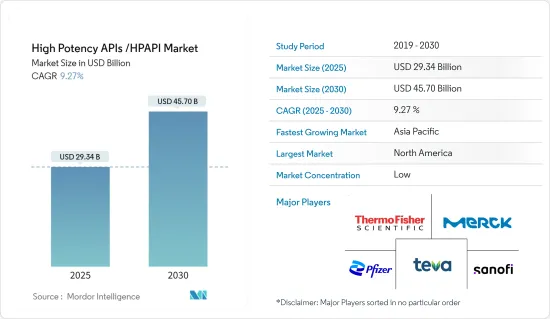

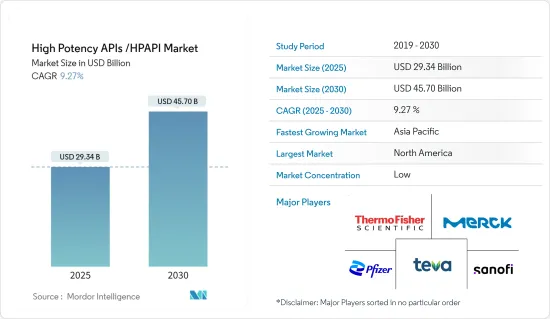

고활성 API(HPAPI) 시장 규모는 2025년에 293억 4,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 9.27%로 성장할 전망이며, 2030년에는 457억 달러에 이를 것으로 예측됩니다.

COVID-19 팬데믹 동안 고활성 API(HPAPI) 시장은 악영향을 받았습니다. COVID-19의 유행은 주로 API 시장 공급망에 영향을 주었습니다. 중국과 인도는 API 생산 거점이고, 코로나19가 이 지역에서 증가하면서 시장은 심각한 타격을 입었습니다. 2022년 6월 European Pharmaceutical Review에 게재된 기사에 따르면, 고활성 API를 포함한 API의 60%는 인도 또는 중국에서 제조되었습니다.

인도만으로 세계 제네릭 의약품 제조 시장의 18%를 차지하며, 그 대부분이 타국에 수출되고 있습니다. 중국은 인도의 제네릭 의약품 산업을 위해 고활성 API를 포함한 API의 70%를 제조하고 있습니다. 중국에서는 엄격한 봉쇄 규제가 깔려 있기 때문에 44개사가 API 제조 공장을 폐쇄했습니다. 그 결과 중요한 API 및 의약품에 대한 접근이 현저히 제한되었습니다.

미국에서는 중요한 치료 영역의 중요한 의약품 API의 80%가 국내에서 제조되지 않을 것으로 예상되며, 이는 세계 보건에 중대한 영향을 미칩니다. 전체적으로 시장은 단기적으로는 방해받는다고 생각되었습니다. 하지만 코로나19 백신 제조에는 다양한 API가 사용되고 있어 예측 기간 동안 시장은 크게 성장할 것으로 예상됩니다.

시장의 성장을 가속하는 요인으로는 의약품 수요 증가, 정밀의료 및 고활성 API에 대한 주목 고조, 고활성 API 제조의 기술 진보 등을 들 수 있습니다.

API는 암, 심혈관질환, 뇌졸중, 심장마비, 당뇨병 등과 같은 만성기초질환의 치료에 사용되는 의약품의 필수성분입니다. 이러한 만성질환 유병률 상승은 HPAPI에 대한 수요를 증가시켜 시장 성장을 증대시킬 가능성이 높습니다. 예를 들어 미국암협회가 2023년 1월 발표한 Cancer Facts and Figures 2023에 따르면 2023년에 새로 진단된 암 환자는 약 190만 명으로 그 중 전립선암은 28만 8,300명, 그 다음으로 폐암 23만 8,340명, 여성 유방암 30만 5,590명으로 평가되었습니다. 이와 같이 국내에서 암의 부담 증가는 효과적인 의약품을 제조하기 위해 HPAPI를 필요로 하는 선진적 치료에 대한 수요를 증가시킬 것으로 예상되며, 시장의 성장을 뒷받침할 것으로 보입니다.

시장 전체에서 HPAPI 제조 시설이 설립되는 것은 시장을 크게 견인할 것으로 예상됩니다. 예를 들어, Novasep는 2021년 5월 르망(프랑스) 거점에서 고활성 의약품 성분(HPAPI) 제조 능력을 확대하고 추가 투자를 통해 암 치료를 위한 혁신적인 표적 분자를 생산합니다. 이어 2022년 3월 인도 보건, 가족복지 및 화학비료부 장관은 중국에서 수입하던 35개 품목의 의약품 원료 제조를 시작했다고 밝혔습니다. 이러한 이니셔티브는 각국의 API에 대한 언메트 니즈를 충족시키며, 따라서 예측 기간 동안의 시장을 끌어올릴 것으로 기대됩니다.

이와 같이 만성질환 부담 증가나 제조시설 설립 등 위의 모든 요인이 시장 확대의 원동력이 될 것으로 예측됩니다. 그러나 설비 투자가 고액이기 때문에 예측 기간 동안 시장이 억제될 것으로 예상됩니다.

제네릭 고활성 API는 브랜드 API 및 혁신적인 API와 동일한 약리 효과를 나타냅니다. 제네릭 HPAPI 부문은 주로 제네릭 의약품에 대한 수요 증가와 저렴한 가격으로 고품질의 의약품을 제조하기 위한 제네릭 HPAPI에 대한 수요 증가에 의해 견인되고 있습니다. 기업간의 합병 및 인수 증가도, 이 부문 확대에 기여하고 있습니다.

브랜드 의약품의 특허 부족과 비용 저하 등의 요인도 이 부문의 성장을 뒷받침하고 있습니다. 2021년 6월 American Journal of Managed Care가 발표한 보고서에 따르면 2023년에는 약 20개의 종양생물제제의 특허가 실효되기 때문에 암 의료에서 더 많은 바이오시밀러가 생산되어 비용이 절감될 수 있습니다. 이러한 이유로 예측 기간 동안 시장은 높은 성장률을 보일 가능성이 있습니다.

또한 API 생산에 중점을 둔 정부의 이니셔티브도 조사 대상 시장의 성장에 기여하고 있습니다. 2021년 6월 인도 재무장관은 의약품 유효성분, 의약품 중간체, 중요한 출발원료 등 13개 주요 부문의 의약품 생산 연동 장려금(PLI) 계획에 대해 5년간 1조 9,700억 루피(240억 2,400만 달러)의 추가 지출을 발표했습니다. 다이나믹한 의약품 원료 부문에 할당된 고액의 장려금은 예측 기간 중의 시장 성장을 대폭 끌어올릴 것으로 생각됩니다.

게다가 시장 진출기업은 경쟁을 높이기 위해 확장 전략을 추진하고 있습니다. 예를 들어 2021년 Moehs Group은 고활성 API(HPAPI) 개발과 상업 생산을 위한 GMP 준거 Kilo Lab Unit의 편입을 발표했습니다. 게다가 2021년 11월, Hovione는 그 능력과 능력을 높이기 위해 1억 7,000만 달러를 투자하겠다고 발표했습니다. 호비오네의 이 능력과 능력은 고활성 API(HPAPI) 생산도 업그레이드합니다.

이와 같이, 특허 만료 증가나 HPAPI 제조 시설의 기동 등, 상기의 요인은 모두, 예측 기간중의 동 부문의 성장을 뒷받침할 것으로 예상됩니다.

북미는 암이나 신경질환 등의 질병 만연으로 시장에서 큰 점유율을 차지할 것으로 예상됩니다. 이들 질환은 유병률이 증가하고 있기 때문에 이 지역에서는 HPAPI 생산이 증가하고 있습니다. HPAPI는 암 및 기타 중요한 질환과 관련된 많은 치료, 신약 및 기타 조사 연구에 널리 사용됩니다. 따라서 북미 지역에서는 다른 나라에 비해 환자 인구가 증가하고 있기 때문에 HPAPI 수요가 크게 증가합니다.

이 지역의 만성 질환 유병률과 발생률 증가는 예측 기간에 걸쳐 시장을 밀어 올릴 것으로 예상됩니다. 예를 들어 캐나다 정부가 발표하고 2022년 5월에 발표된 통계에 따르면 2022년에는 약 23만 3,900명의 캐나다인이 암 진단을 받았으며 전립선암은 계속해서 가장 많이 진단되는 암으로 평가되고 있습니다. 이와 같이 이 지역의 암 부담 증가는 예측 기간 동안 시장 성장을 끌어올릴 것으로 예상됩니다.

또한 World Alzheimer's Report 2023에 따르면 2023년에는 추정 670만 명의 65세 이상의 미국인이 알츠하이머형 치매를 앓을 것으로 예상되고 있습니다. 이처럼 신경질환 부담이 커지면서 효과적인 치료 및 관리 방법에 대한 수요가 높아져 예측 기간 동안 HPAPI 시장을 끌어올릴 것으로 예상됩니다.

주요 시장 진출 기업에 의한 이 나라의 사업 확대도 시장 성장의 요인 중 하나입니다. 예를 들면, 2021년 8월, 연구 개발 및 제조 수탁 기관 대기업의 Curia(구 AMRI)는, 뉴욕주 렌셀러 시설에서의 상업 생산 능력의 확대를 발표했습니다. 복잡한 의약품 API를 연질적으로 제조하는 능력의 증강은 쿠리아의 고객과의 제휴 능력을 더욱 강화합니다.

이와 같이 위의 요인들로부터 미국의 고활성 API(HPAPI) 시장은 예측기간 동안 높은 성장률을 보일 것으로 예상됩니다.

고활성 API(HPAPI) 시장은 세분화되어 경쟁이 격렬하고, 여러 선도 기업으로 구성되어 있습니다. 시장 점유율 면에서는 Thermo Fisher Scientific Inc., Merck KGaA, Pfizer, Novartis International AG, 및 Teva Pharmaceutical Industries 등 소수의 대기업이 시장을 독점하고 있습니다.

The High Potency APIs /HPAPI Market size is estimated at USD 29.34 billion in 2025, and is expected to reach USD 45.70 billion by 2030, at a CAGR of 9.27% during the forecast period (2025-2030).

During the COVID-19 pandemic, the high-potency API (HPAPI) market was adversely affected. The COVID-19 outbreak primarily affected the supply chain of the API market. China and India are the hubs for the production of API, and the market was severely hampered as COVID-19 increased in the region. According to the article published in the European Pharmaceutical Review in June 2022, 60% of APIs, including high-potency APIs, are manufactured in India or China.

India alone accounts for 18% of the global generic drug manufacturing market, most of which is exported to other countries. China manufactures 70% of the APIs, including high-potency APIs, for India's generics industry. Due to stringent lockdown restrictions in China, 44 firms closed API manufacturing plants during the outbreak. As a result, access to critical APIs and medicines was severely limited.

It is anticipated that 80 percent of APIs for vital medications in critical therapeutic areas in the United States do not have a domestic manufacturing source, which has significant global health consequences. Overall, the market was considered to be hindered in the short term. However, various APIs are used in producing COVID-19 vaccines, and the market is expected to grow significantly over the forecast period.

Factors driving the market's growth include increasing demand for drugs, increasing focus on precision medicine and high-potency APIs, and technological advancements in high-potency API manufacturing.

APIs are essential components of drugs used to treat chronic underlying health disorders like cancer, cardiovascular disease, strokes, heart attacks, diabetes, and others. The rising prevalence of these chronic diseases is likely to increase demand for HPAPI, increasing market growth. For instance, according to Cancer Facts and Figures 2023, published in January 2023 by the American Cancer Society, an estimated 1.9 million new cancer cases will be diagnosed in 2023, among which prostate cancer is estimated to be 288,300, followed by 238,340 cases of lung cancer, and 300,590 cases of female breast cancer. Thus, the growing burden of cancer in the country is expected to increase demand for advanced treatments that need HPAPI to produce effective medicine, which is likely to boost market growth.

Establishing HPAPI manufacturing facilities across the market will drive the market significantly. For instance, in May 2021, Novasep expanded its highly potent active pharmaceutical ingredients (HPAPIs) manufacturing capabilities on its Le Mans (France) site to produce innovative and targeted molecules to treat cancer by investing in additional capacity. Additionally, in March 2022, the Indian Minister of Health and Family Welfare and Chemicals and Fertilisers announced that India had started manufacturing 35 pharmaceutical ingredients that had been imported earlier from China. Such initiatives are expected to meet the unmet need of API in countries and, hence, boost the market over the forecast period.

Thus, all the factors above, such as the increasing burden of chronic diseases and the establishment of manufacturing facilities, are projected to drive market expansion. However, the high capital investment is expected to restrain the market over the forecast period.

Generic high-potency active pharmaceutical ingredients show the same pharmacological effects as branded or innovative API. The generic HPAPI segment is primarily driven by the rising demand for generic pharmaceuticals and the rising need for generic HPAPI to generate high-quality drugs at affordable prices. Rising mergers and acquisitions between businesses have also helped expand the segment.

Factors such as the expiration of patents on branded drugs and lower costs are also driving segment growth. According to the report published by the American Journal of Managed Care in June 2021, patents on around 20 oncology biologics will expire in 2023, which may lead to the production of more biosimilars in cancer care and reduce costs. Due to these reasons, the market may see a high growth rate during the forecast period.

Also, government initiatives focusing on active pharmaceutical ingredient production are contributing to the growth of the studied market. In June 2021, the Indian Finance Minister announced an additional outlay of INR 197,000 crore (USD 24,024 million) for utilization over five years for the pharmaceutical Production Linked Incentive (PLI) Scheme in 13 key sectors such as active pharmaceutical ingredients, drug intermediaries, and critical starting materials. The significant incentives allocated to the dynamic pharmaceutical ingredient segment would significantly boost market growth over the forecast period.

Furthermore, market players are also involved in expansion strategies to gain a competitive edge. For instance, in 2021, MoehsGroup announced the incorporation of the GMP-compliant Kilo Lab Unit for developing and commercially producing high-potency APIs (HPAPIs). Additionally, in November 2021, Hovione announced an investment of USD 170 million to increase its capacity and capabilities. This capacity and capability of Hovione will also upgrade the production of highly potent active pharmaceutical ingredients (HPAPI).

Thus, all the factors above, such as an increase in patent expirations and the launch of HPAPI manufacturing facilities, are anticipated to boost the segment's growth over the forecast period.

North America is expected to hold a significant share of the market owing to the prevalence of disorders such as cancer and neurological disorders. These disorders are increasing in prevalence, thus increasing the production of HPAPIs in the region. HPAPIs are widely used in many therapeutic, drug discovery, or other research studies related to oncology and other significant disorders. Thus, the demand for the same will be significantly higher in the North American region as the patient population is increasing compared to other countries.

The increasing prevalence and incidence of chronic diseases in this region are expected to boost the market over the forecast period. For instance, according to statistics published by the Government of Canada and released in May 2022, about 233,900 Canadians were diagnosed with cancer in 2022, and prostate cancer is expected to remain the most commonly diagnosed cancer. Thus, the growing burden of cancer in the region is expected to boost market growth over the forecast period.

Further, according to the World Alzheimer's Report 2023, an estimated 6.7 million Americans age 65 and older are expected to be living with Alzheimer's dementia in 2023. Thus, the growing burden of neurological diseases is expected to increase demand for effective treatment and management methods, thereby boosting the market for HPAPI over the forecast period.

The country's expansion by key market players is another factor in the market's growth. For instance, in August 2021, Curia, formerly AMRI, a leading contract research, development, and manufacturing organization, announced the expansion of its commercial manufacturing capacity at its Rensselaer, New York, facility. The increased capability to flexibly manufacture complex active pharmaceutical ingredients (APIs) will further strengthen Curia's ability to partner with customers.

Thus, owing to the factors above, the United States high-potency API (HPAPI) market is expected to witness a high growth rate over the forecast period.

The high-potency APIs/HPAPI market is fragmented, competitive, and consists of several major players. In terms of market share, a few major players are currently dominating the market, including Thermo Fisher Scientific Inc., Merck KGaA, Pfizer, Novartis International AG, and Teva Pharmaceutical Industries.