아시아태평양의 건설용 접착제 및 실란트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Asia-Pacific Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1692579

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

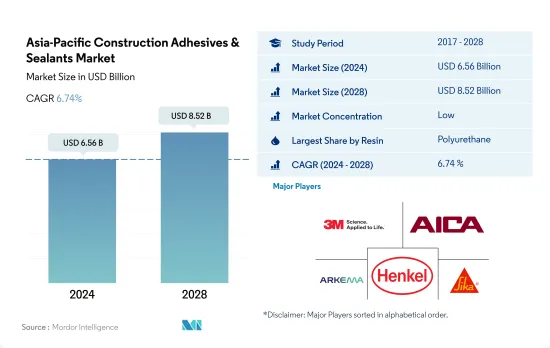

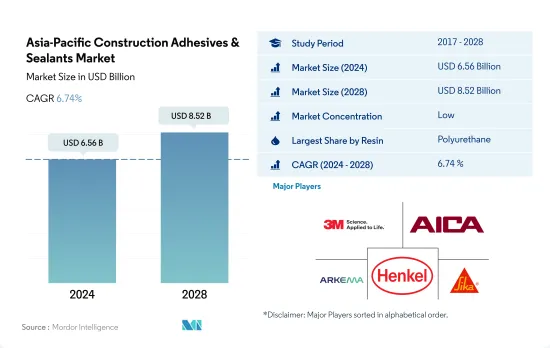

아시아태평양의 건설용 접착제 및 실란트 시장 규모는 2024년 65억 6,000만 달러, 2028년에는 85억 2,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR은 6.74%로 성장할 전망입니다.

중국과 일본의 건설용 접착제 및 실란트의 성장을 지원하는 인프라 프로젝트

폴리우레탄 및 아크릴 수지 기반 접착제 및 실란트는 과거 기간(2017-2021년) 및 기준연도(2021년)에서 다른 수지 유형 중에서 가장 많이 사용되고 있습니다.

지역별로는 2019-2020년 사이에 건설용 접착제 및 실란트 수요는 약 13% 성장하고, 예측기간(2022-2028년)에는 약 4.6%의 성장이 예상됩니다. 모든 수지 유형 중 실리콘 수지 베이스의 접착제 및 실란트는 예측 기간(2022-2028년)에 약 5%의 최대 CAGR을 나타낼 것으로 예상됩니다.

건설용 접착제 및 실란트의 세계 수요에서 중국은 가장 큰 점유율을 차지합니다. 2021년 중국에서 만들어진 수요는 12억 킬로그램이며, 2028년까지 연평균 복합 성장률(CAGR) 6.9%로 18억 킬로그램에 이를 것으로 예상됩니다. 폴리우레탄, 아크릴, 실리콘 수지 기반 접착제 및 실란트 제품은 중국의 건설 산업이 생산하는 총 수요의 50% 이상을 차지할 것으로 예상됩니다. 일본은 건설용 접착제의 2위의 소비국이며, 2021년의 점유율은 약 12%로, 예측 기간(2022-2028년)의 CAGR은 약 2.7%로 예상됩니다. 일본에서는 초고층 빌딩과 고층 빌딩의 건설 프로젝트가 증가하고 있으며, 이것이 접착제 수요의 주요 요인이 되고 있습니다.

건설 투자 증가는 미래 접착제 및 실란트 수요를 밀어 올릴 가능성이 높습니다.

아시아태평양은 건설용 접착제의 활황 시장입니다. COVID-19 팬데믹이 아시아태평양 국가에 영향을 미쳤기 때문에 2020년 전반에는 건설 및 부동산 활동이 감속한 것, 2021년에는 급속히 회복하고 예측기간 2022-2028년을 통해 견조한 성장을 유지할 것으로 예상됩니다. 아시아태평양은 가장 중요한 건설 및 부동산 시장이 되어, 2030년까지 세계의 생산액의 약 40%를 차지할 것으로 예상됩니다.

예측기간 2022-2028년에는 중국이 세계 건설 및 부동산업계를 선도해 지역 성장에 박차를 가할 것으로 예상됩니다. 중국은 2020년 상반기에 주택 및 비주택 건설물의 침체에 휩쓸렸지만, 소비자와 기업의 신뢰가 회복되었기 때문에 급속히 회복했습니다.

