ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

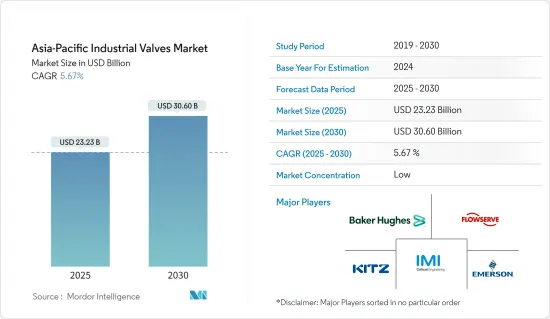

아시아태평양의 산업용 밸브 시장 규모는 2025년에 232억 3,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 5.67%를 나타낼 전망이며, 2030년에는 306억 달러에 이를 것으로 예측됩니다.

주요 하이라이트

COVID-19 팬데믹은 산업용 밸브 시장에 있어서 큰 과제였습니다. 전 세계 제조업체의 공급망에 직접적인 영향을 미치고 바이러스 확산 위험을 최소화하기 위해 생산 설비를 중단했습니다.

시장을 견인하는 요인은 수처리 플랜트나 석유 및 가스 산업으로부터의 밸브 수요 증가입니다.

또한, 하류 시장에서 보다 폭넓은 용도로 밸브를 사용할 수 있도록 할 필요성이 아시아태평양의 밸브 시장의 성장에 기여하고 있습니다.

아시아태평양 산업용 밸브 시장에서는 중국이 최대의 점유율을 차지하고 있습니다.

아시아태평양의 산업용 밸브 시장 동향

석유 및 가스 산업 수요 증가

업스트림의 석유 및 가스 산업은 수백만의 갱구의 '크리스마스 트리'에 장착하는 밸브의 최대 유저이며, 통상 1개당 3-5개의 밸브(사이즈 2-8')를 포함합니다.

각국에 걸친 파이프라인 증가에 따라 탄화수소를 저장하기 위한 저장기지의 필요성도 높아집니다. 따라서 아시아 태평양 국가들은 수요를 충족시키기 위해 저장 터미널에 투자를 계획하고 있습니다.

아시아태평양은 석유 및 가스 하류 시장을 독점하고 있으며, 수요의 대부분은 중국, 동남아시아 국가, 인도에서 초래되고 있습니다. 에너지 수요는 20년간 50-60% 성장할 것으로 예상되고 있습니다.

중국은 2030년까지 약 85억 달러를 투자하여 23개 가스 저장 시설을 건설할 예정입니다. 저장 시설의 완성과 향후 예정된 가스 파이프라인은 중류 부문을 활성화시킬 것으로 예상됩니다. 그 결과 석유 제품 수요는 10년대 중반까지 650MT를 넘어설 것으로 예상되며, 그 중에서도 수송 부문 수요가 370MT 가까이로 가장 높습니다.

이 지역에서는 여러 석유화학 프로젝트의 건설이 예정되어 있습니다. 예를 들어, 중국에서는 2021-2025년 512개의 석유화학 프로젝트가 조업을 시작할 것으로 예상되고 있습니다. 국제에너지기구(IEA)가 발표한 석유화학 보고서에 따르면 유럽을 제외한 거의 모든 지역에서 2050년까지 1차 화학품 생산이 증가할 가능성이 있습니다. 그러나, 가장 생산 능력이 성장하는 것은 아시아태평양입니다.

또한 중국은 에너지 공급을 확보하기 위해 셰일 오일전과 같은 국내 프로젝트를 강화함으로써 증가하는 가스 수입 의존도를 삭감하는 것을 목표로 하고 있습니다. 정부는 특히 셰일가스와 같은 비재래형 가스원에서 국내 생산을 촉진하기 위한 새로운 노력에 자금을 제공할 것으로 예상됩니다. 또, 중국의 셰일가스 생산량은 2035년까지 약 2,800억 입방미터에 달할 것으로 추정되고 있습니다. 따라서 셰일가스 생산을 촉진하기 위한 중국 정부의 노력과 계획은 향후 몇 년간 산업용 밸브에 호기를 창출할 것으로 예상됩니다.

이러한 요인은 산업용 밸브 수요를 증가시킬 것으로 예상됩니다.

인도가 가장 빠른 성장을 기록할 전망

인도는 제조업과 기계분야에서 가장 급성장하는 국가 중 하나이며, 산업용 밸브의 요구를 창출하고 있습니다. 인도 정부는 제조 부문을 설립하는 기업에 대해 편의를 도모하고 있습니다. 또, 제조 부문을 지지하기 위해서 여러가지 시책을 내놓고 있습니다. 예를 들면, India Brand Equity Foundation(IBEF)에 의하면, 2023년, 인도의 제조업 수출은 사상 최고를 기록했으며 4,474억 6,000만 달러에 이르렀고 4,220억 달러였던 전년보다 6.03%의 성장을 나타냈습니다.

