남미의 미량영양소 비료 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

South America Micronutrient Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693536

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

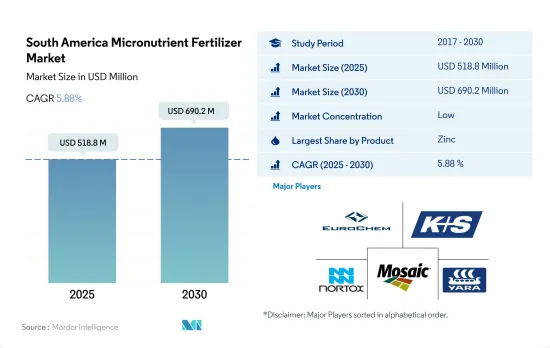

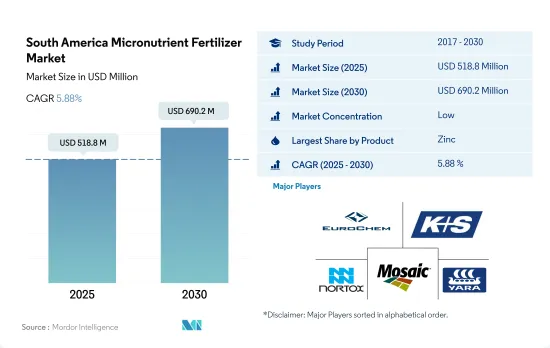

남미의 미량영양소 비료 시장 규모는 2025년에 5억 1,880만 달러, 2030년에는 6억 9,020만 달러에 이르고, 예측 기간(2025-2030년)의 CAGR은 5.88%를 나타낼 전망입니다.

작물 수율을 최적화하기 위해 결핍증을 다루어야 하기 때문에 이 지역에서는 아연에 대한 수요가 높습니다.

미량영양소는 세포벽 개발, 꽃가루 생성, 발아, 엽록소 생산, 질소 고정, 단백질 합성 등 많은 식물의 대사 활동에 필수적입니다.

미량영양소 비료 중에서 철은 2022년에 이 지역에서 가장 많이 사용되는 미량영양소 비료 중 하나입니다.

미량영양소 비료로서의 아연의 용도는 철에 이어 이 지역에서 가장 높습니다. 아연 결핍증은 이 지역, 특히 남미 북서부에서 널리 문제가 되고 있습니다.

콩과 밀의 재배는 이 지역의 농지 전체의 약 61.13%를 차지하고 있습니다. 이 2개의 작물은 망간 결핍증이 될 가능성이 높습니다.

니켈, 코발트, 셀레늄, 염화물은 기타 미량영양소입니다.

대부분의 미량영양소는 토양에서 사용할 수 있음에도 불구하고, 그 대부분은 성질상 이동성이 없고, 식물이 섭취할 수 없습니다.그러므로, 미량영양소 비료 수요는 이 지역에서 증가하고 있습니다.

토양 영양 부족이 브라질의 주요 시장 점유율로 이어집니다.

브라질은 남미의 미량영양소 비료 시장을 독점하고, 2022년에는 3억 3,170만 달러에 이르렀고, 전체 시장의 약 60.6%를 차지했습니다. 부문은 2017-2022년까지 약 14.8% 증가한 재배면적 증가로 2030년 말까지 3억 8,220만 달러로 증가할 것으로 예측되고 있습니다.

2022년 아르헨티나의 미량영양소 비료 시장은 밭작물이 97.7% 시장 매출 점유율을 차지했습니다. 우모로코시에서 이들을 합치면 작물 총 면적의 97.7%를 차지합니다. 한편, 아르헨티나의 원예 작물에 의한 미량영양소 비료의 소비는 2022년에 284만 달러로 평가되어, 2030년에는 390만 달러에 달할 것으로 예측되고 있습니다.

농업 종사자는 고품질의 농산물과 더 나은 수율을 달성하기 위해 작물에 미량영양소 비료를 채용하고 있습니다. 붕소, 몰리브덴의 토양 미량영양소의 결핍이 주목 받았습니다.

남미의 미량영양소 비료 시장 동향

자급 자족을 향한 정부의 대처가 밭작물의 재배 확대에 크게 공헌

남미의 농작물 재배면적은 2017년 1억1,160만ha에서 2022년에는 1억2,610만ha로 12.8%의 성장을 보였습니다. 경작 면적의 확대는 이 지역의 비료 수요를 밀어 올릴 것으로 예측됩니다. 에어를 차지해 아르헨티나가 29.3%로 이어집니다.대두 생산과 수출의 세계적 리더로 알려진 브라질의 대두 생산량은 2021년에 1억 3,500만 톤 가까이에 이르렀습니다.이 중 82%에 해당하는 대두

남미에서는 브라질과 아르헨티나가 재배면적의 64.4%, 26.1%를 차지하고, 대두재배의 정점에 군림하고 있습니다. 이것은 광범위하게 영향을 미치고, 대두를 중심으로 하는 중요한 여름 작물의 수확과 수송의 양쪽 모두에 지장을 초래하고 있습니다.

