북미의 수축 및 스트레치 필름 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

North America Shrink And Stretch Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690949

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

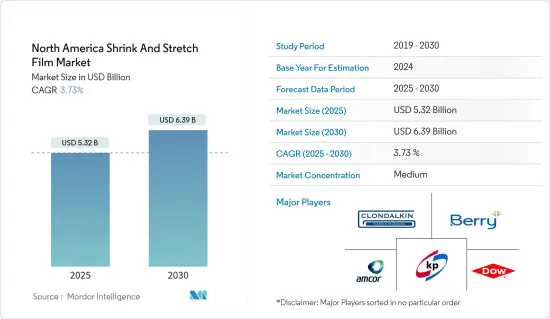

북미의 수축 및 스트레치 필름 시장 규모는 2025년에 53억 2,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 3.73%로 성장할 전망이며, 2030년에는 63억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

수축 및 스트레치 필름은 첨단 기술로 제조된 폴리스티렌 필름입니다. 이러한 필름은 포장용으로 사용되며 유연성과 신축성 측면에서 차별화된 고유의 화학적 특성을 가지고 있습니다. 스트레치 필름은 유연하고 신축성이 뛰어난 얇은 폴리에틸렌 필름으로 팔레트의 수하물에 감는 데 사용되는 반면, 수축 필름은 얇은 필름으로 하나의 제품과 제품에 감겨 포장에 열이 필요합니다. 이 필름은 공기와 습기에 의한 제품의 부패를 방지하고 포장된 제품의 품질을 향상시킵니다.

수축 슬리브 라벨은 360도 인쇄된 라벨을 말하며, 라벨을 붙이는 제품의 모양에 맞게 열을 가하는 것이 일반적입니다. 수축 슬리브 라벨은 플라스틱 또는 폴리에스테르 필름 소재의 양면에 인쇄됩니다. 수축 슬리브의 내구성은 습기 및 마찰에 노출되는 제품에 이상적입니다.

다양한 브랜드들이 2025년 지속가능성 목표에 초점을 맞추고 있는 가운데, 더 많은 지속가능성 선택을 모색하는 것은 그 맹세를 달성하는데 있어서 점점 더 중심이 되고 있습니다. 많은 플라스틱 병 음료 제조업체는 골판지 및 판지보다 재활용 가능한 폴리에틸렌(PE) 수축 필름을 선택합니다.

암코는, PE 수축 필름이 미국에서 가장 재활용되는 플라스틱 필름 중 하나이며 북미 18,000곳 매장의 드롭오프 로케이션을 통해 회수되고 있다고 말합니다. 포스트 소비자 재활용(PCR) 컨텐츠를 사용하여 순환 경제의 고리를 닫는 노력을 확대함으로써 표준 PE 수축 필름과 동일한 다목적성과 성능을 제공하면서 지속 가능한 이점을 얻을 수 있습니다.

기능적 이점 외에도 스트레치 필름 및 수축 필름에는 물류상의 이점이 있습니다. 이러한 필름을 사용하면 벌크 제품의 취급 및 보관이 용이해지고 창고 효율이 크게 향상됩니다. 한편, 수축 포장된 다발은 콤팩트하고 적층이 용이하기 때문에 보관 시설이나 차량내의 공간 이용이 최적화됩니다. 그 결과 기업은 비용 절감을 달성하고 공급망의 전반적인 업무 효율성을 향상시킬 수 있습니다.

북미의 수축 및 스트레치 필름 시장 동향

식음료 산업이 대폭적인 시장 성장을 이룹니다.

주로 선형 저밀도 폴리에틸렌(LLDPE)으로 만들어진 스트레치 필름은 북미의 식음료 산업의 핵심입니다. 팔레타이징에 이상적이며 운송 중 제품의 안전성을 보장하고 편차로 인한 잠재적 손상을 방지합니다. 신축성과 견고성으로 유명한 이 필름은 다양한 모양과 크기의 제품에 능숙하게 적합하며 먼지와 습기와 같은 외부 요인으로부터 안정성 및 차폐성을 제공합니다.

한편, 수축 필름은 종종 폴리올레핀과 폴리 염화 비닐(PVC)로 만들어지며 그 역할은 다르지만 마찬가지로 중요합니다. 수축 필름은 열을 가하면 수축하고 상품을 딱 감싸고 단단히 밀봉합니다. 이 기능은 병, 캔, 상자 등의 상품을 묶는 데 이상적이며 취급 및 운송이 간단합니다. 또한, 변조 방지 씰은 제품의 무결성을 유지하고 식품 및 음료 분야에서 소비자의 신뢰를 높이는 데 매우 중요합니다.

스트레치 필름 및 수축 필름도, 식음료의 유통 기한을 연장하는데 있어서 매우 중요합니다. 먼지, 습기, 미생물 등 오염물질에 대한 보호 실드 역할을 하는 이 필름은 제품의 신선도와 품질을 유지하는 데 도움이 됩니다. 이러한 요소는 보관 및 운송 중 엄격한 위생 관리 및 온도 관리가 필요한 신선한 식품에 특히 중요합니다. 유통 기한을 연장함으로써, 이러한 필름은 식품 폐기에 대항할 뿐만 아니라 소비자가 최고의 상태로 제품을 받도록 보장합니다.

상품의 시인성을 높이고, 선반에 진열할 때의 어필을 강화하는 것도, 스트레치 필름 및 수축 필름의 장점으로 삼는 부분입니다. 투명하고 광택있는 수축 필름은 포장된 제품을 우아하게 보여줄 수 있으며, 시각적 매력이 소비자의 선택을 크게 좌우하는 소매 현장에서 특히 특이합니다. 또한 제조업체는 브랜드 이름과 제품 세부 사항을 필름에 직접 인쇄할 수 있으므로 라벨 및 포장 재료를 추가할 필요가 줄어들고 포장 공정이 간소화됩니다.

2023년 12월 미국 인구조사국의 데이터에 따르면 미국 음식점에 의한 월간 소매 매출은 약 903억 달러에 달하였고, 전월보다 7.4% 증가했습니다. 이 소매 매출 증가는 특히 야채, 과일, 생선, 고기와 같은 포장용 필름에 대한 수요 증가를 뒷받침합니다.

미국이 시장의 대부분을 차지할 전망

미국에서 수축 및 스트레치 필름 수요 증가는 주로 효과적인 포장, 묶음, 창고 보관 및 유통 시 상품 보호에 대한 요구가 증가하고 있습니다. 게다가 이 지역에서는 소비자 산업으로부터 이러한 필름에 대한 왕성한 수요를 강조하는 연례 프로그램이 개최되고 있습니다.

미국에서는 가공 식품의 소비가 현저하게 증가하고 있으며, 그에 따라 스트레치 필름 및 수축 필름의 요구도 높아지고 있습니다. 소비자의 편의점 식품 지향이 높아짐에 따라 효율적인 패키징 솔루션의 중요성이 커지고 있습니다. 특히 수축 필름은 냉동식품, 스낵팩, 조리된 제품 등을 묶어 보호하는 역할을 하기 때문에 높은 수요가 있습니다.

수축 필름은 밀폐성이 높고 변조를 방지할 수 있는 것으로 알려져 있으며 가공식품 분야에서는 특히 비중이 높고 신선도 및 안전성을 모두 보장하고 있습니다. 게다가 투명하고 광택 있는 마무리는 제품의 시인성을 높일 뿐만 아니라 경쟁이 치열한 소매 업계에서 매우 중요한 장점인 선반에 대한 어필력을 높입니다. 이러한 시각적 매력과 수축 필름의 보호 특성이 결합되어 식품 회사는 소비자를 끌어들여 제품의 무결성을 보장할 수 있습니다.

