ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

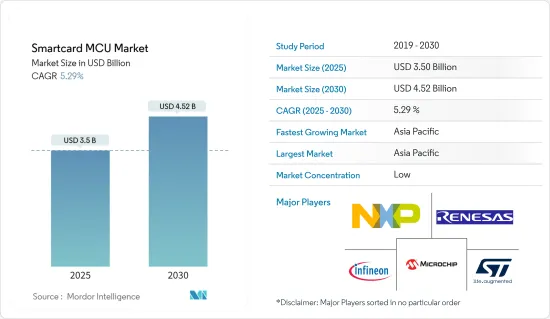

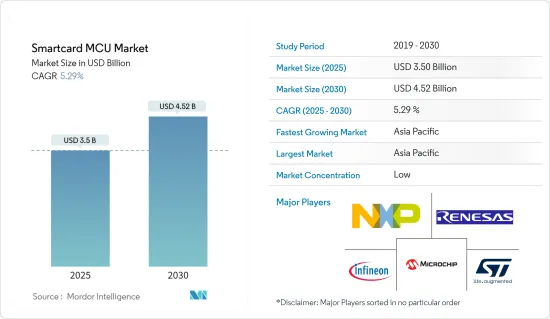

스마트카드 MCU 시장 규모는 2025년 35억 달러, 2030년에는 45억 2,000만 달러에 달할 것으로 예측됩니다.예측기간(2025-2030년)의 CAGR은 5.29%를 나타낼 전망입니다.

출하 대수에서는 2025년 93억 2,000만대, 2030년에는 155억 3,000만대로 성장할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 10.74%를 나타낼 전망입니다

주요 하이라이트

인터넷의 급속한 확대로 인해 전자상거래는 컴퓨터 사용자들 사이에서 습관이 아니더라도 현실이 되었습니다. 그럼에도 불구하고 전자상거래 용도에서 사용되는 현재의 비즈니스 모델은 전자 매체의 잠재력을 충분히 끌어낼 수 없습니다.

시장 개척의 원동력이 되고 있는 것은 스마트 카드에 있어서의 RFID 기술과 NFC의 개발 확대입니다. 무선 주파수 식별(RFID) 기술의 급속한 진화를 활용한 비접촉형 스마트 카드가 인기를 끌고 있습니다. 이 카드는 RFID 기술을 사용하여 거래를 처리합니다. 주요 공급업체는 소비자 수요 증가로 인해 비접촉식 스마트 카드 도입에 주력하고 있으며 시장 성장의 원동력이 될 것으로 기대되고 있습니다.

운송 업계에서 스마트 카드 기술의 보급은 디지털 기술 도입을 위한 정부 투자 증가와 함께 시장 성장의 원동력이 되고 있습니다. 전자 스마트 결제 카드는 현재 교통 사업자에게 수행할 수 있는 대체 결제 수단이 되고 있습니다. 최근 몇 년동안 많은 사업자와 시스템 제공 업체가 기존 결제 방법을 보완하거나 대체하기 위해 스마트 카드 기반 시스템을 도입했습니다.

또한, 보안과 소형화는 스마트 카드 기술의 두 가지 가장 빠른 발전을 상징합니다. 보다 안전한 EMV 뱅킹 카드로의 세계 전환으로 인해 최신 세대의 스마트 카드는 완벽한 온칩 암호화를 자랑하며 업계 전반의 카드 보안을 크게 강화하고 있습니다.

또한 IC 카드는 미니 태그와 스마트 웨어러블과 같은 다양한 폼 팩터로 소형화가 진행되고 있습니다. 이러한 추세는 스마트 카드가 전화 및 생체 인식과 함께 2 요소 자격 증명으로 점점 더 많이 채택됨에 따라 계속 될 것입니다.

스마트 카드가 직면한 주요 과제는 보안 수준입니다. 잠재력을 최대한 발휘하려면 스마트 카드는 다양한 인터페이스와 상호작용해야 합니다. 그러나 일반적인 인식과 관련된 보안 문제가 발생합니다. 사람들은 카드에 저장된 개인 정보가 안전하다는 것을 인식해야 할 수도 있습니다. 그러나 스마트 카드에서 추출한 정보는 다른 곳에서 수집되고 분석된다는 인식이 필요합니다.

