North America Commercial Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1692479

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

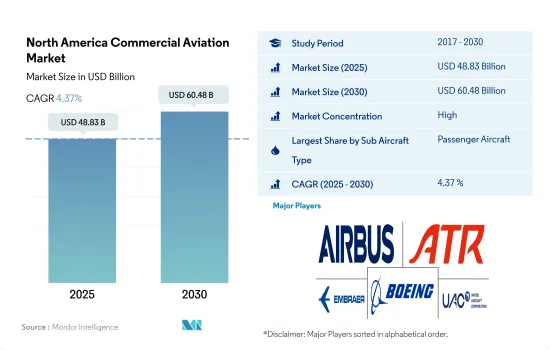

북미의 상업항공시장 규모는 2025년에 488억 3,000만 달러로 추정되고, 2030년에는 604억 8,000만 달러에 이를 것으로 예측되며, 예측기간(2025-2030년)의 CAGR은 4.37%로 성장할 것으로 예측됩니다.

항공사의 항공기 개발과 연료 효율이 높은 항공기에 대한 수요 증가가 북미 상업항공 수요를 견인

북미의 상업항공 시장은 예측 기간 동안 국내 여행객의 증가로 인한 여객기 수요로 인해 상당한 성장을 경험할 것으로 예상됩니다.

항공사의 항공기 개발, 연료 효율이 높은 항공기에 대한 수요 증가, 항공 승객 수 증가, 항공 업계의 무공해 2050 목표에 대한 고려가 상업항공기 수요를 촉진하고 있습니다. 2023년 8월 현재 이 지역에는 1,474대의 보잉 항공기와 986대의 에어버스 항공기가 수주잔고를 보유하고 있습니다. 이 전체 항공기 중 미국에만 2,405대의 항공기가 수주잔고를 보유하고 있습니다.

또한 북미에서 미국은 가장 많은 상업항공를 보유하고 있으며 세계 최대 항공사의 본거지이기도 합니다. 2017-2022년 동안 이 지역에서는 다양한 항공사에서 총 2,065대의 신규 상업항공를 인도받았습니다. 이 2,065대의 항공기 중 여객기는 1,919대, 화물기는 146대를 차지했습니다.

또한, 전자상거래 도입이 가속화되면서 전용 화물기의 물동량과 수익이 증가함에 따라 항공 화물 운송 능력의 혼란은 화물기 부문에 긍정적인 영향을 미쳤습니다.

북미 지역의 상업항공 활동을 주도하는 협동체 항공기

북미의 상업항공 산업은 오랫동안 글로벌 항공 시장에서 중요한 역할을 해왔습니다. 이 지역의 상업 항공 활동에 대한 수요는 매년 증가하는 항공 여행객 수에 의해 주도되고 있습니다. 2022년 이 지역의 항공 여객 수는 60억 명에 달할 것으로 예상됩니다

저비용항공사(LCC)와 초저비용항공사(ULCC)의 부상은 전통적인 항공사 비즈니스 모델에 지각변동을 일으켰습니다. 이들 항공사는 경쟁력 있는 요금으로 더 많은 고객층을 확보하고 더 많은 사람이 항공 여행을 이용할 수 있도록 확장하고 있습니다. 2017년부터 2022년까지 이 지역의 다양한 항공사에서 총 2,049대의 항공기를 조달했습니다.

787 드림라이너의 일시적인 인도 중단, 777X 프로그램의 지연, 인증 문제로 인한 A350의 생산량 증가 지연, 광동체 제트기에 대한 수요 약세는 예측 기간 상반기 동안 광동체 부문의 성장을 저해할 것으로 예상됩니다. 반대로 737MAX, A220, A321neo, A321XLR의 생산량 증가 계획은 향후 10년간 이 지역의 협동체 부문의 성장을 뒷받침할 것입니다.

북미의 상업항공 시장 동향

국내 여행객의 수요 증가가 시장을 견인/h4>

북미는 오랫동안 항공 여행의 허브 역할을 해왔습니다. 광활한 국토와 다양한 목적지로 인해 수백만 명의 승객이 국내선 및 국제선 항공편을 이용하고 있습니다. 경제 성장, 항공 여행의 경제성 향상, 중산층 증가 등의 요인으로 인해 항공 승객 수가 크게 증가했습니다.

2022년 1월부터 12월까지 연중 미국 항공사가 운반한 여객수는 8억 5,300만명으로, 2021년 6억 5,800만명, 2020년 3억 8,800만명 이상 돌았습니다. 캐나다 항공사가 운반한 총 여객수는 2022년에 1억 700만 명에 달했으며 2021년 수준을 6% 웃돌았습니다. 2022년 멕시코의 항공 승객 수는 1억 명으로 2021년 대비 7% 성장했습니다.

또한 항공 여객 수요 증가에 대응하기 위해 이 지역의 다양한 항공사가 신규 항공기 도입을 계획하고 있습니다. 예를 들어, 2023년 전 세계 항공기 인도량의 약 3분의 1이 북미 지역의 다양한 항공사에서 인도받을 것으로 예상됩니다. 지난해 이 지역의 항공기 인도량은 이미 2019년 수준을 넘어섰지만, 올해에는 72대가 추가로 증가할 것으로 예상됩니다.

북미의 상업항공 산업 개요

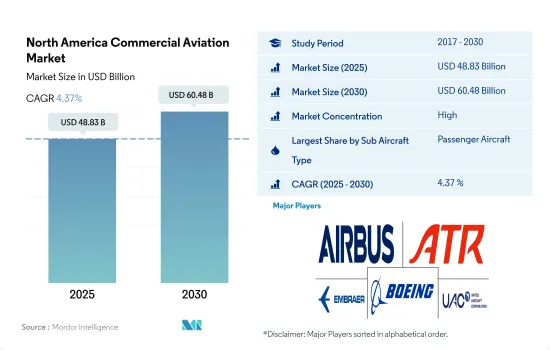

북미의 상업항공 시장은 상당히 통합되어 있으며 상위 5개사가 87.70%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

항공 여객 수송량

항공 화물 수송량

국내총생산

수입 여객 킬로미터(rpk)

인플레이션율

규제 프레임워크

밸류체인 분석

제5장 시장 세분화

서브 항공기 부문

화물기

여객기

협동체 항공기

광동체 항공기

국가명

캐나다

멕시코

미국

기타 북미

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Airbus SE

ATR

COMAC

De Havilland Aircraft of Canada Ltd.

Embraer

The Boeing Company

United Aircraft Corporation

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The North America Commercial Aviation Market size is estimated at 48.83 billion USD in 2025, and is expected to reach 60.48 billion USD by 2030, growing at a CAGR of 4.37% during the forecast period (2025-2030).

Fleet development of the airlines, and increasing demand for fuel-efficient aircraft is driving the demand for the commercial aircraft in North America

The commercial aircraft market in North America is expected to experience significant growth during the forecast period, primarily driven by the demand for passenger aircraft due to the growing number of domestic passengers traveling.

Fleet development of the airlines, increase in demand for fuel-efficient aircraft, growth in the number of airline passengers, and the airline industry's consideration of the zero-emission 2050 goal fuel the demand for commercial aircraft. As of August 2023, the region has a backlog of 1,474 Boeing aircraft and 986 Airbus aircraft. Of these total aircraft, the US alone has 2,405 aircraft in backlog. Hence, the country is expected to witness larger growth.

Additionally, in North America, the United States has the largest fleet of commercial aircraft and is home to some of the biggest carriers in the world. In terms of new aircraft deliveries, in the region during 2017-2022, a total of 2,065 new commercial aircraft were procured by various airlines. Of these 2,065 aircraft, passenger aircraft accounted for 1,919, and freighter aircraft accounted for 146 aircraft. With the demand for air travel recovering, the airlines are restructuring their procurement plans and trying to maintain a relatively younger fleet to reduce operational costs, thus generating demand for new passenger aircraft.

