유럽의 건설 보수보강용 화학제품 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Construction Repair and Rehabilitation Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693667

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

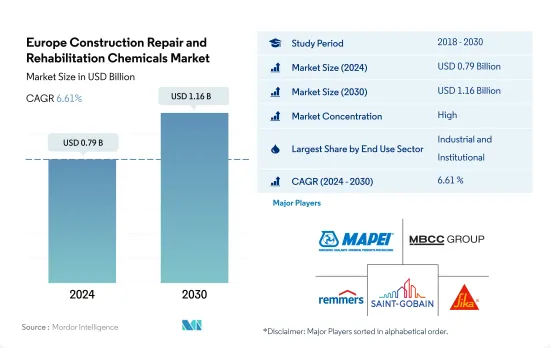

유럽의 건설 보수보강용 화학제품 시장 규모는 2024년에 7억 9,000만 달러로 추정되고, 2030년에는 11억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2030년)의 CAGR은 6.61%를 나타낼 것으로 예측됩니다.

상업 부문은 시장에서 가장 빠르게 성장하는 최종 용도 부문이 될 전망

2022년 유럽의 건설 보수보강용 화학제품 시장은 상업 및 산업 및 기관 건설 부문의 수요 증가에 힘입어 3.65%의 가치 성장을 경험했습니다.

산업 및 기관 부문은 2022년 유럽 건설 보수보강용 화학제품 시장의 47.03%를 차지하며 최대 소비처로 부상했습니다. 산업, 교육, 의료 등의 분야에 대한 투자가 증가함에 따라 이 지역의 바닥 면적은 2030년까지 114억 평방피트로 2023년보다 크게 증가할 것으로 예상됩니다

이 지역의 상업 부문은 건설 수리 및 재활 화학 물질의 가장 빠르게 성장하는 소비자가 될 것으로 예상되며 예측 기간 동안 7.59 %의 가장 높은 CAGR을 기록 할 것으로 예상됩니다. 이 부문의 기존 바닥 면적은 2023년에 비해 2030년까지 104억 제곱피트 증가할 것으로 예상됩니다.

프랑스 내 기존 제조 시설의 리노베이션에 대한 투자 증가로 인해 건설 수리 화학 제품에 대한 높은 수요 예측

건설 보수보강용 화학제품 시장에는 수리용 모르타르, 사출 그라우팅 재료, 섬유 래핑 시스템, 마이크로 콘크리트 모르타르 등 다양한 제품이 포함됩니다. 이러한 화학 물질은 건물과 구조물의 복원 및 수리에 매우 중요합니다.

2022년 유럽의 건설 수리 및 재활 화학 제품 시장은 전년 대비 3.65% 성장했습니다. 특히 러시아와 스페인이 각각 5.01%와 4.42%의 성장률로 선두를 차지했습니다.

2독일은 인프라 개발에 주력한 덕분에 2022년 건설 수리 및 재활 화학 제품 시장에서 가치 기준으로 22%의 높은 점유율을 차지하며 압도적인 1위를 차지했습니다. 예를 들어, 독일 국영 도로 회사인 아우토반은 교량, 도로, 항구 등 노후화된 인프라를 개선하기 위해 5억 7,800만 달러를 배정했습니다. 그 결과 건설 부문은 2021년에 비해 2022년에 4.51%의 가치 성장을 기록했습니다.

프랑스는 예측 기간 동안 건설 수리 및 재활 화학 제품 시장에서 가장 높은 7.36%의 연평균 성장률을 보일 것으로 예상됩니다. 프랑스는 2050년까지 탄소 배출 제로를 달성하겠다는 약속에 따라 건물의 열 개조에 327억 달러를 투자하기로 했습니다. 또한, 프랑스는 더 많은 산업 기업을 유치하기 위한 프랑스 릴랑스 계획에 따라 기존 제조 시설을 개선하고 있습니다. 그 결과 산업 건설 부문이 눈에 띄게 급증할 것으로 예상되며, 2030년에는 2022년에 비해 산업 건설 면적이 129억 제곱피트 증가할 것으로 전망됩니다.

유럽의 건설 보수보강용 화학제품 시장 동향

이탈리아, 스페인 등의 국가에서 상업용 건설 프로젝트가 증가하면서 상업 부문이 활성화될 것

2022년 유럽의 상업용 바닥면적은 사무실, 호텔, 리테일 몰과 같은 부동산에 대한 수요 증가로 인해 전년 대비 1.88% 증가했습니다.

유유럽의 상업 부문은 2020년의 모멘텀을 바탕으로 2021년에 바닥 면적이 1.70% 확장되었습니다. 이러한 성장은 이 부문의 디지털화 노력과 외국인 투자 급증에 힘입어 이루어졌습니다. 특히, 2021년 유럽 상업용 부동산에 대한 외국인 투자는 2,730억 유로에 달해 전년 대비 15% 증가했습니다.

앞으로 유럽의 상업용 건축 부문은 크게 성장할 것으로 예상되며, 예측 기간 동안 기존 연면적은 2.02%의 연평균 성장률을 기록할 것으로 예상됩니다. 이탈리아 밀라노 미국 총영사관 복합건물과 같은 주목할 만한 프로젝트는 2025년까지 6,500만 달러를 투자하여 완공될 예정입니다. 스페인의 아르테이소 오피스 빌딩 확장은 2024년 가동 예정인 180만 평방피트, 2억 6,000만 달러 규모의 프로젝트로 상업용 건설 환경을 강화할 예정입니다.

주택에 대한 수요 증가와 정부의 주택 투자로 인해 주거 부문이 활성화될 전망

2022년 유럽의 주거용 면적은 전년 대비 1.43% 증가할 것으로 예상됩니다. 이러한 성장은 도시 인구가 2021년 73.5%에서 전체 인구의 75%에 달하면서 도시화율이 상승한 데 기인한 것으로 볼 수 있습니다. 이러한 추세는 2023년에도 지속될 것으로 예상되며, 주거 면적은 1.68% 성장할 것으로 전망됩니다. 또한 유럽은 2023년에 헝가리, 아일랜드, 노르웨이, 폴란드에서 눈에 띄는 성장세를 보이며 주택 프로젝트 완공 건수가 2.7% 증가할 것으로 예상됩니다.

2018년부터 2021년까지 유럽은 주거용 연면적이 4.02% 증가했습니다. 2021년에만 이 지역은 주택 수요의 급증에 힘입어 약 45억 평방피트의 주거 면적이 추가되었습니다. 예를 들어, 프랑스는 2021년에 전년 대비 단독주택이 0.025%, 공동주택이 1.23% 증가했습니다.

유럽의 주거 면적은 예측 기간 동안 1.58%의 연평균 성장률을 기록하며 성장할 것으로 예상됩니다. 이러한 성장은 지속적인 주택 수요, 투자 증가, 정부 지원 정책에 힘입어 촉진되고 있습니다. 특히, 80억 달러의 투자로 뒷받침되는 영국의 저렴한 주택 프로그램과 같은 이니셔티브는 2026년까지 13만 채의 주택 공급을 목표로 하고 있습니다. 또한 유럽은 2030년까지 주거용 주택 개보수에 약 25억 유로를 투자할 것으로 예상됩니다.

유럽의 건설 보수보강용 화학제품 산업의 개요

유럽의 건설 보수보강용 화학제품 시장은 상위 5개 기업이 85.85%를 점유하는 등 상당히 통합되어 있습니다. 이 시장의 주요 업체는 MAPEI S.p.A., MBCC Group, Remmers Gruppe AG, Saint-Gobain 및 Sika AG (알파벳 순 정렬)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 용도 분야의 동향

상업

산업 및 시설

주거

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 용도 분야

상업

산업 및 시설

인프라

주거

서브제품

섬유 래핑 시스템

사출 그라우팅 재료

마이크로 콘크리트 모르타르

수리용 모르타르

철근 프로텍터

국가명

프랑스

독일

이탈리아

러시아

스페인

영국

기타 유럽

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Ardex Group

Fosroc, Inc.

MAPEI SpA

MBCC Group

MC-Bauchemie

Remmers Gruppe AG

RPM International Inc.

Saint-Gobain

Sika AG

Simpson Strong-Tie Company, Inc.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

시장 역학(DROs)

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Europe Construction Repair and Rehabilitation Chemicals Market size is estimated at 0.79 billion USD in 2024, and is expected to reach 1.16 billion USD by 2030, growing at a CAGR of 6.61% during the forecast period (2024-2030).

The commercial sector is expected to be the fastest-growing end use sector in the market

In 2022, the construction repair and rehabilitation chemicals market in Europe experienced a 3.65% growth in value, driven by increased demand from the commercial and industrial & institutional construction sectors. By 2023, the market was expected to hold a significant share of approximately 26.71% globally.

The industrial & institutional sector emerged as the largest consumer, accounting for 47.03% of Europe's construction repair and rehabilitation chemicals market in 2022. With investments increasing in sectors like industrial, education, and healthcare, the floor area in the region is projected to increase by 11.4 billion square feet by 2030, a significant increase from 2023. Consequently, the industrial & institutional sector is projected to witness an increase in value of USD 208 million by 2030 compared to 2023.

The commercial sector in the region is expected to be the fastest-growing consumer of construction repair and rehabilitation chemicals, recording the highest CAGR of 7.59% during the forecast period. The economy's rapid expansion has considerably impacted the need for commercial property to meet the demands of enterprises, such as offices, hotels, and retail shopping malls. The existing floor area for the sector is projected to increase by 10.4 billion sq. ft by 2030 compared to 2023. As a result, the construction repair and rehabilitation chemicals for the sector in the region are projected to reach USD 218 million in 2030 from USD 131 million in 2023.

High demand predicted for construction repair chemicals in France due to rising investments in the renovation of existing manufacturing units in the country

The market for construction repair and rehabilitation chemicals contains a range of products, such as repair mortars, injection grouting materials, fiber wrapping systems, and microcrete mortars. These chemicals are crucial for the restoration and repair of buildings and structures.

In 2022, the construction repair and rehabilitation chemicals market in Europe witnessed a 3.65% growth in value compared to the previous year. Notably, Russia and Spain led the pack with growth rates of 5.01% and 4.42%, respectively.

Germany dominated the construction repair and rehabilitation chemicals market in 2022, capturing a significant share of 22% by value, primarily driven by its focus on infrastructure development. For instance, Autobahn, a German government road firm, allocated USD 578 million to revamp the nation's aging infrastructure, including bridges, roads, and seaports. Consequently, the construction sector witnessed a 4.51% growth in value in 2022 compared to 2021.

France is poised to witness the highest CAGR of 7.36% in the construction repair and rehabilitation chemicals market during the forecast period. In line with its commitment to achieving zero carbon emissions by 2050, France has earmarked a significant investment of USD 32.7 billion for thermal renovations in buildings. Furthermore, under the France Relance plan, a move to attract more industrial firms, the country is revamping its existing manufacturing facilities. As a result, the industrial construction sector is projected to witness a notable surge, with the floor area for industrial construction expected to increase by 12.9 billion square feet in 2030 compared to 2022. This surge in industrial construction is anticipated to drive a CAGR of 8.48% in the value of the sector during the forecast period.

Europe Construction Repair and Rehabilitation Chemicals Market Trends

Rising commercial construction projects in countries, such as Italy, Spain, and others, will boost the commercial sector

In 2022, the commercial floor area in Europe saw a 1.88% uptick from the previous year, driven by heightened demand for properties like offices, hotels, and retail malls. This growth continued into 2023, with Europe witnessing a volume increase of around 1.2 billion sq. ft. This surge was primarily fueled by a rise in foreign direct investment (FDI), necessitating the development of new offices, warehouses, and retail spaces.

The commercial sector in Europe saw a 1.70% expansion in its floor area in 2021, building on the momentum from 2020. This growth was propelled by the sector's digitalization efforts and a surge in foreign investments. Notably, foreign investments in European commercial real estate reached EUR 273 billion in 2021, marking a 15% increase from the previous year. Germany's office real estate market also witnessed a notable uptick, with transactions amounting to EUR 30.5 billion, an 11% rise from 2020.

Looking ahead, the commercial construction sector in Europe is poised for significant growth, with the existing floor area projected to achieve a CAGR of 2.02% during the forecast period. Noteworthy projects, such as the Milan US Consulate General Complex in Italy, are set to be completed by 2025 with a planned investment of USD 65 million. The Arteixo Office Building Expansion in Spain, spanning 1.8 million sq. ft, valued at USD 260 million, slated for operation in 2024, is set to bolster the commercial construction landscape. Furthermore, as European consumers increasingly favor brick-and-mortar retail experiences, the construction of retail shopping malls is expected to surge. By 2030, the existing floor area is projected to expand by 10.44 billion sq. ft, a significant jump from 2022.

The increase in the demand for housing units and government investments in housing are likely to boost the residential sector

In 2022, the residential floor area in Europe saw a 1.43% volume increase from the previous year. This growth can be attributed to the rising urbanization rate, as the urban population reached 75% of the total population, up from 73.5% in 2021. This trend is expected to persist in 2023, with a projected growth of 1.68% in the residential floor area. Additionally, Europe is set to witness a 2.7% rise in housing project completions in 2023, with notable growth in Hungary, Ireland, Norway, and Poland.

Between 2018 and 2021, Europe witnessed a 4.02% increase in its residential floor area. In 2021 alone, the region added approximately 4.5 billion sq. ft of residential floor area, driven by a surge in housing demand. For instance, France saw a .025% rise in standalone houses and a 1.23% increase in collective housing units in 2021, compared to the previous year.

Europe's residential floor area is projected to grow, registering a CAGR of 1.58% during the forecast period. This growth is fueled by sustained housing demand, increased investments, and supportive government policies. Notably, initiatives like the UK's Affordable Homes Programme, backed by an USD 8 billion investment, aim to deliver 130,000 housing units by 2026. Moreover, Europe is expected to invest approximately EUR 2.5 billion in residential dwelling renovations by 2030.

Europe Construction Repair and Rehabilitation Chemicals Industry Overview

The Europe Construction Repair and Rehabilitation Chemicals Market is fairly consolidated, with the top five companies occupying 85.85%. The major players in this market are MAPEI S.p.A., MBCC Group, Remmers Gruppe AG, Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End Use Sector Trends

4.1.1 Commercial

4.1.2 Industrial and Institutional

4.1.3 Residential

4.2 Regulatory Framework

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

5.1 End Use Sector

5.1.1 Commercial

5.1.2 Industrial and Institutional

5.1.3 Infrastructure

5.1.4 Residential

5.2 Sub Product

5.2.1 Fiber Wrapping Systems

5.2.2 Injection Grouting Materials

5.2.3 Micro-concrete Mortars

5.2.4 Modified Mortars

5.2.5 Rebar Protectors

5.3 Country

5.3.1 France

5.3.2 Germany

5.3.3 Italy

5.3.4 Russia

5.3.5 Spain

5.3.6 United Kingdom

5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles

6.4.1 Ardex Group

6.4.2 Fosroc, Inc.

6.4.3 MAPEI S.p.A.

6.4.4 MBCC Group

6.4.5 MC-Bauchemie

6.4.6 Remmers Gruppe AG

6.4.7 RPM International Inc.

6.4.8 Saint-Gobain

6.4.9 Sika AG

6.4.10 Simpson Strong-Tie Company, Inc.

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)