스마트 카드 MCU 시장 동향

성장이 예상되는 BFSI

은행 및 금융 기관용 스마트 카드에는 현재 전용 집적 회로 카드가 내장되어 있어 견고한 보안 대책이 확보되어 있습니다. 이 카드에는 메모리 칩과 마이크로프로세서가 내장되어있어 안전한 데이터를 저장하고 처리 할 수 있습니다. 이러한 카드는 거래 인증, 온라인 뱅킹 서비스에 대한 안전한 액세스, 직불카드 및 신용카드로 결제, 비접촉식 결제 방법 등 금융 활동에서 다양한 기능을 수행합니다.

결제 프로세스의 디지털화는 인터넷의 개발과 전자상거래의 등장에 크게 기여하고 있습니다. 이 전환으로 결제 카드(신용 및 직불)부터 디지털 지갑, 전자 캐시, 비접촉식 결제 방법에 이르기까지 전자 결제 옵션이 풍부해졌습니다. 인기 급상승 중인 모바일 결제 서비스는 현재 과도기를 맞이하고 있으며, 미래의 기술적 진보에 대비하는 태세가 갖추어지고 있습니다. 이러한 결제 방법의 진보는 스마트카드 기술을 활용하여 시장 성장을 가속할 것으로 예상됩니다.

MCU(마이크로컨트롤러 유닛)가 장착된 스마트 카드는 개인 식별 번호(PIN)와 함께 일반적으로 사용됩니다. MCU는 조직의 보안 강화, 다중 요소 인증(MFA) 토큰으로서의 기능, 싱글 사인온(SSO) 사용자 인증 등 다양한 목적을 수행합니다. 유행과 Apple Pay, Klarna, Stripe, Amazon Pay와 같은 대체 결제 수단이 등장했으며 온라인 거래의 급증은 대면 거래를 능가합니다. 이러한 진보는 스마트 카드 기술 업계에서의 응용 가능성을 크게 확대합니다.

EMV 카드 기술은 신용 카드와 직불 카드에 통합된 작고 견고한 칩을 채택하여 진화하는 결제 솔루션으로 인정받고 있습니다. EMV는 Europay, Mastercard 및 Visa의 이니셜을 취하며 이 업계 표준을 지원하는 공동 노력을 보여줍니다. 이러한 고급 카드는 신용카드의 무단 사용으로 인한 손실을 줄이고, 보다 안전한 결제 환경을 촉진하고, 보다 안전한 거래 경험을 보장함으로써 비즈니스와 고객의 보안을 강화하는 데 필수적입니다.

대부분의 새로운 EMV 카드와 칩 기반 리더에는 근거리 무선 통신(NFC) 기술이 탑재되어 비접촉 결제가 가능합니다. 고객은 카드를 지도자에게 들고 보다 빠르고 안전한 거래를 할 수 있습니다. 보안 강화 외에도 EMV 스마트 카드는 카드와 단말기 간의 안전한 통신을 통해 속도와 편의성을 향상시켜 가맹점과 카드 소유자 모두에게 이점을 제공합니다.

암호화 알고리즘을 채택한 칩을 탑재한 EMV 카드는 사용할 때마다 데이터를 고유하게 암호화하여 거래의 안전성을 높입니다. 카드 프리젠 테이션 거래에서 이러한 카드는 물리적 카드와 고객의 비밀번호가 필요한 이중 인증 프로세스를 채택합니다. 이 인증 방법은 카드 소유자를 확인하고 칩에서 생성한 일회용 암호(OTP)를 확인하고 승인할 수 있습니다. 예측되는 기술의 진보는 스마트 카드 기술에 대한 광범위한 수요를 불러 일으켜 시장의 성장을 가속합니다.

아시아태평양이 큰 시장 점유율을 차지할 전망

아시아태평양에서 스마트 카드 기술을 채택하면 멀티 용도 스마트 카드로의 변화를 경험하고 있습니다. 이러한 카드는 결제, 식별, 액세스 제어 등 여러 목적으로 사용되며, 소비자에게는 편의성과 효율성 향상, 기업에게는 비용 절감으로 이어지고 있습니다. 또한, 특히 온라인 거래가 증가함에 따라 스마트 카드의 보안 기능 강화 요구가 커지고 있습니다.

정부가 디지털화에 힘을 쏟고 있는 경우도 있어, 인도에서는 스마트 카드 기술이 널리 보급되고 있습니다. 거의 모든 인도 국민이 어떤 형태로 스마트 카드를 소유하고있는 것 같습니다. 이 카드는 은행, 건강 관리, 교통, 정부 신분증 등 다양한 분야에서 널리 사용됩니다. 예를 들어 인도에서는 운전면허증, 차량등록증명서(DL/RC), 다목적 국민 ID 카드(MNIC), Rashtriya Swasthya Bima Yojana(RSBY), 전자 여권(e-Passport) 등에 스마트 카드가 채용되고 있습니다. 이 지역에서는 스마트 카드 기술의 채용이 증가하고 있어 시장의 견인역이 될 것으로 예상됩니다.

