북미의 산업용 배터리 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

North America Industrial Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690725

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

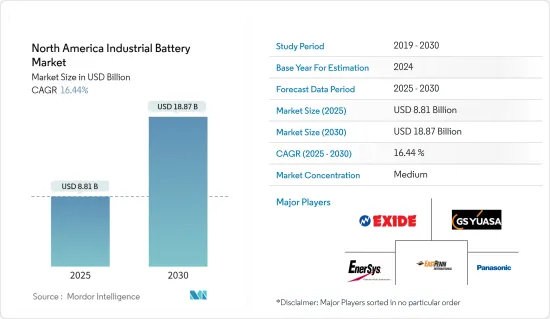

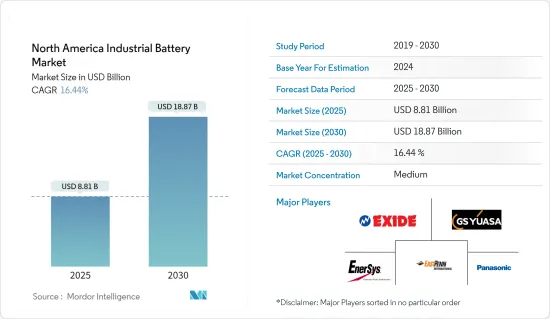

북미의 산업용 배터리 시장 규모는 2025년에 88억 1,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 16.44%로 성장할 전망이며, 2030년에는 188억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

장기적으로는 리튬이온 배터리 가격 하락, 데이터센터, 지역통신산업 수요 증가, 신재생 에너지 통합 증가 등이 시장을 견인하는 주요 요인이 되고 있습니다.

한편, 현지 생산에 필요한 원재료의 매장량이 부족한 것 등이 예측 기간 중 시장 성장률을 억제하는 요인이 되고 있습니다.

그럼에도 불구하고, 기술적으로 첨단 배터리에 대한 주목 증가와 배터리 제조의 연구개발 단계에서 인공지능의 이용 증가는 배터리 기업이 획기적인 배터리 기술을 만들기 위해 투자하고 자원을 돌이킬 수 있는 큰 기회를 만들어낼 가능성이 높습니다.

미국은 재생가능 전력 인프라와 산업 생산 확대로 예측 기간 동안 북미 산업용 배터리 시장을 독점할 것으로 예상됩니다.

북미의 산업용 배터리 시장 동향

리튬 이온 배터리(LIB) 기술이 가장 급성장하는 시장 부문 및 예측

다양한 유형의 산업용 배터리 기술 중에서 리튬 이온 배터리(LIB) 유형은 주로 그 유리한 용량 대 중량비로 인해 예측 기간 동안 북미의 산업용 배터리 시장에서 큰 성장이 예상됩니다. LIB의 채용을 뒷받침하는 기타 요인으로는 성능 향상, 에너지 밀도 향상, 가격 저하 등의 특성을 들 수 있습니다.

세계의 리튬 이온 배터리 제조업체는 리튬 이온 배터리의 비용 절감에 주력하고 있습니다. 리튬 이온 배터리의 가격은 지난 10년간 급락했습니다. 2023년에는 평균 리튬 이온 배터리의 가격이 1kWh당 약 139달러로 평가되었으며 2013년에 비해 82% 이상 감소했습니다. 리튬 이온 배터리 가격의 하락은 산업용 배터리 제조업체가 전자 기기, 소형 및 대형 가전, UPS, 전기 에너지 저장 시스템의 생산을 보다 저렴하게 동원할 것을 촉구할 것으로 보입니다.

미국 정부는 2023년 11월 리튬 이온 등 선진 전지의 국내 생산을 촉진하기 위해 인프라 법의 범위 내에서 35억 달러의 자금 제공을 발표했습니다. 미국에 대한 투자 의제의 일환으로 정부의 자금 지원은 앞으로 몇 년동안 리튬 이온 배터리와 팩의 제조 능력을 돕는 것으로 기대되고 있습니다.

게다가 미국에서는 최근 몇 년간 리튬 이온 기가팩토리의 개발이 진행되고 있습니다. 2024년 2월, EnerSys는 그린빌의 오거스타 글로브 비즈니스 파크에서 평방 피트의 리튬 이온 배터리 제조 장비 개발을 언급했습니다. EnerSys는 2027년까지 미국의 산업방 및 방위 용도 수요에 부응하기 위해 리튬 이온 배터리 셀의 제조를 개시할 예정입니다.