음료용 병의 소비량이 많은 것도 수축 및 스트레치 필름 수요를 견인하고 있습니다. 특히 수축 필름은 6개나 12개들이 같은 음료병의 멀티팩에 선호되고 있습니다. 병의 모양에 딱 맞는 능력은 매력적이고 안정적인 패키지를 보장하고 소비자의 취급을 용이하게 합니다. 또한 수축 필름을 통한 변조 방지 씰은 제품 안전에 대한 소비자의 신뢰를 더욱 높입니다. 미국에서는 병에 담긴 음료의 소비량이 증가하고 있기 때문에 스트레치 필름 및 슈링크 필름과 같은 패키징 솔루션에 대한 수요도 증가의 길을 따라가고 있습니다.

이 지역 시장 기업은 시장에서의 지위를 높이고 고객 기반을 확대하기 위해 적극적으로 제품을 혁신하고 새로운 제품을 발표합니다.

음료 업계 잡지에 따르면, 미국의 프라이빗 브랜드 식수 매출은 2023년 5월 21일까지 52주 동안 53억 달러를 돌파했습니다. 건강한 수분 보급에 대한 소비자의 관심 증가를 배경으로 한 병에 담긴 음료수의 판매 급증은 수축 필름 및 스트레치 필름의 소비에 큰 영향을 주어 이러한 소재에 대한 수요를 더욱 촉진할 전망입니다.

북미의 수축 및 스트레치 필름 산업 개요

북미의 수축 및 스트레치 필름 시장은 많은 기업들이 패키징 업계에 진입함에 따라 단편화되고 있습니다. 또한 기업의 기술 혁신과 개발이 시장 경쟁을 격화시키고 있습니다.

2023년 8월-패키징 솔루션 제공업체인 Group O는 패키징의 지속가능성을 재정의하는 신제품을 제공하는 북미에서 유일한 대리점으로 선정되었습니다. 이 회사가 제공하는 제품은 소비자 재생 이용(PCR) 원료를 30% 사용한 최초의 기계용 스트레치 필름입니다. 이 제품은 최첨단 성능과 지속가능성이 융합되어 책임있는 상거래의 미래를 형성하는 패키징 영역에서 큰 도약을 보여줍니다.

2023년 4월-Holden Industries Inc.의 자회사인 Nosco Inc.는 StretchPak 및 기타 카드 포장 용도로 자체 EcoClear 필름을 출시한다고 발표했습니다. 이 PVC 프리 필름은 선도적인 소매업체의 지속가능성 요구에 부응하기 위해 전략적으로 개발되었습니다. 제품의 외관을 향상시키기 위해 투명도가 높은 디스플레이를 제공합니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도-Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

서큘러 이코노미를 중시한 산업 생태계 분석

규제 프레임워크

수축 및 스트레치 필름의 가격 분석

제5장 시장 역학

시장 성장 촉진요인

산업 부문에서 수요 증가

자재관리에 있어서 변조 방지의 필요성

시장의 과제

재활용의 과제

제6장 시장 세분화

제품 유형별

후드

랩

슬리브 라벨

재료별

저밀도 폴리에틸렌(LDPE) 및 선형 저밀도 폴리에틸렌(LLDPE)

폴리염화비닐(PVC)

폴리에틸렌테레프탈레이트(PET)

기타 재료

최종 이용 산업별

음식

소비재

의약품

공업용

기타 최종 이용 산업

지역별

미국

캐나다

제7장 경쟁 구도

기업 프로파일

Berry Global Inc.

Klockner Pentaplast Group

Amcor Group GmbH

Clondalkin Group Holdings BV

Dow Inc.

Taghleef Industries LLC

Sealed Air Corporation

Intertape Polymer Group Inc.

Emsur Macdonell SA

Transcontinental Inc.

히트 맵 분석

경쟁자 분석-신흥 기업 및 기성 기업

제8장 투자 분석

제9장 시장의 미래

AJY

영문 목차

영문목차

The North America Shrink And Stretch Film Market size is estimated at USD 5.32 billion in 2025, and is expected to reach USD 6.39 billion by 2030, at a CAGR of 3.73% during the forecast period (2025-2030).

