북미의 물류 자동화 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

North America Logistics Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690871

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

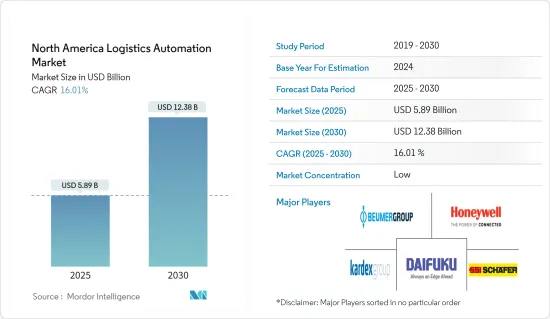

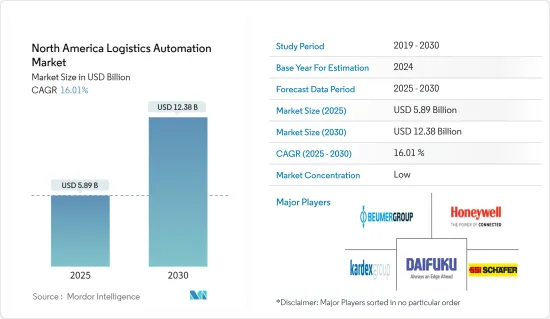

북미의 물류 자동화 시장 규모는 2025년 58억 9,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 16.01%로 성장할 전망이며, 2030년에는 123억 8,000만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

코로나 바이러스의 대유행은 물류 부문에서 자동화 도입의 상황을 복잡하게 만들었습니다. 사회적 거리두기와 비접촉 작업이라는 독특한 과제를 제기함으로써 표준 운영 절차를 변경하고 조직은 노동력을 제한하며 증가하는 수요를 해결해야 했습니다. 2020년 이후에도 계속되는 COVID-19는 미국에서 많은 중요한 근로자에 감염되어 최전선에 있는 주요 기업이 새로운 안전 프로세스의 도입에 착수하는 계기가 되었습니다. 바이러스의 확산은 예를 들어 식품 제조 시설의 운영 중단을 정당화할 정도로 심각했지만, 다른 여러 기업들은 새로운 건강 조치를 추가함으로써 운영을 계속할 수 있었습니다.

DHL의 조사에 따르면, 창고업과 트럭 운송업의 조직은 일반적으로 자동화를 재빨리 도입한 기업으로 알려져 있지 않습니다. 실제로 2016년에는 세계 창고의 80%가 프로세스 자동화를 도입하지 못했습니다.

물류의 자동화는 업무의 효율을 높이기 위한 제어 시스템, 기계, 소프트웨어의 사용을 가리킵니다. 이는 일반적으로 창고나 배송 센터에서 실행되는 프로세스에 적용되며 최소한의 인적 개입을 필요로 합니다. 자동화 물류의 이점으로는 고객 서비스 향상, 확대성 및 속도, 조직 관리, 실수 감소 등을 들 수 있습니다.

테네시 대학에 따르면 로봇 공학은 그 보급과 용도이라는 점에서 공급망 전체에서 가장 진보된 기술 중 하나입니다. 전자상거래의 지속적인 성장 및 창고 관리 서비스 수요는 앞으로도 계속 증가할 것으로 예상됩니다. 이는 자동화에 의한 비용 절감 솔루션을 찾기 위해 이 부문을 가속화하기 위해 더욱 정렬되어 있습니다.

전자상거래의 대두에 의해 분할 케이스 주문이나 1개 단위의 출하도 증가하고 있어, 풀 팔레트 주문보다 효율적이기 때문에 자동화 기술에 크게 의존하고 있습니다. 또한, 자동화된 스토리지 솔루션은 생산성을 향상시키면서, 창고의 설치 면적을 불과 15%로 축소할 수 있습니다.

2021년 4월 현재, SoftBank Robotics와 SB Logistics는 전자상거래 풀필먼트 업무의 혁신을 추진하기 위해 Berkshire Grey와 협업하고 있습니다. 버크셔 그레이의 로봇 픽 앤 팩 시스템은 SB 물류가 다른 제품 카테고리의 여러 SKUS를 로봇 처리함으로써 고객 주문을 처리하는 데 도움이 됩니다. SB Logistics 3PL은 AI를 활용한 최첨단 로봇 자동화 솔루션을 포함한 인텔리전트 엔터프라이즈 로보틱스 솔루션을 사용하며, 일본 시장에서 일반적인 매우 높은 기준을 충족시키기 위해 고객 주문을 자율적으로 피킹, 배치, 포장합니다. 이는 국내 진입 기업이 다른 나라에서 확대되고 있음을 보여주는 것입니다.

북미의 물류 자동화 시장 동향

하드웨어 중에서 정렬 시스템이 큰 성장을 이룰 전망

분류 시스템은 우편 및 소포 서비스, 음식, 전자상거래 산업 등 다양한 지역의 최종 사용자 산업에서 수요가 증가하고 있습니다. 인건비 증가 및 소비자의 구매 행동 변화 등의 요인이 보다 신속하고 정확한 배송 업무에 대한 수요를 높이고 있으며, 그 결과 자동 분류 시스템에 대한 수요가 높아지고 있다

이 지역의 현대적인 제조 시설은 보다 고품질의 제품을 더 빠르고 저렴한 비용으로 생산하는 새로운 기술과 혁신에 의존하고 있습니다. 스마트한 소프트웨어 및 하드웨어의 도입은 현재의 경쟁 시장에서 살아남기 위한 유일한 실현 가능한 방법입니다.

게다가 제조 및 가공 부문에 있어서 효율 향상을 위한 산업 자동화의 채용 확대도, 이 지역에 있어서 선별 시스템의 채용을 뒷받침할 것으로 예상됩니다. 새로운 기술과 혁신은 또한 산업 전체에서 몇 가지 규제의 필요성을 의무화하고 있습니다.

예를 들어, FDA 식품안전근대화법(FSMA)은 식중독이나 이물 혼입에 대한 대응으로부터 그 예방에 중점을 옮겨 식품회사의 업무를 일변시키고 있습니다. 이 때문에 머티리얼 핸들링의 자동화를 촉진하는 식품 안전 기준을 충족시키기 위해 산업은 고도로 규제되고 있습니다. 이 요인은 예측 기간 동안 식음료 산업의 구분 시스템을 촉진할 것으로 예상됩니다.

소매 및 전자상거래 분야의 현저한 성장과 창고의 확대는 조사된 시장 성장의 또 다른 주요 촉진요인입니다. 전자상거래 매출은 2020년 3분기에 전체 소매 매출의 약 14.3%에 기여했으며, 그 중 미국에서는 아마존이 전체 전자상거래 매출의 3분의 1 이상을 차지했습니다.

이 지역의 소매업체의 대부분은 이러한 고가격의 렌탈 환경에서 사업을 확대하는 것보다 창고의 자동화를 계획하고 있습니다. 그러나 이 지역 창고의 80% 가까이는 아직 수작업으로 운영되고 있습니다.

미국이 주요 시장 점유율을 차지할 전망

미국은 자동화 솔루션의 세계 최대이자 최첨단 시장 중 하나입니다. 현저한 항만 교통, 전자상거래 활성화, 주요 제조업 지표 등, 호조한 경제가 제조업의 현저한 성장을 가져오고, 이 나라 물류 부문 전체에서 자동화 솔루션 수요를 견인하고 있습니다.

소매, 자동차, 식품, 의약품 등의 분야가 국내에서의 자동화 물류 솔루션의 최대 수요원입니다. 식음료는 가장 큰 산업이며 미국의 연간 포장 출하량의 35% 이상을 차지하고 있습니다.

이 때문에 팔레타이저, 유닛 로드 AGV, 태그 AGV, 분류 시스템 등, 음식 제조 시설에 널리 도입되고 있는 기기에 대한 큰 수요가 발생하고 있습니다. 또한, 엄격한 식품 안전 규제나, 생산 공정에 있어서의 인적 개입의 적음을 선호하는 경향은 예측 기간 중에 음식 식품 산업 수요를 증가시킬 것으로 예상됩니다.

이 지역에서는 수많은 파트너십이 확인되고 있으며, 보다 높은 품질의 제품을 보다 빠른 속도와 저렴한 비용으로 제조하기 위한 최신 기술이나 혁신에 의존하고 있습니다.

예를 들어 최근 미국의 대형 소매업체 Kroger는 영국의 온라인 슈퍼마켓 Ocado와 제휴를 시작하여 창고 업무, 물류, 자동화, 배송 루트 계획 등에 이 회사의 기술을 활용하게 되었습니다. 이 제휴에 의해, 미국에서는 자동화 솔루션에 의한 소매 부문의 변혁이 진행되게 됩니다.

또, 창고의 공실률이 낮고, 임대료가 급등하고 있기 때문에 기업은 창고용으로 대출하는 소규모의 장소를 찾게 되어 있습니다. 이러한 좁은 공간의 생산성을 최적화하기 위해 자동화 솔루션 도입이 진행될 것으로 예상됩니다.

또한 많은 창고 및 배송 단위를 보유한 대기업은 인건비를 절감하고 수익성을 높이기 위해 인수 전략을 활용하고 있습니다. 예를 들어 거대 소매기업 아마존은 2012년 7억 7,500만 달러를 들여 키바시스템즈라는 젊은 로봇기업을 인수해 신종 이동로봇 소유자를 얻었습니다. 이 투자로 새로운 버전의 창고 로봇을 구축하기 위한 기술적 기반이 마련되었고, 로봇의 미래 가능성의 무대가 마련되었습니다.

북미의 물류 자동화 산업 개요

승인된 자본 예산과 예상되는 리드타임의 범위 내에서 필요한 장비를 제조 및 통합할 수 있는 벤더가 시장을 계속 독점하고 있습니다. 물류 자동화 시장은, 복수의 세계의 참가 기업으로 구성되어, 상당히 경합이 치열한 시장 공간에서 주목을 끌고자 경쟁하고 있습니다.

기술적 혼란은 지속 가능한 경쟁 우위의 중요한 요인이 되고 있습니다. 또한, 제공하는 서비스의 차별화를 도모하기 위해, 각 참가 기업은 서비스 기능으로 이행하고 있습니다. 예를 들어 로커스는 자사 기술의 훈련 측면을 고려해 이 회사의 로커스엠파워솔루션은 훈련을 지원하고 몇 달이 아닌 며칠 만에 근로자를 입사시킨다고 합니다.

이 시장에서의 저명한 진출기업으로는 Honeywell, Swisslog, Daifuku, Scheefer 등을 들 수 있습니다. 이러한 참가 기업의 존재와 끊임없는 혁신적인 활동이 시장 시나리오를 격화시키고 있습니다. 이 시장은 신규 참가 기업에 있어서 적당한 참가 장벽이 되고 있기 때문에, VC의 지원을 받은 복수의 신규 참가 기업이 이 시장에서 견인력을 발휘하고 있습니다. 이로 인해 시장 경쟁은 더욱 격화될 가능성이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업 밸류체인 분석

산업의 매력-Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

경쟁 기업간 경쟁 관계

대체품의 위협

COVID-19의 산업 생태계에 미치는 영향

시장 성장 촉진요인

전자상거래의 활성화

시장의 과제

높은 설비 투자 및 기술의 초기성

제5장 시장 세분화

솔루션 유형별

하드웨어

이동 로봇(무인 반송차(AGV), 자율 이동 로봇(AMR))

자동 창고(AS/RS)(AS/RS)

컨베이어(벨트, 롤러, 팔레트, 오버헤드)

팔레타이저 및 디파레타이저(기존-하이 레벨+로우 레벨, 로봇식)

분류 시스템

소프트웨어-창고 관리 시스템(WMS), WES, WCS

기타 솔루션

운송 관리 솔루션

기타(피스 피킹 로봇, 협동 로봇, 창고 드론, 서포트 인프라)

업종별

일반 상품

의류

음식

식료품

우편 및 소포

제조업(내구 및 비내구)

기타

국가별

미국

캐나다

제6장 경쟁 구도

기업 프로파일

SSI SCHAEFER AG

Daifuku Co. Limited

Kardex Group

Honeywell Intelligrated

Beumer Group GMBH & Co. KG

Jungheinrich AG

Murata Machinery Limited

TGW Logistics Group GmbH

Witron Logistik

Mecalux SA

Viastore Systems GmbH

Swisslog Holdings AG(KUKA AG)

Kion Group AG(Dematic 포함)

Vanderlande Industries BV

벤더 랭킹 분석

Mobile Robots

AS/RS

Collaborative Robots

Palletizers/De-palletizers

Conveyors/Sortation Systems

제7장 투자 분석

제8장 시장의 미래

AJY

영문 목차

영문목차

The North America Logistics Automation Market size is estimated at USD 5.89 billion in 2025, and is expected to reach USD 12.38 billion by 2030, at a CAGR of 16.01% during the forecast period (2025-2030).

Key Highlights

The Coronavirus pandemic complicated the situation of automation adoption in logistics sector. By bringing in unique challenges of social distancing and contactless operation it has changed the standard operating procedure and organizations were forced to limit workforce, and deal with the increasing demand. COVID-19 over 2020 and continuing has infected a number of essential workers in the United States, leading companies on the front lines to implement new safety processes. While the spread of the virus has been grave enough to warrant shutdowns for instance, food production facilities, multiple other businesses have been able to continue operations with the addition of new health measures.

Organizations within the warehousing and trucking industries, when considered, are generally not known as early adopters to automation; in fact, 80% of warehouses globally didn't have any process automation in 2016 as per DHL study.

Automation in logistics refers to the use of control systems, machinery, and software to enhance the efficiency of operations. It usually applies to the processes performed in a warehouse or distribution center, which requires minimal human intervention. Some of the benefits of automation logistics are improved customer service, scalability and speed, organizational control, and reduced mistakes.

As per the University of Tennessee, robotics has been one of the most advanced technologies across a supply chain in terms of its proliferation and application. The continued growth in e-commerce and the demand for warehousing services is expected to continue to increase. This is further aligned for acceleration in the segment in order to find cost-reduction solutions through automation.

The rise of e-commerce has brought a rise in split case orders and even single-unit shipments, which rely much more heavily on automation technologies to be efficient than full-pallet orders. Additionally, an automated storage solution serves an ability to shrink a warehouse's footprint to just 15 percent while increasing productivity.

As of April 2021, SoftBank Robotics and SB Logistics collaborated with Berkshire Grey to drive innovation in E-Commerce fulfillment operations. Berkshire Grey's robotic pick and pack systems would benefit SB Logistics to process customer orders by robotically handling multiple SKUS in different product categories. SB Logistics' 3PL would use Intelligent Enterprise Robotics solutions, including leading AI-enabled robotic automation solutions to autonomously pick, place, and pack customer orders to best meet the extremely high standards prevalent in the Japanese market. This marks domestic player's expanding in other countries.

North America Logistics Automation Market Trends

Among Hardware, Sortation System is Expected to Witness Significant Growth

Sortation systems are witnessing increased demands from various regional end-user industries, such as post and parcel services, food and beverages, and the e-commerce industry. Factors such as increasing labor costs and changing consumer buying behavior have bolstered the demand for faster and more accurate delivery operations, which have, in turn, developed a considerable demand for automated sortation systems.

Modern manufacturing facilities in the region rely on new technologies and innovations to produce higher quality products at faster speeds, with lower costs. Implementing smart software and hardware proves to be the only feasible way to survive in the current competitive market.

Further, the growing adoption of industrial automation to enhance efficiency in the manufacturing and processing sectors is also expected to boost the adoption of sortation systems in the region. New technologies and innovations have further mandated the need for several regulations across the industries.

For instance, the FDA Food Safety Modernization Act (FSMA) is transforming the operations of food companies by shifting the focus from responding to foodborne illness and foreign material contamination to preventing it. This makes the industry highly regulated to meet food safety norms that promote automation in material handling. This factor is expected to drive the sortation system in the food and beverage industry over the forecast period.

The significant growth of the retail and e-commerce sector and warehouse expansion is another primary driver of the studied market growth. E-commerce sales contributed to about 14.3% of total retail sales in the third quarter of 2020, of which Amazon accounted for more than a third of all e-commerce sales in the United States.

Most of the retailers in the region are planning to automate their warehouse establishments rather than expanding in such a high-priced rental environment. However, almost 80% of the warehouses in the region are still manually operated.

United States is Expected to Account for Major Market Share

The United States is one of the largest and most advanced markets for automated solutions globally. The strong economy, with notable port traffic, increased e-commerce activity, and key manufacturing indices, all resulting in significant growth in manufacturing, drive the demand for automated solutions across the logistics sector in the country.

Sectors, including retail, automotive, food and beverage, and pharmaceutical, are the largest sources of demand for automated logistics solutions in the country. Food and beverage is the largest industry and represents more than 35% of all US packaging shipments annually.

This creates a significant demand for equipment, such as palletizers, unit load AGVs, tug AGVs, and sortation systems, which are extensively deployed in food and beverage manufacturing establishments. Moreover, the stringent food safety regulations and preference for low human intervention in the production process are expected to increase the demand for the food and beverage industry over the forecast period.

The region is witnessing numerous partnerships and is relying on the latest technologies and innovations to manufacture a higher quality of products at quicker speeds and cheaper costs.

For instance, recently, a principal American retail company, Kroger, started a partnership with the UK online supermarket, Ocado, to utilize its technology to handle warehouse operations, logistics, automation, and delivery route planning in the region. This partnership is set to transform the retail sector, with the aid of automation solutions, in the United States.

Additionally, owing to low vacancy and a surge in the rental prices of warehouses, enterprises are progressively looking for smaller places to rent out for warehouse purposes. In order to optimize the productivity of these narrow spaces, they are expected to deploy more automated solutions soon.

Also, the major companies with many warehouses and distribution units utilize acquisition strategies to reduce labor costs and increase their profitability. For instance, Amazon, the giant retail, has spent USD 775 million in 2012 to acquire a young robotics company called Kiva Systems that gave it ownership over a new breed of mobile robots. This investment gave a technical foundation for building new versions of warehouse robotics, setting the stage for a potential future of the robots.

North America Logistics Automation Industry Overview

The market vendors that can fabricate and integrate the required equipment within the approved capital budgets and expected leads times have been continuing to dominate the market. The logistics automation market comprises several global players, vying for attention in a fairly-contested market space.

Technological disruption has been a key factor in sustainable competitive advantage. Also, in order to differentiate amongst offerings, the players have been witnessed moving toward the service capabilities. For instance, Locus considered the training aspect of its technology, and its LocusEmpower solution aids in training and the company claims it would onboard workers in days, rather than months.

Some of the prominent players in the market include Honeywell, Swisslog, Daifuku, Schaefer, among others. The presence of these players and their constant innovative activities are intensifying the market scenario. As the market poses moderate barriers to entry for new players, several new entrants backed by VC's have been able to gain traction in the market. This could further intensify the market competition.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions & Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Intensity of Competitive Rivalry

4.3.5 Threat of Substitute Products

4.4 Impact of COVID-19 on the Industry Ecosystem

4.5 Market Drivers

4.5.1 Increased E-commerce Activity

4.6 Market Challenge

4.6.1 High Capital Investment & Nascency Of The Technology

5 MARKET SEGMENTATION

5.1 By Solution Type

5.1.1 Hardware

5.1.1.1 Mobile Robots (Automated Guided Vehicle (AGV) and Autonomous Mobile Robots (AMR))

5.1.1.2 Automated Storage and Retrieval System (AS/RS) (Unit Load - Fixed and Movable Aisle, Mini Load, Shuttle & Bot Systems and Other Systems - Carousels and Vertical Lift Modules)

5.1.1.3 Conveyor (Belt, Roller, Pallet and Overhead)

5.1.1.4 Palletizer/De-palletizer (Conventional - High Level + Low Level, and Robotic)

5.1.1.5 Sortation System

5.1.2 Software - Warehouse Management Systems (WMS), WES and WCS