다양한 산업에서 리튬 이온 배터리의 사용이 급증하고 있기 때문에 제어 불가능한 자기 발열이나 폭발의 가능성을 배제하는 데 있어서, 그 안전성은 매우 중요합니다. 그러나 고품질 리튬 이온 배터리의 경우 이러한 사건은 드물지만 안전 점검을 수행하는 것이 결정적으로 중요합니다.

2024년 2월 캐나다 국립연구회의(NRC)는 리튬 이온 배터리 모듈 또는 팩의 단일 셀 열폭주 고장을 평가하는 테스트 기술 개발을 발표했습니다. 열폭주 개시 메커니즘(또는 TRIM) 장치로 알려진 특허 메커니즘은 리튬 이온 배터리 설계 및 부품 테스트에 사용할 수 있습니다. 이는 관련 규제 당국이 배터리 사용자를 위한 안전 지침을 개발할 때 매우 유용합니다.

따라서, 상기 요인에 기초하여, 리튬 이온 배터리 기술은 큰 수요를 나타내며, 예측 기간 동안 북미의 산업용 배터리 시장에서 가장 빠르게 성장하는 부문이 될 것으로 예상됩니다.

미국이 시장을 독점할 것으로 예측

미국은 배터리를 이용한 에너지 저장 프로젝트의 급증, 신재생 전력 인프라의 확대, 견고한 산업 인프라로 인해 세계 산업용 배터리의 주요 핫스팟 중 하나입니다. 게다가 미국에서 에너지 저장 시스템(ESS)의 개발을 지원하는 유리한 정책이 향후 몇 년동안 산업용 배터리 시장을 견인할 가능성이 높습니다.

미국의 배터리 에너지 저장 시스템(BESS) 산업은 국내 신재생 에너지 인프라에 대한 투자 증가에 힘입어 지난 몇 년간 현저한 성장을 이루고 있습니다. 지난 몇 년동안 신재생 에너지의 설비 용량과 발전량은 세계적으로 꾸준히 증가하고 있으며, 미국은 세계 신재생 에너지의 핫스팟 중 하나입니다.

에너지정보국(EIA)에 따르면 2023년 미국은 6.4기가와트의 축전지를 대폭 증설하여 전기용량을 증강했습니다. 이 확장은 신재생 에너지 인프라를 강화하고 화석연료에 대한 의존도를 줄이는 국가의 헌신을 강조했습니다.

국제신재생에너지기구(IRENA)에 따르면, 2013년부터 2023년까지 신재생 에너지의 설비 용량은 2배 이상으로 증가하였고, 2023년 시점에서 미국의 신재생 에너지의 설비 용량은 합계 약 387.54GW에 달했습니다.

미국 에너지정보국에 따르면 미국의 유틸리티 규모의 축전지 용량은 거의 두배로 될 것으로 예상되며 개발자는 2023년 1550만 kW에 1430만 kW를 추가할 계획입니다. 2023년에는 미국의 송전망에 새롭게 6.4GW의 축전지 용량이 추가되어 연간 70% 증가를 기록했습니다. 텍사스는 640만 kW, 캘리포니아는 520만 kW로 신규 용량의 82%를 차지할 것으로 예상됩니다.

게다가 2022년부터 2025년에 걸쳐 개발자가 설치할 계획인 유틸리티 규모의 배터리용량 2,080만 kW의 75%는 텍사스주(790만kW)와 캘리포니아주(760만kW)에 있습니다.

미국에서는 캘리포니아 주 독립 계통 운영 기관(CAISO)과 텍사스 주 전력 신뢰성 평의회(ERCOT)가 가장 큰 축전지 용량을 추가하고 있습니다. 지난 12개월 동안 CAISO의 태양광 발전 용량에서 차지하는 축전지 용량의 비율은 크게 증가하여 2023년 1월의 29%에서 2023년 12월에는 41%까지 상승했습니다.

또한 정부는 미국의 BESS 산업을 견고하게 만들기 위해 국제적인 협력도 적극적으로 확보하고 있습니다. 예를 들어, 2023년 12월, 유럽 위원회는 호주, 미국, 캐나다 각국 정부와 함께 저배출 전력으로의 세계적 전환에서 축전지 추진을 위한 새로운 이니셔티브를 지원했습니다.

COP28 유엔 기후회의에서 발표된 이 이니셔티브는 '배터리 저장의 과충전 이니셔티브'로 불리며, 많은 국가의 에너지부가 회원으로 참여하는 청정 에너지 각료 회의에서 비롯됩니다. 이러한 양국 간의 청정 에너지 활동은 미국이 배터리 에너지 저장 시스템의 견고한 시장을 개척하는 데 도움이 될 것으로 기대됩니다.

따라서 위의 요인들로부터 예측기간 동안 미국이 북미의 산업용 배터리 시장을 독점할 것으로 예상됩니다.

북미의 산업용 배터리 산업 개요

북미의 산업용 배터리 시장은 절반으로 단절되었습니다. 주요 기업(순부동)에는 Exide Industries Ltd, GS Yuasa Corporation, East Penn Manufacturing Company Inc., Panasonic Holding Corporation, EnerSys 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

서문

시장 규모 및 수요 예측(단위 : 달러)(-2029년)

주요 기술 유형별 배터리 가격 동향 및 예측(-2029년)

최근 동향 및 개발

정부 규제 및 정책

시장 역학

성장 촉진요인

리튬 이온 배터리의 비용 저하

성장 억제요인

현지 생산에 필요한 원재료의 부족

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

기술 분야별

리튬 이온 배터리

납축전지

기타 기술(니켈 카드뮴 전지, 니켈 수소 전지, 아연 탄소 등)

용도별

지게차

텔레콤

UPS

기타 용도

지역별

미국

캐나다

기타 북미

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

주요 기업의 전략

기업 프로파일

C&D Technologies Pvt. Ltd

East Penn Manufacturing Company Inc.

EnerSys

Exide Industries Ltd

GS Yuasa Corporation

Leoch International Technology Limited Inc.

Panasonic Holding Corporation

Saft Groupe SA

기타 저명한 기업 목록(Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

시장 랭킹 분석

제7장 시장 기회 및 향후 동향

AJY

영문 목차

영문목차

The North America Industrial Battery Market size is estimated at USD 8.81 billion in 2025, and is expected to reach USD 18.87 billion by 2030, at a CAGR of 16.44% during the forecast period (2025-2030).

Key Highlights

Over the long term, declining lithium-ion battery prices, increasing demand from data centers, regional telecom industries, and rising renewable energy integration are some major factors driving the market.

On the other hand, factors such as the lack of prominent raw material reserves required for local production are likely to curtail the market's growth rate during the forecast period.

Nevertheless, the rising focus on technologically advanced batteries and the growing use of artificial intelligence in the R&D phase of battery manufacturing are likely to create massive opportunities for battery companies to invest and redirect their resources to make breakthrough battery technologies.

The United States is expected to dominate the North American industrial batteries market during the forecast period, owing to the country's expansion in renewable power infrastructure and industrial production.

North America Industrial Battery Market Trends

Lithium-ion Battery (LIB) Technology Projected to be the Fastest-growing Market Segment

Among the different types of industrial battery technologies, the lithium-ion battery (LIB) type is expected to witness significant growth in the North American industrial batteries market over the forecast period, majorly due to its favorable capacity-to-weight ratio. Other factors boosting LIB adoption include properties like better performance, higher energy density, and decreasing price.

Global lithium-ion battery manufacturers are focusing on reducing the cost of lithium-ion batteries. The price of lithium-ion batteries declined steeply over the past ten years. In 2023, the price of an average lithium-ion battery was valued at around USD 139 per kWh, having witnessed a decrease of more than 82% in the price compared to 2013. The decline in lithium-ion battery prices will encourage industrial battery manufacturers to mobilize the production of electronics, small and large appliances, UPS, and electrical energy storage systems at cheaper rates.

In November 2023, the US government announced a funding of USD 3.5 billion under the ambit of its Infrastructure Law to expedite indigenous production of advanced batteries such as lithium-ion in the country. As a part of the Invest in America Agenda, government funding is expected to help lithium-ion cell and pack manufacturing capabilities over the coming years.

Further, the United States has been witnessing the development of lithium-ion gigafactories in recent years. In February 2024, EnerSys noted the development of a square-foot lithium-ion battery manufacturing unit at the Augusta Grove Business Park in Greenville. By 2027, EnerSys plans to start manufacturing lithium-ion battery cells to cater to the demand for industrial and defense applications in the United States.

Owing to the surge in the utilization of lithium-ion batteries across various industries, their safety is of immense importance in eliminating the possibility of uncontrolled self-heating instances and explosions. Such events are, however, rare for high-quality lithium-ion batteries, but it becomes critically important to hold safety checks.

In February 2024, the National Research Council of Canada (NRC) announced the development of a testing technique to assess the single-cell thermal runaway failure of lithium-ion battery modules or packs. The patented mechanism known as the Thermal Runaway Initiation Mechanism (or TRIM) device can be used to test the design and components of lithium-ion batteries. This can significantly help the concerned regulators devise safety guidelines for battery users.

