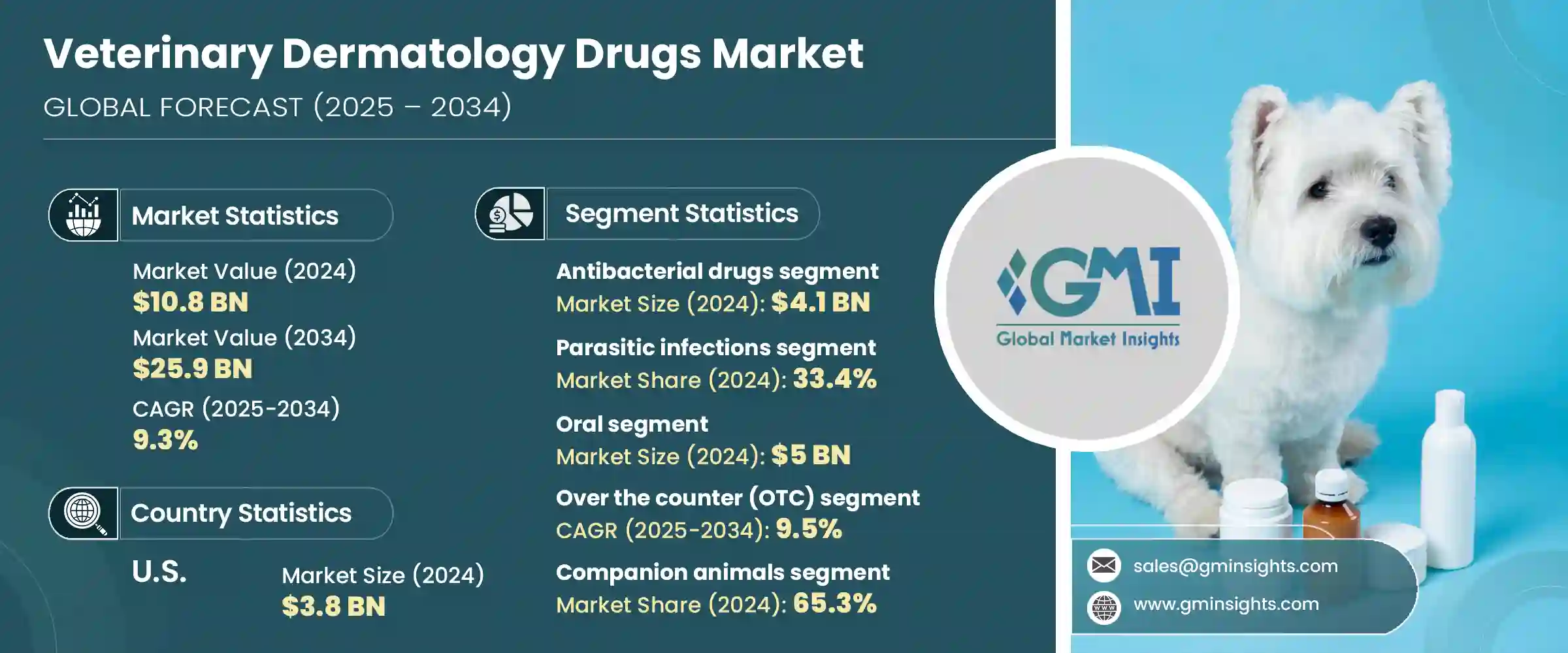

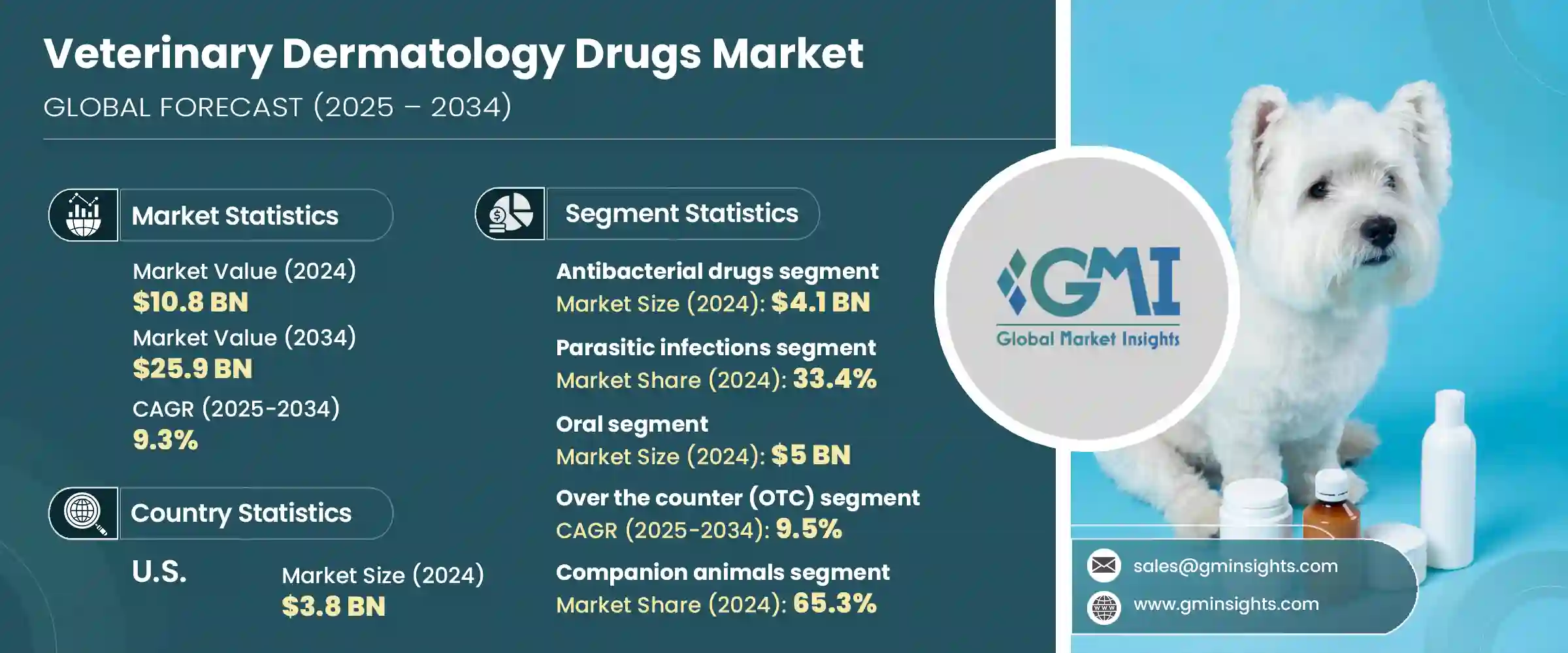

세계의 동물용 피부과 치료제 시장은 2024년에는 108억 달러로 평가되었고, CAGR 9.3%로 성장하여 2034년에는 259억 달러에 이를 것으로 추정되고 있습니다.

반려동물의 건강과 웰빙에 대한 인식이 높아지면서 반려동물의 피부질환 발생률이 급증하고 있는 것이 이러한 성장을 견인하고 있습니다. 전 세계적으로 반려동물 사육률이 지속적으로 증가함에 따라 피부질환 치료용 동물용 의약품에 대한 수요가 급증하고 있습니다. 특히 반려동물을 많이 키우는 도시 지역에서는 동물 의료비 지출 증가와 의료화율 증가로 인해 이러한 수요가 더욱 증가하고 있습니다. 동물 헬스케어 인프라에 대한 투자는 특히 아시아태평양과 라틴아메리카 등 신흥 경제권에서 가속화되고 있어 시장 확대에 유리한 여건을 조성하고 있습니다.