COVID-19 팬데믹 후의 건설 및 부동산 업계의 부활에는 정부의 인프라 투자가 빠뜨릴 수 없습니다.

아시아태평양 건설용 접착제 및 실란트 시장 동향

인프라 활동 확대를 위한 투자 증가로 업계 규모 확대

아시아태평양은 중국, 일본, 인도 등 세계의 주요 경제국에 의해 견인되고 있습니다. 로 도시에서 필요로 하는 거주 공간이 증가해, 도시의 중간 소득층이 생활 환경의 개선을 바라게 되는 것으로, 주택 시장에 영향을 주어, 국내의 주택 건설이 증가할 가능성이 있습니다.

비주택 인프라는 크게 확대될 가능성이 높습니다. 세계 건설 투자의 20%를 차지하고 있습니다. 2030년까지 정부는 13조 미국을 넘는 건설 투자를 계획하고 있습니다.

건설 산업은 아시아태평양 최대의 산업 중 하나이며, 2019년에는 유망한 성장을 기록했습니다. 하지만 계속 COVID-19 팬데믹을 위해, 건설 부문은 인도, 중국, 일본, ASEAN 국가를 포함한 개발 도상국에 심각한 영향을 미친 지역 전체의 정부에 의한 락다운 때문에 크게 감소했습니다.

아시아태평양에서도 건설 분야에 대한 해외 투자자의 관심이 높아지고 있습니다.

아시아태평양의 건설용 접착제 및 실란트 산업 개요

아시아태평양의 건설용 접착제 및 실란트 시장은 단편화되어 있으며 상위 5개사에서 17.60%를 차지하고 있습니다. 시장 주요 기업에는 3M, Aica Kogyo, Arkema Group, Henkel AG & Co. KGaA, Sika AG(알파벳순)가 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

건설

규제 프레임워크

호주

중국

인도

인도네시아

일본

말레이시아

싱가포르

한국

태국

밸류체인과 유통채널 분석

제5장 시장 세분화

수지

아크릴

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타 수지

기술

핫멜트

반응성

실란트

용제형

수성

국가명

호주

중국

인도

인도네시아

일본

말레이시아

싱가포르

한국

태국

기타 아시아태평양

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Aica Kogyo Co..Ltd.

Arkema Group

HB Fuller Company

Henkel AG & Co. KGaA

Momentive

Shin-Etsu Chemical Co., Ltd.

Sika AG

Soudal Holding NV

THE YOKOHAMA RUBBER CO., LTD.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Asia-Pacific Construction Adhesives & Sealants Market size is estimated at 6.56 billion USD in 2024, and is expected to reach 8.52 billion USD by 2028, growing at a CAGR of 6.74% during the forecast period (2024-2028).

Infrastructure projects to support the growth of construction adhesives and sealants in China and Japan

Polyurethane and Acrylic resin-based adhesives and sealants are the most used among other reins types during the historical period, 2017-2021, and base year, 2021. They are expected to be the most used resin types during the forecast period because of the strong bonds and their applicability as structural adhesives. In Asia-Pacific, about 49% of the acrylic-based construction adhesives were manufactured in water-borne technology in 2021 and polyurethane based products were manufactured majorly in sealant technology.

Regionally, during 2019-20, the demand for construction adhesives and sealants grew by about 13% and is expected to grow by about 4.6% during the forecast period (2022 - 2028). Among all the resin types, silicone resin-based adhesives and sealants are expected to register the largest CAGR of around 5% during the forecast period (2022 - 2028).

China occupied the largest share of the demand for construction adhesives and sealants globally. In 2021, the demand generated from China was 1.2 billion kilograms and the demand is expected to reach 1.8 billion kilograms with a CAGR of 6.9% by 2028. Polyurethane, acrylic, and silicon resin-based adhesives and sealants products are expected to occupy more than 50% of the total demand generated by China's construction industry. Japan is the second-largest consumer of construction adhesives, and it had about 12% of shares in 2021, is expected to register a CAGR of about 2.7% during the forecast period (2022 - 2028). Japan is seeing an increased number of skyscraper and high-rise building projects, which has been the major source of the demand for adhesives.

