아시아태평양의 소형 위성 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Asia-Pacific Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690108

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

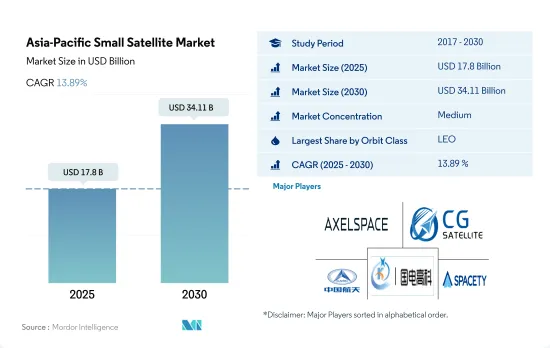

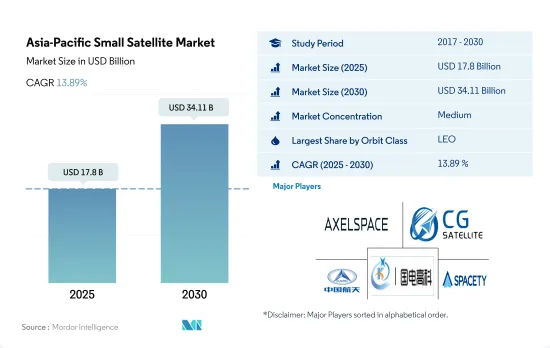

아시아태평양의 소형 위성 시장 규모는 2025년에 178억 달러에 달할 것으로 추정됩니다. 2030년에는 341억 1,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 13.89%로 성장할 전망입니다.

LEO에 발사되는 위성이 시장 수요를 견인

최근 이 지역에서는 소형 위성 수요가 급속히 높아지고 있으며, 비용 효율적이고 다목적 우주선의 장점을 활용하려는 기업과 정부가 늘고 있습니다.

LEO 위성은 아시아태평양에서 발사되는 소형 위성 중 가장 인기 있는 유형 중 하나입니다. 이들은 원격 감지, 지구 관측, 통신 등 다양한 용도로 사용됩니다. 이 지역에서는 2017년부터 2022년에 걸쳐 약 240기의 위성이 LEO로 발사되었으며, 그 중 128기가 지구 관측용, 이어서 67기가 기술 개발용, 24기가 통신용, 12기가 우주 과학용이었습니다.

MEO 위성도 아시아태평양에서 인기를 끌고 있는 소형 위성입니다. 이 위성은 세계 네비게이션, 통신 및 원격 감지 용도에 사용됩니다. MEO 위성은 LEO 위성보다 커버 범위가 넓고 광대역 통신 서비스를 제공할 수 있는 등 몇 가지 장점이 있습니다.

아시아태평양에서 발사되는 또 다른 위성은 GEO 위성입니다. 이 위성은 통신 및 기상 관측에 사용됩니다. GEO 위성의 주요 장점 중 하나는 지구에 대해 일정한 위치에 머물 수 있으므로 TV 방송 및 인터넷 연결과 같은 지속적인 적용 범위가 필요한 용도에 이상적입니다. 2017년부터 2022년까지 감시용으로 1대의 위성이 GEO에 발사되었습니다. 이러한 발전으로 인해 2023년부터 2029년 사이에 이 부문의 성장률이 182% 증가할 것으로 예상됩니다.

아시아태평양의 소형 위성 시장 동향

연료 효율과 운영 효율 향상에 대한 동향이 성장의 주요 원동력이 될 것으로 예상

최근의 위성은 소형화되고 있습니다. 소형 위성은 기존 위성의 몇 분의 비용으로 기존 위성이 수행하는 거의 모든 작업을 수행한다는 사실이 소형 위성 별자리를 구축, 출시 및 운영하는 것을 점점 더 실용화했습니다. 이에 따라 소형 위성에 대한 의존도도 비약적으로 높아지고 있습니다.

소형 위성은 일반적으로 개발 사이클이 짧고 개발 팀도 소규모이며 발사 비용도 훨씬 낮습니다. 혁명적인 기술의 진보는 전자의 소형화를 촉진하고, 스마트 재료의 발명을 뒷받침하고, 위성 버스의 크기와 질량을 제조업체가 시간이 지남에 따라 줄였습니다.

위성의 질량은 위성 발사에 큰 영향을 미칩니다. 이는 위성이 무거울수록 우주로 위성을 발사하는 데 필요한 연료와 에너지가 증가하기 때문입니다. 인공위성을 발사하려면 시속 약 2만 8,000km라는 초고속까지 가속하여 지구 주회 궤도에 투입해야 합니다.

위성이 무거울수록 우주로 발사하려면 더 큰 로켓과 더 많은 연료가 필요하며 발사 비용이 높아지고 사용할 수있는 로켓 유형도 제한됩니다. 마찬가지로 500kg 미만의 위성은 소형 위성으로 간주되었으며,이 지역에서는 약 200 개 이상의 소형 위성이 발사되었습니다. 전반적으로 위성의 질량은 발사에 크게 영향을 미치고 무거운 위성을 발사하려면 더 많은 에너지와 연료가 필요하므로 비용이 상승하고 사용 가능한 발사 옵션이 제한 될 수 있습니다. 아시아태평양에서 운용되고 있는 위성의 수는 상업·군사 우주 분야 수요 증가에 따라 2023-2029년에 급증할 것으로 예측되고 있습니다.

각 우주 기관의 우주 개발비 증가는 아시아태평양의 소형 위성 시장에 긍정적 영향을 미칠 것으로 예상됩니다.

아시아태평양의 소형 위성 시장은 기술 발전, 투자 증가, 소형 위성 서비스 수요 증가로 최근 급속히 성장하고 있습니다. 초소형·초소형 위성은 기존의 위성보다 작고 비용 효율이 높기 때문에 폭넓은 조직이 이용하기 쉽습니다.

중국, 인도, 일본은 완전한 엔드 투 엔드 우주 개발 능력을 가지며, 우주 인프라, 우주 기술 위성 제조, 로켓, 우주항을 완비하고 있습니다. 다른 지역의 국가들은 각각의 우주 계획을 수행하기 위해 국제 협력에 의존하지 않을 수 있지만, 이것은 향후 몇 년 동안 어느 정도 변할 것으로 예상됩니다. 그러나 이 지역의 많은 국가들은 최신의 민첩한 전략의 일환으로 고유한 우주 능력을 개발하고 있습니다. 2022년 6월, 한국은 누리 로켓을 발사하여 6기의 위성을 궤도에 올려 완전 국산 페이로드의 발사에 성공한 세계에서 7번째 국가가 되었습니다.

2022년 일본 예산안에 따르면 일본 우주 예산은 14억 달러 이상이었습니다. 여기에는 H3 로켓 개발, 기술 시험 위성 9호, 정보 수집 위성 계획 등 11개 부처의 우주 활동에 대한 투자가 포함됩니다.

아시아태평양에서 우주 관련 활동이 증가함에 따라 위성 제조업체는 급속히 상승하는 시장의 잠재력을 활용하기 위해 위성 제조 능력을 강화하고 있습니다. 견고한 우주 인프라를 갖춘 아시아태평양의 대표 국가는 중국, 인도, 일본, 한국입니다. 중국국가우주국(CNSA)은 국가민간우주 인프라 강화 등 2021년부터 2025년까지 우주탐사 우선순위를 발표했습니다.

아시아태평양의 소형 위성 산업 개요

아시아태평양의 소형 위성 시장은 적당히 통합되어 상위 5개사에서 61.64%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Axelspace Corporation, Chang Guang Satellite Technology, China Aerospace Science and Technology Corporation(CASC), Guodian Gaoke and Spacety Aerospace Co.(알파벳순 정렬).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

위성의 질량

우주 프로그램에 대한 지출

규제 프레임워크

호주

중국

인도

일본

뉴질랜드

싱가포르

한국

밸류체인과 유통채널 분석

제5장 시장 세분화

용도

통신

지구 관측

네비게이션

우주 관측

기타

궤도 등급

GEO

LEO

MEO

최종 사용자

상업

군사 및 정부

기타

추진 기술

전기

가스

액체 연료

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 프로파일

Axelspace Corporation

Chang Guang Satellite Technology Co. Ltd

China Aerospace Science and Technology Corporation(CASC)

Guodian Gaoke

MinoSpace Technology

Spacety Aerospace Co.

Zhuhai Orbita Control Engineering

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

The Asia-Pacific Small Satellite Market size is estimated at 17.8 billion USD in 2025, and is expected to reach 34.11 billion USD by 2030, growing at a CAGR of 13.89% during the forecast period (2025-2030).

Satellites that are being launched into LEO is driving the market demand

In recent years, demand for small satellites in the region has been rising rapidly, with more and more businesses and governments seeking to leverage the benefits of the cost-effective and versatile spacecraft.

LEO satellites are one of the most popular types of small satellites launched in the Asia-Pacific region. They are used for various applications, including remote sensing, Earth observation, and communication. In the region, during 2017-2022, around 240 satellites were launched into LEO, of which 128 satellites were launched for Earth observation, followed by 67 satellites for technology development, 24 for communication, and 12 for space science.

The MEO satellite is another small satellite gaining popularity in the Asia-Pacific region. These satellites are used for global navigation, communication, and remote sensing applications. MEO satellites offer several advantages over LEO satellites, including broader coverage and the ability to provide high-bandwidth communication services.

The other type of satellites being launched into space in the Asia-Pacific region are GEO satellites. These satellites are used for communication and weather monitoring applications. One of the main advantages of GEO satellites is their ability to remain in a fixed position relative to the Earth, making them ideal for applications requiring continuous coverage, including television broadcasting and internet connectivity. During 2017-2022, one satellite was launched into GEO for surveillance. These advancements are projected to increase this segment's growth rate by 182% during 2023-2029.

Asia-Pacific Small Satellite Market Trends

The trends for better fuel and operational efficiency are expected to be major drivers of growth

Satellites are getting smaller nowadays. The fact that the small-sized satellite does almost everything that a conventional satellite does at a fraction of the cost of the conventional satellite made the building, launching, and operation of the small satellite constellations increasingly viable. Correspondingly, our reliance on them has been growing exponentially.

Small satellites typically have shorter development cycles, smaller development teams, and cost much less for launch. Revolutionary technological advancements facilitated the miniaturization of electronics, which pushed the invention of smart materials, reducing the satellite bus size and mass over time for manufacturers.

The mass of a satellite has a significant impact on the launch of the satellite, and this is because the heavier the satellite, the more fuel and energy are required to launch it into space. Launching a satellite involves accelerating it to a very high speed, typically around 28,000 km per hour, to place it in orbit around the Earth.

A heavier satellite requires a larger rocket and more fuel to launch it into space, which increases the cost of the launch and limits the types of launch vehicles that can be used. Similarly, satellites with less than 500 kg are considered small satellites, and around 200+ small satellites were launched in this region. Overall, the mass of a satellite significantly impacts its launch, requiring more energy and fuel to launch a heavier satellite, which increases the cost and can limit the launch options available. The number of operating satellites in the Asia-Pacific region is projected to surge during 2023-2029 due to growing demand in the commercial and military space sector.

Increasing space expenditures of different space agencies are expected to impact the Asia-Pacific small satellite market positively

The Asia-Pacific small satellite market has grown rapidly in recent years, owing to technological advancements, increased investment, and growing demand for small satellite services. Nano and microsatellites are smaller and more cost-effective than traditional satellites, making them more accessible to a broader range of organizations

China, India, and Japan have complete end-to-end space capacity and complete space infrastructure, space technology satellite manufacturing, rockets, and spaceports. Other regions' countries must rely on international cooperation to carry out their respective space programs, which is expected to change to some extent in the coming years. However, many countries in the region are developing indigenous space capabilities as part of their latest agile strategies. In June 2022, South Korea launched the Nuri rocket, putting six satellites into orbit, making it the seventh country in the world to successfully launch a wholly indigenous payload.

In 2022, according to the draft budget of Japan, the space budget of the country was over USD 1.4 billion. It included investment in space activities of 11 government ministries, such as the development of the H3 rocket, Engineering Test Satellite-9, and the country's Information Gathering Satellite program.

Considering the increase in space-related activities in the Asia-Pacific region, satellite manufacturers are enhancing their satellite production capabilities to tap into the rapidly emerging market potentials. The prominent Asia-Pacific countries that possess robust space infrastructure are China, India, Japan, and South Korea. China National Space Administration (CNSA) announced space exploration priorities during 2021-2025, including enhancing national civil space infrastructure.

Asia-Pacific Small Satellite Industry Overview

The Asia-Pacific Small Satellite Market is moderately consolidated, with the top five companies occupying 61.64%. The major players in this market are Axelspace Corporation, Chang Guang Satellite Technology Co. Ltd, China Aerospace Science and Technology Corporation (CASC), Guodian Gaoke and Spacety Aerospace Co. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Satellite Mass

4.2 Spending On Space Programs

4.3 Regulatory Framework

4.3.1 Australia

4.3.2 China

4.3.3 India

4.3.4 Japan

4.3.5 New Zealand

4.3.6 Singapore

4.3.7 South Korea

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application

5.1.1 Communication

5.1.2 Earth Observation

5.1.3 Navigation

5.1.4 Space Observation

5.1.5 Others

5.2 Orbit Class

5.2.1 GEO

5.2.2 LEO

5.2.3 MEO

5.3 End User

5.3.1 Commercial

5.3.2 Military & Government

5.3.3 Other

5.4 Propulsion Tech

5.4.1 Electric

5.4.2 Gas based

5.4.3 Liquid Fuel

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 Axelspace Corporation

6.4.2 Chang Guang Satellite Technology Co. Ltd

6.4.3 China Aerospace Science and Technology Corporation (CASC)