인도의 항공, 방위 및 우주 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

India Aviation, Defense, And Space - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690919

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

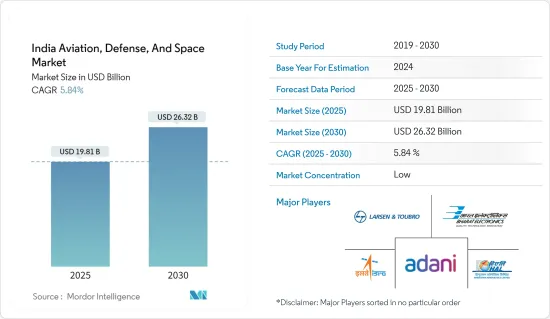

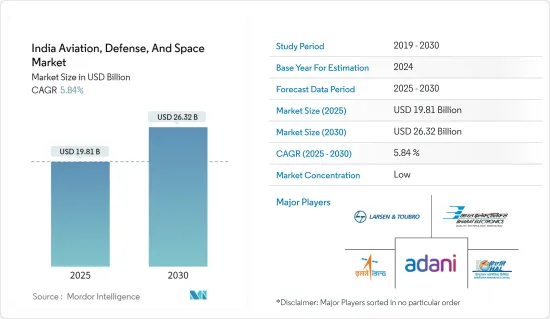

인도의 항공, 방위 및 우주 시장 규모는 2025년에 198억 1,000만 달러로 추정되고, 예측 기간 중 2025년부터 2030년까지 CAGR 5.84%로 성장할 전망이며, 2030년에는 263억 2,000만 달러에 이를 것으로 예측됩니다.

항공 여객의 요구를 충족시키기 위한 상용 항공기의 취득 증가, 상용 항공 사업 증가, 상용 공항 건설수 증가가 예측 기간 중 시장을 견인할 것으로 예상됩니다. 또한 인도의 국방예산 증가, 국방능력 향상을 위한 첨단무장 취득 증가, 우주개발계획 증가, 국산방위제조에 대한 정부지원 증가 등 향후 수년간 시장을 밀어올릴 것으로 예상됩니다.

반면 국내 규제 증가는 장기적으로 시장 성장을 방해할 것으로 예상됩니다. 또한 공항 건설 및 설계, 군사 훈련, 감시, 우주 미션의 정확성 향상 등 인공지능 등 첨단 기술의 이용이 확대되고 있기 때문에 다양한 시장 기회의 성장이 전망되고 있습니다.

인도의 항공, 방위 및 우주 시장 동향

현저한 성장을 보이는 민간 항공 부문

최근 몇 년동안 인도의 항공 부문은 눈부신 성장을 이어 세계 3위를 차지하고 있습니다. 이 급성장을 뒷받침하는 것은 주로 여행 의욕이 증가함에 따른 인구 증가입니다. 그 결과, 항공 여행을 보다 충실하게 하기 위해 최신 항공기에 대한 수요가 급증하고 있습니다. 이에 따라 인도의 민간 항공사 여러 회사는 최신예기의 도입에 많은 투자를 하고 있습니다.

예를 들어, 2023년 9월, 에어 인디아는 HSBC와의 금융리스를 통해 회사 최초의 A350-900을 확보했습니다. 에어 인디아는 총 6대의 A350-900을 주문했습니다. 5대는 2024년 3월까지 인도될 예정이었습니다. 또한 인도에서는 새로운 공항의 건설 수가 현저하게 증가하고 있습니다. 연간 항공 여객 수가 증가함에 따라 인도의 기존 공항은 혼잡과 병목 현상에 시달리고 있으며 새로운 공항의 개발이 급증하고 있습니다. 예를 들어, 아요디야의 마리아다 풀쇼타무 슐리 람 국제공항은 2023년 12월에 개항했습니다. 이러한 인프라의 발전은 앞으로 수년간 동 부문의 성장을 뒷받침할 것으로 보입니다.

무기 및 군수 분야가 시장을 독점

인도는 특히 중국과 국경 분쟁의 격화를 배경으로 국방비를 크게 증강하고 있습니다. 이 때문에 인도 국방군은 선진적인 무기와 탄약 획득을 우선하여 그 능력을 강화하고 있습니다. 동시에 많은 기업들이 인도의 방위 부문과 제휴하여 군의 진화하는 요구에 부응하기 위해 연구 투자를 늘리고 있습니다. 예를 들어, 2023년 9월, 인도 육군은 600억 달러라는 고액을 투입해 국내 기업이 독점적으로 개발 및 제조하는 차세대포의 계획을 발표했습니다. 이 새로운 예언 탄총 시스템은 가볍고 적응성이 높으며 최첨단 기술을 자랑한다고 홍보되었습니다.

인도는 또한 선진적인 155mm 포탄약의 제조 기지로서 세계의 역할을 노리고 있습니다. 이 야심을 뒷받침하기 위해 2023년 2월 국방부는 국내 5개 업체에 계약을 주문했습니다. 이러한 계약은 39구경, 45구경, 52구경에 걸친 육군의 기존 155mm포용 155mm 말단 유도탄(TGM) 약 2,000발의 납품을 수반합니다. 국산무기의 생산이 증가하고 국방지출이 견조하게 추이하고 있기 때문에 이 부문은 당분간 큰 성장을 이룰 가능성이 있습니다.

인도의 항공, 방위 및 우주 산업 개요

인도의 항공, 방위 및 우주 시장은 단편화되어 있어 다양한 기업이 시장을 독점하고 있습니다. 주요 시장 기업으로는 Hindustan Aeronautics Limited(HAL), Bharat Electronics Limited(BEL), Indian Space Research Organisation(ISRO), Larsen & Toubro Limited, Adani Group 등이 있습니다.

일부 시장 기업은 장기적으로 국가의 방위 능력을 강화하기 위해 인도 정부와 합작 투자를 형성하고 있습니다. 이러한 협력 관계는 인도의 방위력을 강화할 뿐만 아니라 지역 기업 시장 존재도 강화합니다. 게다가 특히 제트 추진 시스템이나 국산 무기, 민간 항공기, 우주 부품의 생산 등의 분야에서 제휴가 활발해지고, 새로운 기회가 탄생하고 있습니다. 이 추세는 앞으로 몇 년동안 상당한 성장을 가속할 것으로 보입니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인

시장 성장 억제요인

Porter's Five Forces 분석

구매자 및 소비자의 협상력

공급기업의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

공군별

전투기, 비전투기(고정익 및 헬리콥터) 및 UAV

무기 및 군수품

MRO

육군별

장갑차, 헬리콥터 및 UAV

무기 및 군수품

MRO

해군별

함정, 전투기, 비전투기 및 UAV

무기 및 군수품

MRO

우주별

인공위성

로켓 및 로버

민간 항공별

민간 항공기

비즈니스 제트

MRO

제6장 경쟁 구도

벤더의 시장 점유율

기업 프로파일

Hindustan Aeronautics Limited(HAL)

Indian Ordnance Factories

Bharat Electronics Limited(BEL)

Goa Shipyard Limited

Hinduja Group

Kalyani Steels Ltd(KSL)

Tata Sons Private Limited

Larsen & Toubro Limited

Mahindra & Mahindra Limited

Mistral Solutions Pvt. Ltd

Adani Group

Indian Space Research Organisation(ISRO)

제7장 시장 기회 및 향후 동향

AJY

영문 목차

영문목차

The India Aviation, Defense, And Space Market size is estimated at USD 19.81 billion in 2025, and is expected to reach USD 26.32 billion by 2030, at a CAGR of 5.84% during the forecast period (2025-2030).

The growing acquisition of commercial aircraft to meet the needs of air passengers, increasing commercial aviation operations, and the growth in the number of commercial airport constructions are anticipated to drive the market during the forecast period. In addition, the growth in India's defense budget, increasing acquisition of advanced armaments to improve the country's defense capabilities, growth in the number of space programs, and increasing governmental support for indigenous defense manufacturing are expected to boost the market in the coming years.

On the other hand, growth in regulations within the country is expected to hamper the market's growth in the long run. Furthermore, the growing use of advanced technologies such as artificial intelligence for airport construction and design, military training, surveillance, and improving accuracy for space missions, amongst others, is anticipated to lead to growth in various market opportunities.

India Aviation, Defense, and Space Market Trends

Civil Aviation Segment to Showcase Remarkable Growth

In recent years, the Indian aviation sector has experienced remarkable growth in operations, solidifying its position as the world's third-largest. An increasing population with a growing appetite for travel primarily fuels this surge. Consequently, there has been a surge in demand for modern aircraft to enhance the flying experience. In response, several commercial airlines in India are investing substantially in acquiring cutting-edge aircraft.

For example, in September 2023, Air India secured its first A350-900 through a finance lease with HSBC. Air India placed orders for a total of six A350-900s. Five units were scheduled for delivery by March 2024. Furthermore, India has seen a notable rise in the number of new airport constructions. With a rising number of air passengers annually, existing airports in India are grappling with congestion and bottlenecks, prompting a surge in new airport developments. For instance, the Maryada Purushottam Shri Ram International Airport in Ayodhya was inaugurated in December 2023. Such infrastructural strides are poised to bolster the sector's growth in the coming years.

The Weapons and Munitions Segment Dominates the Market

India has significantly boosted its defense spending, driven by escalating border disputes, notably with China. This has prompted the Indian defense forces to prioritize acquiring advanced weaponry and ammunition, bolstering their capabilities. Simultaneously, numerous companies have partnered with India's defense sector, increasing their research investments to meet the military's evolving demands. For instance, in September 2023, the Indian Army announced plans for next-gen guns to be exclusively developed and manufactured by domestic firms with a hefty price tag of USD 60 billion. These new towed gun systems are touted to be lighter and more adaptable, boasting cutting-edge technology.

India is also eyeing a global role as a manufacturing hub for advanced 155 mm artillery ammunition, a caliber favored by more than 75 armies worldwide. Underscoring this ambition, in February 2023, the Ministry of Defense awarded contracts to five domestic manufacturers. These contracts entail delivering around two thousand 155 mm terminally guided munitions (TGMs) for the Army's existing 155 mm guns, spanning 39, 45, and 52 calibers. With the uptick in indigenous weapon production and robust defense spending, this sector is primed for significant growth in the foreseeable future.

India Aviation, Defense, and Space Industry Overview

The Indian aviation, defense, and space market is fragmented, with various players dominating it. Some of the major market players are Hindustan Aeronautics Limited (HAL), Bharat Electronics Limited (BEL), Indian Space Research Organisation (ISRO), Larsen & Toubro Limited, and Adani Group.

Several market players are forming joint ventures with the Indian government to bolster the nation's defense capabilities in the long term. These collaborations not only enhance India's defense but also strengthen the market presence of regional players. In addition, new opportunities emerge as partnerships flourish, especially in sectors such as jet propulsion systems and the production of indigenous weapons, commercial aircraft, and space components. This trend is poised to drive substantial growth in the coming years.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Buyers/Consumers

4.4.2 Bargaining Power of Suppliers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Air Force

5.1.1 Combat and Non-combat Aircraft (Fixed Wing and Helicopter) and UAVs

5.1.2 Weapons and Munitions

5.1.3 MRO

5.2 By Army

5.2.1 Armored Vehicles, Helicopters, and UAVs

5.2.2 Weapons and Munitions

5.2.3 MRO

5.3 By Navy

5.3.1 Naval Vessels, Combat and Non-combat Aircraft, and UAVs