Key Highlights

Stretch and shrink films are polythene films made with advanced engineering. These films are used for packing items and have unique chemical properties that differentiate them in terms of flexibility and stretchability. Stretch films are thin polythene films that are flexible and elastic and are used to wrap around pallet loads, whereas shrink films are thin films wrapped around a single product or commodity and require heat to pack. These films help keep items from spoiling due to air and moisture, improving the quality of packed goods.

Shrink sleeve labels refer to 360-degree printed labels that typically use heat in the application process to conform to the product's shape to which the label is applied. Shrink sleeve labels are printed on either side of the plastic or polyester film materials. The durability of the shrink sleeves makes them ideal for products that encounter moisture or friction.

With various brands increasing their focus on sustainability goals for 2025, exploring more sustainability options is becoming increasingly central to meeting their pledges. Many bottled beverage producers are choosing recycle-ready polyethylene (PE) shrink film over corrugate and paperboard because it uses less energy and lowers greenhouse emissions in the distribution channel without compromising run speeds and machinability.

Amcor stated that PE shrink is one of the most recycled types of plastic films in the United States, collected through the 18,000 in-store drop-off locations in North America. Expanding efforts to close the loop on a circular economy with post-consumer recycled (PCR) content can achieve additional sustainability benefits while providing the same versatility and performance as standard PE shrink films.

In addition to their functional benefits, stretch and shrink films offer logistical advantages. The use of these films can significantly improve warehouse efficiency by enabling easier handling and storage of bulk products. Shrink-wrapped bundles, on the other hand, are compact and easier to stack, optimizing space utilization in storage facilities and vehicles. As a result, companies can achieve cost savings and improve overall operational efficiency in their supply chains.

North America Shrink and Stretch Film Market Trends

The Food and Beverage Industry is Witnessing Significant Market Growth

Stretch film, primarily crafted from linear low-density polyethylene (LLDPE), is a cornerstone in the North American food and beverage industry. It is the go-to choice for palletizing, ensuring products remain secure during transit, thus averting potential damages from shifting. Renowned for its elasticity and robustness, this film adeptly conforms to products of varied shapes and sizes, providing stability and shielding against external elements like dust and moisture.

On the other hand, shrink film, often fashioned from polyolefin or polyvinyl chloride (PVC), serves a distinct yet equally vital role. When subjected to heat, it contracts, snugly enveloping the goods and creating a secure seal. This feature makes it perfect for bundling items like bottles, cans, and boxes, simplifying handling and transportation. Furthermore, its tamper-evident seal is pivotal in upholding product integrity and bolstering consumer trust in the food and beverage domain.

Both stretch and shrink films are pivotal in prolonging the shelf life of food and beverage items. Acting as a protective shield against contaminants such as dust, moisture, and microbes, these films are instrumental in preserving product freshness and quality. These factors are especially crucial for perishables, demanding stringent hygiene and temperature controls during storage and transit. By extending shelf life, these films not only combat food wastage but also ensure consumers receive products in prime condition.

Enhancing product visibility and shelf appeal is another forte of stretch and shrink films. Shrink film, with its clear, glossy finish, elegantly showcases packaged products, a feature particularly prized in retail settings where visual allure can sway consumer choices significantly. Furthermore, manufacturers can directly print branding and product details on the film, reducing the need for additional labels and packaging materials, thereby streamlining the packaging process.

According to data from the US Census Bureau for December 2023, monthly retail sales from US food and beverage stores hit around USD 90.3 billion, marking a notable 7.4% surge from the preceding month. This uptick in retail sales underscores the heightened demand for films, especially for packaging items like vegetables, fruits, fish, and meat.

The United States is Expected to Hold the Majority Share in the Market

The rising demand for shrink and stretch films in the United States is primarily fueled by the growing need for effective packaging, bundling, and safeguarding of goods during warehousing and distribution. Additionally, the region hosts annual programs highlighting the robust demand for these films from consumer industries.

