유럽의 바이오디젤 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Biodiesel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690774

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

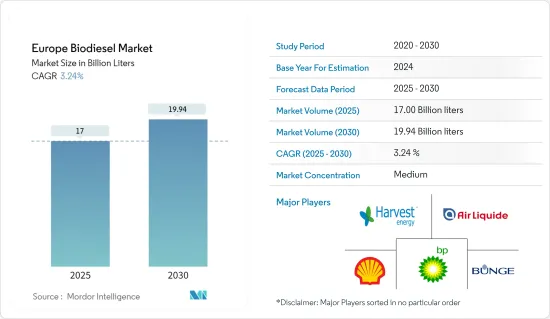

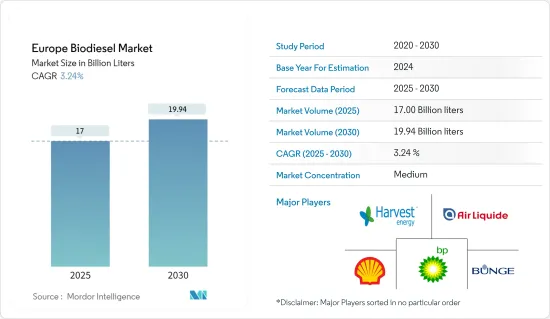

유럽의 바이오디젤 시장 규모는 2025년에 170억 리터로 추정되고, 2030년에는 199억 4,000만 리터에 달할 것으로 예측되며, 예측기간 중(2025-2030년)의 CAGR은 3.24%를 나타낼 전망입니다.

주요 하이라이트

중기적으로는 정부 지원 정책 및 규제, 에너지 안보에 대한 우려와 같은 요인이 예측 기간 동안 시장을 주도 할 것으로 예상됩니다.

반면에 식물성 기름 및 동물성 지방과 같은 공급 원료의 가용성과 가격은 예측 기간 동안 시장의 성장을 저해 할 것으로 예상됩니다.

그럼에도 불구하고 연구 개발 노력은 대체 바이오디젤 생산 공급 원료를 찾는 데 초점을 맞추고 있습니다.

독일은 예측 기간 동안 시장을 지배할 것으로 예상됩니다.

유럽의 바이오디젤 시장 동향

팜유가 시장을 독점할 전망

팜유는 전 세계적으로 가장 널리 생산되는 식물성 오일 중 하나입니다.

팜유는 에너지 함량이 높아 바이오디젤 생산에 효율적인 공급원료입니다.

또한 팜유는 낮은 점도와 높은 윤활성 등 바이오디젤 생산에 유리한 특성을 지니고 있습니다.

2021년과 2022년 사이에 유럽으로 수입되는 바이오디젤의 가치가 크게 증가했습니다.

2022년 12월, 유럽연합은 기업들이 유럽연합 내에서 판매하는 팜유 및 기타 상품이 삼림 벌채와 관련이 없다는 증거를 제공하도록 의무화하는 규정을 도입하기로 예비 합의에 도달했습니다.

따라서 위에서 논의한 사항에 따라 팜유 부문은 예측 기간 동안 시장을 지배할 가능성이 높습니다.

시장을 독점하는 독일

독일은 바이오디젤을 포함한 재생 에너지를 장려하기 위해 지원 정책과 규제를 시행하고 있습니다.

독일은 야심찬 재생 에너지 목표를 가지고 있으며 바이오디젤 생산에 대한 재정적 인센티브와 보조금을 제공합니다.

2022년 2월 Renewable Energy Group은 독일의 엠덴에 있는 바이오디젤 정유공장의 전처리 능력을 강화할 계획을 발표했습니다.

독일은 바이오디젤의 생산, 유통, 사용을 위한 인프라가 잘 발달되어 있습니다.

2022년 독일의 바이오디젤 소비량은 251만 6,000톤(약 7억 5,500만 갤런)으로, 2021년 256만 톤(약 7억 6,850만 갤런)에서 감소했습니다. 반면 혼합 에탄올의 사용량은 2.9% 가까이 증가하여 115만 3,000톤(약 3억 8,600만 갤런)에서 118만 6,000톤(약 3억 9,700만 갤런)으로 증가했습니다.

따라서 위에서 언급한 바와 같이 독일은 유럽의 바이오디젤 시장에서 중요한 역할을 할 것으로 보입니다.

유럽 바이오디젤 산업 개요

유럽의 바이오디젤 시장은 반쯤 세분화되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

시장 규모와 수요 예측(-2028년)

정부의 규제와 시책

최근 동향과 개발

시장 역학

성장 촉진요인

정부 지원 정책 및 규정

에너지 안보

억제요인

공급 원료 가용성 및 가격 변동성

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

원료

유채 기름

팜유

사용한 식용유

기타 원료

바이오디젤 블렌드

B5

B20

B100

지역

독일

스페인

영국

프랑스

기타 유럽

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Shell PLC

BP PLC

Bunge Limited

Air Liquide SA

Harvest Energy

Abengoa Bioenergia SA

Envien Group

Greenergy International Ltd.

GBF German Biofuels GMBH

제7장 시장 기회와 앞으로의 동향

새로운 첨단 원료

HBR

영문 목차

영문목차

The Europe Biodiesel Market size is estimated at 17.00 billion liters in 2025, and is expected to reach 19.94 billion liters by 2030, at a CAGR of 3.24% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as government-supportive policies and regulations and concerns over energy security are expected to drive the market during the forecasted period.

On the other hand, the availability and price of feedstocks, such as vegetable oils and animal fats, are expected to hinder the market's growth during the forecasted period.

Nevertheless, research and development efforts focus on finding alternative biodiesel production feedstocks. Advanced feedstocks, such as algae and waste oils, offer the potential for improved sustainability, reduced land-use impact, and increased feedstock availability, creating new opportunities for biodiesel production.

Germany is expected to dominate the market during the forecasted period. Due to supportive government policies.

Europe Biodiesel Market Trends

Palm Oil Is Likely To Dominate The Market

Palm oil is one of the most widely produced vegetable oils globally. Major palm oil-producing countries, such as Indonesia and Malaysia, have large-scale plantations and efficient extraction processes, leading to a significant and reliable palm oil supply. This abundant supply gives palm oil a competitive advantage in terms of availability and cost compared to other feedstocks.

Palm oil has a high energy content, making it an efficient feedstock for biodiesel production. Its energy density allows for higher biodiesel yields per unit of feedstock, resulting in cost-effective production. The energy efficiency of palm oil contributes to its attractiveness for biodiesel manufacturers and can potentially drive its dominance in the market.

Moreover, palm oil possesses favorable properties for biodiesel production, such as its low viscosity and high lubricity. These properties enhance the performance of biodiesel in diesel engines and make it compatible with existing diesel infrastructure. The favorable properties of palm oil-based biodiesel contribute to its market potential and competitiveness.

The value of biodiesel imported into Europe has increased significantly between 2021 and 2022. According to Statista, the total import value for biodiesel increased by more than 36%, signifying increased biodiesel consumption in the regions.

In December 2022, the European Union reached a preliminary agreement to introduce a regulation that would mandate companies to provide evidence that their palm oil and other commodities sold within the EU are not linked to deforestation.

Therefore, per the points discussed above, the palm oil segment will likely dominate the market during the forecasted period.

Germany to Dominate the Market

Germany has implemented supportive policies and regulations to promote renewable energy, including biodiesel. The country has ambitious renewable energy targets and offers financial incentives and subsidies for biodiesel production. This support encourages investment and growth in the biodiesel industry, positioning Germany as a key player.

Germany is known for its advanced engineering and technological expertise. The country has a strong research and development infrastructure, enabling innovative biodiesel production technologies to be developed and implemented. German companies are at the forefront of developing efficient and cost-effective biodiesel production processes, giving them a competitive advantage in the market.

In February 2022, Renewable Energy Group announced its plans to enhance the pretreatment capacity at its biodiesel refinery in Emden, Germany. This expansion aims to enable the processing of challenging feedstocks into renewable fuel feed, including those that are typically difficult to convert.

Germany has a well-developed infrastructure for producing, distributing, and using biodiesel. The country has many biodiesel production plants, an extensive blending facility network, and fueling stations. This existing infrastructure provides a solid foundation for the growth and dominance of the biodiesel market in Germany.

In 2022, Germany's biodiesel consumption amounted to 2.516 million metric tons (around 755 million gallons), decreasing from 2.560 million tons (approximately 768.5 million gallons) in 2021. In contrast, ethanol utilization in blends grew nearly 2.9 percent, rising from 1.153 million tons (386 million gallons) to 1.186 million tons (approximately 397 million gallons).

Therefore, as per the points mentioned above, Germany is likely to be a significant player in the biodiesel market in Europe.

Europe Biodiesel Industry Overview

Europe's biodiesel market is semi fragmented. Some of the major players in the market (in no particular order) include Shell PLC, BP PLC, Bunge Limited, Air Liquide SA, Harvest Energy, and others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast, until 2028

4.3 Government Policies and Regulations

4.4 Recent Trends and Developments

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Government Supportive Policies and Regulations

4.5.1.2 Energy Security

4.5.2 Restraints

4.5.2.1 Feedstock Availability and Price Volatility

4.6 Supply-Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Feedstock

5.1.1 Rapeseed Oil

5.1.2 Palm Oil

5.1.3 Used Cooking Oil

5.1.4 Other Feedstocks

5.2 Biodiesel Blends

5.2.1 B5

5.2.2 B20

5.2.3 B100

5.3 Geography

5.3.1 Germany

5.3.2 Spain

5.3.3 United Kingdom

5.3.4 France

5.3.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements