ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

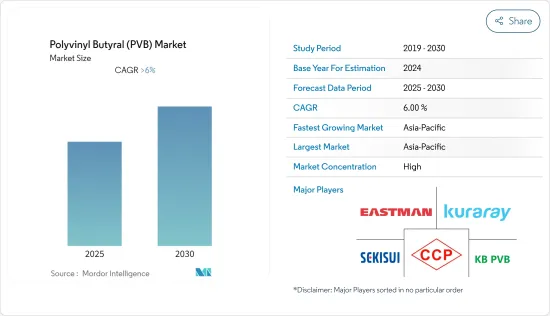

폴리비닐부티랄(PVB) 시장은 예측 기간 동안 CAGR 6% 이상을 기록할 전망입니다.

시장은 COVID-19에 의해 부정적인 영향을 받았습니다. 팬데믹(세계적 유행) 상황을 바탕으로 감염 확대를 막기 위해 자동차 제조 공장이 일시적으로 가동 중지되어 안전하고 내충격성이 뛰어난 자동차용 앞유리의 제조에 사용되는 PVB 재료 수요가 제한되었습니다. 그러나 2021년 이후 업계는 활기를 되찾고 있으며, 예측 기간 동안에도 시장은 비슷한 궤도를 따라갈 것으로 보입니다.

주요 하이라이트

단기적으로는 적층 유리 용도 증가와 세계 건설 및 인프라 활동의 활성화가 시장 성장을 뒷받침할 것으로 보입니다.

반면, 시장에는 대체품이 존재하기 때문에 시장 성장을 방해할 것으로 예상됩니다. 또한, 신흥 경제 국가에서 폴리비닐부티랄의 재활용량이 많으면 환경 문제를 일으키기 때문에 시장에 타격을 줄 수 있습니다.

앞으로 몇 년동안 태양광 발전 산업에서 수요가 증가하고 전기자동차를 구매하는 사람이 증가함에 따라 시장이 성장할 것으로 보입니다.

예측 기간 동안 아시아태평양이 선도하고 CAGR이 가장 높을 것으로 예상됩니다.

폴리비닐부티랄(PVB) 시장 동향

시장을 독점하는 자동차 부문

폴리비닐부티랄은 기계적 특성이 우수한 폴리머로, 합판 유리의 중간막 재료로서 일반적으로 사용되고 있습니다. PVB 시트는 유리의 두 층에 접착하고 충격이 가해도 손상되지 않습니다. PVB 시트와 유리의 결합은 화학적이기 때문에 쉽게 벗겨지지 않습니다.

PVB는 주로 자동차 윈드스크린용 맞춤 안전유리에 사용됩니다. 자동차의 앞유리에 안전성과 안심감을 가져오기 때문에 샌드위치 맞추는 유리의 중간막으로서의 PVB 수요는 급증하고 있습니다. 또한, 차음성과 UV 컷도 PVB의 중요한 장점이며 자동차 산업에서 PVB의 이용을 높이고 있습니다.

OICA(Organization Internationale des Constructeurs d'Automobiles)는 2021년에는 세계 8,000만 대의 자동차가 제조된 것으로 평가했으며, 이는 2020년의 7,800만 대보다 약 3% 많습니다.

유명한 자동차 회사인 도요타는 2022년 11월 자동차 판매 및 생산 대수를 전년 대비 약 4% 증가시켰습니다. 도요타의 2022년 1월부터 11월까지 총 자동차 판매 대수는 약 950만 대, 생산 대수는 약 970만 대였습니다. 판매량은 전년과 크게 다르지 않지만 생산량은 전년 대비 약 7% 증가했습니다.

유럽 자동차 공업회는 최신 보고서에서 총 194개의 자동차 제조 공장이 미국 내에서 운영하고 있다고 말합니다. 또한 2021년에는 총 약 1,200만 대의 자동차가 유럽에서 생산되었습니다.

ACEA는 또한 2022년 12월 승용차 등록 대수가 2021년 12월에 비해 전월 대비 약 13% 증가한 것을 확인했습니다. 등록 대수 증가율이 가장 높았던 것은 독일(38%), 이어 이탈리아(21.0%)였습니다. 승용차 등록이 증가함에 따라 업계에서는 생산 수요도 증가했으며 PVB 시장에 큰 영향을 미쳤습니다.

이상과 같은 요인으로부터 폴리비닐부티랄 시장은 앞으로도 호조를 유지할 전망입니다.

시장을 독점하는 아시아태평양

아시아태평양 지역이 세계 최대 시장이 될 것으로 예상되는 이유는 중국, 인도, 일본, 싱가포르가 더 많은 건물을 건설하고 더 많은 자동차를 판매 및 제조하고 있기 때문이며, 이 지역에서는 태양에너지 생산을 돕기 위한 투자가 이루어지고 있기 때문입니다.

