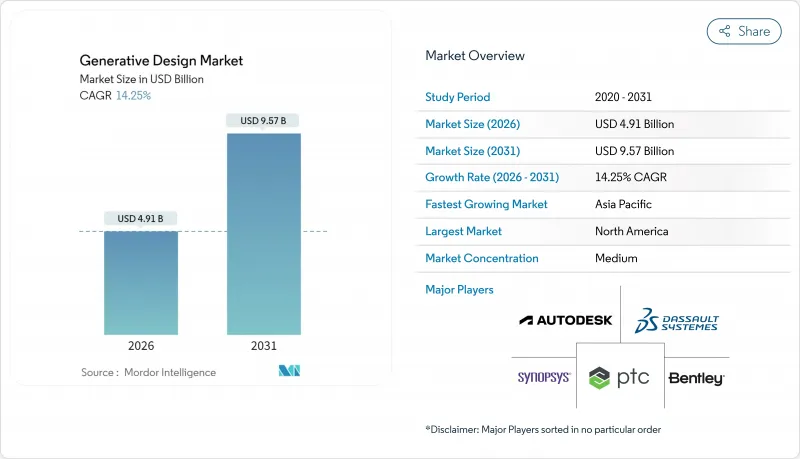

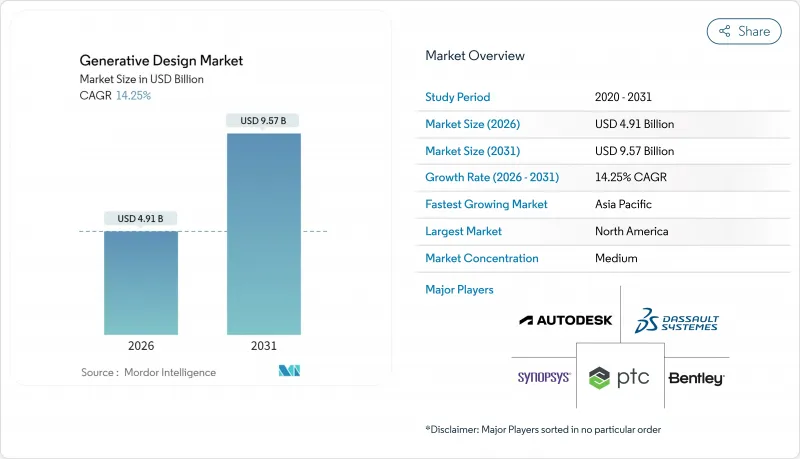

제너레이티브 디자인 시장은 2025년 43억 달러에서 2026년에는 49억 1,000만 달러로 성장해 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 14.25%를 나타낼 전망입니다. 2031년까지 95억 7,000만 달러에 달할 것으로 예측되고 있습니다.

이 확장은 기존 설계→반복이라는 프로세스 대신 엔지니어가 단일 계산 처리로 중량, 비용, 성능을 최적화할 수 있는 AI 퍼스트 설계 워크플로우에 의해 형성되고 있습니다. 클라우드 액세스의 용이성은 중소 제조업체의 진입 장벽을 낮추는 반면, 엄격한 지속가능성 요구 사항은 수명주기 배출량을 줄이는 재료 효율적인 제품을 홍보합니다. 최근 업계 재구성, 특히 Siemens에 의한 Altea의 106억 달러 인수는 발전 설계가 전문적인 엔지니어링 보조 도구가 아니라 핵심 경쟁력으로 인식되고 있음을 보여줍니다. 기존 CAD 공급업체가 AI 알고리즘을 내장하고 AI 네이티브 기업이 클라우드 퍼스트 플랫폼을 제공하는 가운데 경쟁이 격화되고 시장 구조가 완만하면서도 긴밀해지고 있습니다.

규제에 의한 연비 목표나 전기자동차의 항속 거리에 대한 기대로부터, 자동차 제조업체는 충돌 성능을 손상시키지 않고 경량화를 도모할 수밖에 없습니다. 제너럴 모터스에서는 생성 알고리즘을 시트 브라켓에 적용한 프로그램에 의해 안전 기준을 모두 충족하면서 40%의 경량화를 달성. 이것은 종래 다수의 수작업에 의한 반복을 필요로 한 다변수 제약을, AI가 동시에 밸런스 시키는 좋은 예입니다. 항공사도 기체 규모에서 같은 논리를 추구하고 있으며, 에어버스는 토폴로지 최적화에 의해 개발한 객실 분할 브래킷으로 45%의 경량화를 실현. 이로 인해 수천 비행 시간에 걸친 연료 절약 효과가 확대되고 있습니다. 북미와 유럽에서는 배출 가스 규제가 해마다 엄격해지기 때문에 경량화가 직접적인 규제 적합과 비용 절감에 직결되어 가장 강한 긴급성이 요구되고 있습니다. AI 주도의 신속한 재설계를 습득한 공급업체는 새로운 플랫폼 계약을 획득하여 밸류체인 전반의 보급을 가속화하고 있습니다. 경량화의 기준치가 상승하는 가운데, 종래의 설계 수법에서는 대응이 곤란해져, 향후 10년간에 걸쳐 AI 생성 지오메트리에 대한 수요가 높아질 전망입니다.

예전에는 수십만 달러 규모의 하드웨어 투자로 참가가 막혀 있던 중소 제조업체도 월액 불과 1,000달러부터 클라우드 고성능 컴퓨팅을 이용할 수 있게 되어 포춘 500기업과 동등한 계산 규모를 획득하고 있습니다. 이 구독 모델은 아시아태평양의 도입 경제성을 재구성합니다. 이 지역에서는 많은 수탁 제조 기업이 박리로 운영하면서도 세계 OEM 기업에 서비스를 제공합니다. 전용 클라우드 인스턴스는 범용 서버에 비해 생성형 솔버의 해법 시간을 10배 가속화하고 반복 사이클을 며칠에서 몇 시간으로 단축합니다. 엔지니어링 팀은 워크로드를 탄력적으로 마이그레이션하고 설계 스프린트 시 최대 계산량만을 지불하므로 단일 제품 기업이라도 비즈니스 사례가 명확해집니다. 공급자는 향상된 보안 프레임 워크를 번들로 남아있는 지적 재산(IP)의 우려를 완화. 이를 통해 규제 산업은 On-Premise 스토리지와 클라우드 컴퓨팅 버스트를 융합한 하이브리드 모델로 전환하고 있습니다. 그 결과, 제너레이티브 디자인 시장에 진입하는 사용자의 퍼널이 확대되고, 소프트웨어 및 서비스의 양 라인에서의 라이선스 성장이 촉진되고 있습니다.

엔터프라이즈용 생성 플랫폼의 연간 라이선스 번들은 1사용자당 5만-20만 달러의 범위이며, 주류의 CAD 툴보다 자릿수에 비싸고 많은 중소기업에게는 손이 닿지 않는 가격대입니다. 통합 커넥터, 교육 세션 및 워크플로 컨설팅을 가미하면 비용이 더욱 부풀어집니다. 예산을 확보할 수 있어도 신규 사용자가 익숙해지려면 6-12개월이 소요되므로 단기적인 생산성 향상이 제한됩니다. 엔지니어의 급여 수준이 낮은 신흥 국가에서는 소프트웨어 정가가 세계 수준으로 연결되어 있기 때문에 비용 대 급여 비율이 특히 까다로운 상황입니다. 공급업체는 종량제 라이선싱으로 대응하고 있지만, 자본 예산이 희박하고 투자 회수 기간이 짧은 분야에서는 도입이 늦어지고 있습니다. 가격 모델이 더 진화하지 않는 한, 제조업의 일부는 도입을 앞두고 제너레이티브 디자인 시장의 단기적인 확대는 둔화될 것입니다.

제너레이티브 디자인 시장에서 서비스 분야는 가장 높은 성장 궤도를 기록하고 CAGR 14.88%를 향해 상승하고 있습니다. 한편, 소프트웨어 분야는 2025년 시점에서 57.62%의 수익 우위를 유지했습니다. 컨설팅 팀은 제조업체가 AI 솔버를 PLM 시스템에 통합하고, 데이터 파이프라인을 구축하고, 업계 규범을 반영하는 최적화 목표를 사용자 정의할 수 있도록 지원합니다. 개념 증명 단계를 넘는 기업이 늘어남에 따라 통합 복잡성과 변경 관리의 필요성이 높아지고 서비스 수익을 높일 수 있습니다. 주요 공급업체는 워크숍, 파일럿 프로젝트 및 자체 교육 커리큘럼을 패키징하고 단일 라이선스 판매를 능가하는 지속적인 수익원을 확보하고 있습니다.

소프트웨어는 여전히 밸류체인의 핵심을 담당하고 있습니다. 핵심 알고리즘은 독자 기술이며 연간 1만-5만 달러의 고액 구독이 설정되어 있기 때문입니다. 공급업체는 가격 상승을 정당화하고 마진을 지키기 위해 구조 분석, 열 분석, 피로 해석, 탄소 계산 등의 모듈을 지속적으로 추가하고 있습니다. 파일 형식 및 데이터 분석 대시보드로 생태계로 둘러싸여 고객 이탈률은 낮은 수준이지만 소프트웨어와 컨설팅 프로젝트를 결합한 번들 계약을 요구하는 고객이 증가하는 경향이 있습니다. 성공적인 공급업체는 항공우주 좌석 부품 및 정형외과 임플란트와 같은 수직 시장에 신속하게 도입할 수 있는 템플릿을 제공함으로써 차별화를 도모하고 ROI 달성까지의 시간을 단축함과 동시에 서비스 파트너가 증가하는 가운데도 자체 소프트웨어 우위성을 지키고 있습니다.

2025년 시점에서 On-Premise 도입은 제너레이티브 디자인 시장의 61.68%를 차지하고 항공우주 및 방위 분야에서의 엄격한 지적재산 보호규범을 반영했습니다. 이러한 섹터는 자체 설계를 보호하기 위해 경계 관리형 데이터센터 및 직접 연결 GPU 클러스터를 선호합니다. 한편, 중소기업이나 기밀성이 낮은 프로젝트에서는 에어갭 제어보다 탄력적인 컴퓨팅을 중시하기 때문에 클라우드 구독은 CAGR 14.95%를 나타낼 전망입니다. 조기 도입 기업은 마스터 모델을 로컬 저장소에 보관하면서 클라우드에서 감도 분석을 수행하는 하이브리드 패턴을 채택하여 위험과 속도의 균형을 맞추고 있습니다.

클라우드 프로바이더는 전용 설계의 HPC 인스턴스로 제안력을 강화. 수천 코어에 걸쳐 거의 직선적인 스케일링을 실현하여 복잡한 어셈블리의 최적화 실행 시간을 8시간에서 40분으로 단축합니다. 보존시 암호화 및 제로 트러스트 액세스 프레임워크는 많은 컴플라이언스 감사에 대응할 수 있어 신중한 업계의 우려를 완화하고 있습니다. 구독형 라이선싱은 고정 용량이 아닌 실제 계산 사이클에 비용이 연동되기 때문에 더욱 매력적인 조건이 됩니다. 이러한 경제성과 성숙한 보안기준이 융합함에 따라 클라우드 이용에 연동하는 제너레이티브 디자인 시장 규모는 확대될 전망이지만, 규제가 심한 분야에서는 On-Premise 환경의 절대적인 이용량은 지속될 것입니다.

북미는 2025년 세계 수익의 38.02%를 차지했습니다. 이는 자동차 및 항공우주 분야의 초기 파일럿 프로젝트가 기업 규모로의 전개로 성숙한 것, 또 소프트웨어 본사의 근접성이 고객과의 공동 개발 사이클을 가속화했기 때문입니다. 연구개발세제 우대조치와 견조한 벤처자금이 신규 진입기업을 지원하여 보다 광범위한 생태계에 대한 혁신공급을 촉진하였습니다. 성장은 안정되어 있는 것, 신흥 지역에 비하면 완만합니다. Fortune 500에 이름을 붙이는 대부분의 제조업체는 첫 번째 파도의 도입을 이미 완료했으며 현재는 새로운 라이선스보다 스케일 업에 주력하고 있기 때문입니다.

아시아태평양은 가장 급속한 확대를 기록하고 있으며, 중국의 제조업 디지털화 정책, 일본의 Society 5.0 로드맵, 한국의 반도체 경쟁력 강화 계획을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 16.21%를 나타낼 것으로 전망되고 있습니다. 현지 클라우드 제공업체는 소프트웨어 기업과 연계하여 인터페이스의 현지화 및 데이터 거주성 확보를 추진하고 있으며, 지금까지 해외 호스팅에 저항감을 갖고 있던 국내 중소기업에서의 도입을 가속화하고 있습니다. 정부는 공유 혁신 센터를 설치하고 보조 HPC 크레딧을 제공함으로써 발전 디자인의 보급을 더욱 촉진하고 있습니다.

유럽에서는 재료 절약 및 수명 주기 탄소 감축을 평가하는 엄격한 지속가능성 규제와 관련하여 견조한 중간 정도의 단일 자릿수 성장을 보여줍니다. 독일의 자동차 대기업은 공급자에게 AI 주도의 경량화 도입을 추진하고, 스칸디나비아의 건설회사는 목재·모듈 건축에 생성형 툴을 활용하고 있습니다. 일부 부문에서는 거시 경제의 불확실성이 설비 투자를 억제하는 것, 규제 압력에 의해 프로젝트는 계속되고 있습니다. 남미, 중동, 아프리카는 지연을 겪고 있지만, 인프라 지출과 지역제조업 클러스터의 성장에 따라 기세를 늘리고 있습니다. 각 공급업체는 이러한 신흥 시장에서 조기 인지도 획득을 도모하기 위해 지역 파트너십을 구축하고 있습니다.

The Generative Design market is expected to grow from USD 4.30 billion in 2025 to USD 4.91 billion in 2026 and is forecast to reach USD 9.57 billion by 2031 at 14.25% CAGR over 2026-2031.

The expansion is shaped by AI-first design workflows that allow engineers to optimize weight, cost, and performance in a single computational pass, replacing the traditional design-then-iterate routine. Cloud accessibility lowers entry barriers for small manufacturers, while increasingly stringent sustainability mandates encourage material-efficient products that cut lifecycle emissions. Recent consolidation, most notably Siemens' USD 10.6 billion acquisition of Altair, signals that buyers now regard generative design as a core competitive capability rather than a specialized engineering add-on . Competitive intensity rises as established CAD vendors embed AI algorithms and AI-native firms offer cloud-first platforms, resulting in a moderate but tightening market structure.

Regulatory fuel-economy targets and electric-vehicle range expectations leave automakers little choice but to strip mass without sacrificing crash performance. A General Motors program that applied generative algorithms to a seat bracket achieved a 40% weight cut while meeting all safety criteria, illustrating how AI simultaneously balances multi-variable constraints that previously required many manual iterations . Airlines pursue the same logic at fleet scale; Airbus reported a 45% lighter cabin-partition bracket developed through topology optimization, resulting in fuel savings that amplify across thousands of flight hours. North America and Europe feel the greatest urgency because emissions standards tighten each year, translating weight into direct compliance and cost benefits. Suppliers that master rapid AI-led redesign win new platform contracts, accelerating diffusion across the value chain. As lightweight benchmarks rise, traditional design approaches struggle to keep pace, reinforcing demand for AI-generated geometries throughout the decade.

Small manufacturers once excluded by six-figure hardware investments now subscribe to cloud high-performance computing for as little as USD 1,000 per month, gaining the same compute scale Fortune 500 peers enjoy. The subscription model reshapes adoption economics across the Asia Pacific, where many contract manufacturers operate on thin margins yet serve global OEMs. Specialized cloud instances deliver 10X faster solve times for generative solvers than general-purpose servers, shortening iteration cycles from days to hours. Engineering teams shift workloads elastically, paying only for peak computation during design sprints, which makes business cases straightforward even for single-product firms. Providers bundle hardened security frameworks that ease lingering IP concerns, nudging regulated industries toward hybrid models that blend on-premise storage and cloud compute bursts. The outcome is a wider funnel of users entering the generative design market, boosting license growth on both software and services lines.

Annual license bundles for enterprise-grade generative platforms range between USD 50,000 and USD 200,000 per seat, an order of magnitude above mainstream CAD tools and out of reach for many small firms. The expense grows when integration connectors, training sessions, and workflow consulting are factored in. Even when budgets stretch, new users need 6-12 months to become proficient, limiting short-term productivity gains. In emerging economies where engineering salaries are lower, software list prices remain pegged to global rates, making the cost-to-salary ratio especially painful. Vendors respond with consumption-based licensing, but adoption still lags where capital budgets are tight and payback horizons short. Unless pricing models evolve further, a portion of the manufacturing base will postpone entry, muting near-term expansion of the generative design market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The services line of the generative design market recorded the fastest growth trajectory, rising toward a 14.88% CAGR, while software retained a 2025 revenue lead of 57.62%. Consulting teams help manufacturers stitch AI solvers into PLM systems, configure data pipelines, and customize optimization objectives that reflect industry codes. As more firms move beyond proofs of concept, integration complexity and change-management needs rise, propelling service revenues. Top providers bundle workshops, pilot projects, and proprietary training curricula, capturing annuity-like fees that outpace one-off license sales.

Software still anchors the value chain because core algorithms remain proprietary and command premium annual subscriptions in the USD 10,000-USD 50,000 range. Vendors continuously add modules, structural, thermal, fatigue, and carbon calculi, to justify price escalations and defend margins. Ecosystem lock-in from file formats and data analytics dashboards keeps churn low, but customers increasingly negotiate bundled deals that mix software and advisory projects. Successful suppliers differentiate by offering rapid-start templates for verticals such as aerospace seat components or orthopedic implants, shortening time to ROI and protecting their software positions even as service partners bloom.

On-premise installations captured 61.68% of the generative design market share in 2025, reflecting strict IP-protection norms in aerospace and defense. Those sectors prioritize perimeter-controlled data centers and direct GPU clusters to guard proprietary geometries. However, cloud subscribership is expanding at a 14.95% CAGR as SMEs and less-classified projects prize elastic compute over air-gapped control. Early adopters run sensitivity analyses in the cloud while keeping master models in local vaults, a hybrid pattern that balances risk and speed.

Cloud providers sharpen their pitch with purpose-built HPC instances that offer near-linear scaling across thousands of cores, cutting optimization runtimes from eight hours to 40 minutes on complex assemblies. Encryption at rest and zero-trust access frameworks now meet many compliance audits, eroding objections from cautious industries. Subscription licensing further sweetens the deal because costs align with actual compute cycles rather than static capacity. As these economies converge with maturing security standards, the generative design market size linked to cloud consumption is set to widen, though absolute on-premise volumes will persist in highly regulated domains.

The Generative Design Market Report is Segmented by Component (Software, Services), Deployment (On-Premise, Cloud), Technology (Topology Optimization, Fluid and Thermal Optimization, and More), End-User Industry (Automotive, Aerospace and Defense, Architecture and Construction, Industrial Equipment, Consumer Products, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 38.02% of 2025 global revenue as early automotive and aerospace pilots matured into enterprise roll-outs, and software headquarters proximity accelerated co-development cycles with customers. R&D tax incentives and robust venture funding supported new entrants that feed innovation into the wider ecosystem. Growth is steady but slower than in emerging regions because many Fortune 500 manufacturers have already finished first-wave deployments and now focus on scaling rather than new licenses.

Asia Pacific is recording the fastest expansion, charting a 16.21% CAGR through 2031 on the back of China's manufacturing-digitization mandates, Japan's Society 5.0 roadmap, and South Korea's semiconductor competitiveness agenda. Local cloud providers team with software firms to localize interfaces and ensure data residency, which accelerates adoption among domestic SMEs that previously balked at foreign-hosted options. Governments set up shared innovation centers, offering subsidized HPC credits that further stimulate generative design uptake.

Europe shows solid mid-single-digit growth tied to stringent sustainability regulations that reward material savings and lifecycle-carbon cuts. Germany's automotive giants push suppliers to adopt AI-led lightweighting, while Scandinavian builders use generative tools for timber and modular construction. Although macroeconomic uncertainty tempers capital spending in some segments, regulatory pressure keeps projects moving. South America, the Middle East, and Africa trail but build momentum as infrastructure spending and local manufacturing clusters grow; vendors plant regional partnerships to capture early mindshare in these nascent arenas.