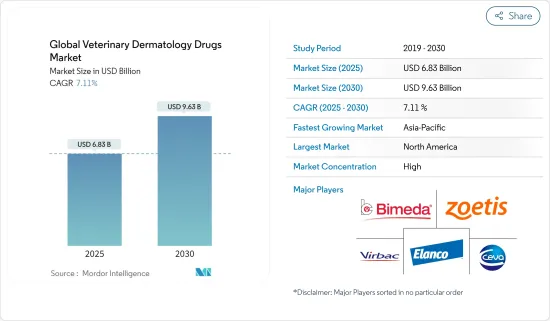

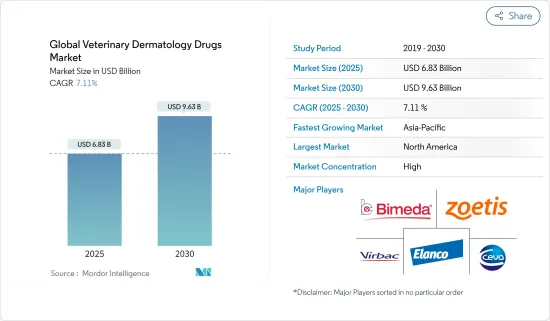

세계의 동물용 피부약 시장 규모는 2025년에 68억 3,000만 달러로 추정되거, 예측 기간인 2025-2030년 CAGR 7.11%로 성장할 전망이며, 2030년에는 96억 3,000만 달러에 달할 것으로 예측됩니다.

반려동물의 피부병 부담 증가, 반려동물 사육 및 동물 케어 증가 등의 요인이, 동물용 피부과 의약품 수요를 환기할 것으로 예상됩니다. 이것은 예측 기간 중, 시장 전체의 성장을 가속할 것으로 예상됩니다.

세계 대부분의 동물은 기생충성 피부 질환, 탈모증, 비듬 관련 피부 질환, 내재성 피부 감염, 경미한 유해한 피부암, 자가면역 피부 질환 및 기타 내부 피부 이상과 같은 주요 피부 질환을 앓고 있습니다. 예를 들어 2022년 7월 Veterinary Sciences Journal에 발표된 연구에 따르면 아토피 피부염(AD)은 가장 흔한 반려동물 알레르기 중 하나입니다. 개에서는 실내 환경이나 반려동물용 가공식품에 노출될 기회가 늘어났기 때문에 유병률이 점점 높아지고 있습니다. 따라서 개 AD의 부담이 증가하고 있으며, 피부약 수요가 높아지고 있습니다. 이는 이 나라의 시장 성장을 촉진할 것으로 예상됩니다.

게다가, 반려동물 사육이 증가하고 있는 것도 예측 기간 동안 시장 성장에 기여할 것으로 예상됩니다. 예를 들어, 2023-2024년 미국 반려동물 제품 협회(APPA)의 전국 반려동물 사육자 조사에 따르면, 미국에서는 약 66%의 가구가 반려동물을 사육하고 있으며, 이는 약 8,690만 가구에 해당합니다. 주요 반려동물은 고양이와 개로 각각 4,530만 명과 6,900만 명입니다.

게다가, 연구 소스의 가용성이 높아지고 있으며, 신제품을 혁신하기 위한 기업의 연구개발 활동이 시장 경쟁을 높이고 있는 요인이 되고 있습니다. 예를 들어 Boehringer Ingelheim은 2022년 9월 미국 식품의약국이 성인의 범발성 농포성 건선(GPP) 재연에 대한 최초 승인 치료제 선택사항인 SPEVIGO를 승인했다고 발표했습니다. SPEVIGO는 인터루킨-36 수용체(IL-36R)의 활성화를 억제하는 새로운 선택적 항체로, GPP의 원인에 관여하는 것으로 나타난 면역계 내 신호전달 경로의 주요 부분입니다. 더 나은 피부과 건강은 반려동물, 반려동물 주인, 가축 동물에게 매우 중요하기 때문에 제품 수가 증가하면 동물용 피부약 시장의 성장에 기여할 것으로 예상됩니다.

그러나 약물의 가용성이 낮거나 인지도가 낮아 분석 기간 동안 시장 성장을 억제할 수 있습니다.

반려동물 부문은 예측 기간 동안 큰 성장을 이룰 가능성이 높습니다. 반려동물의 피부약에 대한 수요는 반려동물의 사육수 증가, 반려동물 질환의 유병률 상승, 반려동물의 건강에 대한 의식 증가 등의 요인에 의해 세계 시장에서 현저한 상승을 관찰하고 있습니다.

2022년 7월 FEDIAF 연례 보고서에 따르면 유럽에서는 고양이와 개가 가장 인기있는 반려동물이며 반려동물을 키우는 가구의 26%가 고양이를 키우고 있으며, 이는 1억 1,000만 가구 고양이에 해당하고, 25%가 개를 기르고 있으며, 이는 9,000만 마리의 개에 해당합니다. 상기 소스에 의하면, 러시아가 가장 많은 고양이를 기르고 있고(2,290만 마리), 그 다음으로 독일(1,670만 마리), 프랑스(1,510만 마리)입니다. 개도 러시아가 1,750만 마리로 가장 많고, 2021년에는 영국이 1,200만 마리, 독일이 1,030만 마리로 뒤를 잇습니다. 반려동물에서는 피부 감염병이나 질병이 가장 전반적인 건강 문제이기 때문에 반려동물의 피부약이 늘어날 가능성이 높습니다. 따라서 이 부문의 성장을 촉진할 것으로 예상됩니다.

게다가 인간의 알레르기와 마찬가지로 아토피 피부염(AD) 등의 개 알레르기도 일반적으로 되고 있습니다. 만성 알레르기는 그렇게 가려움과 재발성 염증성 병변을 특징으로 합니다. 예를 들어, 2022년 12월에 MDPI가 발표한 연구지제에 따르면, 최근 개 주인 수의 대폭적인 증가와 함께 개의 건강에 관한 우려가 높아지고 있습니다. 개는 보통 알레르기, 감염증, 내분비 문제를 포함한 피부질환 때문에 동물병원에 다닙니다. 따라서 반려동물의 피부질환 부담 증가는 치료제를 위한 피부약의 수요를 증가시켜 이 부문 성장을 촉진할 것으로 예상됩니다.

게다가, 시장 진출기업에 의한 반려동물용 신제품의 출시는 시장의 성장에 큰 역할을 하고 있습니다. 예를 들어, 2023년 10월, Pet King Brands Inc.는 수의사가 권장하는 ZYMOX Enzymatic Dermatology 제품 라인에 귀와 피부에 문제를 겪는 고양이와 새끼 고양이를 돕는 3가지 신제품을 추가했습니다. 이러한 신제품의 발매에 의해, 동물용 피부약 대기업의 제품 포트폴리오가 충실해, 예측 기간 중 시장의 견인역이 될 것으로 생각됩니다.

북미는 동물의 소양증, 누출, 탈모증, 종괴, 발진, 비늘, 지루증, 농포, 배농관 등의 유병률이 높기 때문에 예측 기간 동안 동물용 피부약 시장에서 높은 성장률을 보일 것으로 예측됩니다.

2022년 9월 캐나다 동물 위생 실험실(CAHI)의 데이터에 따르면, 2022년에는 캐나다 가구의 절반 이상(60%)이 적어도 한 마리의 개 또는 고양이를 기르고 있습니다. 또한 같은 해 개 인구는 790만 마리로, 고양이 인구는 850만 마리로 증가했습니다.