Rising construction investments likely to propel the demand for adhesives & sealants in the future

Asia-Pacific is a booming market for construction adhesives. Despite a slowdown in construction and real estate activities during the first half of 2020 as the COVID-19 pandemic affected Asia-Pacific countries, the area rebounded fast in 2021 and is expected to maintain solid growth throughout the forecast period 2022-2028. The Asia-Pacific region is expected to be the most important construction and real estate market, accounting for roughly 40% of global production value by 2030.

Over the forecast period 2022-2028, China is expected to be the leading global construction and real estate industry, fueling regional growth. Decades of substantial Chinese investments in infrastructure expansions, a fast-rising urban population, and extensive foreign direct investment (FDI) into industrial facilities in the nation have contributed significantly to the rise of the Chinese construction sector. Due to the COVID-19 outbreak, China suffered a drop in residential and non-residential buildings in the first half of 2020 but recovered quickly as consumers' and corporate confidence returned. With the global surge in building material prices, including metals and wood, Chinese construction businesses are seeing a significant increase in manufacturing costs but are still able to pass these costs on to final customers.

Government infrastructure investment is critical to the building and real estate industries' revival following the COVID-19 pandemic. Major investments planned in China, India, Japan, and other regional leaders are expected to boost the Asia-Pacific market's growth in the short to medium term. All such factors are expected to increase the demand for construction adhesives and sealants across the region over the forecast period.

Asia-Pacific Construction Adhesives & Sealants Market Trends

Raising investment to expand infrastructural activities will augment the industry size

Asia-Pacific is driven by the world's major economies, such as China, Japan, and India. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increased living spaces required in the urban areas resulting from increasing urbanization and the desire of middle-income urban residents to improve their living conditions may impact the housing market and, thereby, increase the residential constructions in the country.

Non-residential infrastructure is likely to expand significantly. The Chinese government approved 26 infrastructure projects worth approximately USD 142 billion in 2019, with completion due in 2023. The country has the largest construction market globally, accounting for 20% of all worldwide construction investments. By 2030, the government plans to spend over USD 13 trillion on construction. Thus, the construction market is expected to register a 4.48% CAGR during the forecast period (2022-2028).

The construction industry is one of the largest industries in Asia-Pacific and recorded promising growth in 2019. The industry continues to grow as the region constitutes many developing countries such as Vietnam, Malaysia, Indonesia, Thailand, and other South Asian countries. However, due to the COVID-19 pandemic, the construction sector witnessed a significant decline owing to lockdowns by governments across the region, which severely affected developing countries, including India, China, Japan, and ASEAN countries.

The Asia-Pacific region is also witnessing significant interest from international investors in the construction space. Foreign Direct Investment (FDI) in the construction development sector is increasing as developing countries provide better returns and opportunities for investors.

Asia-Pacific Construction Adhesives & Sealants Industry Overview

The Asia-Pacific Construction Adhesives & Sealants Market is fragmented, with the top five companies occupying 17.60%. The major players in this market are 3M, Aica Kogyo Co..Ltd., Arkema Group, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Building and Construction

4.2 Regulatory Framework

4.2.1 Australia

4.2.2 China

4.2.3 India

4.2.4 Indonesia

4.2.5 Japan

4.2.6 Malaysia

4.2.7 Singapore

4.2.8 South Korea

4.2.9 Thailand

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 Resin

5.1.1 Acrylic

5.1.2 Cyanoacrylate

5.1.3 Epoxy

5.1.4 Polyurethane

5.1.5 Silicone

5.1.6 VAE/EVA

5.1.7 Other Resins

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Sealants

5.2.4 Solvent-borne

5.2.5 Water-borne

5.3 Country

5.3.1 Australia

5.3.2 China

5.3.3 India

5.3.4 Indonesia

5.3.5 Japan

5.3.6 Malaysia

5.3.7 Singapore

5.3.8 South Korea

5.3.9 Thailand

5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Aica Kogyo Co..Ltd.

6.4.3 Arkema Group

6.4.4 H.B. Fuller Company

6.4.5 Henkel AG & Co. KGaA

6.4.6 Momentive

6.4.7 Shin-Etsu Chemical Co., Ltd.

6.4.8 Sika AG

6.4.9 Soudal Holding N.V.

6.4.10 THE YOKOHAMA RUBBER CO., LTD.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)