미국의 포토닉스 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

US Photonics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1692452

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

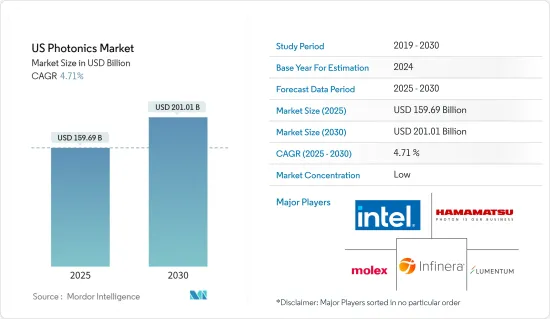

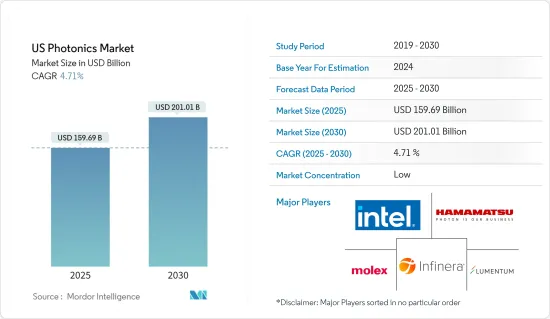

미국의 포토닉스 시장 규모는 2025년 1,596억 9,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 4.71%로 확대되어, 2030년에는 2,010억 1,000만 달러에 달할 것으로 예측되고 있습니다.

주요 하이라이트

포토닉스는 헬스케어, 자동차, 통신, 제조, 소매 등 다양한 산업에서 에너지 효율이 높은 스마트 시스템 구축을 가능하게 하는 중요한 기술로 여겨지고 있습니다.

최근에는 다양한 분야에 대한 투자가 대폭 늘어나고 있습니다.

포토닉스에서는 LiDAR 기술이 각광을 받고 있습니다. 원래는 대기 중의 가스 분포나 오염물질의 연구에 사용되고 있었지만, 지금은 자율주행에 빠뜨릴 수 없는 것이 되고 있습니다.

Google, Microsoft, Facebook과 같은 업계 기업의 존재가 미국 시장을 견인하는 주된 힘이 되고 있어 각 데이터센터의 데이터 전송 프로세스의 최적화가 필요해지고 있습니다.

2023년 2월, Excelitas Technologies O Corp.는 혁신적이고 시장 중심의 포토닉스 솔루션을 제공하는 데 집중하는 산업 기술 제조업체로 미국 오레곤 주 힐즈버러의 Phoseon Technology, Inc.를 인수했습니다. Phoseon사는 LED 기반의 산업용 경화 및 과학용 조명 솔루션의 설계·제조에 있어서의 주요 기업이며, 폭넓은 세계 고객에게 현장에서 입증된 신뢰성과 대폭적인 효율 향상을 제공합니다.

그러나 기존 제품에 비해 실리콘 대응 포토닉 제품과 디바이스는 초기 비용이 높아 많은 분야에서 기술 전개를 방해하고 있습니다.

미국 포토닉스 시장 동향

실리콘 기반 포토닉스 용도의 등장으로 시장을 견인

포토닉스의 신흥 분야인 실리콘 포토닉스는 반도체에서 볼 수 있는 기존의 전도체와는 다른 명확한 이점을 제공합니다. 이 반도체는 고속 트랜스미션 시스템에서 일반적으로 사용되고 있습니다. 이 기술은 IBM, Intel, Kothura 등의 기업이 브레이크스루를 달성하고 트랜스미션 속도를 100Gbps까지 끌어올릴 것으로 기대되고 있습니다. 게다가 이 기술은 반도체 업계에 혁명을 일으켜 고속 데이터 전송과 처리를 가능하게 하고 있습니다.

또한 실리콘 기반 포토닉스는 에너지 효율이 뛰어난 데이터 전송 및 처리 솔루션을 제공하기 때문에 데이터센터나 고전력 컴퓨팅 등 소비 전력이 우려되는 용도에 적합합니다.

인터넷 트래픽 증가는 보다 높은 포트 밀도와 빠른 속도 전환을 지원하는 차세대 기술의 필요성을 가속화할 뿐만 아니라 물리적 데이터센터의 대규모화와 데이터센터 간의 연결 속도를 높여줍니다. 고속 데이터를 전송하기 위한 데이터 레이트와 거리가 증가함에 따라, 기존 동선 케이블이나 멀티 모드 파이버를 베이스로 한 솔루션의 한계가 밝혀지고 있어, 업계는 싱글 모드의 광 파이버 솔루션을 채용하는 방향으로 시프트하고 있습니다.

실리콘 기반 포토닉스는 데이터센터의 진화에 있어서 단기적으로는 100G, 그 후 400G, 800G의 플러그 케이블에서 중요한 역할을 할 것으로 예상되고 있습니다. 이 기술은 도달 거리 500m의 DR 표준 연결에 사용되는 것이 증가하고 있지만, 데이터 통신 용도에서는 코히런트 기술과 함께 사용되는 경우도 있습니다.