왕성한 세계 수요와 양호한 수익성에 힘입어 머코수르 지역의 대두 재배는 급증하고 있습니다.

2022년 미량영양소 중에서 가장 평균 살포량이 많은 것은 망간으로 약 12.2kg/헥타르입니다.

남미의 토양은 옥소졸과 울티졸로 차지되고 있습니다.옥소졸은 풍화가 진행되고 있어 질감이 균일하고, 철이나 알루미늄의 산화물이 많다고 하는 특징이 있어, 울티졸은 풍화는 진행되지 않지만 산성이 강하다는 대조적인 토양입니다.그러나, 양의 토양 따라서 작물 수율을 최적화하기 위해서는 미량영양소의 보급이 필요합니다.

2022년, 농작물에서 미량영양소 비료의 평균 시용량은 4.3kg/헥타르였습니다., 2022년의 평균 시용량이 12.2kg/헥타르이며, 미량영양소 중에서는 톱입니다. 늘어나기 위해, 천수 벼나 저지벼에서는 그다지 볼 수 없습니다.

남미의 주요 농작물인 유채종은 다른 작물에 비해 더 많은 미량영양소를 필요로 합니다. 스의 작물 영양이 중시되게 되어, 전체적인 수량에 있어서 미량영양소가 지극히 중요한 역할을 하는 것으로부터, 미량영양소의 시용은 향후 수년에 증가할 것으로 예측됩니다.

남미의 미량영양소 비료 산업 개요

남미의 미량영양소 비료 시장은 세분화되어 있으며 상위 5개 기업에서 28.08%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

주요 작물의 작부 면적

밭작물

원예작물

평균 양분 시용률

미량영양소

밭작물

원예작물

관개 설비가 있는 농지

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

제품

붕소

구리

철

망간

몰리브덴

아연

기타

적용방법

시비

잎면 살포

토양

작물 유형

밭작물

원예작물

잔디 및 관상용

생산국

아르헨티나

브라질

기타 남미

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

BMS Micro-Nutrients NV

EuroChem Group

Grupa Azoty SA(Compo Expert)

Haifa Group

ICL Group Ltd

Inquima LTDA

KS Aktiengesellschaft

Nortox

The Mosaic Company

Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

SHW

영문 목차

영문목차

The South America Micronutrient Fertilizer Market size is estimated at 518.8 million USD in 2025, and is expected to reach 690.2 million USD by 2030, growing at a CAGR of 5.88% during the forecast period (2025-2030).

The demand for zinc is higher in the region due to the need to address deficiency to optimize crop yield

Micronutrients are vital for many plant metabolic activities, such as cell wall development, pollen creation, germination, chlorophyll production, nitrogen fixation, and protein synthesis. Micronutrient fertilizers account for less than two percent of the total fertilizer market value, which amounted to about USD 547.7 million in 2022.

Among micronutrient fertilizers, iron is one of the most commonly used micronutrient fertilizer in the region in 2022. Iron accounted for about 8.5% of the total micronutrient fertilizer market value, amounting to about USD 46.6 million in 2022. Iron is a component of many enzymes associated with energy transfer, nitrogen reduction and fixation, and lignin formation.

The application of zinc as a micronutrient fertilizer is the highest in the region, after iron. Zinc deficiency is a widespread problem in the region, particularly in the northwestern region of South America. Zinc accounts for about 27.5% of the total micronutrient fertilizer market value, which amounted to about USD 150.5 million in 2022.

Soybean and wheat cultivation accounts for about 61.13% of the total agricultural land in the region. These two crops are most likely to suffer from manganese deficiency. Manganese accounted for about 3.7% of the total micronutrient fertilizer market value in 2022.

Nickel, cobalt, selenium, and chloride are the other micronutrients. The total other micronutrient segment accounts for 11.8% of the region's total micronutrient fertilizer market value, which amounted to about USD 64.6 million in 2022.

Even though most micronutrients are available in soils, most are immobile in nature and not available for plant uptake. Hence, the demand for micronutrient fertilizers is increasing in the region.

Nutrient deficiencies in the country's soils translate to a major market share for Brazil

Brazil dominated the South American micronutrient fertilizer market, accounting for about 60.6% of the total market value, amounting to USD 331.7 million in 2022. The Brazilian micronutrient fertilizer market segment is anticipated to increase to USD 382.2 million by the end of 2030, owing to the growing cultivation area, which increased by about 14.8% from 2017 to 2022.

Field crops dominated the Argentine micronutrient fertilizer market with a 97.7% market value share in 2022. This dominance was attributed to the larger area occupied by field crops in the country. Major field crops grown in Argentina are soybean, wheat, and maize, which together account for 97.7% of the total crop area. Meanwhile, micronutrient fertilizers consumption by horticultural crops in Argentina was valued at USD 2.84 million in 2022 and is anticipated to reach USD 3.9 million by 2030.

By application type, soil application dominated micronutrient consumption, accounting for 95.1% of the total volume, followed by fertigation with a 2.5% share and foliar application with a 2.3% share in 2022.

Farmers are adopting micronutrient fertilizers for their crops to achieve high-quality produce and better yields. Deficiency in micronutrients that are essential for plant growth can lead to lower crop yields. During the past decade, soil micronutrient deficiencies were noticed primarily for zinc, boron, and molybdenum. Soil deficiencies of zinc are widespread in the northwestern region of South America. Hence, the micronutrient fertilizers market in Brazil is expected to grow from 2023 to 2030.

South America Micronutrient Fertilizer Market Trends

The government's initiatives to achieve self-sufficiency have significantly contributed to the increased field crop cultivation

The cultivation area for field crops in South America witnessed growth from 111.6 million ha in 2017 to 126.1 million ha in 2022, marking a 12.8% increase. This expansion in cultivation is projected to drive up the demand for fertilizers in the region. Field crops dominated the landscape, accounting for a substantial 96.8% share. In 2022, Brazil held the lion's share of the market at 56.9%, with Argentina trailing at 29.3%. Brazil, known as the global leader in soy production and exports, saw its soy output touch nearly 135 million tonnes in 2021. Out of this, a significant 105.5 million tonnes, or 82%, was exported, with 82% in raw soybean form, 16% as soybean cake, and 2% as soybean oil.

Soybean cultivation reigns supreme in South America, with Brazil and Argentina leading the pack, accounting for 64.4% and 26.1% of the cultivated area, respectively. However, the region is currently grappling with an extended drought, leading to alarmingly low water levels in major rivers. This has far-reaching consequences, hampering both harvests and the transportation of crucial summer crops, especially soybeans. Consequently, this situation amplifies the urgency of increasing fertilizer applications in South America.

Driven by robust global demand and favorable profitability, soybean cultivation in the Mercosur region has witnessed a surge. The price surge in raw materials, including soy, has incentivized producers to expand their operations, investing in new lands and equipment to enhance their scale and efficiency. As a result, the region is poised for further expansion in its field crop cultivation, aligning with the growth in both domestic and international markets.

In 2022, the highest average application rate among micronutrients is for manganese, approximately 12.2 kg/hectare

Oxisols and ultisols dominate the South American soil landscape. Oxisols, characterized by high weathering, uniform texture, and abundant iron and aluminum oxides, contrast with ultisols, which are less weathered but more acidic. However, both soil types necessitate micronutrient supplementation for optimal crop yields, given the immobility of most micronutrients in the soil. Micronutrient deficiencies are increasingly limiting annual crop production in South America. Crops like rice, corn, wheat, soybean, and common bean have reported deficits in essential micronutrients such as zinc, copper, boron, manganese, and iron.

In 2022, the average application rate of micronutrient fertilizers in field crops stood at 4.3 kg/hectare. Despite the presence of iron in these soils, its availability to plants is hampered by its binding with excessive phosphates. Consequently, the average iron application rate in field crops across the region is 3.3 kg/hectare. Manganese, with an average application rate of 12.2 kg/hectare in 2022, leads among the micronutrients. While it is prevalent in upland rice, it is less common in rainfed or lowland rice, as its solubility increases under submerged conditions. Manganese-deficient plants exhibit stunted growth, fewer leaves, reduced weight, and smaller root systems during tillering.

Rapeseed, a prominent field crop in South America, demands higher micronutrient quantities compared to others. In 2022, its average micronutrient fertilizer application rate reached 4.40 kg/hectare. Given the growing emphasis on balanced crop nutrition and the pivotal role of micronutrients in overall yield, an uptick in micronutrient application is anticipated in the coming years.

South America Micronutrient Fertilizer Industry Overview

The South America Micronutrient Fertilizer Market is fragmented, with the top five companies occupying 28.08%. The major players in this market are EuroChem Group, K+S Aktiengesellschaft, Nortox, The Mosaic Company and Yara International ASA (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Acreage Of Major Crop Types

4.1.1 Field Crops

4.1.2 Horticultural Crops

4.2 Average Nutrient Application Rates

4.2.1 Micronutrients

4.2.1.1 Field Crops

4.2.1.2 Horticultural Crops

4.3 Agricultural Land Equipped For Irrigation

4.4 Regulatory Framework

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)