P2G(Power to Gas) 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

Power to Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1689841

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

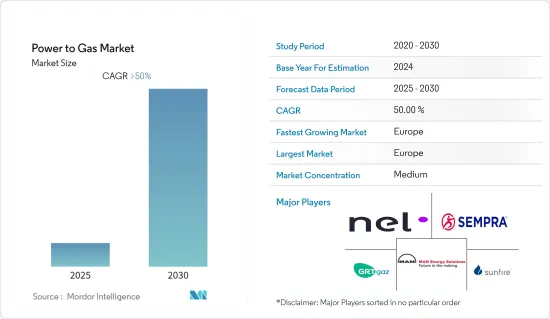

세계의 P2G(Power to Gas) 시장은 예측 기간 중 50% 이상의 CAGR로 추이할 전망입니다.

COVID-19는 2020년 시장에 부정적인 영향을 미쳤습니다.

주요 하이라이트

장기적으로는 온실가스가 기후에 미치는 영향을 저감하기 위한 탈탄소화의 진전과 재생가능 에너지원의 등장에 의한 전력비용의 저감이 시장을 견인하는 주요 요인이었습니다.

반면 P2G(Power to Gas) 플랜트를 설치하기 위한 높은 초기 비용이나 메탄이나 수소를 위해 미개발 경제 국가나 선진 경제 국가에서 추가적인 수송 파이프라인 인프라를 필요로 하는 것이 시장의 성장을 둔화시킬 것으로 예상됩니다.

시장에 있어서의 그린수소의 인프라 개척의 이니셔티브의 고조는 P2G 시장의 참가 기업에 있어서 중요한 기회를 곧 창출할 것으로 예상됩니다.

유럽은 독일, 프랑스, 스페인과 같은 국가들 수요가 대부분을 차지하고 P2G 시장을 독점할 것으로 예상됩니다.

가스발전시장 동향

Power to Hydrogen 부문이 급성장

Power to Hydrogen 부문에는 전기를 이용하여 전기분해를 하고 물을 수소와 산소로 분해하는 다양한 기술이 포함되어 있습니다. 에 의해 풍력이나 태양광 등의 재생 가능 에너지의 변동 억제를 최소화해, 전해조에 의한 장기 저장과 그리드 밸런싱 서비스를 제공해, 기존의 가스 송전 인프라를 이용해 그린 수소의 형태로 에너지를 장거리 수송할 수 있습니다.

게다가 총 용량 5,400만 kW의 350개 가까운 프로젝트가 현재 개발 중이며, 2030년까지 가동할 예정입니다.

전해조에서 제조된 그린 수소는 경자동차, 철도, 해양 용도로 석유를 대신하는 수송용 연료로서, 혹은 공업 용도의 원료로서 직접 사용할 수도 있습니다.

이 기술에는 축전 용량이 크고 방전 시간이 길다는 현재 에너지 저장 기술에는 없는 이점이 있습니다. 수소는 천연 가스 계통에 직접 주입할 수 있습니다.

태양광 발전 및 풍력 발전과 같은 신재생에너지 기술의 비용이 낮아 P2G(Power to Gas) 기술과 같은 에너지 저장 기술은 점점 매력적이 되고 있습니다. 업무용 전해조 시스템의 설치 용량은 최근 몇 년 동안 꾸준히 증가하고 있습니다.

따라서, 상기 요인으로부터 예측 기간 동안 Power to Hydrogen 부문이 가장 급성장할 것으로 예상됩니다.

유럽이 시장을 독점

2021년 현재 유럽은 P2G 시장의 최대 지역 중 하나입니다.

유럽위원회에 의하면, 2021년에는 정유소 섹터가 수소 소비량의 48%를 차지하고, 이어서 비료, 화학 섹터가 계속됩니다.

독일은 유럽의 P2G 시장의 주요국 중 하나입니다. 2020년 현재 독일에는 주로 풍력발전과 태양광 발전 프로젝트에 의한 잉여 그린 전력을 이용하여 물을 산소와 수소로 분해하는 전기분해를 실시하고, 제로 카본 연료를 생산하는 약 40개의 소규모 발전 가스 파일럿 프로젝트가 있습니다.

Deutscher Verein des Gas-und Wasserfaches(DVGW)에 따르면 독일은 가정, 공장, 자동차용 제로 카본 연료의 개발을 목표로 하고 있으며, 2023년까지 5GW, 2050년까지 40GW의 발전 능력을 건설할 계획입니다. 따라서 이러한 정부 목표는 예측 기간 중 지역의 P2G 시장을 끌어올릴 가능성이 높습니다.