북미에서는 미국이 동물용 종양학 시장에서 큰 점유율을 차지할 것으로 예상됩니다. 이는 이 지역에서 가장 많은 동물을 사육하고 있는 데다 동물 의료에 대한 지출이 많아 동물 암 환자의 부담이 크기 때문입니다. 2023-2024년 미국 반려동물용품협회(APPA) 전국 반려동물 소유자 조사에 따르면 미국에서는 약 66%의 가구가 반려동물을 키우고 있으며, 이는 약 8,690만 가구에 해당합니다. 주요 반려동물은 고양이와 개로 각각 4,530만 명과 6,900만 명입니다. 따라서 반려동물 사육 수 증가와 수의사 피부병 관리를 포함한 동물의 의료 지출 증가가 이 지역 시장을 견인할 것으로 예상됩니다.

주요 기업은 신제품의 승인과 발매와 함께 전략적 계획과 시장 개척을 적극적으로 실시하여 시장에 공헌하고 있습니다. 예를 들어, 2022년 11월, Vetoquinol Canada는 전국 수의사들이 반려동물의 피부과 부문에서 오늘날의 많은 과제에 도전하고 해결하기 위한 새로운 도구를 사용할 수 있게 되었다고 발표했습니다. 시장 관계자에 의한 최근의 동향이나 신제품의 발매가 증가하고 있는 것으로부터, 조사 대상 시장의 북미는 성장이 가속하고 있어 동물용 피부약 시장의 예측 기간 중에 현저한 성장률을 나타내는 것이 될 것으로 예상됩니다.

동물용 피부약 시장의 경쟁은 적당하며 주요 기업은 소수입니다. 현재 시나리오에서는 시장 진출기업 간의 합병과 인수의 수가 증가하고 있으며, 이는 동물용 피부과 의약품 시장에 박차를 가하고 있습니다. 시장의 주요 기업은 세계 수요 증가에 전략적으로 대응하고 시장에서 확고한 지위를 얻기 위해 제품 개발 및 전략적 제휴를 추진하고 있습니다. 조사 대상 시장의 주요 기업으로는 Elanco, Bimeda, Inc., Merck & Co., Inc., Virbac, Ceva, Mars Incorporated(미국 버지니아 주), Zoetis, Inc., Nestle SA 등이 있습니다.

The Global Veterinary Dermatology Drugs Market size is estimated at USD 6.83 billion in 2025, and is expected to reach USD 9.63 billion by 2030, at a CAGR of 7.11% during the forecast period (2025-2030).

Factors such as an increasing burden of dermatological diseases in pet animals and increasing pet adoption and animal care are expected to garner the demand for the availability of dermatology drugs available for veterinary use. They are anticipated to drive the overall market growth during the forecast period.

Most animals globally are affected by major skin diseases like parasitic skin diseases, alopecia, dander-related skin disorders, intrinsic skin infections, mild to harmful skin cancer, autoimmune skin diseases, and other internal skin abnormalities. For instance, according to a study published in the Veterinary Sciences Journal in July 2022, atopic dermatitis (AD) is one of the most common pet allergies. In dogs, the prevalence has become increasingly common due to rising exposure to indoor environments and processed foods for pets. Hence, the burden of AD among canines is rising and is creating demand for the availability of dermatology drugs. This is anticipated to fuel the growth of the market in the country.

Moreover, increasing pet adoption is expected to contribute to the growth of the market over the forecast period. For instance, According to the 2023-2024 American Pet Product Association (APPA) National Pet Owners Survey, about 66% of households in the United States owned a pet, which translates to about 86.9 million homes. Cats and dogs were the major pets, with a total population of 45.3 million and 69 million, respectively.

Furthermore, the growing availability of research sources and company research and development activities to innovate new products are the factors fueling competitiveness in the market. For instance, in September 2022, Boehringer Ingelheim announced today the U.S. Food and Drug Administration has approved SPEVIGO, the first approved treatment option for generalized pustular psoriasis (GPP) flares in adults. SPEVIGO is a novel, selective antibody that blocks the activation of the interleukin-36 receptor (IL-36R), a key part of a signaling pathway within the immune system shown to be involved in the cause of GPP. As better dermatological health is crucial for pets, pet owners, and livestock animals, the increasing number of products is expected to contribute to the growth of the veterinary dermatology drugs market.