Furthermore, disruption in air cargo capacity proved to be positive for the freighter segment, as dedicated freighter fleets experienced volume and revenue increases, supported by accelerated e-commerce adoption. FedEx, UPS, and Atlas Air have plans to expand their fleet with new freighter aircraft during the forecast period.

Narrowbody aircraft is driving the region's commercial aviation activity

The commercial aviation industry in North America has long been a significant player in the global aviation market. The demand for commercial aviation activity in the region is driven by the rising number of passengers traveling by air annually. In 2022, the region's air passenger traffic stood at 6 billion. The US accounted for the largest share, which was 83%, followed by Canada, Mexico, and the Rest of North America at 8%, 6%, and 2%, respectively.

The rise of low-cost carriers (LCCs) and ultra-low-cost carriers (ULCCs) has disrupted the traditional airline business model. These carriers offer competitive fares, enticing a larger customer base and expanding air travel accessibility to more people. In terms of deliveries during 2017-2022, a total of 2,049 aircraft were procured by various airlines in the region. Of these 2,049 aircraft, passenger aircraft accounted for 96% and freighter aircraft accounted for 4%.

A temporary halt in delivery of the 787 Dreamliner, delay in the 777X program, and delay in production ramp-up of A350s due to certification problems, as well as weak demand for the widebody jet, are expected to hamper the growth of the widebody segment during the first half of the forecast period. On the contrary, production ramp-up plans for 737MAX, A220, A321neo, and A321XLR will support the growth of the narrowbody segment in the region over the next decade. Overall, with developments such as these, the demand for commercial aviation aircraft is expected to rise, and during 2023-2030, a total of 2,997 commercial aviation aircraft is scheduled to be procured.

North America Commercial Aviation Market Trends

The increase in demand from domestic travelers is driving the market

North America has long been a hub for air travel. With a vast landmass and diverse destinations, millions of passengers choose to fly domestically and internationally. Factors such as a growing economy, increased affordability of air travel, and a rising middle class have all contributed to a significant uptick in air passenger traffic. The air passenger traffic in the US reached 1.04 billion in 2022, up by 7% compared to 2021 and 12% compared to 2019.

For the full year 2022, January through December, US airlines carried 853 million passengers, up from 658 million in 2021 and 388 million in 2020. The total number of passengers carried by airlines in Canada reached 107 million in 2022, surpassing the levels in 2021 by 6%. In 2022, Mexico had 100 million air passenger traffic, representing a 7% growth compared to its 2021 traffic levels. North America has benefitted from fewer and shorter-lasting travel restrictions than many other countries and regions. This has boosted domestic travel in a large home market, as well as international travel. Net profits for the region are expected to rise from USD 9.9 billion in 2022 to USD 11.4 billion in 2023.

Additionally, to cater to the demand driven by air passenger traffic, various airlines in the region are planning to procure new aircraft. For instance, around one-third of global aircraft deliveries for 2023 are anticipated to be received by various carriers in North America. Although the region's aircraft deliveries were already above 2019 levels last year, they are expected to grow by an additional 72 units this year. Overall, with consistent air travel, the region's air passenger traffic is expected to increase by 1.7 billion in 2030, compared to 1.2 billion recorded in 2022.

North America Commercial Aviation Industry Overview

The North America Commercial Aviation Market is fairly consolidated, with the top five companies occupying 87.70%. The major players in this market are Airbus SE, ATR, Embraer, The Boeing Company and United Aircraft Corporation (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Air Passenger Traffic

4.2 Air Transport Freight

4.3 Gross Domestic Product

4.4 Revenue Passenger Kilometers (rpk)

4.5 Inflation Rate

4.6 Regulatory Framework

4.7 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)