Therefore, based on the abovementioned factors, lithium-ion battery technology is expected to witness significant demand and be the fastest-growing segment of the North American industrial batteries market during the forecast period.

United States Projected to Dominate the Market

The United States is one of the major hotspots for industrial batteries worldwide on account of the surging deployment of battery-based energy storage projects, expansion in renewable power infrastructure, and a robust industrial infrastructure. Moreover, favorable policies backing the deployment of energy storage systems (ESS) in the United States are likely to drive the industrial batteries market over the coming years.

The US battery energy storage systems (BESS) industry has been experiencing notable growth over the past few years, supported by rising investments in renewable energy infrastructure in the country. Over the past few years, the installed renewable energy capacity and generation have been rising steadily globally, and the United States is one of the global renewable energy hotspots.

In 2023, according to the Energy Information Administration (EIA), the United States augmented its electric capacity with a significant addition of 6.4 gigawatts in battery storage, marking a notable 2.2 gigawatt increase over the previous year. This expansion underscored the country's commitment to enhancing its renewable energy infrastructure and reducing reliance on fossil fuels.

According to the International Renewable Energy Agency (IRENA), during 2013-23, installed renewable energy capacity grew by more than two times, and as of 2023, the total installed renewable capacity stood at around 387.54 GW in the United States.

According to the US Energy Information Administration, the US utility-scale battery storage capacity was expected to nearly double, with developers planning to add 14.3 GW to the 15.5 GW in 2023. In 2023, 6.4 GW of new battery storage capacity was added to the US grid, marking a 70% annual increase. Texas and California were expected to contribute 82% of the new capacity, with 6.4 GW and 5.2 GW, respectively.

Moreover, 75% of the 20.8 GW of utility-scale battery capacity planned by developers to be installed from 2022 to 2025 is in Texas (7.9 GW) and California (7.6 GW).

In the United States, the California Independent System Operator (CAISO) and Electric Reliability Council of Texas (ERCOT) have the most large-scale battery storage capacity additions. Over the past twelve months, battery capacity as a percentage of solar generation capacity in CAISO has significantly increased, climbing from 29% in January 2023 to 41% by December 2023.

In addition, the government is also proactively assuring international ties to make a robust BESS industry in the United States. For instance, in December 2023, the European Commission, together with the national governments of Australia, the United States, and Canada, supported a new initiative to promote battery storage in the global transition to low-emission electricity.

This initiative, announced during the COP28 UN Climate Conference, called the 'Supercharging Battery Storage Initiative,' originates from the Clean Energy Ministerial, which includes energy departments from numerous countries as members and participants. Such bilateral clean energy activities are expected to help the United States develop a robust market for battery energy storage systems.

Therefore, based on the abovementioned factors, the United States is expected to dominate the North American industrial batteries market during the forecast period.

North America Industrial Battery Industry Overview

The North American industrial batteries market is semi-fragmented. Some of the major players (not in any particular order) include Exide Industries Ltd, GS Yuasa Corporation, East Penn Manufacturing Company Inc., Panasonic Holding Corporation, and EnerSys.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, Till 2029

4.3 Battery Price Trends and Forecasts, By Major Technology Type, Till 2029

4.4 Recent Trends and Developments

4.5 Government Policies and Regulations

4.6 Market Dynamics

4.6.1 Drivers

4.6.1.1 Declining Costs of Lithium-ion Batteries

4.6.2 Restraints

4.6.2.1 Lack of Prominent Raw Material Reserves Required for Local Production

4.7 Supply Chain Analysis

4.8 Porter's Five Forces Analysis

4.8.1 Bargaining Power of Suppliers

4.8.2 Bargaining Power of Consumers

4.8.3 Threat of New Entrants

4.8.4 Threat of Substitute Products and Services

4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Technology

5.1.1 Lithium-ion Battery

5.1.2 Lead-acid Battery

5.1.3 Other Technologies (Nickel Cadmium Battery, Nickel Metal Hydride, Zinc Carbon, etc.)

5.2 Application

5.2.1 Forklift

5.2.2 Telecom

5.2.3 UPS

5.2.4 Other Applications

5.3 Geography

5.3.1 United States

5.3.2 Canada

5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 C&D Technologies Pvt. Ltd

6.3.2 East Penn Manufacturing Company Inc.

6.3.3 EnerSys

6.3.4 Exide Industries Ltd

6.3.5 GS Yuasa Corporation

6.3.6 Leoch International Technology Limited Inc.

6.3.7 Panasonic Holding Corporation

6.3.8 Saft Groupe SA

6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)