However, the low availability and lack of awareness of the drugs might restrain the market growth over the analysis period.

The companion animal segment is likely to witness significant growth during the forecast period. The demand for companion animal dermatological drugs has been observing a significant rise in the global market, owing to factors such as increasing pet adoption, rising prevalence of companion animal diseases, and rising awareness about companion animal health.

According to the annual report of the FEDIAF in July 2022, cats and dogs are the most popular companion animals in Europe, with 26% of all pet-owning households owning a cat, amounting to 110 million household cats, and 25% owning dogs, amounting to 90 million dogs. As per the above source, Russia has the most cats (22.9 million), followed by Germany (16.7 million) and France (15.1 million). Russia also has the most dogs, with 17.5 million, followed by the United Kingdom with 12.0 million and Germany with 10.3 million in 2021. This is likely to lead to more dermatological care for pet animals since skin infections and diseases are the most common health problems in companion animals. Hence it is anticipated to fuel the segment's growth.

Furthermore, similar to human allergies, canine allergies, such as atopic dermatitis (AD), are becoming more common. Chronic allergies are characterized by pruritus and recurring inflammatory lesions. For instance, as per a research article published by MDPI in December 2022, concerns regarding canine health have grown along with the large growth in the number of dog owners in recent years. Dogs typically attend veterinary clinics for skin illnesses, including allergies, infections, and endocrine issues. Hence, the rising burden of skin diseases in pets likely increases the demand for dermatology drugs for treatment and is expected to drive the growth of the segment.

Moreover, new product launches by market players for companion animals play a major role in the growth of the market. For example, in October 2023, Pet King Brands, Inc. added three new products to the line of veterinarian-recommended ZYMOX Enzymatic Dermatology products to help cats and kittens with problems with their ears and skin. These new product launches increase the product portfolios of major players in veterinary dermatology drugs and will drive the market over the forecast period.

North America is anticipated to witness a high growth rate in the veterinary dermatology drugs market during the forecast period, owing to the high prevalence of pruritus, sores, alopecia, masses, eruptions, scales, seborrhea, pustules, and draining tracts in animals.

The growth of the veterinary dermatology drugs market in developed countries such as the United States and Canada is driven by increased pet adoption, awareness about animal health, and animal health expenses.According to data from the Canadian Animal Health Institute (CAHI) in September 2022, more than half of Canadian households (60%) own at least one dog or cat in 2022. Additionally, the dog population increased to 7.9 million, and the cat population increased to 8.5 million in the same year.

In the North American region, the United States is expected to hold a significant share of the veterinary oncology market due to having one of the highest numbers of animals in the region, coupled with high animal health expenditure and a high burden of animal cancer cases. According to the 2023-2024 American Pet Product Association (APPA) National Pet Owners Survey, about 66% of households in the United States owned a pet, which translates to about 86.9 million homes. Cats and dogs were the major pets, with a total population of 45.3 million and 69 million, respectively. Hence, increasing pet adoption along with rising expenditure on the healthcare of animals, which also includes veterinary dermatological disease management, is expected to drive the market in the region.

The major players are actively making strategic plans and new developments, along with new product approvals and launches, to contribute to the market. For instance, in November 2022, Vetoquinol Canada announced that veterinarians across the country now have a new tool available to try and address many of today's challenges in the field of pet dermatology. Owing to the increasing number of recent developments and new product launches by market players, the North American region for the studied market is growing faster and will witness a prominent growth rate during the forecast period for the veterinary dermatology drugs market.

The veterinary dermatology drugs market is moderately competitive, with few key players. In the current scenario, the number of mergers and acquisitions among market players is increasing, which is fueling the veterinary dermatology drugs market. The major players in the market are engaged in product development and strategic alliances to strategically cater to the growing global demand for the market and to gain a robust place in it. Major companies in the studied market include Elanco, Bimeda, Inc., Merck & Co., Inc., Virbac, Ceva, Mars Incorporated (Virginia, USA), Zoetis, Inc., and Nestle S.A., among others.