2022년 1월 ThyssenKrupp Uhde Chlorine Engineers는 네덜란드 로테르담 항구에서 대규모 프로젝트 'Hydrogen Holland I'공급 계약을 Shell과 체결했습니다. 이 계약에 따라 ThyssenKrupp Uhde는 20MW의 대형 알칼리수 전해 모듈을 기반으로 200MW의 전해 플랜트의 설계, 조달, 제작을 실시했습니다.

러시아와 우크라이나의 전쟁이 시작된 후, EU는 2022년 5월에 통과된 일부로서 재생가능 에너지 발전을 증가시킴으로써 러시아의 가스 수입에 대한 과도한 의존을 줄이는 것을 목표로 하고 있습니다. 2030년까지 1,000만 톤의 재생가능 수소를 생산하여 1,000만 톤을 EU에 수입하는 것을 목표로 하고 있습니다.

마찬가지로 EU는 2022년 5월, 유럽의 전해조 제조업체와 목표를 설정해, 2025년까지 유럽의 전해조 제조 능력을 175만 kW/년으로부터 1,750만 kW/년에 10배 가까이 증가시킨다고 하는 산업 전체의 목표를 설정했습니다.

따라서, 상기 요인에 의해 예측 기간중, 유럽이 시장을 독점할 것으로 예상됩니다.

P2G(Power to Gas) 산업 개요

P2G(Power to Gas) 시장은 그 성격상 적당히 통합되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

조사의 전제조건과 시장 정의

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2027년까지 시장 규모와 수요 예측(단위: 100만 달러)

지역별·용량에 의한 기존 발전소 일람

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

억제요인

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

기술별

P2H(Power to Hydrogen)

P2M(Power to Methane)

용량별(정성 분석만)

1,000KW 이상

100-1,000KW

100KW 이하

최종 사용자

유틸리티

산업용

상업

지역별

북미

유럽

아시아태평양

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Nel ASA

Sempra Energy

GRT Gaz SA

MAN Energy Solutions

Sunfire GmbH

Ineratec GmbH

Electrochaea GmbH

MicroPyros BioEnerTec GmbH

Siemens Energy AG

Hitachi Zosen Inova AG

AquahydreX Inc.

제7장 시장 기회와 앞으로의 동향

JHS

영문 목차

영문목차

The Power to Gas Market is expected to register a CAGR of greater than 50% during the forecast period.

COVID-19 negatively impacted the market in 2020. Presently, the market has reached pre-pandemic levels.

Key Highlights

Over the long term, the major driving factors of the market were increasing decarbonization to reduce the impact of greenhouse gases on the climate and reduction in the cost of electricity with the advent of renewable energy sources.

On the flip side, high initial costs to set up power-to-gas plants and the need for additional transportation pipeline infrastructure in underdeveloped and developed economies for methane or hydrogen is expected to slow down the market growth.

Increasing initiatives in developing the infrastructure of green hydrogen in the emerging markets are expected to create vital opportunities for the power-to-gas market players soon.

Europe is expected to dominate the power to gas market, with most of the demand coming from countries like Germany, France, and Spain.

Power to Gas Market Trends

Power-to-hydrogen to be the Fastest-growing Segment

Power-to-hydrogen includes a range of technologies that utilize electricity to perform electrolysis and split water into hydrogen and oxygen. When hydrogen is manufactured using renewable energy, it is called green hydrogen and can be used to store, transport, and utilize renewable energy. This helps minimize variable renewable energy curtailment from sources such as wind and solar, provides long-term storage and grid-balancing services via electrolyzers, and uses existing gas transmission infrastructure for transporting energy in the form of green hydrogen over long distances.

Additionally, nearly 350 projects with an aggregate capacity of 54 GW are currently under development and expected to come online by 2030; 40 other projects accounting for almost 35 GW capacity are in the early stages of development. If all planned projects are commissioned within time, it is expected that by 2030, the global green hydrogen supply from electrolyzers could reach 8 million tons per year.

The green hydrogen produced by electrolyzers can also be used directly as a fuel for transport, replacing oil in light vehicles, railways, and marine applications, or as a feedstock for industrial applications. Green hydrogen fuel cells can also be used for energy storage.

