아프리카의 특수 비료 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Africa Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693539

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

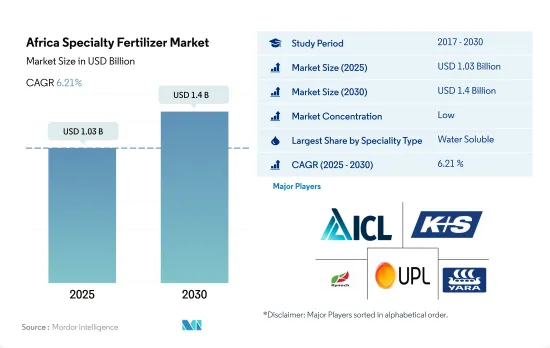

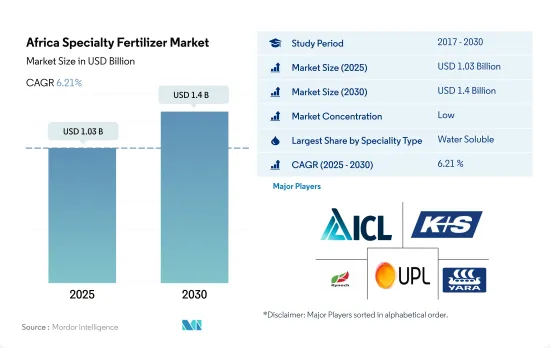

아프리카의 특수 비료 시장 규모는 2025년 10억 3,000만 달러로 추정되고, 2030년에는 14억 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 6.21%로 성장할 전망입니다.

기존의 비료보다 특수 비료를 사용하는 것이 다양한 이점이 있기 때문에 시장의 성장이 촉진될 것으로 예상됩니다.

2022년에는 방출 조절 비료(CRF)가 특수 비료 시장에서 7.4%의 점유율을 차지했습니다. CRF의 꾸준한 성장은 기존의 비료에 대한 명확한 이점과 효율적인 농법에 대한 의식이 높아지기 때문입니다. CRF는 장기간에 걸쳐 서서히 양분을 방출하므로 식물에 안정적인 양분 공급을 보장합니다. 이 때문에 양분의 낭비가 억제될 뿐만 아니라 기존의 비료에 흔히 발생하는 용출이나 증발의 위험도 최소화됩니다.

수용성 비료 시장 점유율은 47.8%로 2022년 특수 비료 시장에서 2위를 차지했습니다. 수용성 비료의 사용은 건강한 식물의 재배에 필요한 물과 비료를 모두 줄일 가능성을 보여줍니다.

액체 비료 시장은 관개 시스템의 진보와 수경 재배 및 아쿠아포닉스와 같은 고급 재배 기술의 채택 증가에 힘입어 성장을 시도하고 있습니다. 액체 비료 시장 가치는 2023-2030년간 CAGR 5.8%가 될 것으로 예측됩니다.

완효성 비료의 채용은 농가에게 경제적인 메리트뿐만 아니라, 절수, 질소의 휘발 및 용출의 방지, 비료 취급의 노력 경감 등 환경면에서의 메리트도 가져옵니다. 이러한 요인에 의해 2023-2030년 사이에 완효성 비료 시장가치는 5.4% 성장할 것으로 예상됩니다.

정확한 영양분 방출, 시비량 감소, 농민들의 경제적 이점 등 특수 비료의 장점을 감안할 때 특수 비료 시장은 향후 수년간 성장할 태세를 마련하고 있습니다.

정부의 이니셔티브와 생산성 향상에 주력하는 농가들이 시장 성장을 뒷받침할 전망

2022년, 나이지리아는 아프리카의 특수 비료 시장에서 27.0%의 압도적인 금액 점유율을 차지했습니다. 이 나라의 농업부문은 복잡한 토지소유권 문제, 불충분한 관개 인프라, 기후 변화의 악영향, 최첨단 농업기술의 단계적 도입 등의 과제에 직면하면서도 정부의 이니셔티브에 힘입어 시장의 성장을 이루어 왔습니다. 이들은 농업 진흥 정책(APP), 나이지리아 아프리카 무역 투자 촉진 프로그램, 국가 농업 기술 및 혁신 계획(NATIP), 앵커 차입인 프로그램(ABP) 등이 있어 모두 농업 생산성 향상에 도움이 되고 있습니다.

남아프리카는 대륙에서 가장 선진적이고 생산성이 높고 다양성이 풍부한 농업지역입니다. 2022년에는 그 견조한 농업 부문이 아프리카의 특수 비료 시장 전체의 37.0%라는 큰 점유율을 차지했습니다. 이 시장은 예측 기간 동안 CAGR 6.7%를 나타낼 것으로 예상됩니다. 이러한 성장이 예상되는 것은 보다 효율적인 비료 솔루션을 채택함으로써 장기간 가뭄이나 폭염 등 기후 관련 위험의 영향을 줄일 필요성이 높아지고 있는 것이 주요 요인입니다.

아프리카의 특수 비료 시장은 인구의 급증, 경지 감소, 기존 농지에서의 수량 향상이 급무인 것, 지역 전체에서 농업 생산성을 향상시키는 노력이 이루어지고 있는 것 등이 배경에 있으며 확대가 전망되고 있습니다.

아프리카 특수 비료 시장 동향

국내 수요가 증가함에 따라 가까운 미래에 농업 생산이 두배로 늘어날 것으로 보입니다.

아프리카의 농업 생태계 구역은 연 2회 강우가 있는 밀생한 열대우림에서 강우량이 적은 건조한 사막까지 다양합니다. 2022년에는 이 작물의 재배면적은 2억 2,480만 헥타르에 이르고, 이 지역의 농지의 95% 이상을 차지하고 있습니다. 가격 억제로 이어지는 옥수수의 초과 재고로 인해, 남아프리카의 옥수수 농가는 2018-2019년 시즌에 면적을 10% 축소해 210만 헥타르로 했습니다. 이 시프트에 의해 생산자는 기름 작물, 특히 대두에 더 많은 밭을 할당하게 되어, 그 결과 2018-2019년의 아프리카 전체의 옥수수 재배는 감소했습니다.

나이지리아가 아프리카 최대의 수수 생산국이며, 에티오피아가 잇따르고 있습니다. 수수는 가뭄과 홍수 내성으로 알려져 있으며, 다양한 토양 조건에서 자랍니다.

케냐, 소말리아, 에티오피아의 대부분은 심각한 식량 부족의 위기와 싸우고 있습니다. 과거 10년간, 아프리카의 농업과 경작지가 계속 확대되고 있음에도 불구하고, 식량 수입에 대한 지출은 3배 가까워지고 있습니다.

유채는 질소 소비량이 가장 많은 작물

유채는 칼륨과 인의 시용률이 가장 높고 각각 162.4kg/헥타르와 281.7kg/헥타르를 차지합니다. 이 우위성은 밭작물 전용의 광대한 토지 면적에 기인하고 있습니다.

나이지리아의 기니 사바나는 옥수수 생산에 적합한 환경 조건을 제공합니다. 밭작물은 경작, 잎 면적의 확대, 곡물의 형성, 충전, 단백질 합성의 촉진 등, 질소에는 복수의 이점이 있기 때문에 질소 시용이 우선됩니다.

1차 영양소는 작물의 생육에 불가결하며, 토양의 고갈이나 질소의 용출이 우려되기 때문에 1차 영양소의 시용률은 향후 수년간 크게 성장할 것으로 예상됩니다.

아프리카 특수 비료 산업 개요

아프리카의 특수 비료 시장은 단편화되어 있으며 상위 5개사에서 29.76%를 차지하고 있습니다. 이 시장 주요 기업은 ICL Group Ltd, K+S Aktiengesellschaft, Kynoch Fertilizer, UPL Limited, Yara International ASA(알파벳순) 입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

주요 작물의 작부 면적

밭 작물

원예 작물

평균 양분 시용률

미량 영양소

밭 작물

원예 작물

1차 영양소

밭 작물

원예 작물

2차 다량 영양소

밭 작물

원예 작물

관개 농지

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

스페셜리티 유형

CRF

폴리머 코트

폴리머 유황 코팅

기타

액체 비료

SRF

수용성

시비 모드

시비

엽면 살포

토양

작물 유형

밭 작물

원예 작물

잔디 및 관상용

생산국

나이지리아

남아프리카

기타 아프리카

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Gavilon South Africa(MacroSource, LLC)

Haifa Group

ICL Group Ltd

KS Aktiengesellschaft

Kynoch Fertilizer

UPL Limited

Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Africa Specialty Fertilizer Market size is estimated at 1.03 billion USD in 2025, and is expected to reach 1.4 billion USD by 2030, growing at a CAGR of 6.21% during the forecast period (2025-2030).

The various advantages of using specialty fertilizers over conventional fertilizers is expected to bolster the growth of the market

In 2022, controlled-release fertilizers (CRFs) held a 7.4% share of the specialty fertilizer market. The steady growth of CRFs can be attributed to their distinct advantages over traditional fertilizers and the increasing awareness of efficient agricultural practices. CRFs gradually release nutrients over an extended period, ensuring a consistent nutrient supply to plants. This not only reduces nutrient wastage but also minimizes the risk of leaching or evaporation, which is common with conventional fertilizers.

Water-soluble fertilizers, with a 47.8% market share, ranked second in the specialty fertilizer market in 2022. The use of water-soluble fertilizers has shown potential in reducing both water and fertilizer requirements for cultivating healthy plants.

The liquid fertilizer market is poised for growth, propelled by advancements in irrigation systems and the rising adoption of advanced cultivation techniques such as hydroponics and aquaponics. The market value of liquid fertilizers is projected to witness a CAGR of 5.8% during 2023-2030.

The adoption of slow-release fertilizers offers farmers not only economic benefits but also environmental advantages, such as water conservation, prevention of nitrogen volatilization and leaching, and reduced labor in fertilizer handling. These factors are expected to drive a 5.4% growth in the market value of slow-release fertilizers during 2023-20230.

Given the benefits of specialty fertilizers, including precise nutrient release, reduced application rates, and economic advantages for farmers, the specialty fertilizer market is poised for growth in the coming years.

Government initiatives and farmers' focus on increasing productivity are expected to bolster the growth of the market

In 2022, Nigeria held a commanding 27.0% value share in the African specialty fertilizer market. The country's agricultural sector, while facing challenges such as complex land tenure issues, inadequate irrigation infrastructure, the adverse effects of climate change, and the gradual adoption of cutting-edge agricultural technologies, has seen growth in the market supported by government initiatives. These include the Agriculture Promotion Policy (APP), the Nigeria-Africa Trade and Investment Promotion Programme, the National Agricultural Technology and Innovation Plan (NATIP), and the Anchor Borrowers Program (ABP), all of which have been instrumental in enhancing agricultural productivity.

South Africa distinguishes itself as the continent's most advanced, productive, and diverse agricultural region. In 2022, its robust agricultural sector held a substantial 37.0% share of the total African specialty fertilizer market. The market is expected to record a CAGR of 6.7% during forecast period. This anticipated growth is largely due to the increasing need to mitigate the effects of climate-related risks, such as prolonged droughts and intense heat waves, by adopting more efficient fertilizer solutions.

The African specialty fertilizer market is set to expand, driven by a rapidly growing population, the diminishing availability of arable land, the urgent necessity to improve yields on existing farmland, and concerted efforts to enhance agricultural productivity across the region. Thus, the market is forecasted to witness a CAGR of 6.0% from 2023 to 2030.

Africa Specialty Fertilizer Market Trends

The rising domestic demand will lead to double the agricultural production in the near future

The agro-ecological zones in Africa span from dense rainforests with bi-annual rainfall to arid deserts with minimal precipitation. Key field crops in the region include corn, sorghum, wheat, and rice. In 2022, the cultivation area for these crops reached 224.8 million hectares, accounting for over 95% of the region's agricultural land. In response to a surplus of corn stocks leading to price suppression, South African corn farmers scaled back their planting by 10% to 2.1 million hectares in the 2018-19 season. Consequently, corn production in the country dipped by 11% from 13 million to 12 million tonnes, and exports fell from 2.5 million to 1 million tonnes. This shift prompted producers to allocate more of their fields to oilseed crops, particularly soybeans, resulting in an overall decline in corn cultivation across Africa in 2018-2019.

Nigeria takes the lead as the largest sorghum producer in Africa, closely followed by Ethiopia. Sorghum, accounting for 50% of the total cereal output, dominates about 45% of Nigeria's cereal crop land. Known for its drought and waterlogging tolerance, sorghum thrives in diverse soil conditions. These attributes position sorghum as the go-to staple crop in Africa's drier regions, ensuring both food and income security.

Kenya, Somalia, and significant parts of Ethiopia are grappling with the looming specter of severe food shortages. Over the past decade, Africa's spending on food imports has nearly tripled, even as its agricultural industry and cultivated land have continued to expand.

Rapeseed is the highest nitrogen consuming crop

Rapeseed crops have the highest potassium and phosphorous application rates, accounting for 162.4 kg/hectare and 281.7 kg/hectare, respectively. Meanwhile, the average nitrogen application rate for field crops in Africa stands at 364.9 kg/hectare. In 2022, field crops in Africa accounted for 87.1% of the total primary nutrient consumption, which amounted to 556.1 thousand metric tons. This dominance can be attributed to the extensive land area dedicated to field crops. Specifically, the average nutrient application rates for nitrogen, phosphorous, and potassium in these crops were 223.2 kg/ha, 125.3 kg/ha, and 155.3 kg/ha, respectively.

The Guinea savannas in Nigeria offer favorable environmental conditions for maize production. However, despite this potential, farmers in the region struggle with low yields. The primary culprits are soil degradation and nutrient depletion, primarily nitrogen, resulting from intensified land use. Field crops prioritize nitrogen application due to its multiple benefits, including promoting tillering, leaf area development, grain formation, filling, and protein synthesis. Nitrogen also plays a crucial role in enhancing both grain yield and quality.

Given that primary nutrients are vital for crop growth and with concerns over soil depletion and nitrogen leaching, the application rates for primary nutrients are expected to witness significant growth in the coming years.

Africa Specialty Fertilizer Industry Overview

The Africa Specialty Fertilizer Market is fragmented, with the top five companies occupying 29.76%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Kynoch Fertilizer, UPL Limited and Yara International ASA (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Acreage Of Major Crop Types

4.1.1 Field Crops

4.1.2 Horticultural Crops

4.2 Average Nutrient Application Rates

4.2.1 Micronutrients

4.2.1.1 Field Crops

4.2.1.2 Horticultural Crops

4.2.2 Primary Nutrients

4.2.2.1 Field Crops

4.2.2.2 Horticultural Crops

4.2.3 Secondary Macronutrients

4.2.3.1 Field Crops

4.2.3.2 Horticultural Crops

4.3 Agricultural Land Equipped For Irrigation

4.4 Regulatory Framework

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)