중국 자동차공업협회에 따르면 중국에서도 2022년 자동차 생산 대수가 전년 대비 약 2.1% 증가했습니다. 미국에서는 2014년에 약 2,686만 대의 자동차가 판매되었습니다. 중국에서도 2022년 자동차 생산 대수가 전년 대비 약 2.1% 증가합니다. 2021년 자동차 판매 대수가 2,627만 대였던 반면, 2022년에는 약 2,686만 대가 판매되었습니다.

인도 브랜드 에퀴티 재단에 따르면 인도 자동차 산업은 2026년까지 약 3,000억 달러에 달할 것으로 예상됩니다. 또한 2022년도 국내 승용차 판매량은 약 300만 대에 달했습니다.

2000년 4월부터 2022년 6월까지 자동차 산업은 누계 약 335억 3,000만 달러의 주식을 직접 투자를 받았습니다. 인도 정부는 2023년까지 80억-100억 달러가 인도나 기타 국가에서 자동차 사업에 투자된다고 생각했습니다.

일본의 건설 업계도 일본에서 개최될 예정의 행사에 의해 꽃이 열릴 것으로 기대되고 있습니다. 예를 들어, 오사카에서는 2025년에 만국박람회가 개최됩니다. 건설은 주로 재개발과 자연재해로부터의 부흥에 의해 추진됩니다. 도쿄역의 2개의 고층 타워, 당초 2021년 완성 예정인 지상 37층, 높이 230m의 오피스 타워와 2027년 완성 예정의 지상 61층, 높이 390m의 오피스 타워가 있습니다.

일본의 국토교통성에 따르면 2022년 건설 부문 총 투자액은 전년대비 0.6% 증가한 66조 9,900억 엔(5,081억 6,000만 달러) 정도가 된 것으로 평가되었습니다.

폴리비닐부티랄(PVB)은 자동차 산업, 건설 산업 및 기타 산업에 대한 투자가 증가함에 따라 이러한 산업에 기여하기 때문에 수요가 증가하게 됩니다. 이것은 향후 몇 년동안 시장에 좋은 일이라고 생각됩니다.

폴리비닐부티랄(PVB) 산업 개요

폴리비닐부티랄(PVB) 시장은 부분적으로 통합되어 소수의 대기업이 시장의 상당 부분을 차지하고 있습니다. 이 시장의 주요 기업은 아래와 같습니다(순부동). : Eastman Chemical Company, Kuraray, Sekisui Chemical, Kingboard(Fogang) Specialty Resins(KB PVB), Chang Chun Group 등입니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

세계 건설 및 인프라 활동 확대

적응 유리의 용도 확대

성장 억제요인

시장에서 대체 제품의 존재

신흥 경제 국가에서 폴리비닐부티랄의 높은 재활용률

밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형별

점착 필름

페인트 및 코팅(워시 프라이머 포함)

인쇄 잉크 및 래커

기타 유형(세라믹용 바인더, 복합 섬유용 바인더)

최종 사용자 산업별

자동차

건설

발전

기타 최종 사용자 산업(항공우주 및 방위)

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Chang Chun Group

Everlam

Genau Manufacturing Company LLP

Huakai plastic(Chongqing) Co., Ltd.

Kingboard FoGang Specialty Resins Co. Ltd

KURARAY CO. LTD

Eastman Chemical Company

Sekisui Chemical Co. Ltd.

WMC GLASS

제7장 시장 기회 및 향후 동향

태양광 발전 산업에서 수요 증가

EV의 보급 확대

AJY

영문 목차

영문목차

The Polyvinyl Butyral Market is expected to register a CAGR of greater than 6% during the forecast period.

The market was negatively impacted by COVID-19. Given the pandemic situation, car manufacturing plants were temporarily halted to prevent the spread, limiting demand for PVB materials used to manufacture safe, impact-resistant automotive windscreens. However, the industry has picked up speed since 2021, and the market is expected to follow a similar trajectory throughout the projection period as well.

Key Highlights

Over the short term, the growing number of laminated glass applications and the ever-increasing construction and infrastructure activities across the world are likely to boost market growth.

On the flip side, the availability of product substitutes in the market is expected to hinder the market's growth. The high amount of polyvinyl butyral recycling in developed economies could also hurt the market because it would cause environmental problems.

In the coming years, the market is likely to grow thanks to growing demand from the photovoltaic industry and more people buying electric cars.

During the period of the forecast, the Asia-Pacific region is expected to lead and have the highest CAGR.

Polyvinyl Butyral (PVB) Market Trends

The Automotive Segment to Dominate the Market

Polyvinyl butyral is a polymer with good mechanical properties that are commonly used as an interlayer material in laminated glass. The PVB sheet adheres to both layers of glass, keeping them unbroken even after impact. Because the bond between the PVB sheet and the glass is chemical, it does not delaminate easily.

PVB is mostly found in laminated safety glass for car windshields. Because of the safety and security it provides in automotive windscreens, the demand for PVB as an interlayer in sandwich laminated glass has skyrocketed. Furthermore, acoustic insulation and UV protection are important advantages of PVB that increase its use in the automotive industry.

The Organization Internationale des Constructeurs d'Automobiles (OICA) predicts that 80 million vehicles will be made around the world in 2021, which is about 3% more than the 78 million vehicles that will be made in 2020.

Toyota, a renowned automobile company, increased vehicle sales and manufacturing by around 4% in November 2022 compared to the previous year. Toyota's total vehicle sales and production from January to November 2022 were around 9.5 million and 9.7 million, respectively. Even though sales didn't change much from the year before, production did go up by about 7% compared to the year before.

The European Automobile Manufacturers' Association stated in its latest report that a total of 194 automobile manufacturing units operate on European Union soil. Also, a total of about 12 million vehicles will be made in Europe in 2021.

The ACEA also saw an increase in passenger automobile registrations in December 2022, which grew by roughly 13% month over month compared to December 2021. Germany gained the highest percentage of registrations (+38%), followed by Italy (+21.0%). With the increased registration of passenger vehicles, demand for production is also increasing in the industry, significantly impacting the PVB market.

So, the above factors are likely to keep the polyvinyl butyral market going in the years to come.

The Asia-Pacific Region to Dominate the Market

Asia-Pacific is expected to be the biggest market in the world because China, India, Japan, and Singapore are building more buildings and selling and making more cars, and because investments are being made in the region to help solar energy production.

According to the China Association of Automobile Manufacturers, China has also seen an increase in automotive production in the country of around 2.1% in the year 2022, compared to the previous year. About 26.86 million units of automobiles were sold in the United States in 2014. China has also seen an increase in automotive production in the country of around 2.1% in the year 2022, compared to the previous year. About 26.86 million units of automobiles were sold in 2022, as compared to 26.27 million units sold in 2021.

According to the Indian Brand Equity Foundation, the Indian automotive industry is expected to reach around USD 300 billion by 2026. Moreover, in FY 2022, passenger vehicle sales in the country reached about 3 million.

Between April 2000 and June 2022, the automobile industry received approximately USD 33.53 billion in cumulative equity FDI inflows. The Indian government thought that between USD 8 billion and USD 10 billion more would be invested in the car business from India and other countries by 2023.

The Japanese construction industry is also expected to bloom due to the events expected to be hosted in the country. For instance, Osaka will host the World Expo in 2025. The construction is mostly driven by redevelopment and recovery from natural disasters. Two high-rise towers for Tokyo Stations, a 37-story, 230-meter-tall office tower initially planned to be completed in 2021, and a 61-story, 390-meter-tall office tower, are due for completion in 2027.

According to Japan's Ministry of Land, Infrastructure, Transport, and Tourism (MLIT), total investment in the construction sector in 2022 is expected to be around 66,990 billion yen (USD 508.16 billion), which is a 0.6% increase over the previous year.

Growing investments in the auto, construction, and other industries would lead to a rise in demand for polyvinyl butyral (PVB) because it serves those industries. This would be good for the market over the next few years.

Polyvinyl Butyral (PVB) Industry Overview

The polyvinyl butyral (PVB) market is partially consolidated, with a few major players dominating a significant portion of the market. Some of the key players in the market include (in no particular order): Eastman Chemical Company, Kuraray Co. Ltd., Sekisui Chemical Co. Ltd., Kingboard (Fogang) Specialty Resins Co. Ltd. (KB PVB), and Chang Chun Group.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Construction and Infrastructure Activities Across the World

4.1.2 Growing Applications for Laminated Glass

4.2 Restraints

4.2.1 Availability of Product Substitutes in the Market

4.2.2 High Recycling Activities of Polyvinyl Butyral in Developed Economies

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitutes

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Adhesive Films

5.1.2 Paints and Coatings (including Wash Primers)

5.1.3 Printing Inks and Lacquers

5.1.4 Other Types (Binders for Ceramics and Composite Fibers)

5.2 End-user Industry

5.2.1 Automotive

5.2.2 Construction

5.2.3 Power Generation

5.2.4 Other End-user Industries (Aerospace, Defense)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements