생체인식 카드 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Global Biometric Card - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690916

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

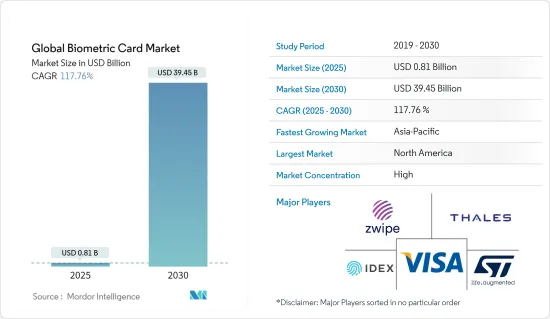

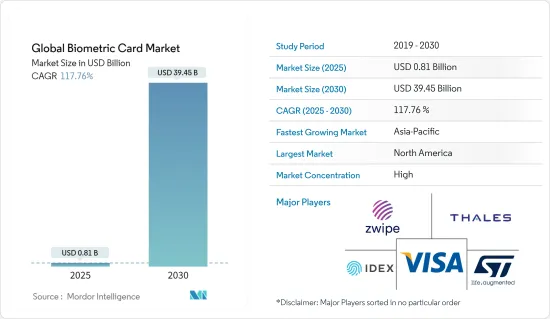

세계의 생체인식 카드 시장 규모는 2025년에 8억 1,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 117.76%로 성장할 전망이며, 2030년에는 394억 5,000만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

결제 보안을 혁신하는 생체인식 인증 : 생체인식 카드 시장은 안전하고 편리한 결제 수단에 대한 수요가 증가함에 따라 크게 성장하고 있습니다. 지문 센서 및 기타 생체인식 기술을 통합한 생체인식 카드는 사용자 경험을 향상시키면서 결제 사기 문제를 해결하여 금융 업계에 혁명을 일으키고 있습니다.

안전한 거래 : 생체인식 카드는 지문 인증과 스마트 카드 기술을 통합하여 안전한 결제를 실현합니다.

생태계 파트너십 : 생태계에서 기업간의 제휴 급증이 시장을 견인하고 있습니다.

주요 인증 : Mastercard, Visa, China UnionPay가 생체인식 카드 솔루션 인증을 받고 있습니다.

금융 포섭이 시장 확대를 견인 : 생체인식 카드 시장의 주요 촉진요인은 특히 신흥 시장에서 금융 포섭 이니셔티브 수요입니다. 정부와 금융기관은 은행 계좌가 없는 사람들을 금융시스템에 통합하기 위해 생체인증 기술을 채택하여 새로운 성장 기회를 창출하고 있습니다.

아프리카 이니셔티브 : Mastercard와 Paycode는 생체인식 스마트 카드를 통한 금융 포용 프로그램에 3,000만 명의 아프리카인을 등록하는 것을 목표로 하고 있습니다.

브라질의 가능성 : 브라질은 데스티와 같은 디지털 뱅크가 충분한 서비스를 받지 못한 사람들에게 초점을 맞추고 있으며, 높은 가능성을 보여줍니다.

세계 평가판 : 폴란드, 이라크, 인도, 멕시코, 레바논, 이집트 등 국가에서 생체인식 카드 평가판이 진행 중입니다.

다요소 인증이 시장 성장을 뒷받침 : 다요소 인증(MFA)의 채택이 확대되고 있다는 것이 생체인식 카드 시장을 뒷받침하고 있습니다. 사이버 보안 위협이 진화하는 동안 기업과 소비자는 보안 강화를 위해 생체 인증을 통합한 MFA 솔루션을 도입하고 있습니다.

MFA에 통합 : 생체인식 인증은 MFA 시스템의 중요한 요소가 되고 있습니다.

헬스케어 채용 : 헬스케어 분야는 환자 데이터를 보호하기 위해 MFA를 채택하고 있습니다.

전자상거래 급증 : 모바일 뱅킹 및 전자상거래의 상승으로 강력한 인증에 대한 수요가 증가하고 있습니다.

경쟁 구도 및 전략적 이니셔티브 : 생체인식 카드 시장은 경쟁이 치열하고 전략적 제휴 및 혁신이 시장 역학을 결정하고 있습니다. 대기업은 시장에서의 지위를 강화하기 위해 기술의 진보 및 인증에 주력하고 있습니다.

탈레스 그룹 리더십 : 탈레스는 20개가 넘는 생체인식 결제 카드 프로젝트에서 최첨단을 실행하고 있습니다.

확대를 위한 파트너십 : Zwipe, Idemia Group, Fingerprint Cards AB 등의 기업은 지역 기업와 제휴하여 세계 리치를 확대하고 있습니다.

혁신 추진 : 주요 금융 플랫폼은 안전하고 혁신적인 기술의 채택을 추진하고 있습니다.

미래 전망 및 시장 가능성 : 생체인식 카드 시장의 미래는 유망하고, 새로운 동향은 지속적인 성장을 보여줍니다. 생체인식 및 IoT나 스마트 시티 구상과의 융합이 기존의 결제에 그치지 않는 새로운 기회를 이끌어내고 있습니다.

멀티모달 생체인식 : 시장은 지문, 얼굴 인식, 손 모양을 결합한 멀티모달 솔루션으로 진화하고 있습니다.

비접촉 결제 : 비접촉식 생체인식 결제 카드는 안전성과 편리성으로 인기를 얻고 있습니다.

암호화폐 통합 : 암호화폐 거래에서 생체인식 카드의 사용은 새로운 추세입니다.

생체인식 카드 시장 동향

BFSI 부문 : 생체인식 카드 상황 석권

부문 성장 및 시장 점유율 : BFSI(은행/금융서비스/보험) 부문은 생체인식 카드 시장을 선도하고 있으며, 2022년 3,676만 달러에서 2029년에는 12억 8,200만 달러로 성장할 것으로 예상됩니다. 이 부문의 2021년 시장 점유율은 66.10%로 시장 확대의 우위성이 두드러지고 있습니다.

부정 행위와의 싸움 : 금융 기관은 증가하는 카드 사기를 완화하기 위해 보안 강화에 주력하고 있습니다.

비접촉식 결제의 유행 : 세계의 비접촉 결제로의 전환은 생체인식 카드 도입을 위한 비옥한 토양을 생산합니다.

MFA 매칭 : 금융 거래에서 MFA 중시 증가는 생체인식 카드와 완벽하게 일치합니다.

미세 동향 및 업계 이니셔티브 : 금융기관과 기술 제공업체의 협업이 생체인식 카드의 혁신을 촉진하고 있습니다. 예를 들어, Mastercard는 요르단 쿠웨이트 은행과 제휴하여 PIN 불필요한 결제를 가능하게 하는 카드에 지문 리더를 탑재한 생체인식 결제 카드를 출시했습니다.

혁신을 추진하는 파트너십 : 이러한 제휴는 보다 안전하고 사용자 친화적인 결제 방법을 추진하는 자세를 돋보이게 합니다.

디지털 위안 평가판 : 중국 건설 은행은 IDEX Biometrics와 제휴하여 디지털 위안화 실증 실험을 수행하고 새로운 디지털 통화 생태계에서 생체인식 카드의 역할을 보여줍니다.

시장 역학 및 미래 전망 : 안전하고 원활한 지불 방법에 대한 소비자 수요 증가로 BFSI 부문의 이점은 앞으로도 계속될 것으로 예상됩니다. 생체인식 기술이 성숙하고 제조 비용이 낮아짐에 따라 은행 서비스 전반에 걸쳐 광범위한 채용이 예상되고, 이 부서의 역할이 더욱 견고해집니다.

원활한 업그레이드 경로 : 생체인식 카드는 기존 인프라를 파괴하지 않고도 안전하고 확장 가능한 솔루션을 금융기관에 제공합니다.

비용 절감 및 성숙 : 제조 비용이 낮아짐에 따라 BFSI 분야 전체에서 생체인식 카드의 보급이 급증할 것으로 예상됩니다.

아시아태평양 : 급성장하는 지역 부문

시장 성장 궤적 : 아시아태평양은 생체인식 카드 시장에서 가장 급성장하며 2022년 1,402만 달러에서 2027년에는 7억 3,796만 달러로 확대될 것으로 예측되며, CAGR 120.92%로 성장할 전망입니다.

인구 역학 동향 : 중간층 증가 및 도시화의 진전은 생체인식 카드 솔루션의 대규모 대응 시장을 형성하고 있습니다.

정부 이니셔티브 : 인도와 중국의 금융 포용 프로그램은 생체인식 카드 도입에 이상적인 환경을 만들어 냅니다.

미세 동향 및 지역 이니셔티브 : 아시아태평양에서는 생체인식 카드 채택을 가속화하기 위한 다수의 노력이 이루어지고 있습니다. 예를 들어, Fingerprint Cards AB는 Transcorp와 제휴하여 인도에서 생체인식 카드를 출시하고, 일본의 MoriX는 Fingerprint Cards와 제휴하여 안전한 결제 방법을 개발하고 있습니다.

인도에 있어서의 비접촉 결제의 추진 인도에서는 비접촉형 결제의 추진에 의해 생체인식 카드의 도입이 가속하고 있습니다.

일본의 안전한 결제 사정 : 일본의 소비자는 안전하고 마찰이 없는 결제 방법을 요구하고 있어 생체인식 카드에 대한 관심을 높이고 있습니다.

시장 역학 및 미래 전망 : 아시아태평양의 생체인식 카드 시장의 성장은 일본과 같은 하이테크 선진국에서 인도와 인도네시아와 같은 신흥 시장에 이르기까지 다양한 시장 역학을 특징으로 합니다.

다양한 기회 : 이 지역의 다양성은 생체인식 카드 기업에게 독특한 도전을 제공하는 동시에 큰 비즈니스 기회를 제공합니다.

폭넓은 분야에서의 채용 : BFSI 뿐만 아니라, 헬스케어나 정부의 ID 프로그램 등의 분야가 추가 성장을 가속할 것으로 예상됩니다.

생체인식 카드 산업 개요

세계의 기술 대기업이 시장을 독점

세계의 생체인식 카드 시장은 선도적인 기술 대기업 및 생체인식 솔루션의 전문 공급자가 주도하고 있습니다. Thales Group, IDEMIA Group, Mastercard 등 주요 기업들이 기술력과 세계적인 전개로 시장을 독점하고 있습니다.

통합 시장 : 이러한 기업들은 기술적 전문성에 더 큰 시장 점유율을 얻고 있습니다.

세계 도달 범위 : 여러 지역에서 사업을 전개함으로써 시장에서의 지위를 강화하고 있습니다.

혁신 및 파트너십이 시장의 주도권을 잡습니다.

혁신 및 전략적 파트너십은 시장에서 리더십을 유지하는 데 필수적입니다. Fingerprint Cards AB 및 IDEX Biometrics ASA와 같은 기업은 첨단 생체인식 센서 및 소프트웨어 솔루션 개발을 선도하고 있습니다. 주요 결제 네트워크와의 제휴는 시장 인증을 얻는 데 필수적입니다.

기술적 리더십 : 이러한 기업들은 차세대 생체인식 솔루션 개발을 위한 연구 개발에 많은 투자를 하고 있습니다.

전략적 제휴 : 금융기관과의 제휴를 통해 시장에 깊은 침투와 인증을 준수할 수 있습니다.

시장의 미래 성공 요인 : 생체인식 카드 시장의 향후 성공에는 몇 가지 요인이 필수적입니다. 생산 비용 절감, GDPR(EU 개인정보보호규정)과 같은 규제 규정 준수 보장, 신흥 시장 진출이 성장에 필수적입니다.

비용 효율성 : 카드 당 제조 비용을 20달러에서 5달러로 낮추는 것이 중요한 목표입니다.

보안 및 컴플라이언스 : 시장 성공을 위해서는 보안 기능 강화 및 규정 준수가 필수적입니다.

신흥 시장 기회 : 신흥 시장의 현지 기관과의 파트너십은 새로운 성장의 길을 제공합니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도-Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

시장에 대한 COVID-19의 영향 평가

업계 생태계 분석

생체인식 카드의 진화

제5장 시장 역학

시장 성장 촉진요인

신흥국에서의 금융포섭에 근거한 이니셔티브 수요 증가

다 요소 인증으로의 전환이 시장 성장에 좋은 재료

금융포섭이 시장 확대 촉진

결제 보안에 혁명을 가져오는 생체인식 인증이 시장 성장 견인

시장의 과제

비카드형 생체인식 기기와의 강한 경쟁

높은 도입 비용

제6장 시장 세분화

용도별

결제

액세스 제어

정부 ID 및 금융 포섭

기타 용도

업계별

BFSI

소매

정부기관

헬스케어

상업 단체

기타 최종 사용자 업계별

지역별

북미

유럽

아시아태평양

세계 기타 지역

제7장 경쟁 구도

기업 프로파일

Zwipe AS

Thales Group

IDEX Biometrics ASA

ST Microelectronics NV

Visa Inc.

Seshaasai Business Forms(P) Ltd

IDEMIA Group

Goldpac Fintech

Mastercard Incorporated

Fingerprint Cards AB

Ethernom Inc.

Samsung's System LSI Business

Shanghai Fudan Microelectronics Group Co. Ltd

제8장 투자 분석

제9장 미래 전망

제10장 시장 기회 분석

AJY

영문 목차

영문목차

The Global Biometric Card Market size is estimated at USD 0.81 billion in 2025, and is expected to reach USD 39.45 billion by 2030, at a CAGR of 117.76% during the forecast period (2025-2030).

Key Highlights

Biometric Authentication Revolutionizing Payment Security: The Biometric Card Market is witnessing significant growth as demand for secure and convenient payment methods rises. Biometric cards, incorporating fingerprint sensors or other biometric technologies, are revolutionizing the financial industry by addressing payment fraud concerns while improving user experience.

Secure transactions: Biometric cards integrate fingerprint recognition with smart card technology to ensure secure payments.

Ecosystem partnerships: A surge in collaborations among players in the ecosystem is driving the market forward.

Major certifications: Mastercard, Visa, and China UnionPay are leading the way in certifying biometric card solutions.

Financial Inclusion Driving Market Expansion: A key driver of the biometric card market is the demand from financial inclusion initiatives, particularly in emerging markets. Governments and financial institutions are adopting biometric technologies to integrate unbanked populations into the financial system, creating new growth opportunities.

African initiatives: Mastercard and Paycode aim to enroll 30 million Africans in a biometric smart card financial inclusion program.

Brazilian potential: Brazil shows high potential, with digital banks like Desty focusing on underserved populations.

Global trials: Biometric card trials are ongoing in countries like Poland, Iraq, India, Mexico, Lebanon, and Egypt.

Multi-Factor Authentication Boosting Market Growth: The growing adoption of multi-factor authentication (MFA) is a major factor fueling the biometric card market. As cybersecurity threats evolve, businesses and consumers are integrating MFA solutions that incorporate biometrics for enhanced security.

Integration in MFA: Biometric authentication is becoming a key element of MFA systems.

Healthcare adoption: The healthcare sector is embracing MFA to protect patient data.

Ecommerce surge: The rise of mobile banking and ecommerce is increasing the demand for strong authentication.

Competitive Landscape and Strategic Initiatives: The biometric card market is highly competitive, with strategic collaborations and innovations defining market dynamics. Leading players are focusing on technological advancements and certifications to strengthen their market positions.

Thales Group leadership: Thales is at the forefront with over 20 biometric payment card projects.

Partnerships for expansion: Companies like Zwipe, Idemia Group, and Fingerprint Cards AB are expanding their global reach by partnering with regional players.

Innovation push: Major financial platforms are driving the adoption of secure, innovative technologies.

Future Outlook and Market Potential: The future of the biometric card market looks promising, with emerging trends indicating sustained growth. The integration of biometrics with IoT and smart city initiatives is unlocking new opportunities beyond traditional payments.

Multimodal biometrics: The market is evolving towards multimodal solutions, combining fingerprint, facial recognition, and hand geometry.

Contactless payments: Contactless biometric payment cards are gaining popularity due to their security and convenience.

Cryptocurrency integration: The use of biometric cards in cryptocurrency transactions is an emerging trend.

Biometric Card Market Trends

BFSI Segment: Dominating the Biometric Card Landscape

Segment Growth and Market Share: The BFSI (Banking, Financial Services, and Insurance) sector is leading the biometric card market, with projected growth from USD 36.76 million in 2022 to USD 1.282 billion by 2029. The sector held a 66.10% market share in 2021, underscoring its dominance in driving market expansion.

Combatting fraud: Financial institutions are focusing on enhanced security to mitigate rising card fraud.