With a notable surge in processed food consumption, the United States has witnessed a corresponding uptick in the need for stretch and shrink films. As consumers increasingly favor convenience foods, the importance of efficient packaging solutions has escalated. Shrink films, in particular, are in high demand, given their role in bundling and safeguarding items like frozen meals, snack packs, and ready-to-eat products.

Shrink films, known for their ability to create a tight, tamper-evident seal, are especially prized in the realm of processed foods, ensuring both freshness and security. Furthermore, their clear, glossy finish not only enhances product visibility but also boosts shelf appeal, a crucial advantage in the fiercely competitive retail landscape. This visual allure, coupled with the protective attributes of shrink films, aids food companies in attracting consumers and ensuring product integrity.

The significant consumption of beverage bottles is yet another driver for the demand for stretch and shrink films. Shrink films, in particular, are favored for crafting multi-packs of beverage bottles, such as six or twelve-packs. Their ability to snugly conform to bottle shapes ensures an appealing and stable package and makes them easier for consumers to handle. Moreover, the tamper-evident seal provided by shrink films further bolsters consumer confidence in product safety. Given the escalating consumption of bottled beverages in the United States, the demand for packaging solutions like stretch and shrink films is poised for a corresponding rise.

Market players in the region have been actively innovating their products and launching new offerings to bolster their market standing and expand their customer base.

According to the Beverage Industry Magazine, sales of private-label bottled still water in the United States surpassed USD 5.3 billion for 52 weeks ending May 21, 2023. This surge in bottled still water sales, driven by heightened consumer interest in healthy hydration, is poised to significantly impact the consumption of shrink and stretch films, further propelling demand for these materials.

North America Shrink and Stretch Film Industry Overview

The North American shrink and stretch film market is fragmented due to many players entering the packaging industry. Moreover, innovations and developments by players are making the market competitive.

August 2023: Packaging solutions provider Group O was selected as one of the only distributors in North America to offer a new product that redefines sustainability in packaging. The product offered by the company is a first-ever machine-grade stretch film with 30% post-consumer recycled (PCR) content. This product marks a significant leap in the realm of packaging, where cutting-edge performance meets sustainability, shaping the future of responsible commerce.

April 2023: Nosco Inc., a subsidiary of Holden Industries Inc., announced the launch of its exclusive EcoClear Film for StretchPak and other carded packaging applications. This PVC-free film was strategically developed to meet the sustainability demands of major retailers. It offers a crystal-clear display for enhanced product appearance.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Ecosystem Analysis with an Emphasis on Circular Economy

4.4 Regulatory Framework

4.5 Shrink and Stretch Film Pricing Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand From Industrial Sector

5.1.2 The Need for Tamper-evident Protection in Material Handling

5.2 Market Challenges

5.2.1 Recycling Challenges

6 MARKET SEGMENTATION

6.1 Product Type

6.1.1 Hoods

6.1.2 Wraps

6.1.3 Sleeve Labels

6.2 Material

6.2.1 Low-density Polyethylene (LDPE) and Linear Low-density Polyethylene (LLDPE)

6.2.2 Polyvinyl chloride (PVC)

6.2.3 Polyethylene terephthalate (PET)

6.2.4 Other Materials

6.3 End-use Industry

6.3.1 Food and Beverage

6.3.2 Consumer Goods

6.3.3 Pharmaceutical

6.3.4 Industrial

6.3.5 Other End-use Industries

6.4 Geography

6.4.1 United States

6.4.2 Canada

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Berry Global Inc.

7.1.2 Klockner Pentaplast Group

7.1.3 Amcor Group GmbH

7.1.4 Clondalkin Group Holdings BV

7.1.5 Dow Inc.

7.1.6 Taghleef Industries LLC

7.1.7 Sealed Air Corporation

7.1.8 Intertape Polymer Group Inc.

7.1.9 Emsur Macdonell SA

7.1.10 Transcontinental Inc.

7.2 Heat Map Analysis

7.3 Competitor Analysis - Emerging Vs. Established Players