가까운 미래에 디지털 결제와 스마트 카드 수요가 급증할 것으로 예상됩니다. 인도의 BFSI 부문은 스마트 카드 기술의 채택을 추진하고 있으며 MCU 제조업체에 큰 전망을 가져올 것으로 예상됩니다. 특히 Rashtriya Swasthya Bima Yojana(RSBY) 하에서 운영되는 보험 회사와 은행의 비즈니스 코레스폰던트는 수백만 장의 칩 카드를 생산하고 있으며 인도를 스마트 카드 기술의 가장 빠른 도입 국가 중 하나로 만들고 있습니다. 이러한 요인이 시장 수요를 높일 것으로 예상됩니다.

또한 인도에서 IC 카드 기술을 도입하면 일반 시민의 삶의 질을 향상시키고 사회 복지 프로그램과 교통 시스템에 혜택을 줄 수 있습니다. 그 예는 카르나타카 주에 거주하는 여성이 프리미엄 버스 이외의 버스를 자유롭게 이용할 수 있도록 하는 Shakti 스마트 카드 체계입니다. EMVCo에 따르면 스마트 카드 인디아 이니셔티브는 거래 시간을 단축하고 손실을 최소화하며 수혜자의 만족도를 높였습니다. 스마트 카드와 같은 혁신적인 기술의 활용은 미래의 복지 프로그램을 강화할 잠재력을 가지고 있습니다.

단거리 무선 접속을 확립할 수 있는 MCU를 탑재한 스마트 결제 카드는 비접촉 결제 시스템에 활용될 가능성을 가지고 있습니다. 이 지역에서는 비접촉형 카드의 이용이 계속 증가하고 있으며, 그 보급률이 높아짐에 따라, 이 방법에 의한 결제량이 대폭 급증하고, 그 결과, 주목해야 할 시장 수요가 발생하고 있습니다.

스마트 카드 MCU 시장 개요

스마트카드 MCU 시장은 대기업간 경쟁 격화를 특징으로 하는 반통합적인 모습을 보여줍니다. 이 상황은 통합의 진전, 기술의 진보, 진화하는 지정학적 시나리오의 영향을 받은 변동이 특징입니다. 지속가능한 경쟁우위를 위한 기술 혁신이 중시되고 있는 가운데, 최종사용자 업계의 신규 고객에서의 수요 급증이 예상되고, 경쟁은 격화의 길을 따라가고 있습니다.

이러한 상황에서 마이크로 컴퓨터 제조에서 최종 사용자의 품질에 대한 기대를 감안할 때 브랜드 아이덴티티는 가장 중요합니다. 이 시장에는 Infineon Technologies AG, Renesas Electronics Corporation, Texas Instruments Incorporated, STMicroelectronics NV 등 유명한 기존 기업이 진입하고 있으며 시장 침투도가 높습니다.

2023년 9월 GlobalFoundries와 Microchip Technology는 Microchip의 자회사인 SST(Silicon Storage Technology)를 통해 SST ESF3 3세대 임베디드 SuperFlash 기술 NVM 솔루션을 발표했습니다. GF 28SLPe 파운드리 프로세스에서 생산이 가능해진 이 최첨단 솔루션은 GF 고객으로부터 높은 평가를 받고 있습니다. 탁월한 성능, 탁월한 신뢰성, 다양한 IP 옵션, 비용 효율성을 자랑하며 고급 MCU, 복잡한 스마트 카드, 소비자 및 산업용 IoT 칩에 이상적인 용도을 찾을 수 있습니다.

Samsung Electronics는 2023년 6월 올인원 결제 솔루션을 특징으로 하는 생체인증 카드 IC를 발표하고 혁신적인 결제 체험을 약속했습니다. 이 새로운 지문 보안 칩은 CES 2023의 사이버 보안 및 개인 프라이버시 부문에서 Best of Innovation Awards를 수상하여 높은 평가를 받았습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 및 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

경쟁 기업간 경쟁 관계

대체품의 위협

업계 밸류체인 분석

COVID-19와 거시 경제 동향 시장에 대한 영향

제5장 시장 역학

시장 성장 촉진요인

디지털 기술의 급속한 개발

정부에 의한 교통 시스템 투자 증가

시장의 과제

모바일 월렛이나 디지털 월렛의 보급 확대

제6장 시장 세분화

제품별

8비트

16비트

32비트

기능별

거래

통신

보안 및 액세스 제어

최종 사용자 산업별

BFSI

통신업계

정부 및 헬스케어

교육

소매

운수

기타 최종 사용자 산업

지역별

북미

유럽

아시아

호주 및 뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

NXP Semiconductors NV

Renesas Electronics Corporation

Infineon Technologies AG

STMicroelectronics

Microchip Technology Inc.

Idemia Group

Thales group

Giesecke Devrient

Zilog, Inc.

Samsung Electronics Co. Ltd

제8장 투자 분석과 시장 전망

SHW

영문 목차

영문목차

The Smartcard MCU Market size is estimated at USD 3.50 billion in 2025, and is expected to reach USD 4.52 billion by 2030, at a CAGR of 5.29% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 9.32 billion units in 2025 to 15.53 billion units by 2030, at a CAGR of 10.74% during the forecast period (2025-2030).

Key Highlights

The Internet's rapid expansion has made electronic shopping a real possibility among computer users if not a habit; nevertheless, the present business model used in electronic commerce applications cannot fully exploit the potential of the electronic medium.

The market growth is driven by the increasing development in RFID technology and NFC in smart cards. Contactless smart cards, leveraging the rapid evolution of radio frequency identification (RFID) technology, are gaining popularity. These cards use RFID technology to process transactions. Key vendors are concentrating on introducing contactless smart cards due to their growing consumer demand, which is expected to fuel market growth.

The proliferation of smart card technology in the transportation industry, along with growing government investments in implementing digital technology, drives market growth. Electronic smart cards are now viable alternative payment methods for transport operators. In recent years, many operators and system providers have initiated smart card-based systems either to complement or replace existing payment methods.

Furthermore, security and miniaturization represent the two fastest-evolving aspects of smart card technology. With global migration to higher security EMV banking cards, the newest generation of smart cards boasts full on-chip cryptography, significantly enhancing industry-wide card security.

Moreover, smart cards are increasingly being miniaturized into diverse form factors like mini-tags and smart wearables. These trends will persist as smart cards are increasingly employed as a two-factor credential alongside phones or biometrics.

The primary challenge facing smart cards is their security level. To realize their full potential, smart cards must interact with various interfaces. However, a security issue arises concerning public perception; people might need to be made aware of the personal details stored on their cards, assuming they are secure. Yet, there needs to be an awareness that information extracted from smart cards is collected and analyzed elsewhere.

Smartcard MCU Market Trends

BFSI to Witness the Growth

Smart cards for banking and finance now incorporate specialized integrated circuit cards, ensuring robust security measures. These cards house embedded memory chips and microprocessors, enabling secure data storage and processing. They serve diverse functions in financial activities, including transaction authentication, secure access to online banking services, debit and credit card payments, and contactless payment methods.

The digitization of payment processes owes much to the Internet's development and the emergence of e-commerce. This transition has led to a plethora of electronic payment options, ranging from payment cards (credit and debit) to digital wallets, electronic cash, and contactless payment methods. The surging popularity of mobile payment services is currently undergoing a transitional phase, poised for future technological advancements. These advancements in payment methods are expected to leverage smart card technology, driving market growth.

Smart cards featuring MCUs (microcontroller units) are commonly used alongside personal identification numbers (PINs). They serve multiple purposes, enhancing organizational security, acting as multifactor authentication (MFA) tokens, and verifying single sign-on (SSO) users, ultimately facilitating passwordless authentication. The rapid increase in online transactions, partly due to the pandemic and the rise of alternative payment methods like Apple Pay, Klarna, Stripe, and Amazon Pay, has surpassed face-to-face transactions. These advancements significantly expand the potential applications of smart card technology in the industry.

EMV card technology, employing compact yet robust chips integrated into credit and debit cards, is increasingly recognized as an evolving payment solution. EMV, an acronym for Europay, Mastercard, and Visa, denotes the collaborative efforts behind this industry standard. These advanced cards are indispensable in fortifying businesses and customer security by mitigating credit card fraud losses, fostering a more secure payment environment, and ensuring a safer transactional experience.

Most new EMV cards and chip-based readers come equipped with near-field communication (NFC) technology, enabling contactless payments. Customers can wave their cards across the reader, facilitating quicker and more secure transactions. Besides heightened security, EMV smart cards offer enhanced speed and convenience by securely communicating between the card and the terminal, benefitting both merchants and cardholders.

EMV cards, featuring chips employing cryptographic algorithms, heighten transaction security by uniquely encrypting data with each use. During card-present transactions, these cards employ a dual verification process, requiring the physical card and the customer's PIN. This authentication method validates the cardholder, enabling the confirmation and approval of the one-time password (OTP) generated by the chip. Anticipated technological advancements are poised to stimulate extensive demand for smart card technology, propelling market growth in the foreseeable future.

Asia-Pacific Expected to Hold Significant Market Share

The adoption of smart card technology in the APAC is experiencing a change towards multi-application smart cards. These cards are being used for multiple purposes, such as payment, identification, and access control, resulting in greater convenience and efficiency for consumers and cost savings for businesses. Moreover, the need for enhanced security features in smart cards has been growing, particularly with the increase in online transactions.

Smart card technology has gained widespread popularity in India, owing to the government's focus on digitalization. Almost every Indian citizen probably possesses some form of a smart card. These cards are extensively utilized in various sectors, such as banking, healthcare, transportation, and government identification. For example, smart cards are employed for Driving License/Vehicle Registration Certificate (DL/RC), Multi-purpose National Identity Card (MNIC), Rashtriya Swasthya Bima Yojana (RSBY), and Electronic Passport (e-Passport) in India. The increasing adoption of smart card technology in the region is expected to drive the market.

The near future is expected to witness a surge in the demand for digital payments and smart cards. The Indian BFSI sector is progressively embracing smart card technology, which is anticipated to provide substantial prospects for MCU makers. Notably, insurance companies operating under the Rashtriya Swasthya Bima Yojana (RSBY) and business correspondents for banks are producing millions of chip cards, making India one of the swiftest adopters of smart card technology. Such factors are expected to drive the demand for the market.

In addition, implementing smart card technology in India has benefited social welfare programs and transportation systems, as it has improved the quality of life for the general public. An example is the Shakti smart card scheme, which enables women residing in Karnataka to travel freely on non-premium buses. According to EMVCo, the Smart Card India initiative has reduced transaction time, minimized losses, and increased satisfaction among beneficiaries. The utilization of innovative technologies like smart cards has the potential to enhance future welfare programs.

Smart cards equipped with MCUs that possess the ability to establish short-range wireless connections have the potential to be utilized in contactless payment systems. As the usage of contactless cards continues to rise and their adoption rates increase within the region, the volume of payments conducted through this method has experienced a substantial surge, consequently generating a notable market demand.

Smartcard MCU Market Overview

The smartcard MCU market demonstrates semi-consolidation, marked by intensifying competition among major players. This landscape is characterized by fluctuations influenced by growing consolidation, technological advancements, and evolving geopolitical scenarios. With a pronounced emphasis on innovation for sustainable competitive advantage, competition is poised to escalate, buoyed by the anticipated surge in demand from new customers within end-user industries.

In this context, brand identity assumes paramount importance, given the expectations of quality from end-users in microcontroller manufacturing. The market features prominent incumbents like Infineon Technologies AG, Renesas Electronics Corporation, Texas Instruments Incorporated, and STMicroelectronics NV, resulting in high market penetration levels.

September 2023 witnessed the unveiling of the SST ESF3 third-generation embedded SuperFlash technology NVM solution by GlobalFoundries and Microchip Technology, introduced through Microchip's subsidiary, Silicon Storage Technology (SST). Now available for production in the GF 28SLPe foundry process, this cutting-edge solution has garnered commendation from GF's clientele. It boasts remarkable performance, exceptional reliability, a diverse array of IP options, and cost efficiency, finding ideal applications in advanced MCUs, intricate smart cards, and IoT chips for consumer and industrial use.

In June 2023, Samsung Electronics introduced a biometric card IC featuring an all-in-one payment solution, promising an innovative payment experience. This new fingerprint security chip earned recognition as the winner of the CES 2023 Best of Innovation Awards in the Cybersecurity & Personal Privacy category.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Intensity of Competitive Rivalry

4.2.5 Threat of Substitutes

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 and Macroeconomic Trends on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rapid Development of Digital Technologies

5.1.2 Increasing Investments by Governments in Transportation Systems

5.2 Market Challenges

5.2.1 Growing Popularity of Mobile or Digital Wallets