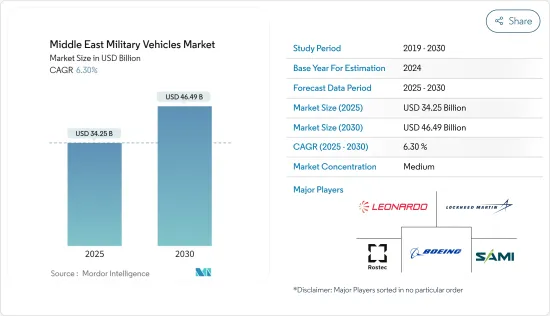

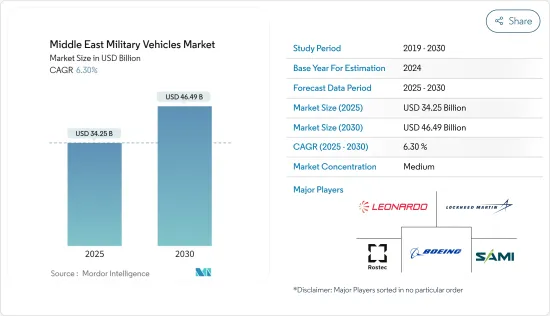

중동의 군용 차량 시장 규모는 2025년 342억 5,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 6.3%로 확대되어, 2030년에는 464억 9,000만 달러에 달할 것으로 예측됩니다.

사우디아라비아, 이스라엘, 아랍에미리트(UAE)과 같은 국가들이 현대 군사 차량을 운영하는 반면, 이 지역의 일부 국가들은 현대화가 필요한 소련 시대의 차량을 보유하고 있습니다. 따라서 이 나라들은 새로운 군사 차량의 조달에 투자하고 있습니다.

게다가, 군용 차량의 노후화에 의해 앞으로 수년간 유효하게 기능시키는 경우, 차량의 효율성, 살상 능력, 세련성을 향상시키기 위한 업그레이드 프로그램에 투자를 강요받고 있는 국가도 있습니다.

신흥국의 밀리터리 차량의 근대화와 확대가 건전한 페이스로 진행되고 있는 한편, 이 지역은 자국 생산 능력을 개발함으로써 자급자족과 외국으로부터의 독립을 강화하고 있습니다. 일부 국가는 자체적으로 군사 차량을 개발하거나 외국 파트너와 제휴하여 기술 이전 협정의 도움으로 현지에서 차량을 제조하고 있습니다.

그러나 원유가격 변동 등의 요인은 중동의 여러 나라의 경제에 영향을 미치고 있으며, 군사비의 성장에도 영향을 미치고 있습니다.

지난 몇 년동안 예멘, 리비아, 소말리아에서의 분쟁과 시나이 반도의 반란으로 인해 중동의 군비 조달이 급격히 증가했습니다.

UAE는 능력 개발을 계속하기 위해 UAE군의 전부대를 신예의 군사 장비로 근대화할 계획입니다. 예를 들어, 2023년 2월 프랑스의 주요 육상 방위 기업인 Nexter는 UAE군의 주요 공급업체인 International Golden Group과 UAE군의 루클레르 주력전차(MBT) 근대화를 위한 제휴 계약을 체결했습니다.

UAE는 또한 병력 보호 강화, 인도주의 지원 활동 실시, 중요한 인프라 보호에 MRAP 차량을 활용할 의향입니다. 2023년 2월, Rabdan 8x8 보병 전투차(IFV) 400대의 첫번째 배치가 UAE 육군에 납품되었으며, 제조업체인 Otokar는 향후 추가 주문을 기대하고 있습니다.

이란에는 일련의 개조를 실시함으로써 화력 지원 등의 임무를 수행하기 위한 장비가 가능한 장륜 장갑차와 모래 장갑차가 매우 많이 존재합니다. 예를 들어 BTR50, 60 시리즈, BMP1, 2병원 수송차 등이 그 예입니다. 이러한 장갑차 보유 수를 급속히 늘리는 중동 국가 정부의 견고한 계획은 앞으로 수년간 밀리터리 차량 시장의 성장을 가속할 것으로 예상됩니다.

터키는 방위 산업에 대한 투자와 생산 확대에 주력하고 있습니다. 최근 국내 설계 및 생산에 대한 주력은 러시아와 다양한 과격파 조직으로부터의 잠재적 위협 증가와 NATO 동맹국에 의한 터키의 방위 산업 제재에 기인하고 있습니다. 이러한 상황에서 2023년 5월, 터키의 FNSS Defence Systems는 터키 육군의 ACV-15 신형 장갑 병원 수송차(AAPC)의 능력 강화를 제공하는 계약을 맺었습니다. 이 계약은 차량의 성능을 향상시키고 서비스 수명을 20년 연장하기 위해 체결되었습니다. 이 회사에 따르면 미공표 수의 AAPC에 최신 서브 시스템이 탑재되어 더 많은 임무를 지원하고 전장에서의 고급 위협에 대처할 수 있습니다.

터키의 조달 및 방위 당국은 기존 F-16 블록 30 전투기의 구조 수명을 8,000 비행 시간에서 12,000 비행 시간으로 연장하는 것을 목표로 한 프로그램을 시작했습니다. 이 업그레이드는 1대당 1,200-1,500개의 부품으로 확장될 수 있습니다.

게다가, 터키는 장갑차 제조에서 크게 발전하고 있으며, 함대를 현대화하기 위해 새로운 차량을 획득하고 있으며, 시장 성장에 더욱 기여하기 위해 해군 함대 업그레이드에 관심을 가지고 있습니다. 예를 들어 2023년 4월, 터키 해군은 터키 최초의 상륙용 플랫폼 도크인 수륙 양용 강습 양륙함 TCG Anadolu를 수령했습니다. 동군은 동함으로부터 중 헬리콥터, 무인기, 경공격기를 배치할 예정입니다.

중동 밀리터리 차량 시장은 반고정적이며 여러 국내외 기업들이 더 큰 시장 점유율을 겨루고 있습니다.

밀리터리 차량의 국산화에 주목이 모여 있기 때문에 예측 기간 중에 현지 기업의 시장 점유율이 높아질 것으로 예상됩니다. 터키, 사우디아라비아, 아랍에미리트(UAE)과 같은 국가들이 국산화의 전면 주자입니다. 예를 들어, 사우디아라비아는 사우디아라비아 정부의 비전 2030에 따라 군비와 무기의 수출 의존도를 줄이기 위해 방위 무기와 탄약의 생산 능력을 강화하는 데 주력하고 있습니다. 이 정부는 2030년까지 국내 군사 장비 지출을 50%까지 늘릴 계획입니다. Saudi Arabian Military Industries(SAMI), BMC Otomotiv Sanayi ve Ticaret AS, Denel SOC Ltd가 유명한 현지 제조업체입니다.

The Middle East Military Vehicles Market size is estimated at USD 34.25 billion in 2025, and is expected to reach USD 46.49 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

While countries like Saudi Arabia, Israel, and the United Arab Emirates operate modern military vehicles, several countries in the region possess Soviet-era vehicles that require modernization. Hence, these countries are investing in the procurement of new military vehicles.

In addition, the aging fleet of military vehicles is also forcing some countries to invest in upgrade programs to improve the efficiency, lethality, and sophistication of the vehicles if they are slated to be effectively functional for some more years.

While the modernization and expansion of the region's vehicle fleets continue at a healthy pace, the region is also becoming increasingly self-sufficient and independent of foreign countries by developing indigenous manufacturing capabilities. Several countries have been developing military vehicles on their own or are partnering with their foreign counterparts and manufacturing vehicles locally with the help of technology transfer agreements.

However, factors like fluctuations in oil prices are affecting the economies of several countries in Middle East, in turn affecting growth in military spending.

Over the past few years, the military equipment procurement of the region increased at a rapid pace, due to the conflicts in Yemen, Libya, and Somalia and the Sinai insurgency.

UAE plans to modernize all units of the UAE armed forces with new and advanced military equipment to continue developing capabilities. For instance, in February 2023, Nexter, the leading French land defense company, signed a teaming agreement with International Golden Group, the leading supplier of the UAE Armed forces, to prepare for the modernisation of the UAE Army's Leclerc main battle tank (MBT).

The UAE also intends to utilize the MRAP vehicles to increase force protection, conduct humanitarian assistance operations, and protect critical infrastructure. In February 2023, the first batch of 400 Rabdan 8x8 infantry fighting vehicles (IFVs) was delivered to the UAE Army and manufacturer Otokar is hopeful that additional orders will be placed in the future.

Iran has a very large fleet of wheeled and sand-blasted armored vehicles that can be equipped to carry out missions such as fire support by making a series of modifications. For example, BTR 50 and 60 series and BMP 1 and 2 personnel carriers are among these armored vehicles. Such robust plans of the government of countries in Middle East to rapidly increase the fleet of armored vehicles are anticipated to propel the growth of the military vehicles market in the coming years.

Turkey has been significantly investing in its defense industry and expanding production. The recent focus on domestic design and production stems from an increase in potential threats from Russia and various militant groups and from sanctions placed on Turkey's defense industry by its NATO allies. In this context, in May 2023, Turkey's FNSS Defence Systems was contracted to provide capability enhancement to the Turkish Army's ACV-15 advanced armored personnel carriers (AAPCs). The agreement was signed to boost the vehicle's performance and extend its service life for an additional 20 years. According to the company, an undisclosed number of AAPCs will be fitted with modern subsystems to support more missions and help address sophisticated threats on the battlefield.

Turkey's procurement and defense authorities have launched a program designed to increase the structural life of the country's existing fleet of F-16 Block 30 jets from 8,000 flight hours to 12,000. The upgrades may cover 1,200 to 1,500 parts per aircraft.

In addition, Turkey has vastly advanced in armored vehicle manufacturing and is acquiring new vehicles to modernize its fleet and with its interest in upgrading its naval fleet to further contribute to the growth of the market. For instance, in April 2023, the Turkish Navy received its largest vessel, the amphibious assault ship TCG Anadolu which is Turkey's first landing platform dock. The military will deploy heavy helicopters, drones and light-attack aircraft from the vessel.

The Middle East military vehicles market is semi-consolidated and is marked by the presence of several local and international players vying for a larger market share. Some of the prominent players include Rostec, Lockheed Martin Corporation, The Boeing Company, Saudi Arabian Military Industries (SAMI), and Leonardo S.p.A.

The growing focus on indigenous manufacturing of military vehicles is anticipated to increase the market share of local players during the forecast period. Countries like Turkey, Saudi Arabia, and the United Arab Emirates are the frontrunners in indigenous manufacturing. For instance, Saudi Arabia is focused on enhancing its defense weapon and ammunition manufacturing capability to reduce its dependency on the export of military equipment and weapons in line with the Saudi government's Vision 2030. The government plans to increase the local military equipment spending to 50% by 2030. Saudi Arabian Military Industries (SAMI), BMC Otomotiv Sanayi ve Ticaret AS, and Denel SOC Ltd are prominent local manufacturers.