The technology offers advantages over current energy storage technologies, such as higher power storage capacity and longer discharge times. Hydrogen can also be injected directly into natural gas grids. However, due to safety and technical concerns, hydrogen injection is subject to regulations and varies from country to country. For instance, the limit of hydrogen in natural gas grids in the United Kingdom is 0.1%, while it is 12% in the Netherlands.

Due to the falling costs of renewable energy technologies like solar and wind, energy storage technologies like power-to-gas (PtG) technology are becoming increasingly attractive. The installed capacity of commercial electrolyzer systems has been growing steadily over the past few years. There are only a few commercially viable water electrolysis technologies, and the two most widely used technologies are alkaline water electrolysis (AWE) and proton exchange membrane (PEM) electrolysis.

Therefore, owing to the above factors, the power-to-hydrogen segment is expected to be the fastest-growing segment over the forecast period.

Europe to Dominate the Market

As of 2021, Europe was one of the largest regions in the power-to-gas market. Increasing investments and funding grants by governments in the region are driving the market.

In 2021, according to the European Commission, the refinery sector accounted for 48% of the hydrogen consumption, followed by the fertilizers and chemical sectors.

Germany is one of the major countries in the European power-to-gas market. As of 2020, Germany was home to around 40 small power-to-gas pilot projects that harnessed surplus green power, mainly from wind and solar projects, to carry out electrolysis by splitting water into oxygen and hydrogen to produce zero-carbon fuel.

According to Deutscher Verein des Gas- und Wasserfaches (DVGW), Germany is planning to build a power-to-gas capacity of 5 GW by 2023 and 40 GW by 2050 as it seeks to develop zero-carbon fuels for homes, factories, and vehicles. Thus, such government targets are likely to boost the power-to-gas market in the region during the forecast period.

In January 2022, ThyssenKrupp Uhde Chlorine Engineers signed a supply contract with Shell for the large-scale project Hydrogen Holland I in Rotterdam, Netherlands port. Under the agreement, ThyssenKrupp Uhde will engineer, procure, and fabricate a 200 MW electrolysis plant based on their large-scale 20 MW alkaline water electrolysis module. The first construction work for the electrolysers that has begun with Shell's final investment decision (FID) to build the project is expected at the end of 2022, after which the intended start of production will be in 2024.

After the commencement of the Russian-Ukraine war, as a part of the passed in May 2022, the EU aims to reduce overreliance on Russian gas imports by increasing renewable energy generation. One of the primary tenets of the plan is the 'hydrogen accelerator' strategy, which aims to produce 10 million tonnes and import 10 million tonnes of renewable hydrogen into the EU by 2030. As green hydrogen is renewable, the plan aims to support the EU's energy transition and help in the decarbonisation of many heavy industries.

SImilarly, in May 2022, the EU set up a target with European electrolyzer manufacturers and set up an industry-wide target of increasing Europe's electrolyser manufacturing capacity from 1.75 GW/year to nearly ten times to 17.5 GW per year by 2025.

Thus, owing to the above factors, Europe is expected to dominate the market during the forecast period.

Power to Gas Industry Overview

The power-to-gas market is moderately consolidated in nature. Some of the major players in the market (in no particular order) include Nel ASA, Sempra Energy, GRT Gaz SA, MAN Energy Solutions, and Sunfire GmbH.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Study Assumptions and Market Definition

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD million till 2027

4.3 List of Existing Power-to-gas Plants by Region and Capacity

4.4 Recent Trends and Developments

4.5 Government Policies and Regulations

4.6 Market Dynamics

4.6.1 Drivers

4.6.2 Restraints

4.7 Supply Chain Analysis

4.8 Porter's Five Forces Analysis

4.8.1 Bargaining Power of Suppliers

4.8.2 Bargaining Power of Consumers

4.8.3 Threat of New Entrants

4.8.4 Threat of Substitute Products and Services

4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Technology

5.1.1 Power-to-Hydrogen

5.1.2 Power-to-Methane

5.2 By Capacity (Qualitative Analysis Only)

5.2.1 More than 1000 KW

5.2.2 100 to 1000 KW

5.2.3 Less than 100 KW

5.3 y End-User

5.3.1 Utilities

5.3.2 Industrial

5.3.3 Commercial

5.4 By Geography

5.4.1 North America

5.4.2 Europe

5.4.3 Asia-Pacific

5.4.4 South America

5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements