거래

정부

제조

미디어 및 엔터테인먼트

통신

기타

제7장 경쟁 구도

시장 점유율 분석

기업 상황

기업 프로파일

Acens Technologies SL

Adam Ecotech SA

Data4

Digital Data Centre Bidco SL(Nabiax)

Equinix Inc.

EXA Infrastructure

Global Switch Holdings Limited

Interxion(Digital Reality Trust Inc.)

NetActuate Inc.

T-Systems International GmbH

VPS House Technology Group LLC

Zenlayer Inc.

제8장 CEO에 대한 주요 전략적 질문

제9장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

세계 시장 규모와 DRO

정보원과 참고문헌

도표 목록

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

The Spain Data Center Market size is estimated at 0.98 thousand MW in 2025, and is expected to reach 1.36 thousand MW by 2030, growing at a CAGR of 6.68%. Further, the market is expected to generate colocation revenue of USD 963.8 Million in 2025 and is projected to reach USD 1,716.5 Million by 2030, growing at a CAGR of 12.24% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, and is expected to dominate through out the forecasted period

In 2023, the IT load capacity of tier 3 data centers in Spain is expected to reach 481.89 MW and then register a CAGR of 8.7% to surpass 795.09 MW by 2029. Conversely, tier 4 data centers are predicted to record a CAGR of 14.45%, reaching a capacity of 547.68 MW by 2029.

Over the coming years, facilities in tiers 1 and 2 will gradually slow down and exhibit negative growth, resulting from lengthy and irregular outages. Additionally, they possess a single channel for cooling and electricity, with a predicted uptime of 99.671%. Although these data centers are less expensive than tier 3 and tier 4 facilities, their reduced capability is prompting end users to increasingly opt for tier 3 and tier 4 facilities.

In 2029, tier 3 and tier 4 facilities are expected to hold major shares of 58.8% and 40.5%, respectively. The year 2023 will witness the highest demand for tier 3 facilities, which are expected to hold a market share of 65.8%. Owing to features like onsite service, power, and cooling redundancy, tier 3 data centers are the most popular. BFSI, telecom, media, and entertainment consumers are primarily using wholesale and hyperscale colocation facilities, driving significant tier 3 facility usage.

The number of digital payment users in the country is projected to reach 40.6 million by 2027, up from 32.35 million users in 2022. Tier 4 data centers are expected to experience significant growth over the coming years. Large businesses prefer tier 4 data centers due to their fault-tolerant capabilities, reduced downtime, and 99.99% uptime. Additionally, as more companies adopt cloud-based services, the demand for tier 3 and tier 4 facilities to offer colocation space with the latest technology will increase.

Spain Data Center Market Trends

Rising smartphone ownership and increase in number of app downloads boost the market growth

The total number of smartphone users in the country was 42.51 million in 2022, which is expected to reach 46.6 million by 2029, witnessing a CAGR of 1.3% during the forecast period. In Spain, digital usage is growing quickly. The swift uptake of the internet and mobile technology in a range of enterprises has had an impact on consumer behavior. Consumer spending in Spain was USD 802.79 billion in 2021, a 12.04% increase from 2020. Thus, more people can now buy smartphones, increasing the usage of smartphones.

Over the next several years, it is anticipated that when 5G technology is deployed throughout Spain, a greater proportion of people will have smartphones that can use the new technology. Spain has four operators: Movistar, Orange, Vodafone, and Yoigo, which have 5G customers. With a 5G smartphone and a 5G tariff plan, consumers on these operators' networks spent 9.6-10.6% of their time connected to a 5G network.

The pandemic accelerated Spain's move toward digitalization. WhatsApp was the social media platform 95.05% of Spaniards utilized, followed by Instagram, Facebook, and YouTube. They spent three to four hours a day on these applications. In order to maintain contactless services, public and private organizations switched to digital platforms, which increased the need for data center services in Spain.

This tendency has been especially noticeable in the financial sector, as Spaniards are becoming more dependent on online banking. For instance, compared to 17.3% before the pandemic, 36.4% of banking service users now utilize their online banking applications every day or virtually daily. As a result, the number of data centers in Spain has increased due to the large amount of data generated by smartphones.

Increase usage of FTTx broadband and fiber optic network lead to market demand

The maximum speed of a copper-based internet connection is 62.8 Mbps, whereas the maximum speed of a fiber-optic internet connection is 134.6 Mbps. Compared to the expected speed of 1,342 Mbps in 2029, the FTTx broadband data speed in 2022 stood at 159.2 Mbps. The goal of data centers' efforts to become faster is to provide higher network connections and simple and flexible scalability as bandwidth demands change on a moment-by-moment basis. More people use the internet, which necessitates data storage that is increasing in size and boosting the volume of processing facilities.

DSL remained the most prevalent technology in Spain till 2020, while its connectivity has decreased since then. The decline of DSL networks demonstrated that Spanish operators prioritize brand-new FTTP deployments over upgrading copper networks. The trend of declining DSL coverage is the result of both targeted decommissioning and a rise in the number of households. By 2020, 84.9% of homes had access to FTTP broadband services, owing to Spanish operators' expansion of their FTTP network infrastructure, which saw a 4.6% increase in FTTP coverage.

Three major operators control the majority of Spain's extensive fiber optic network. Telecom companies better fulfill users' rising bandwidth demands with a quicker network. In terms of gigabit-speed connectivity, Spain is among the top countries, owing to the ongoing improvements in FTTP availability. The Spanish national broadband plan focused primarily on rural areas, given an already high FTTP coverage in urban areas, which is the driving rural FTTP coverage and expansion.

Spain Data Center Industry Overview

The Spain Data Center Market is fragmented, with the top five companies occupying 35.82%. The major players in this market are Acens Technologies SL, Equinix Inc., EXA Infrastructure, Interxion (Digital Reality Trust Inc.) and T-Systems International GmbH (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 MARKET OUTLOOK

4.1 It Load Capacity

4.2 Raised Floor Space

4.3 Colocation Revenue

4.4 Installed Racks

4.5 Rack Space Utilization

4.6 Submarine Cable

5 Key Industry Trends

5.1 Smartphone Users

5.2 Data Traffic Per Smartphone

5.3 Mobile Data Speed

5.4 Broadband Data Speed

5.5 Fiber Connectivity Network

5.6 Regulatory Framework

5.6.1 Spain

5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

6.1 Hotspot

6.1.1 Madrid

6.1.2 Rest of Spain

6.2 Data Center Size

6.2.1 Large

6.2.2 Massive

6.2.3 Medium

6.2.4 Mega

6.2.5 Small

6.3 Tier Type

6.3.1 Tier 1 and 2

6.3.2 Tier 3

6.3.3 Tier 4

6.4 Absorption

6.4.1 Non-Utilized

6.4.2 Utilized

6.4.2.1 By Colocation Type

6.4.2.1.1 Hyperscale

6.4.2.1.2 Retail

6.4.2.1.3 Wholesale

6.4.2.2 By End User

6.4.2.2.1 BFSI

6.4.2.2.2 Cloud

6.4.2.2.3 E-Commerce

6.4.2.2.4 Government

6.4.2.2.5 Manufacturing

6.4.2.2.6 Media & Entertainment

6.4.2.2.7 Telecom

6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

7.1 Market Share Analysis

7.2 Company Landscape

7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).