또한 의료 응용 분야에서 실리콘 포토닉스의 도입이 증가하고 있으며, 많은 신흥 기업이 제조 플랫폼으로 실리콘 집적 옵틱스를 사용하기 시작하고 있습니다.

소비자 헬스 개발은 계속되고 있으며, 록레이는 2022-2023년에 VitalSpexTM 바이오센싱 플랫폼의 출하를 발표하고 있습니다.

데이터 통신 용도 부문이 큰 시장 점유율을 차지할 전망

통신 기술, 특히 광 광대역에서 광 솔루션의 채용이 증가하고 있기 때문에 이 기술 시장 수요가 높아진다고 보여지고 있습니다.

인프라의 일부로 광네트워크가 채용됨에 따라 통신기업은 레거시 네트워크 업그레이드에 투자하게 되었습니다.

광대역에 대한 세계 수요는 기술의 보급과 온라인 비디오 컨텐츠의 소비 증가로 인해 증가하는 경향이 있습니다. 또한 미국 해군 연구소에 의하면, 400개 이상의 광섬유 해저 케이블 중, 미국은 약 88개를 통해 세계와 연결되어 있으며 그 중 17개는 2022년부터 2024년 사이에 완성할 예정입니다.

세계 System for Mobile Communications(GSMA)에 따르면 미국에서 5G의 보급률은 2025년까지 4G를 추구할 것으로 예상되고 있습니다. 바이든 해리스 정권은 개방적이고 상호 운용 가능한 네트워크를 구축하기 위해 15억 달러를 투자하는 공공 무선 공급망 혁신 기금을 도입했습니다.

미국 포토닉스 산업 개요

미국 포토닉스 시장은 다수의 세계 및 지역 기업들로 구성되어 있습니다.

시장 점유율에 타협하지 않고 이만큼의 중요한 벤더가 존재하는 것은 지속가능한 것입니다.

2023년 11월, Innolume사는 광출력 1W에 이른 O밴드 양자점 GaAs SOA를 발매했습니다.

2023년 9월, ADLT Lighting Group은 Cre Lighting 미국, E-conolight, Cre Lighting 캐나다 인수를 발표했으며, 이 회사의 야심찬 성장 전략에서 중요한 이정표가 되었습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자/소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

산업 밸류체인 분석

주요 거시 경제 동향의 영향 평가

제5장 시장 역학

시장 성장 촉진요인

실리콘 기반 포토닉스 용도의 출현

고성능으로 환경 친화적인 솔루션에 대한 주목 증가

시장의 과제/억제요인

포토닉스 대응 디바이스의 높은 초기 비용

제6장 시장 세분화

용도별

측량과 검출

생산기술

데이터 통신

이미지 캡처 및 디스플레이

의료기술

조명

기타 용도

제7장 경쟁 구도

기업 프로파일

Intel Corporation

Neophotonics Corporation(lumentum Holdings)

Infinera Corporation

Molex Inc.

Hamamatsu Photonics KK

IPG Photonics

Coherent, Inc.(Coherent Corp.)

Vescent Photonics LLC

Photonic Systems Inc.

Thorlabs Inc.

NEC Corporation

ams OSRAM AG

Trumpf Group

Polatis Incorporated(huber suhner)

Alcatel-lucent SA(Nokia Corporation)

제8장 포토닉스 산업의 종업원 시나리오

제9장 시장 전망

JHS

영문 목차

영문목차

The US Photonics Market size is estimated at USD 159.69 billion in 2025, and is expected to reach USD 201.01 billion by 2030, at a CAGR of 4.71% during the forecast period (2025-2030).

Key Highlights

Photonics is considered a crucial technology that enables the creation of energy-efficient smart systems across various industries, including healthcare, automotive, communications, manufacturing, and retail. These sectors are adopting photonics to enhance efficiency and drive growth.

In recent times, investments in various sectors have experienced substantial growth. Photonics, as a fundamental technology across multiple industries, is seeing rapid adoption, with the market expanding into new verticals.

LiDAR technology has gained prominence in photonics. Originally used for studying atmospheric gas distribution and contaminants, it has now become crucial for autonomous driving. Advances in LiDAR mapping systems and related technologies have expanded its applications across various verticals, including aerospace, defense, automotive, mining, and oil and gas.

The presence of industry players such as Google, Microsoft, and Facebook is the primary force driving the US market, necessitating optimization of the data transmission process for respective data centers. The country also provides a favorable environment for technological advancements and expansions. Furthermore, the significant funding landscape in the US silicon photonics devices industry has encouraged organizations and start-ups to invest in the expanding photonics market.

In February 2023, Excelitas TechnologiesO Corp. which is a industrial technology manufacturer concentrated on delivering innovative, market-driven photonic solutions, acquired the Phoseon Technology, Inc, Hillsboro, OR, USA. Phoseon is a key player in the design and manufacturer of LED-based industrial curing and scientific illumination solutions offering the field-proven reliability and enabling significant efficiency gains for a wide range of global customers.

However, compared to conventional products, the high initial cost of silicon-enabled photonic products and devices hinders technology deployment in many fields. While the technology provides higher performance and efficiency, photonics-based devices remain inaccessible to many small- and medium-sized end-users in various verticals due to limited budgets.

US Photonics Market Trends

Emergence of Silicon-based Photonics Applications to Drive the Market

Silicon photonics, an emerging field within photonics, provides a distinct advantage over traditional electrical conductors found in semiconductors. These semiconductors are commonly used in high-speed transmission systems. This technology is expected to push the transmission speed up to 100 Gbps, with companies like IBM, Intel, and Kothura, achieving breakthroughs. Besides, this technology is revolutionizing the semiconductor industry, enabling high-speed data transfer and processing.

Moreover, silicon-based photonics provides energy-efficient data transmission and processing solutions, making it suitable for applications where power consumption is a concern, such as data centers and high-power computing.

The growth in internet traffic is not only accelerating the need for next-generation technology to support higher port density and faster speed transitions but is also accompanied by large physical data center sizes and faster connectivity between the data centers. As the data rates and distances to carry high-speed data are increasing, the limitations of traditional copper cable and multimode fiber-based solutions are becoming apparent, and the industry is shifting towards adopting single-mode fiber-optic solutions.

Silicon-based photonics is expected to play a significant role in the evolution of data centers in the short term for 100G and then 400G and 800G pluggables. It will also be an enabling technology for disaggregating data centers and a possible future CPO approach. The technology is increasingly used for 500 m reach DR-standard connections but is also used with coherent technology in datacom applications. Moreover, the market is also witnessing increasing demand for 400ZR standard technology.

Additionally, with the rising implementation of silicon photonics in medical applications, many start-ups have started using silicon-integrated optics as a manufacturing platform. According to US Census Bureau, the industry revenue of medical equipment and supplies manufacturing in the United States is expected to reach USD 43.51 billion by 2023. Whereas the national health expenditure in the country is expected to reach USD 7.174 trillion by 2031, which was USD 4.439 trillion in 2022, as stated by CMS.

Consumer health development continues, with Rockley announcing the shipment of its VitalSpexTM biosensing platform in 2022-23. Such trends are expected to boost the integration of silicon photonics-based biosensors in wearables from prominent brands like Apple or Huawei.

Data Communication Application Segment is Expected to Hold Significant Market Share

The increasing adoption of optical solutions in communication technologies, particularly optical broadband, is anticipated to boost demand for this technology in the market. This segment holds a significant market share.

The increasing adoption of optical networks as part of infrastructure has led telecommunication companies to invest in upgrading their legacy networks. Telephone companies were pioneers in replacing their outdated copper wire systems with optical fiber lines. Telephone companies leverage optical fiber as the backbone architecture and a long-distance connection between the city phone systems.

The global demand for broadband is on the rise due to the widespread adoption of technology and the increasing consumption of online video content. According to TeleGeography's submarine cable map, submarine cables act as the backbone of the Internet. Moreover, according to the US Naval Institute, of more than 400 fiber optics undersea cables, the United States is connected to the world through approximately 88, including 17 scheduled to be completed between 2022 and 2024.

According to Global System for Mobile Communications (GSMA), the 5G penetration in the United States is expected to overtake 4G by 2025. In addition, the government is allocating several funds for the faster deployment of 5G services in the region. In April 2023, the Biden-Harris Administration introduced the Public Wireless Supply Chain Innovation Fund, which invested USD 1.5 billion to create open and interoperable networks. The initial round of funding will assist to ensure that the future of 5G and next-generation wireless technology is built by the United States and its global allies and partners.

US Photonics Industry Overview

The United States photonics market comprises several global and regional players vying for attention in a contested market space. Market incumbents, such as Finisar Corporation, Intel Corporation, NeoPhotonics Corporation, Infinera Corporation, Hamamatsu Photonics, IPG Photonics Corporation, and Coherent Inc., have a considerable influence on the overall market, with access to well-established distribution networks.

The existence of such a sheer number of significant vendors without compromising on their market shares is sustainable. Brand identity associated with major vendors became a synonym for various product offerings under the scope of the study worldwide. Overall, the intensity of competitive rivalry among the vendors in the market studied is expected to be high and remain the same during the forecast period.

November 2023, Innolume launched O band Quantum Dot GaAs SOA that has reached 1W of optical power. It can be further leveraged in LiDARs, PONs and FSO.

In September 2023, the ADLT Lighting Group announced the acquisition of Cree Lighting US, E-conolight, and Cree Lighting Canada, marking a significant milestone in the company's ambitious growth strategy. These acquisitions solidify ADLT Lighting Group's position as a global provider in the lighting industry and reinforce its commitment to innovation and excellence.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyer/Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Emergence of Silicon-based Photonics Applications

5.1.2 Increasing Focus on High-performance and Eco-Friendly Solutions

5.2 Market Challenges/Restraints

5.2.1 High Initial Cost of Photonics - Enabled Devices