인도는 세계 제3위의 전력 생산 및 소비국이며, 2024년 1월 31일 설비 용량은 429.96GW였습니다.

인도는 광업이 번성합니다. 2022년도에는 총 1,319개의 광산이 보고되었으며, 그 중 545개가 금속광물, 775개가 비금속광물에 특화되어 있습니다. 또한 India Brand Equity Foundation(IBEF)이 발표한 데이터에 따르면 2022-2023년 인도의 철광석 수출액은 17억 5,000만 달러였고 2021-2022년도는 31억 8,000만 달러였습니다.

인도의 제약산업은 세계적으로 중요한 지위를 차지하고 있으며, 생산량은 3위, 생산액은 14위입니다. India Brand Equity Foundation(IBEF)의 예측에 의하면, 이 산업의 시장 규모는 2024년에 650억 달러에 이르렀으며, 2030년에는 2배의 1,300억 달러, 2047년에는 경이적인 4,500억 달러로 급증할 전망입니다.

석유 및 가스 산업은 인도의 8개의 기간 산업 중 하나이며 경제의 다른 중요한 부문 모든 의사결정에 큰 영향을 미치는 역할을 담당하고 있습니다. 인도의 석유 수요는 세계적으로 급증해 2030년에는 하루 1,000만 배럴에 이를 것으로 예측되고 있습니다.

국제에너지기구(IEA)에 따르면 인도의 천연가스 소비량은 250억 입방미터(bcm) 증가하여 2024년까지 연평균 9%의 성장이 평가되었습니다.

이러한 요인에 의해 예측 기간 중 인도의 산업용 밸브 수요가 증가할 가능성이 높습니다.

아시아태평양의 산업용 밸브 산업 개요

아시아태평양의 산업용 밸브 시장은 세분화되어 있으며 모든 기업이 큰 점유율을 얻지 못했습니다. 이 시장의 주요 참가 기업에는, Emerson Electric Co., KITZ Corporation, Flowserve Corporation, Baker Hughes, IMI Critical Engineering 등이 있습니다(순부동).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

수처리 플랜트에서 밸브 수요 증가

석유 및 가스 산업에서 밸브 수요 증가

기타 촉진요인

성장 억제요인

높은 설비 투자가 시장 성장 방해

산업 밸류체인 분석

산업의 매력-Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형별

나비 밸브

볼 밸브

글로브 밸브

게이트 밸브

플러그 밸브

기타

제품별

1/4 회전 밸브

멀티턴 밸브

기타 제품(컨트롤 밸브)

용도별

전력

상하수도 관리(해수 담수화 포함)

금속 및 광물, 광업

기타

화학제품별

석유 및 가스

상류

중류

하류

식품가공

펄프 및 제지

기타

지역별

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

제6장 경쟁 구도

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Alfa Laval

AVK Holding AS

Baker Hughes

CIRCOR International Inc.

Crane Co.

Curtiss-Wright Corporation

Danfoss AS

EBRO ARMATUREN Gebr. Brer GmbH

Emerson Electric Co.

Flowserve Corporation

Georg Fischer Ltd

Hitachi Metals Ltd

Honeywell International Inc.

IMI Critical Engineering

ITT Inc.

KITZ Corporation

NIBCO

Okano Valve Mfg. Co. Ltd

PARKER HANNIFIN CORP.

SAMSON AKTIENGESELLSCHAFT

Schlumberger Limited

The Weir Group PLC

Valvitalia SpA

Velan Inc.

제7장 시장 기회 및 향후 동향

AJY

영문 목차

영문목차

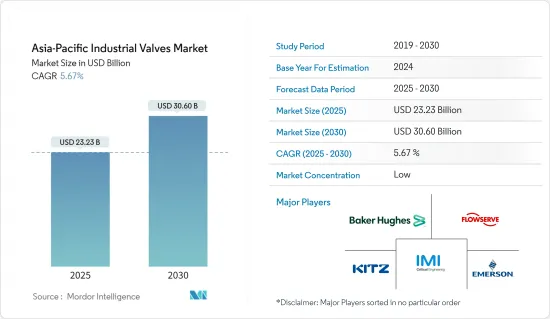

The Asia-Pacific Industrial Valves Market size is estimated at USD 23.23 billion in 2025, and is expected to reach USD 30.60 billion by 2030, at a CAGR of 5.67% during the forecast period (2025-2030).

Key Highlights

The COVID-19 pandemic was a major challenge for the industrial valves market. It directly affected the manufacturer's supply chain across the globe and shut down the production facilities to minimize the risk of spreading the virus.

The factors driving the market are increasing demand for valves from water treatment plants and the oil and gas industry.

Further, the need to enable valves for a wider range of applications in the downstream market is contributing to the growth of the Asia-Pacific valves market.

China accounts for the largest share of the Asia-Pacific industrial valves market.

Asia-Pacific Industrial Valves Market Trends

Growing Demand in the Oil and Gas Industry

The upstream oil and gas industry is the largest user of valves to outfit millions of wellhead 'Christmas trees' that usually include 3 to 5 valves per tree in sizes of 2' to 8', as well as to segment and control flow through millions of miles of gathering pipelines (2' to 20' valves) and cross-country trunk pipelines (up to 60' or larger) required to bring the crude oil and gas to refineries, and the refined product (gasoline, diesel, natural gas) to end-user markets.

With the increase in pipelines across the countries, the need for storage terminals to store hydrocarbons also increases. Therefore, Asia-Pacific countries plan to invest in storage terminals to meet the demand.

Asia-Pacific has dominated the oil and gas downstream market, with most of the demand coming from China, Southeast Asian countries, and India. The energy demand is anticipated to grow by 50-60% in two decades.

China is expected to build 23 gas storage facilities by 2030, with an investment of around USD 8.5 billion. Completing the storage facilities and the upcoming gas pipelines in the country are expected to boost the midstream sector. As a result, the demand for petroleum products is expected to cross 650 MT by the mid-decade, with the transportation segment having the highest demand of nearly 370 MT.

Several petrochemical projects are planned to be constructed in the region. For instance, China is expected to have 512 petrochemical projects commence operations in 2021-2025. According to a petrochemicals report published by the International Energy Agency (IEA), nearly all regions except Europe may increase the production of primary chemicals by 2050. However, the most significant capacity growth is seen in Asia-Pacific.

Also, China targets to slash its growing dependence on gas imports by boosting domestic projects like shale fields to secure its energy supply. The government is expected to fund new efforts to boost domestic production, particularly from unconventional sources like shale gas. It is also estimated that China's shale gas production will reach around 280 billion cubic meters by 2035. Thus, the Chinese government's effort and plan to boost its shale gas production are expected to create an opportunity for industrial valves in the coming years

Such factors are expected to augment the demand for industrial valves.

India is Expected to Register the Fastest Growth

India is one of the fastest-growing countries in terms of manufacturing sectors and machinery, giving rise to the need for industrial valves. The government provides benefits to companies setting up manufacturing units. It also outlines various policies to boost the manufacturing sector. For instance, as per the India Brand Equity Foundation (IBEF), in 2023, India's manufacturing exports hit a record high, reaching USD 447.46 billion, marking a 6.03% growth from the previous year, when exports stood at USD 422 billion.

India is the third-largest producer and consumer of electricity worldwide, with an installed power capacity of 429.96 GW as of January 31, 2024.

India boasts a thriving mining industry. In FY22, the country had a total of 1,319 reporting mines, with 545 dedicated to metallic minerals and 775 to non-metallic minerals. Moreover, according to the data published by the Indian Brand Equity Foundation (IBEF), during 2022-2023, India's iron ore exports amounted to USD 1.75 billion compared to USD 3.18 billion during 2021-2022.

India's pharmaceutical industry holds a significant position on the global stage, ranking third in production volume and 14th in production value. Projections from the India Brand Equity Foundation (IBEF) suggest that the industry's market size is set to hit USD 65 billion in 2024, double to USD 130 billion by 2030, and soar to a staggering USD 450 billion by 2047.

The oil and gas industry is among the eight core industries in India, playing a major role in influencing decision-making for all the other important sections of the economy. India's oil demand is projected to rise rapidly in the world, reaching 10 million barrels per day by 2030.

According to the International Energy Agency (IEA), natural gas consumption in India is expected to grow by 25 billion cubic meters (bcm), registering an average annual growth of 9% until 2024.

These factors will likely increase the demand for industrial valves in India during the forecast period.

Asia-Pacific Industrial Valves Industry Overview

The Asia-Pacific industrial valves market is fragmented, with no player capturing a significant share of the market. Some of the major players in the market include (not in any particular order) Emerson Electric Co., KITZ Corporation, Flowserve Corporation, Baker Hughes, and IMI Critical Engineering.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand for Valves from Water Treatment Plants

4.1.2 Increasing Demand for Valves in the Oil and Gas Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 High Capital Investment to Hamper the Market Growth

4.3 Industry Value Chain Analysis

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

5.1 By Type

5.1.1 Butterfly Valve

5.1.2 Ball Valve

5.1.3 Globe Valve

5.1.4 Gate Valve

5.1.5 Plug Valve

5.1.6 Other Types

5.2 By Product

5.2.1 Quarter-turn Valve

5.2.2 Multi-turn Valve

5.2.3 Other Products (Control Valves)

5.3 By Application

5.3.1 Power

5.3.2 Water and Wastewater Management (Including Desalination)