Pandemic-driven contactless payments: The global shift towards contactless payments has created fertile ground for biometric card adoption.

MFA alignment: The increasing emphasis on MFA in financial transactions aligns perfectly with biometric cards.

Micro Trends and Industry Initiatives: Collaborations between financial institutions and technology providers are driving innovations in the biometric card space. For example, Mastercard partnered with Jordan Kuwait Bank to launch a biometric payment card featuring an on-card fingerprint reader for PIN-free payments.

Partnerships driving innovation: These collaborations highlight the push towards more secure and user-friendly payment methods.

Digital renminbi trials: China Construction Bank's partnership with IDEX Biometrics for digital renminbi experiments showcases the role of biometric cards in emerging digital currency ecosystems.

Market Dynamics and Future Outlook: The BFSI sector's dominance is expected to continue, driven by increasing consumer demand for secure, seamless payment methods. As biometric technology matures and production costs decrease, widespread adoption is anticipated across banking services, further solidifying the sector's role.

Seamless upgrade path: Biometric cards provide financial institutions with a secure, scalable solution without disrupting existing infrastructure.

Cost reduction and maturity: As production costs fall, widespread biometric card adoption across the BFSI sector is expected to surge.

Asia-Pacific: The Fastest-Growing Regional Segment

Market Growth Trajectory: The Asia-Pacific region is expected to experience the fastest growth in the biometric card market, expanding from USD 14.02 million in 2022 to USD 737.96 million by 2027, with a CAGR of 120.92%.

Demographic trends: A growing middle class and increasing urbanization create a large addressable market for biometric card solutions.

Government initiatives: Financial inclusion programs in India and China are creating an ideal environment for biometric card adoption.

Micro Trends and Regional Initiatives: Asia-Pacific is witnessing numerous initiatives aimed at accelerating biometric card adoption. For instance, Fingerprint Cards AB has partnered with Transcorp to launch biometric cards in India, while MoriX in Japan is collaborating with Fingerprint Cards to develop secure payment methods.

India's contactless push: India's drive for contactless payments is accelerating biometric card adoption.

Japan's secure payment landscape: Japanese consumers are demanding secure, frictionless payment methods, boosting biometric card interest.

Market Dynamics and Future Prospects: Asia-Pacific's growth in the biometric card market is characterized by diverse market dynamics, ranging from tech-savvy economies like Japan to emerging markets like India and Indonesia.

Diverse opportunities: The region's diversity offers unique challenges but also substantial opportunities for biometric card players.

Broader sectoral adoption: Beyond BFSI, sectors such as healthcare and government ID programs are expected to drive further growth.

Biometric Card Industry Overview

Market Dominated by Global Technology Conglomerates

The Global Biometric Card Market is led by major technology conglomerates and specialized biometric solution providers. Key players, including Thales Group, IDEMIA Group, and Mastercard, dominate the market with their technological prowess and global reach.

Consolidated market: These companies command significant market share due to their technological expertise.

Global reach: Their presence in multiple regions strengthens their market positions.

Innovation and Partnerships Drive Market Leadership:

Innovation and strategic partnerships are critical for maintaining market leadership. Companies like Fingerprint Cards AB and IDEX Biometrics ASA lead in the development of advanced biometric sensors and software solutions. Collaborations with major payment networks are essential for gaining market certification.

Technological leadership: These companies invest heavily in R&D to develop next-generation biometric solutions.

Strategic alliances: Partnerships with financial institutions enable deep market penetration and certification compliance.

Factors for Future Success in the Market: Several factors are crucial for future success in the biometric card market. Reducing production costs, ensuring compliance with regulations like GDPR, and expanding into emerging markets are vital for growth.

Cost efficiency: Lowering production costs from USD 20 to USD 5 per card is a key goal.

Security and compliance: Enhanced security features and regulatory compliance are essential for market success.

Emerging market opportunities: Partnerships with local institutions in emerging markets provide new growth avenues.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of Impact of COVID-19 on the Market

4.4 Industry Ecosystem Analysis

4.5 Evolution of Biometric Cards

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Demand from Financial Inclusion-based Initiatives in Emerging Countries

5.1.2 Move Toward Multi-factor Authentication Bodes Well for Market Growth