시장 발전의 또 다른 요인은 치료 효과를 높이면서 부작용을 최소화하는 첨단 피부과 치료제의 개발입니다. 제약회사들은 특히 외용제나 경구제 등 투여의 용이성과 효능을 향상시키는 새로운 제형에 집중하고 있습니다. 피부병이 동물의 건강에 미치는 영향에 대한 인식이 높아짐에 따라 시장에서는 피부과 전문 약품에 대한 수용이 확대되고 있습니다. 또한, 가축과 반려동물의 피부 감염이 증가함에 따라 조기 진단과 조기 치료의 필요성이 높아지면서 동물병원 전체에서 피부과 치료제의 사용이 확산되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 108억 달러 |

| 예측 금액 | 259억 달러 |

| CAGR | 9.3% |

동물용 피부과 치료제는 감염과 염증에서 자가면역성 피부질환에 이르기까지 동물의 피부질환을 관리하고 치료하는 데 사용되는 다양한 치료제를 포함합니다. 이러한 약제는 일반적으로 항균제, 항진균제, 항기생충제, 항염증제 등 몇 가지 약제군으로 분류됩니다. 이러한 약물은 증상과 치료에 대한 동물의 반응에 따라 경구, 외용, 주사 등 다양한 경로로 투여됩니다.

약품 유형별로는 항균제가 가장 큰 시장 점유율을 차지하며 2024년 41억 달러 규모에 달했습니다. 항균 동물용 의약품에 대한 수요는 특히 반려동물에서 세균성 피부 감염의 빈도가 증가하고 있는 것이 주요 요인으로 작용하고 있습니다. 이러한 감염이 보편화됨에 따라 수의사들은 효과적인 결과를 얻기 위해 보다 진보된 항균제 및 병용요법으로 눈을 돌리고 있습니다. 약제 내성 균주의 출현도 더 강력하고 표적화된 항균제의 필요성을 가속화시키고 있습니다. 또한, 이러한 질병에 대한 인식이 높아지고 진단 능력이 향상되어 조기 발견이 가능해짐에 따라 이 부문의 안정적인 우위를 점할 수 있게 되었습니다.

적응증별로는 기생충 감염이 가장 큰 시장 점유율을 차지하며 2024년 전체 시장의 33.4%를 차지했습니다. 기생충에 의한 피부 질환은 동물의 피부과 질환 중 가장 흔한 질환 중 하나입니다. 환경 및 기후 조건의 변화는 특히 열대 기후에서 기생충 질환의 확산에 기여하고 있습니다. 이에 대응하기 위해 제약회사들은 외용제 및 경구용 장기 지속형 항기생충제를 출시하고 있습니다. 이러한 새로운 제제는 지속적인 예방 효과를 제공하면서 치료 루틴을 간소화하는 데 초점을 맞추었습니다. 항기생충제 개발의 지속적인 연구와 기술 혁신은 좋은 규제 조건과 함께 이 분야의 성장을 뒷받침하고 있습니다. 유통망 확대로 인한 접근성 향상도 이 부문의 실적 호조에 기여하고 있습니다.

다양한 투여 경로 중 경구용 의약품은 2024년 50억 달러 규모를 차지했으며, 2034년까지 9%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 경구 투여는 약물이 혈류를 순환하고 피부 문제의 근본 원인을 해결할 수 있는 전신적 접근 방식으로 인해 널리 선호되고 있습니다. 또한, 동물은 외용제보다 경구용 약물을 더 잘 받아들이는 경향이 있어 순응도가 높습니다. 이러한 높은 순응도는 안정적인 치료 결과로 이어져 이 부문 수요를 견인하고 있습니다.

지역별로는 북미가 2024년 38.6%의 점유율로 세계 동물용 피부과 치료제 시장을 주도했습니다. 미국 시장 규모는 2023년 35억 달러에서 2024년 38억 달러로 증가했습니다. 이 지역의 성장은 탄탄한 R&D 역량과 개선된 제형의 꾸준한 도입에 기인합니다. 반려동물의 수가 많고 문화적으로 반려동물을 돌보는 것을 중요하게 여기는 문화가 이 지역의 압도적인 시장 지위의 중심이 되고 있습니다. 반려동물 보호자들이 동물을 위한 프리미엄 건강관리 솔루션에 지속적으로 투자하면서 피부과 치료제에 대한 수요도 함께 증가하고 있습니다.

시장 내 경쟁은 여전히 치열하며, 많은 회사들이 집중적인 연구 개발, 제형 혁신, 지리적 확장, 진화하는 규제 기준 준수를 통해 시장 점유율을 확보하기 위해 노력하고 있습니다. 각 기업들은 동물의 특수한 피부과학적 요구를 충족시키는 특화된 제품 개발에 점점 더 집중하고 있으며, 급성장하는 이 분야에서 전략적 입지를 구축하기 위해 노력하고 있습니다.

The Global Veterinary Dermatology Drugs Market was valued at USD 10.8 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 25.9 billion by 2034. This growth is being driven by a sharp increase in the incidence of skin disorders among animals, coupled with rising awareness around pet health and wellness. As pet ownership continues to rise worldwide, demand for veterinary drugs designed to treat dermatological issues has surged. This demand is further amplified by an uptick in animal healthcare spending and an increasing medicalization rate, particularly in urban areas where companion animals are more prevalent. Investment in animal healthcare infrastructure is gaining momentum across emerging economies, especially in regions such as Asia-Pacific and Latin America, creating favorable conditions for market expansion.

Another factor contributing to the market's progress is the development of advanced dermatological drugs aimed at minimizing side effects while enhancing therapeutic outcomes. Pharmaceutical companies are focusing on new formulations, particularly topical and oral options, that improve ease of administration and efficacy. As awareness continues to grow about the impact of skin diseases on animal health, the market is witnessing greater acceptance of dermatology-specific medications. Additionally, the rise in skin infections among livestock and companion animals is pushing the need for early diagnosis and treatment, encouraging the widespread use of dermatology drugs across veterinary practices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.8 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 9.3% |

Veterinary dermatology drugs encompass a broad spectrum of treatments used to manage and cure skin disorders in animals, ranging from infections and inflammations to autoimmune skin conditions. These medications are typically categorized into several drug classes, including antibacterial, antifungal, antiparasitic, and anti-inflammatory drugs. These drugs are administered through multiple routes, such as oral, topical, and injectable, depending on the condition and the animal's response to treatment.

In terms of drug class, antibacterial medications held the largest market share, reaching a value of USD 4.1 billion in 2024. The demand for antibacterial veterinary drugs is largely fueled by the increasing frequency of bacterial skin infections, particularly among companion animals. As these infections become more common, veterinarians are turning to more advanced antibacterial formulations and combination therapies to deliver effective results. The emergence of drug-resistant strains has also accelerated the need for stronger and more targeted antibacterial products. Furthermore, the rising awareness of these conditions and improvements in diagnostic capabilities have enabled early detection, contributing to the consistent dominance of this segment.

By indication, parasitic infections accounted for the largest market share, capturing 33.4% of the total in 2024. Skin conditions caused by parasites are among the most common dermatological issues in animals. Changes in environmental and climatic conditions are playing a role in the increased spread of parasitic diseases, particularly in tropical climates. In response, pharmaceutical companies are introducing long-acting antiparasitic drugs in both topical and oral forms. These new formulations focus on simplifying treatment routines while delivering lasting protection. Ongoing research and innovation in antiparasitic drug development, combined with favorable regulatory conditions, are supporting segment growth. Enhanced access through expanded distribution networks has also contributed to the segment's strong performance.

Among the various routes of administration, oral drugs accounted for USD 5 billion in 2024 and are forecast to grow at a CAGR of 9% through 2034. Oral administration is widely preferred due to its systemic approach, which allows the drug to circulate through the bloodstream and tackle the root cause of skin issues. It also ensures better compliance, as animals tend to accept oral medications more readily than external applications. This high compliance rate contributes to consistent treatment results, which in turn drives demand in this segment.

Regionally, North America led the global veterinary dermatology drugs market, holding a 38.6% share in 2024. The market in the United States alone was valued at USD 3.8 billion that year, up from USD 3.5 billion in 2023. Growth in this region can be attributed to the presence of robust R&D capabilities and the steady introduction of improved drug formulations. The high volume of companion animals and the cultural emphasis on pet care are central to the region's dominant market position. As pet owners continue to invest in premium healthcare solutions for their animals, the demand for dermatology drugs has followed suit.

Competition within the market remains strong, with numerous players striving to gain market share through targeted R&D, innovation in drug formulations, geographic expansion, and compliance with evolving regulatory standards. Companies are increasingly focusing on creating specialized products that meet the unique dermatological needs of animals, positioning themselves strategically within this rapidly growing sector.