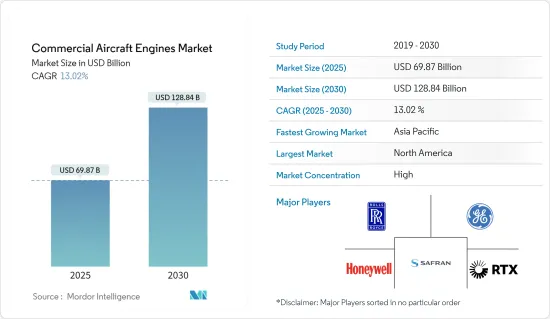

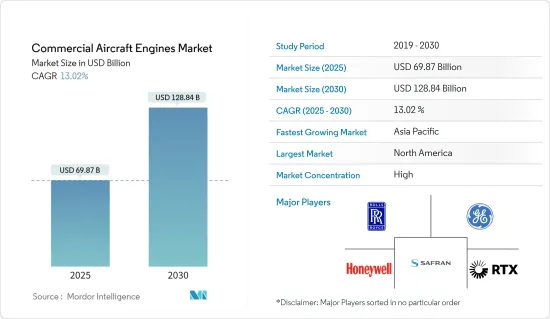

민간 항공기 엔진 시장 규모는 2025년에 698억 7,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 13.02%로 성장할 전망이며, 2030년에는 1,288억 4,000만 달러에 달할 것으로 예측됩니다.

세계 항공 여객 수송량 증가가 신형 상용 항공기 수요 증가로 이어져 민간 항공기 엔진 시장의 성장을 견인하고 있습니다. 아시아태평양과 중동 및 아프리카의 각 도시에서 새로운 중형 및 소형 공항의 개발은 새로운 노선에 취항하는 새로운 항공기 수요를 촉진하여 민간 항공기 엔진 시장의 관련 성장을 이끌고 있습니다.

기술 혁신은 이 시장의 성장을 크게 뒷받침하고 있습니다. 신형 모델의 개발에 의해 경량화, 노이즈 풋 프린트의 저감, 배출 가스의 저감, 고추력화, 정비 작업 경감 등이 실현되고 있습니다. 그러나 첨단 엔진의 연구개발 사이클이 불안정하기 때문에 세계 경제 격차의 영향을 받기 쉽고 시장은 경기 변동에 시달리고 있습니다. 앞으로는 경량화, 공간 절약화, 고출력화 등 배터리 기술의 개발에 의해 완전 전동화가 달성될 때까지 하이브리드 추진 엔진이 개발, 채용될 것으로 보입니다.

트윈아일 항공기라고 불리는 와이드 바디 항공기는 7석 이상의 좌석을 나란히 하여 2개의 승객 통로를 확보할 수 있는 폭의 몸통을 가진 여객기입니다. 일반적인 몸통의 직경은 5-6m(16-20피트)입니다. 보잉 B777X형기나 에어버스 A350형기는 세계 각지에서 취항하고 있는 와이드 바디기의 일례입니다.

항공사는 와이드 바디 기계를 화물 운송에 사용합니다. 이러한 항공기의 높은 수요는 2023년까지 계속된 것으로 평가되었습니다. 개발 업체는 이러한 수요에 부응하기 위해 첨단 엔진을 개발했습니다. 예를 들어, 2023년 2월, 타타 샌즈 산하의 에어 인디아는 GE 에어로 스페이스와 40기의 GEnx-1B 엔진과 20기의 GE9X 엔진의 조달 계약과 다년간의 TrueChoice 엔진 서비스 계약을 체결했습니다. 이 계약은 이 항공사가 보잉 B777X형기 10기와 보잉 B787형기 20기를 확정 발주한 것과 협조하여 체결되었습니다.

에미레이트 항공은 2023년 11월 보잉 B777X형기에 탑재하는 202기의 GE9X형 엔진의 발주를 발표했습니다. 이 주문에는 장기 서비스 계약도 포함됩니다. 이로 인해 에미레이트 항공은 GE9X 엔진을 총 460개 주문했습니다. 2022년 5월, 호주 항공사 캔터스 항공은 롤스로이스 토렌트 XWB-97을 탑재한 A350-1000형기 12기의 계약에 커밋할 것을 발표했습니다. 이 항공기는 런던과 뉴욕과 호주 동해안의 도시 시드니와 멜버른을 직행 항공편으로 연결하는 세계에서 가장 긴 민간 직행 항공편의 운항을 목표로 하는 항공사의 목표를 지원합니다. 이것은 동업 항공사와 항공기 엔진 조달 파트너십으로 이어집니다. 초점은 대륙간 이동에 가장 적합한 와이드 바디 기계입니다. 항공기 엔진 제조업체가 제공하는 와이드 바디 항공기를 위한 여러 파트너십과 혁신을 통해 이 부문은 예측 기간 동안 크게 성장할 것으로 예상됩니다.

아시아태평양은 예측 기간 동안 가장 높은 성장을 보일 것으로 예측됩니다. 항공사의 기체 확대 계획과 화물 서비스 증가로 새로운 여객기와 화물기의 조달이 가속화되고 있으며 예측 기간 동안 항공기 엔진 시장에 긍정적인 영향을 미칠 것으로 보입니다.

현재 최신 C919를 포함하여 중국에서 생산되는 민간 항공기에는 외국제 엔진이 탑재되어 있습니다. 그러나 일본은 첨단 기술의 해외 공급원 의존성을 줄이기 위해 국산 대체 엔진 개발을 시도하고 있습니다. 중국은 CJ1000의 개발을 진행하고 있습니다. CJ1000은 향후 3년에서 5년 사이에 국산 내로우 바디 기계 C919의 동력원으로 설계된 터보 팬 제트 엔진입니다.

2023년 6월, 차이나 에어라인은 증가하는 보잉 787 드림라이너 민간 제트기의 동력원으로서 제너럴 일렉트릭(GE) 에어로스페이스사로부터 17기의 GEnx-1B 엔진과 예비품을 수주했습니다. 이 항공은 현재 여객기 66대와 화물기 21대를 포함한 87대를 운항하고 있습니다.

인도 민간 항공국(DGCA)의 보고에 따르면 2022년 인도의 총 여객 수는 1억 500만 명 이상에 달했습니다. 국제항공운송협회(IATA)에 따르면 인도는 향후 10년간 2030년까지 중국과 미국을 제치고 세계 3위 항공 여객 시장이 될 것으로 예상되고 있습니다. 따라서 항공사는 보유재를 확대하고 확대하는 시장 기회에 대응하기 위해 대규모 조달 계획을 진행하고 있습니다. 2023년 6월, 인디고는 Airbus A320 제품군을 500대 주문했습니다. 이 인디고 주문서는 A320NEO, A321NEO, A321XLR 믹서로 구성되어 있습니다. 이러한 항공사 및 항공기 운항 회사의 항공기 현대화 계획은 예측 기간 동안 항공기 엔진 시장의 민간 부문 성장을 가속할 것으로 예상됩니다.

민간 항공기 엔진 시장은 통합되어 있으며, General Electric Company, Safran SA, Pratt & Whitney (RTX Corporation), Rolls-Royce PLC, 및 Honeywell International Inc. 등의 대기업이 시장을 독점하고 있습니다. 민간 항공기 엔진 시장에서는 항공기의 경량화와 저연비화를 실현하는 신기술을 창출하기 위한 공동 개발 및 공동 개발 프로그램이 진행되고 있습니다. 세계의 민간 항공기 엔진 제조업체는 또한 저비용 노동력을 사용할 수 있으며 항공 산업이 성장함에 따라 아시아태평양과 같은 제조 생태계에 투자하고 있습니다. 시장 기업의 주요 수익 창출 전략은 항공기 제조업체에서 엔진 및 엔진 MRO 서비스 계약 및 주문을 획득하는 것입니다.

The Commercial Aircraft Engines Market size is estimated at USD 69.87 billion in 2025, and is expected to reach USD 128.84 billion by 2030, at a CAGR of 13.02% during the forecast period (2025-2030).

The rise in global air passenger traffic is leading to a growth in the demand for new commercial aircraft, driving the growth of the commercial aircraft engines market. The development of new medium- and small-sized airports in cities across Asia-Pacific and Middle East and Africa is propelling the demand for new aircraft to serve the new routes, thereby driving related growth of the commercial aircraft engines market.

Technological innovations are significantly fueling the growth of the market studied. The development of new models results in weight reduction, fewer noise footprints, fewer emissions, high thrust, reduction in maintenance operations, etc. However, the market is marred by economic fluctuations as the tenuous R&D cycle of advanced engines renders the players vulnerable to global economic disparities. In the future, hybrid propulsion engines will be developed and adopted until full electrification is achieved through the development of battery technology in areas such as weight reduction, less space requirement, and high power.

A wide-body aircraft, called twin-aisle aircraft, is an airliner with a fuselage wide enough to accommodate two passenger aisles with seven or more seats abreast. The typical fuselage diameter is 5 to 6 m (16 to 20 ft). Boeing B777X and Airbus A350 are examples of wide-body aircraft in service across various world geographies.

Airlines use wide-body aircraft to ferry goods. The high demand for such aircraft was expected to continue until 2023. Manufacturers developed advanced engines to meet the demand. For instance, in February 2023, Air India, a part of Tata Sons, signed a procurement contract for 40 GEnx-1B and 20 GE9X engines and a multi-year TrueChoice engine services agreement with GE Aerospace. The deal was signed in coordination with the airline's firm order for 10 Boeing B777X and 20 Boeing B787 aircraft.

In November 2023, Emirates announced an order for 202 GE9X engines to power its upcoming fleet of Boeing B777X aircraft. The order also includes a long-term services agreement. This brings Emirates' total order for GE9X engines to 460. In May 2022, the Australian carrier Qantas announced its commitment to a deal for 12 Rolls Royce Trent XWB-97 powered A350-1000 aircraft that will support the airline's aim to operate the world's longest commercial non-stop flights, allowing passengers to fly direct between London and New York to the Australian east coast cities of Sydney and Melbourne. This leads to aircraft engine procurement partnerships with airlines in the industry. The focus is on wide-body aircraft that are ideal for intercontinental travel. With multiple partnerships and innovations by aircraft engine manufacturers for wide-body aircraft, this segment is expected to grow significantly during the forecast period.

Asia Pacific is projected to show the highest growth during the forecast period. Fleet expansion plans of airlines and increasing cargo services are accelerating the procurement of new passenger and cargo aircraft, which will possess a positive stance on the aircraft engine market during the forecast period.

Currently, the commercial aircraft produced in China, including the latest C919, are equipped with foreign engines. However, the country has been trying to develop a home-grown alternative as it seeks to cut its dependence on foreign sources of sophisticated technology. China is progressing with the development of CJ1000, a turbofan jet engine designed to power the homemade C919 narrow-body aircraft in the next three to five years.

In June 2023, China Airlines made an order for 17 GEnx-1B engines and spares from General Electric (GE) Aerospace to power its growing fleet of Boeing 787 Dreamliner commercial jets. The Airline currently operates a fleet of 87 aircraft, including 66 passenger jets and 21 freighters.

According to a report by the Indian Directorate General of Civil Aviation (DGCA), in 2022, India's total air passenger traffic reached more than 105 million passengers. According to the International Air Transport Association (IATA), India is expected to overtake China and the United States as the world's third-largest air passenger market in the next ten years by 2030. Hence, the airlines are undertaking massive procurement plans to expand their fleet and address the growing market opportunity. On this note, in June 2023, IndiGo ordered 500 Airbus A320 Family aircraft. This IndiGo order-book comprises a mix of A320NEO, A321NEO and A321XLR aircraft. Such fleet modernization plans of the airlines and aircraft operators are expected to drive the growth of the commercial segment of the aircraft engines market during the forecast period.

The commercial aircraft engines market is consolidated, with major players, such as The General Electric Company, Safran SA, Pratt & Whitney (RTX Corporation), Rolls-Royce PLC, and Honeywell International Inc., dominating the market. The commercial aircraft engine market is witnessing collaborations and joint development programs for creating new technologies for lighter and fuel-efficient aircraft. Global commercial aircraft engine manufacturers are also investing in the manufacturing ecosystems in regions such as Asia-Pacific, owing to the availability of low-cost labor and the growing aviation industry. The main revenue generation strategy of market players is winning contracts and orders from aircraft manufacturers for engines and engine MRO services.