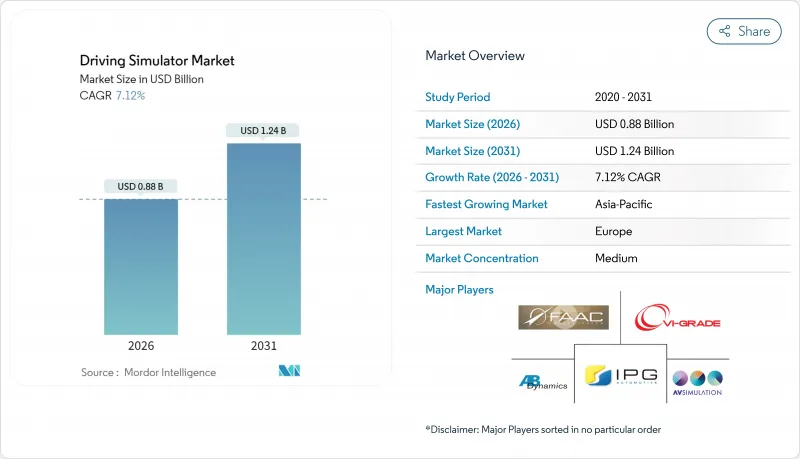

운전 시뮬레이터 시장은 2025년에 8억 2,000만 달러로 평가되었으며, 2026년 8억 8,000만 달러에서 2031년까지 12억 4,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2026-2031년)의 CAGR은 7.12%를 나타낼 것으로 전망됩니다.

이 꾸준한 성장은 보다 안전한 운전자 인증을 요구하는 규제 압력, 프로토타입 시험 비용 절감의 필요성, 자율주행 차량 로드맵 및 가상 검증 의무의 무결성으로 인해 발생합니다. 상용 차량은 채용 사이클 단축을 위해 고도의 시뮬레이터를 채용하고, 자동차 제조업체는 실제 주행 시험을 보완하는 소프트웨어 인 더 루프 시험 장치에 연구 예산을 돌리고 있습니다. 구독형 클라우드 플랫폼은 비용 중심 지역에서의 액세스를 확대하고 새로운 사용자층을 육성하고 있습니다. 유럽은 성숙한 자동차 생태계를 통해 주도권을 유지하고 있지만, 중국과 인도의 물류 네트워크가 확대됨에 따라 아시아태평양이 가장 큰 수익을 얻고 있습니다. 경쟁 우위는 현재 디지털 트윈 맵, 무선 소프트웨어 검증, 하드웨어 독립적인 모션 큐잉을 융합하는 공급자로 흐르고 있습니다. 그러나, 고액의 초기 투자, 모션 세크니스 리스크, 높아지는 사이버 보안 경보가, 소규모 도입자의 발판이 되고 있습니다.

보다 엄격한 인증 규칙은 자율주행 기능이 공도에 도입되기 전에 수십억 마일에 이르는 가상 테스트 주행이 필수가 되었습니다. 2024년에 발표된 Euro NCAP 및 NHTSA 프로토콜은 실제 주행 테스트와 시뮬레이션을 결합하여 고정밀 테스트 장비를 적합성 장벽으로 자리매김했습니다. IEEE는 2030년까지 10억 달러 규모의 자율주행 시뮬레이션 시장을 예측하고 있으며, 자동차 제조업체가 공도에서는 검증 불가능한 엣지 케이스를 조사하기 위해 디지털 트윈에 의존하고 있는 실태를 부각하고 있습니다. 실제 세계의 센서 로그와 확장 가능한 시나리오 엔진을 통합한 플랫폼을 통해 엔지니어는 반복 사이클을 줄이고 프로토타입 차량을 줄일 수 있습니다. 소프트웨어 업데이트가 라디오를 통해 진행됨에 따라 가상 회귀 테스트가 필수적이며 운전 시뮬레이터 시장에 대한 안정적인 수요를 지원합니다. 시나리오 라이브러리, 물리 엔진 및 데이터 융합 인터페이스를 단일 스택에 통합하는 공급업체는 현재 Tier 1 공급업체로부터 견적 요청(RFQ)을 더 많이 획득하고 있습니다.

온라인 소매의 확대에 의해 소포 취급량이 증가하고, 화물 수송 능력이 핍박하고 있습니다. UPS와 프레몬트 계약 경력과 같은 운송 회사는 교실에 모션 기반 시뮬레이터를 도입하여 사고 감축과 신인 운전자의 조기 전력화를 보고합니다. 네브래스카 주 트럭 협회가 제공하는 이동식 훈련 유닛은 원격지의 대학에 훈련을 제공하여 지역 인력 부족을 완화합니다. 재현 가능한 위험 시나리오를 통해 운송 회사는 보험 감사에 대응할 수 있으며, 몇 주 동안 신인의 자격 증명이 완료되므로 도입이 촉진되고 있습니다. 이 상업 분야 수요는 소비자를 위한 운전 교육 프로그램의 성장 문제를 상쇄하고 단기적으로는 운전 시뮬레이터 시장의 성장률을 10%대 전반에 유지하고 있습니다.

8축 모션 베이스, 파노라믹 돔, 전용 홀은 많은 직업 훈련 센터의 도입 비용이 너무 비쌉니다. 유럽의 슈투트가르트 운전 시뮬레이터는 이러한 설비가 요구하는 부동산과 유지 관리의 부담을 여실히 보여줍니다. 자금 조달 장벽은 특히 수업료가 규제되는 지역에서 투자 회수 기간을 장기화합니다. 신흥 시장의 구매자들은 구매를 연기하거나 정적 조종석으로 타협하는 경우가 많으며, 운전 시뮬레이터 시장에서 고가격대 하드웨어의 판매 수량 성장을 억제하고 있습니다.

승용차 시뮬레이터는 2025년에 있어서도 운전 시뮬레이터 시장 점유율의 59.88%를 차지해 초보자 드라이버 교육과 OEM 연구 개발의 두 분야에서 주도적 지위를 유지했습니다. 그러나 소비자 면허 시험 기관의 시뮬레이터 대체 제한으로 인해 성장은 둔화 경향이 있습니다. 도입 동향의 분기는 물류의 디지털화가 시뮬레이터 수요 패턴을 재구성하는 실태를 보여줍니다. 상용차는 2025년 시점에서 수익 기반은 소규모였지만, 7.14%의 연평균 복합 성장률(CAGR)에 의해 운전 시뮬레이터 시장 전망적인 확대를 견인하는 주요 엔진이 됩니다. 함대 관리자는 운전자 1인당 훈련 비용 절감, 차량 가동률 유지, 엄격화하는 운전 시간 규제 감사에 대응을 목적으로 시뮬레이터를 도입. 텔레매틱스 통합은 차내 행동과 교실에서의 복습 훈련을 더욱 연계시킵니다.

상용차에 대한 수요 증가는 위험물 운송 경로를 위한 시나리오 라이브러리 사용자 정의, 다국어 UI 오버레이, 원격지도 스테이션 등 주변 서비스를 촉진합니다. 모듈형 조종석과 클라우드 렌더링을 활용하는 공급업체는 기존에는 가격면에서 진입이 어려웠던 중소규모 운송업체에 진출하고 있습니다. 한편, 승용차용 프로그램은 차세대 인포테인먼트용 휴먼 머신 인터페이스 시험에 주력하고 있으며, 이 틈새 시장은 이익률이 높은 것으로 시장 규모는 한정적입니다. 듀얼 퍼퍼스 아키텍처, 교체 가능한 대시보드 및 적응형 소프트웨어 스택을 개발하는 공급업체는 운전 시뮬레이터 시장에서 부문 횡단적인 유연성을 유지합니다.

2025년 시점에서 운전 훈련 분야는 확립된 교습 커리큘럼과 기업의 컴플라이언스 수요에 의해 운전 시뮬레이터 시장 규모의 50.72%를 차지했습니다. 그러나 시험·조사 분야가 기록한 7.21%의 연평균 복합 성장률(CAGR)은 구조적인 전환을 시사하고 있습니다. 릴리즈 사이클 단축을 목표로 하는 자동차 제조업체는 예산을 소프트웨어 주도의 검증 프로세스에 돌려주고 있어 가상 주행 거리는 실 주행 거리보다 비용 효율이 우수합니다. 규제기관에 의한 충돌 회피 검증을, 제어된 재현성이 있는 환경에서 실시하는 실험실 수요도 성장 요인입니다.

훈련 수요는 견조하게 추이하고 있어 특히 도로 정체나 연료 가격의 상승에 의해 실지 훈련의 효율성이 저하하고 있는 지역에서 현저합니다. 가상현실 헤드셋과 적응형 AI 튜터에 의한 모듈의 개별화가 학습자의 정착율 향상에 기여하고 있습니다. 다만, 예산에 민감한 교육기관에서는 기존 차량의 전 차량 갱신에 대해서 모습의 자세를 계속하고 있습니다. 프로바이더는 테스트 자동화 스크립트와 교실용 컨텐츠를 전환 가능한 혼합 이용 라이선스를 제공하는 것으로 리스크를 분산. 이에 따라 좌석 가동률의 향상과 운전 시뮬레이터 시장에서의 수익의 다양화를 도모하고 있습니다.

유럽은 2025년 밀집한 테스트코스망, 통일된 안전기준, 연구개발세제 우대책을 배경으로 운전 시뮬레이터 시장에서 36.22%의 점유율을 유지했습니다. 독일, 프랑스 및 스웨덴의 자동차 제조업체는 규제 신청 서류 작성에 활용되는 통합 시뮬레이션 파이프라인을 운영하여 하드웨어 업데이트 사이클을 안정화시키고 있습니다. 각국의 운수성은 시뮬레이터를 활용한 라이선싱 제도의 시험 운용을 진행하고 있으며, 민간 예산이 변동하는 가운데도 공공 조달 프로그램이 계속되고 있습니다.

아시아태평양은 7.17%의 연평균 복합 성장률(CAGR)을 나타내 신규 좌석 수를 가장 많이 추가하고 있습니다. 중국은 스마트 시티 예산을 자율주행 셔틀의 조종사 사업에 투입하고 인도는 만성 노동력 부족을 해소하기 위해 트럭 운전사 양성 아카데미를 확대하고 있습니다. 클라우드 렌더링 솔루션은 인프라 병목 현상을 피하고 교육 기관이 노트북 제어 조종석을 임시 교실에 도입할 수 있도록 합니다. 일본의 확립된 자동차 산업은 복잡한 도시 교차로를 재현하는 시나리오 라이브러리에 주력하여 운전 시뮬레이터 시장에서 업스트림 소프트웨어 수요를 강화하고 있습니다.

북미에서는 상용 운전자 자격을 규정하는 연방 가이드라인의 정비와 항공·방위 분야에서의 시뮬레이터 도입의 조기 문화가 이점이 되고 있습니다. 대형화물 운송업체는 지역 허브간을 네트워크화한 차량군에 투자해 집중형 컨텐츠 전달을 활용하고 있습니다. 라틴아메리카와 중동은 여전히 소규모 소비 지역이지만 걸프 지역의 석유 및 가스 수송 콤보 사업자의 관심이 높아지고 있으며 향후 지리적 확대를 시사하고 있습니다.

The Driving Simulator Market was valued at USD 0.82 billion in 2025 and estimated to grow from USD 0.88 billion in 2026 to reach USD 1.24 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

This steady rise stems from regulatory pressure for safer driver certification, the need to cut prototype testing costs, and the alignment of autonomous-vehicle roadmaps with virtual validation mandates. Commercial fleets turn to advanced simulators to shorten recruitment cycles, while carmakers channel research budgets toward software-in-the-loop test beds that complement physical tracks. Subscription-based, cloud-hosted platforms broaden access in cost-sensitive regions and nurture new user segments. Europe keeps its lead on account of a mature automotive ecosystem, but Asia-Pacific contributes the largest incremental revenue as China and India expand logistics networks. Competitive advantage now flows to providers that fuse digital-twin maps, over-the-air software verification, and hardware-agnostic motion cueing, although high capital outlays, motion-sickness risks, and rising cyber-security alerts hold back smaller adopters.

Tougher homologation rules now insist on billions of virtual test miles before autonomous functions reach public roads. Euro NCAP and NHTSA protocols released in 2024 pair track runs with simulation, turning high-fidelity rigs into compliance gates. The IEEE forecasts over a billion dollar autonomous-driving simulation niche by 2030, underscoring how carmakers rely on digital twins to probe edge cases unreachable on open roads. Platforms integrating real-world sensor logs with scalable scenario engines let engineers shorten iteration loops and trim prototype fleets. As software updates move over the air, virtual regression testing becomes mandatory, anchoring steady demand for the driving simulator market. Vendors that wrap scenario libraries, physics engines, and data-fusion interfaces into one stack now win more RFQs from tier-1 suppliers.

Online retail pushes parcel volumes upward, straining freight capacity. Carriers such as UPS and Fremont Contract Carriers equip classrooms with motion-based simulators and report accident reductions alongside faster rookie onboarding. The Nebraska Trucking Association's mobile units bring training to remote colleges, easing the rural talent gap. Repeatable hazard scenarios help fleets meet insurance audits and qualify recruits within weeks, boosting uptake. This commercial pull offsets slower growth in consumer driver-ed programs and keeps the driving simulator market momentum above one-tenth in the short term.

Eight-axis motion bases, panoramic domes, and purpose-built halls push acquisition costs beyond the reach of many vocational centers. Europe's Stuttgart Driving Simulator illustrates the real-estate and maintenance footprint such rigs require. Financing hurdles prolong payback periods, especially where tuition fees are regulated. Emerging-market buyers often defer purchases or settle for static cockpits, tempering volume growth for premium hardware in the driving simulator market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Passenger-car simulators still dominate with 59.88% of the driving simulator market share in 2025, serving both novice driver education and OEM R&D, but growth moderates as consumer licensing boards limit simulator substitution. The divergence in uptake illustrates how logistics digitization reshapes simulator demand patterns. Commercial vehicles accounted for a smaller revenue base in 2025, yet their 7.14% CAGR makes them the primary engine of future expansion for the driving simulator market. Fleet managers deploy simulators to cut per-driver training costs, keep rigs on the road, and satisfy stricter hours-of-service audits. Telematics integration further links in-cab behavior with classroom refreshers.

The commercial-vehicle push stimulates peripheral services scenario library customization for hazmat routes, multi-language UI overlays, and remote instructor stations. Vendors leveraging modular cockpits and cloud rendering penetrate small and mid-sized transport operators previously priced out. Meanwhile, passenger-car programs focus on human-machine interface testing for next-gen infotainment, a niche that commands higher margins but fewer seats. Suppliers that craft dual-purpose architectures, swappable dashboards, and adaptable software stacks retain cross-segment flexibility in the driving simulator market.

Training held 50.72% of the driving simulator market size in 2025 due to entrenched driver-ed curricula and corporate compliance needs. Yet the 7.21% CAGR logged by testing and research signals a structural pivot. Automakers wanting to shorten release cycles channel budgets toward software-dominated validation, where virtual miles are cheaper than track miles. Growth also comes from regulatory labs conducting crash-avoidance verification under controlled, repeatable conditions.

Training demand remains resilient, particularly in regions where road congestion and fuel prices make real-world lessons inefficient. Virtual-reality headsets and adaptive AI tutors personalize modules, boosting learner retention. Still, budget-sensitive schools adopt a wait-and-see stance on replacing entire fleets of conventional cars. Providers hedge by offering mixed-use licenses that toggle between test automation scripts and classroom content, increasing seat utilization and diversifying revenue in the driving simulator market.

The Driving Simulator Market Report is Segmented by Vehicle Type (Passenger Car and Commercial Vehicle), Application (Training and Testing & Research), Simulator Type (Compact Simulator and More), End-User (Driving Schools & Training Centers and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Europe preserved a 36.22% share of the driving simulator market in 2025 on the strength of its dense testing circuits, harmonized safety rules, and R&D tax incentives. Carmakers in Germany, France, and Sweden run integrated simulation pipelines that feed regulatory dossiers, ensuring a steady hardware refresh cycle. National transport ministries pilot simulator-based licensing updates, keeping public procurement programs alive even as private budgets fluctuate.

Asia-Pacific, advancing at a 7.17% CAGR, adds the most new seats. China funnels smart-city budgets into autonomous shuttle pilots, while India scales truck-driver academies to plug chronic labor gaps. Cloud-rendered solutions bypass infrastructure bottlenecks, letting institutes deploy laptop-controlled cockpits in temporary classrooms. Japan's well-established automotive sector focuses on scenario libraries that represent complex urban intersections, reinforcing upstream software demand in the driving simulator market.

North America benefits from structured federal guidelines covering commercial-driver qualifications and an early culture of simulator adoption in aviation and defense. Large freight haulers invest in networked fleets of rigs across regional hubs, leveraging centralized content pushes. Latin America and the Middle East remain smaller consumers, yet oil-and-gas convoy operators in the Gulf show rising interest, signaling wider geographic penetration ahead.